SAN FRANCISCO TRENDS OFFICE MARKET REPORT 2Nd Quarter 2009

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mckesson HBOC, Inc. Securities Litigation 99-CV-20743-US District

US District Court Civil Docket as of February 8, 2013 Retrieved from the court on February 11, 2013 U.S. District Court California Northern District (San Jose) CIVIL DOCKET FOR CASE #: 5:99-cv-20743-RMW Aronson, et al v. McKesson HBOC, Inc., et al Date Filed: 04/28/1999 Assigned to: Judge Ronald M. Whyte Date Terminated: 03/26/2008 Referred to: Magistrate Judge Patricia V. Trumbull Jury Demand: Both Demand: $0 Nature of Suit: 850 Case in other court: Ninth Circuit, 06-15987 Securities/Commodities Cause: 15:78m(a) Securities Exchange Act Jurisdiction: Federal Question Plaintiff Andrew Aronson represented by D. Brian Hufford on behalf of himself and all others Pomerantz Haudek Block Grossman & similarly situated Gross LLP 100 Park Ave 26th Flr New York, NY 10017-5516 (212) 661-1100 LEAD ATTORNEY ATTORNEY TO BE NOTICED Daniel L. Berger Bernstein Litowitz Berger & Grossmann 1285 Avenue of the Americas 33rd Flr New York, NY 10019 (212) 554-1400 LEAD ATTORNEY ATTORNEY TO BE NOTICED Gerald J. Rodos Barrack Rodos & Bacine 2001 Market St 3300 Two Commerce Sq Philadelphia, PA 19103 (215) 963-0600 Email: [email protected] LEAD ATTORNEY ATTORNEY TO BE NOTICED Jeffrey W. Golan Barrack Rodos & Bacine 2001 Market St 3300 Two Commerce Sq Philadelphia, PA 19103 (215) 963-0600 LEAD ATTORNEY ATTORNEY TO BE NOTICED Joseph J. Tabacco , Jr. Berman DeValerio One California Street Suite 900 San Francisco, CA 94111 415-433-3200 Fax: 415-433-6382 Email: [email protected] LEAD ATTORNEY ATTORNEY TO BE NOTICED Leonard Barrack Barrack Rodos & Bacine 2001 Market St 3300 Two Commerce Sq Philadelphia, PA 19103 (215) 963-0600 Email: [email protected] LEAD ATTORNEY ATTORNEY TO BE NOTICED Max W. -

Entertainment Law Directory

Loyola of Los Angeles Entertainment Law Review Volume 26 Number 2 Article 5 1-1-2006 Entertainment Law Directory Follow this and additional works at: https://digitalcommons.lmu.edu/elr Part of the Law Commons Recommended Citation , Entertainment Law Directory, 26 Loy. L.A. Ent. L. Rev. 287 (2006). Available at: https://digitalcommons.lmu.edu/elr/vol26/iss2/5 This Directory is brought to you for free and open access by the Law Reviews at Digital Commons @ Loyola Marymount University and Loyola Law School. It has been accepted for inclusion in Loyola of Los Angeles Entertainment Law Review by an authorized administrator of Digital Commons@Loyola Marymount University and Loyola Law School. For more information, please contact [email protected]. ENTERTAINMENT LAW DIRECTORY The Loyola of Los Angeles Entertainment Law Review Directory is intended as an information guide to entertainment-oriented law firms and entertainment companies located on the West and East Coasts and in the Midwest. The list was compiled from oral and written information provided to the Review during March 2005. We welcome information from additional firms. There is no charge for placement in this Directory. The Directory is meant to be only a guide. No claims are made regarding the accuracy of the information printed therein. WEST COAST ATTORNEYS AARONSON & AARONSON ................................................... 818-783-3858 16133 Ventura Boulevard, Suite 675 Encino, California 91436 ABRAMS GARFINKEL MARGOLIS BERGSON, LLP ............ 310-300-2900 9229 Sunset Boulevard, Suite 710 Los Angeles, California 90069 AKIN, GUMP, STRAUSS, HAUER & FELD, LLP .................. 310-229-1000 2029 Century Park East, Suite 2400 Los Angeles, California 90067 www.akingump.com ALSCHULER, GROSSMAN, STEIN & KAHAN, LLP ............. -

Engineer's Report Prepared by a Registered Professional Engineer Certified by the State of California.3

SECTION 10: ASSESSMENT ENGINEER’S REPORT Downtown Community Benefit District Including the Historic Financial District and Jackson Square of San Francisco and South Side of Market Street Formed under the California Streets and Highway Code Section 36600 et seq. Property and Business Improvement District Law of 1994, Augmented by Article 15 of the San Francisco Business and Tax Regulations Code DISTRICT ASSESSMENT ENGINEER’S REPORT Prepared by Edward V. Henning California Registered Professional Engineer # 26549 Edward Henning & Associates April 15, 2019 V 3 1 DOWNTOWN COMMUNITY BENEFIT DISTRICT – ENGINEER’S REPORT TABLE OF CONTENTS ENGINEER’S CERTIFICATION ...............................................................................................3 ENGINEER’S REPORT: SECTION A: Legislative and Judicial Review ............................................................4 SECTION B: Programs, Improvements and Activities ..............................................7 SECTION C: District Boundaries ................................................................................9 SECTION D: Proportional Benefits ...........................................................................13 SECTION E: Special and General Benefits ...............................................................13 SECTION F: Program, Improvement and Activity Costs .......................................19 SECTION G: Assessment Methodolgy .......................................................................22 SECTION H: Assessment Roll ....................................................................................25 -

Lit Signature Offices

Discovery | Depositions | Trial LIT SIGNATURE OFFICES A San Diego M Phoenix First Allied Plaza Grand Rapids Camelback Commons 655 W. Broadway, Suite 880 River House 4742 N. 24th Street, Suite 300 San Diego, CA 92101 333 Bridge Street NW #215 Phoenix, AZ 85016 Grand Rapids, MI 49504 Santa Ana C Park Center 400 Harper Woods Bakersfield 400 N. Tustin Avenue, Suite 350 20416 Harper Avenue 19237 Flightpath Way, Suite 100 Santa Ana, CA 92705 Harper Woods, MI 48225 Bakersfield, CA 93308 Santa Rosa N Fresno 3510 Unocal Place, Suite 115 Carson City 1326 W. Herndon Ave., Suite 101 Santa Rosa, CA 95403 123 W. Nye Lane, Suite 707 Fresno, CA 93711 Carson City, NV 89706 Ventura Los Angeles 3295 Telegraph Road (First Floor) Las Vegas One California Plaza Ventura, CA 93003 C H 300 South Grand Ave. Suite 3840 3770 Howard Hughes Pkwy, Los Angeles, CA 90071 Visalia Suite 300 2348 W. Whitendale Las Vegas, NV 89169 Los Angeles - Commerce Suite A Bank of the West Visalia, CA 93277 Reno 6055 E. Washington Blvd. 8th Floor 151 Country Estates Circle Los Angeles, CA 90040 San Francisco Reno, NV 89511 Two Embarcadero Center Ontario Suite 1500 N J Inland Empire San Francisco, CA 94111 Cherry Hill 3800 Concours Street Woodland Falls Corp. Center Empire Tower IV, Suite 320 F 200 Lake Drive East, Suite 103 Ontario, CA 91764 Fort Pierce Cherry Hill, NJ 08002 311 So. 2nd Street, Suite 102-C Palm Desert Fort Pierce, FL 34950 N Y One El Paseo Plaza One Penn Plaza West Building, Suite 202 Okeechobee Suite 4205 74199 El Paseo Drive 416 NW Third Street New York, NY 10119 Palm Desert, CA 92260 Okeechobee, FL 34972 P Palm Springs Stuart Philadelphia 777 E. -

In the Supreme Court of the State of California ______

Case No. S244737 IN THE SUPREME COURT OF THE STATE OF CALIFORNIA ______________________________________________________ MONTROSE CHEMICAL CORPORATION OF CALIFORNIA, Petitioner, v. SUPERIOR COURT OF THE STATE OF CALIFORNIA, COUNTY OF LOS ANGELES, Respondent; CANADIAN UNIVERSAL INSURANCE COMPANY, INC., et al. Real Parties in Interest _____________________________________________________________ After a Decision by the Court of Appeal, Second Appellate District, Division Three Civil Case No. B272387 Petition from the Superior Court of the State of California For the County of Los Angeles Case No. BC005158, Honorable Elihu Berle, Presiding _____________________________________________________________ JOINDER TO ANSWER OF CONTINENTAL CASUALTY COMPANY AND COLUMBIA CASUALTY COMPANY TO PETITION FOR REVIEW OF MONTROSE CHEMICAL CORPORATION OF CALIFORNIA ___________________________________________________________ Lewis Brisbois Bisgaard & Smith LLP BUDD LARNER, P.C. Jordon E. Harriman (SBN 117150) Michael J. Balch, Esq. [email protected] [email protected] 633 West 5th Street, Suite 4000 150 John F. Kennedy Parkway Los Angeles, California 90071 Short Hills, NJ 07078-2703 Telephone: 213.250.1800 Telephone: 973.379.4800 Facsimile: 213.250.7900 Facsimile: 973.379.7734 Attorneys for General Reinsurance Corporation and North Star Reinsurance Corporation 4849-3570-3890.1 PLEASE TAKE NOTICE that General Reinsurance Corporation and North Star Reinsurance Corporation join in Continental Casualty Company and Columbia Casualty Company’s Answer -

City and County of San Francisco

PRELIMINARY OFFICIAL STATEMENT DATED JANUARY 30, 2019 NEW ISSUE - BOOK-ENTRY ONLY RATING: Fitch: “AA+” See “RATING” herein. In the opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however to certain qualifications described in this Official Statement, under existing law, the interest on the Bonds is exempt from California personal income taxes. Interest on the Bonds is not intended to be exempt from federal income taxation. Bond Counsel expresses no opinion regarding other federal or State tax consequences relating to the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See “TAX MATTERS” herein. CITY AND COUNTY OF SAN FRANCISCO COMMUNITY FACILITIES DISTRICT NO. 2014-1 (TRANSBAY TRANSIT CENTER) $31,940,000* $152,205,000* Special Tax Bonds, Series 2019A Special Tax Bonds, Series 2019B (Federally Taxable) (Federally Taxable – Green Bonds) Dated: Date of Delivery Due: September 1, as shown on inside cover This cover page contains certain information for general reference only. It is not intended to be a summary of the security or terms of this issue. Investors must read the entire Official Statement to obtain information essential to making an informed investment decision. The City and County of San Francisco, California (the “City”) on behalf of the City and County of San Francisco Community Facilities District No. 2014-1 (Transbay Transit Center) (the “District”) will be issuing Special Tax Bonds, Series 2019A (Federally Taxable) (the “2019A Bonds”) and Special Tax Bonds, Series 2019B (Federally Taxable – Green Bonds) (the “2019B Bonds” and, together with the 2019A Bonds, the “2019 Bonds”). -

Modern Skyline

MODERN SKYLINE Architecture and Development in the Financial District and Bunker Hill area Docent Reference Manual Revised February 2016 Original manual by intern Heather Rigby, 2001. Subsequent revisions by LA Conservancy staff and volunteers. All rights reserved Table of Contents About the tour 3 Gas Company Building 4 Building on the Past: The Architecture of Additions 5 One Bunker Hill (Southern California Edison) 6 Biltmore Tower 7 Tom Bradley Wing, Central Library 8 Maguire Gardens, Central Library 10 US Bank Tower (Library Tower) 11 Bunker Hill Steps 13 Citigroup Center 14 Cultural Landscapes 14 550 South Hope Street (California Bank and Trust) 16 611 Place (Crocker Citizens-Plaza/AT&T) 17 Aon Center (UCB Building/First Interstate Tower) 18 Modern Building and Preservation 19 A Visual Timeline 19 Adaptive Reuse 20 Downtown Standard (Superior Oil Building) 21 Tax Credits 22 The Pegasus (General Petroleum Building) 23 AC Martin and Contemporary Downtown 24 Figueroa at Wilshire (Sanwa Bank Plaza) 24 Destruction and Development 25 City National Plaza (ARCO Plaza) 26 Richfield Tower 28 Manulife Plaza 29 Union Bank Plaza 30 Westin Bonaventure Hotel 31 History of Bunker Hill 33 Four Hundred South Hope (Mellon Bank/O’Melveny and Myers) 34 Bank of America Plaza (Security Pacific Plaza) 35 Stuart M. Ketchum Downtown Y.M.C.A 37 Wells Fargo Plaza (Crocker Center) 38 California Plaza 39 Uptown Rocker 40 Untitled or Bell Communications Across the Globe 40 Appendix A: A Short Summary of Modern Architectural Styles 41 Appendix B: Los Angeles Building Height Limits 42 Appendix C: A Short History of Los Angeles 43 Updated February 2016 Page 2 ABOUT THE TOUR This tour covers some of the newer portions of the downtown Los Angeles skyline. -

Before the Public Utilities Commission of The

FILED 12/22/20 BEFORE THE PUBLIC UTILITIES COMMISSION 01:41 PM OF THE STATE OF CALIFORNIA Order Instituting Rulemaking to Continue Electric Integrated Resource Planning and Rulemaking 20-05-003 Related Procurement Processes. (Filed May 7, 2020) CERTIFICATE OF SERVICE I, the undersigned, state that I am a citizen of the United States and am employed in the City and County of San Francisco; that I am over the age of eighteen (18) years and not a party to the within cause; and that my business address is Pacific Gas and Electric Company, Law Department, B30A, 77 Beale Street, San Francisco, California 94105. On December 22, 2020, I served by electronic mail a true copy of the following document onto the official service list for R.20-05-003: COMMENTS OF PACIFIC GAS AND ELECTRIC COMPANY (U 39 E) ON EVALUATION REPORT OF THE INTEGRATED RESOURCE PLANNING PROCESS I certify and declare under penalty of perjury under the laws of the State of California that the foregoing is true and correct. Executed on December 22, 2020 in Oakland, California. /s/ Tauvela V. U'u TAUVELA V. U'U 1 / 24 CPUC - Service Lists - R2005003 Page 1 of 19 CPUC Home CALIFORNIA PUBLIC UTILITIES COMMISSION Service Lists PROCEEDING: R2005003 - CPUC - OIR TO CONTIN FILER: CPUC LIST NAME: LIST LAST CHANGED: DECEMBER 17, 2020 Download the Comma-delimited File About Comma-delimited Files Back to Service Lists Index Parties BARBARA BOSWELL BARBARA BOSWELL INTERIM CEO CITY OF PALMDALE CLEAN ENERGY ALLIANCE EMAIL ONLY EMAIL ONLY EMAIL ONLY, CA 00000 EMAIL ONLY, CA 00000 FOR: CITY OF PALMDALE FOR: CLEAN ENERGY ALLIANCE BARBARA BOSWELL BARBARA BOSWELL SANTA BARBARA CLEAN ENERGY CITY OF POMONA EMAIL ONLY EMAIL ONLY EMAIL ONLY, CA 00000 EMAIL ONLY, CA 00000 FOR: SANTA BARBARA CLEAN ENERGY FOR: CITY OF POMONA JOHN W. -

Csac Board of Directors

CSAC BOARD OF DIRECTORS BRIEFING MATERIALS Thursday, September 2nd, 2021 10:00 a.m. – 1:00 p.m. Online Meeting Via Zoom: https:https://us02web.zoom.us/j/89224073679?pwd=WEdpZUYrSHUvSW95MGZyTXZnUGhRZz09 Phone: (669) 900-6833 | Meeting ID: 892 2407 3679| Password: 679285 California State Association of Counties CALIFORNIA STATE ASSOCIATION OF COUNTIES BOARD OF DIRECTORS Thursday, September 2, 2021 | 10:00 am – 1:15 pm Zoom: https://us02web.zoom.us/j/89224073679?pwd=WEdpZUYrSHUvSW95MGZyTXZnUGhRZz09 Conference Line: (669) 900-6833 | Meeting ID: 892 2407 3679 | Password: 679285 AGENDA Presiding: James Gore, President THURSDAY, SEPTEMBER 2 10:00 AM PROCEDURAL ITEMS 1. Pledge of Allegiance Page 1 2. Roll Call Page 2-3 SPECIAL ITEMS 3. Executive Director’s Report Page 4 ➢ Graham Knaus | Executive Director 4. Rural County Representatives of California (RCRC) Update ➢ Patrick Blacklock | President & CEO 5. Opioid Litigation Update Page 5 ➢ John Fiske | Shareholder, Baron & Budd, P.C. ACTION ITEMS 6. Approval of Minutes from April 22, 2021 Page 6-13 INFORMATION AND DISCUSSION ITEMS 7. Minute Mics: Board of Directors Roundtable ➢ What’s going on in your county – in one minute? 8. CSAC Legislative Update Page 14-16 ➢ Darby Kernan, Deputy Executive Director, Legislative Affairs Administration of Justice • Josh Gauger | Legislative Representative Agriculture, Environment & Natural Resources • Catherine Freeman | Legislative Representative Government, Finance & Administration • Geoff Neill | Legislative Representative • Ryan Souza | Legislative Representative Health & Human Services • Farrah McDaid Ting | Legislative Representative • Justin Garrett | Legislative Representative Housing, Land Use & Transportation • Chris Lee | Legislative Representative 9. CSAC Finance Corporation Report Page 17-28 ➢ Supervisor Leonard Moty | President, CSAC FC ➢ Alan Fernandes | Chief Executive Officers, CSAC FC ➢ David Andrews | Director, International Homeland Security, IEM 10. -

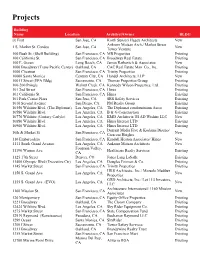

View Projects

Projects Building Name Location Architect/Owner BLDG @ First San Jose, CA Korth Sunseri Hagey Architects New Ankrom Moisan Arch./ Market Street 1 S. Market St. Condos San Jose, CA New Tower Venture 100 Bush St. (Shell Building) San Francisco, CA MB Properties Existing 100 California St. San Francisco, CA Broadway Real Estate Existing 100 E. Ocean Long Beach, CA James Ratkovich & Associates New 1000 Broadway (Trans Pacific Center) Oakland, CA CAC Real Estate Man. Co., Inc. Existing 1000 Chestnut San Francisco, CA Trinity Properties Existing 10000 Santa Monica Century City, CA Handel Architects, LLP New 1001 I Street (EPA Bldg) Sacramento, CA Thomas Properties Group Existing 100-200 Pringle Walnut Creek, CA Kennedy Wilson Properties, Ltd. Existing 101 2nd Street San Francisco, CA Hines Existing 101 California St. San Francisco, CA Hines Existing 101 Park Center Plaza San Jose, CA SRS Safety Services Existing 1010 Second Avenue San Diego, CA PM Realty Group Existing 10350 Wilshire Blvd. (The Diplomat) Los Angeles, CA The Diplomat condominium Assoc Existing 10580 Wilshire Blvd. Los Angeles, CA B & G Construction Existing 10776 Wilshire (Century Carlyle) Los Angeles, CA KMD Architects/ El AD Wishire LLC New 10880 Wilshire Blvd. Los Angeles, CA Hines Interest LTD Existing 10960 Wilshire Blvd. Los Angeles, CA Hines Interest LTD Existing Durrant Media Five & Kodama Diseno/ 10th & Market St. San Francisco, CA New Crescent Heights 110 Embarcadero San Francisco, CA Kendall Heaton Associates/ Hines New 1111 South Grand Avenue Los Angeles, CA Ankrom Moisan Architects New Fountain Valley, 11190 Warner Ave. Healthcare Realty Services Existing CA 1125 17th Street Denver, CO Jones Lang LaSalle Existing 11400 Olympic Blvd (Executive Ctr) Los Angeles, CA Douglas Emmett & Co. -

OMA Bulletin Cypress Security, LLC Is Published Bi-Monthly

MARCH/APRIL 2007 www.bomasf.org BOMA San Francisco advances the commercial real estate industry through advocacy, professional development, and information exchange “The BOMA CareerCenter BOMA Addresses Career Management is an excellent resource for reaching people interested in working in property Needs of Real Estate Professionals— management. I posted an opening Unveils BOMA SF CareerCenter & New Task Force for an Administrative Assistant position at Embarcadero Center to Promote Real Estate Management Careers and received resumes from three qualified candidates in the first week.” Kirsten Walraven Young, RPA, FMA Stephen L. Austin, RPA CB Richard Ellis at PG&E Regional Property Manager Boston Properties OMA San Francisco has been doing use of search agents that notify them a lot to support, and call attention when new candidates who match their to the career criteria have posted their On the Inside management needs of résumés. Job seekers benefit commercial real estate from free and confidential Bprofessionals. Responding to résumé posting, weekly, MEMBERSHIP CAMPAIGN increased demand by automated email notification UPDATE employers and recruiters for of new job listings, the ability access to highly qualified to save jobs for later review ••• 4 ••• property managers, we and related career unveiled the BOMA SF development services. CALENDAR CareerCenter in late February. This interactive job Another key element of the ••• 8 ••• board – found at CareerCenter is the dedicated http://careers.bomasf.org – Customer Support Center. We BOMA YP enables employers and have partnered with recruiters to reach a wide Kirsten Walraven, RPA, FMA Boxwood Technology, the ••• 9 ••• CB Richard Ellis at range of commercial real leading provider of online Pacific Gas & Electric estate management career center technology and 7TH ANNUAL PAC candidates. -

Final Official Statement, It Must Be Available from the MSRB

NEW ISSUE - BOOK-ENTRY ONLY RATING: Fitch: “AA+” See “RATING” herein. In the opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however to certain qualifications described in this Official Statement, under existing law, the interest on the Bonds is exempt from California personal income taxes. Interest on the Bonds is not intended to be exempt from federal income taxation. Bond Counsel expresses no opinion regarding other federal or State tax consequences relating to the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See “TAX MATTERS” herein. $81,820,000 CITY AND COUNTY OF SAN FRANCISCO COMMUNITY FACILITIES DISTRICT NO. 2014-1 (TRANSBAY TRANSIT CENTER) SPECIAL TAX BONDS, SERIES 2020B (FEDERALLY TAXABLE – GREEN BONDS) Dated: Date of Delivery Due: September 1, as shown on inside cover This cover page contains certain information for general reference only. It is not intended to be a summary of the security or terms of this issue. Investors must read the entire Official Statement to obtain information essential to making an informed investment decision. The City and County of San Francisco, California (the “City”) on behalf of the City and County of San Francisco Community Facilities District No. 2014-1 (Transbay Transit Center) (the “District”) will be issuing its Special Tax Bonds, Series 2020B (Federally Taxable – Green Bonds) (the “2020B Bonds”). The City has not yet determined whether a Series 2020A will be issued. The 2020B Bonds are being issued pursuant to a Fiscal Agent Agreement, dated as of November 1, 2017, as supplemented, including by the Second Supplement to Fiscal Agent Agreement, dated as of May 1, 2020 (collectively, the “Fiscal Agent Agreement”), by and between the City and Zions Bancorporation, National Association, as fiscal agent (the “Fiscal Agent”), and will be secured as described herein.