Decision Paper on Cancellation of Generating Unit Agreements in Northern Ireland

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Completed Acquisition by AES Ballylumford Holdings Limited of Premier Power Limited

Completed acquisition by AES Ballylumford Holdings Limited of Premier Power Limited ME/4688/10 The OFT’s decision on reference under section 22(1) given on 24 November 2010. Full text of decision published 14 January 2011. Please note that the square brackets indicate figures or text which have been deleted or replaced in ranges at the request of the parties or third parties for reasons of commercial confidentiality. PARTIES 1. AES Ballylumford Holdings Limited (ABHL) is wholly owned by the AES Corporation (AES), a global power company. AES controls AES Kilroot Power Limited (KPL) which operates the Kilroot power station in Northern Ireland. KPL's turnover in 2009 was £[ ]million. 2. Premier Power Limited (PPL) owns the gas-fired Ballylumford power station in County Antrim, Northern Ireland. PPL's UK turnover in the financial year to 31 December 2009 was £[ ] million. TRANSACTION 3. The acquisition by ABHL of PPL was completed on 11 August 2010 for a total consideration of £102 million. 4. Completion of the transaction was conditional on the receipt of comfort letters from the Northern Ireland Authority for Utility Regulation ('the Utility Regulator') and the Department of Enterprise, Trade and Investment (DETI). These comfort letters essentially confirmed that 'change of control' provisions were not going to trigger the use of revocation powers under relevant generation licences. 1 5. The administrative and statutory deadlines for the OFT to make a decision on this transaction expire on 24 November and 10 December respectively. JURISDICTION 6. As a result of this transaction ABHL and PPL have ceased to be distinct. -

Energy Retail Report 2009

Energy Retail Report 2009 1 Table of Contents Introduction ......................................................................................................................................................... 3 Questions to readers .......................................................................................................................................... 5 PART ONE: BACKGROUND ............................................................................................................................ 7 1. Overview of the electricity and gas sectors .............................................................................................. 7 1.1. The Utility Regulator ........................................................................................................... 7 1.2. Price Controls - A key function in protecting energy consumers ..................................... 10 1.3. Structure of the Northern Ireland energy sector ............................................................... 13 1.4. Wholesale markets ........................................................................................................... 20 1.5. Networks ........................................................................................................................... 24 1.6. Supply sector .................................................................................................................... 28 PART TWO: CORE RETAIL INFORMATION ................................................................................................ -

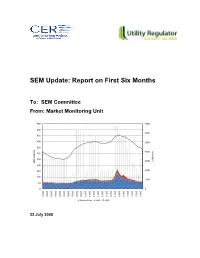

SEM Update: Report on First Six Months

SEM Update: Report on First Six Months To: SEM Committee From: Market Monitoring Unit 550 7000 500 6000 450 400 5000 350 4000 300 MW €/MWhr 250 3000 LOAD SMP 200 150 2000 100 1000 50 0 0 00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00 18:00 19:00 20:00 21:00 22:00 23:00 Shadow Price Uplift LOAD 22 July 2008 1. INTRODUCTION This is the first six‐month report of the Single Electricity Market (SEM) prepared by the Market Monitoring Unit (MMU). The aim of this report is to provide an unbiased assessment of the market. This report covers the first six months of market activity since SEM Go‐Live (1 November 2007 to 3o April 2008) and gives a statistical overview of the market, providing analysis and comparison of market prices to selected indices. The impact of carbon increases on prices and generator offers is also covered, along with an overview of the trends in commercial offers submitted by generators, generator market schedules, peak prices and some coverage of specific events. Constrained‐on and off volumes are also presented and discussed for selected units. Disclaimer: This report is largely data‐oriented. It is largely based on data provided to the MMU by SEMO (the Market Operator). Although every attempt has been made to ensure all data included in this report correct, the MMU cannot accept responsibility for the accuracy of the data presented in this report. -

Eirgrid Plc Annual Report 2009 Investing for the Future Eirgrid Plc Annual Report 2009 Group OPERATING Structure

EirGrid plc Annual Report 2009 Investing for the Future EirGrid plc EirGrid Annual Report 2009 Annual Report Group OpERATING StrucTURE plc UK Holdings Limited 75% Limited TSO 25% TSO EirGrid plc is a leading energy company committed to delivering high quality services in Ireland and Northern Ireland. The Group includes the EirGrid Transmission System Operator (TSO) business in Ireland; System Operator Northern Ireland (SONI), the licenced TSO in Northern Ireland; and the Single Electricity Market Operator (SEMO) which operates the Single Electricity Market on the island of Ireland. Cover: EirGrid’s East-West Interconnector will connect the Irish power system to the electricity grid in Britain through undersea and underground cables and have a capacity of 500 Megawatts (MW). Pictured here is the Marine Survey Vessel that determined the feasible marine route for the 185km High Voltage Direct Current (HVDC) submarine cable across the Irish Sea. This infrastructure will enable two-way transmission of electricity and is vital to the development of Ireland’s economy and energy security and will facilitate the achievement of national renewable energy targets. EirGrid plc 2009 Annual Report and Accounts Contents Chairperson’s Report 2 Chief Executive’s Report 4 Financial Review 8 Operating Ireland’s Power System 11 Developing Ireland’s Transmission Infrastructure 15 Operating the Single Electricity Market 19 Transmission System Map 21 System Operator for Northern Ireland (SONI) 23 1 Corporate & Social Responsibility 28 Our Customers 30 The Board 32 Organisation Structure 36 Executive Team 38 Financial Statements 41 EirGrid plc 2009 Annual Report and Accounts CHAIRPERSON’S REPORT all it needs public understanding and support, so that projects can be delivered across Ireland in a timely fashion and to enable Ireland to utilise its rich renewable energy resources.