Basic Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

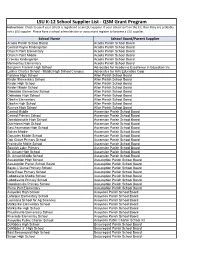

LSU Supplier List K-12 Schools

LSU K-12 School Supplier List - QSM Grant Program Instructions: Check to see if your school is registered as an LSU supplier. If your school isn't on the list, then they are probably not a LSU supplier. Please have a school administrator or accountant register to become a LSU supplier. School Name School Board/Parent Supplier Acadia Parish School Board Acadia Parish School Board Central Rayne Kindergarten Acadia Parish School Board Church Point Elementary Acadia Parish School Board Church Point Middle Acadia Parish School Board Crowley Kindergarten Acadia Parish School Board Mermentau Elementary Acadia Parish School Board Benjamin Franklin High School Advocates for Academic Excellence in Education Inc Lusher Charter School - Middle/High School Campus Advocates for Arts Education Corp Fairview High School Allen Parish School Board Kinder Elementary School Allen Parish School Board Kinder High School Allen Parish School Board Kinder Middle School Allen Parish School Board Oakedale Elementary School Allen Parish School Board Oakedale High School Allen Parish School Board Oberlin Elementary Allen Parish School Board Oberlin High School Allen Parish School Board Reeves High School Allen Parish School Board Central Middle Ascension Parish School Board Central Primary School Ascension Parish School Board Donaldsonville High School Ascension Parish School Board Dutchtown High School Ascension Parish School Board East Ascension High School Ascension Parish School Board Galvez Middle Ascension Parish School Board Gonzales Middel School Ascension Parish School Board Oak Grove Primary School Ascension Parish School Board Prairieville Midlle School Ascension Parish School Board Spanish Lake Primary Ascension Parish School Board St. Amant High School Ascension Parish School Board St. -

Name Abbeville High School Academy of Our Lady

NAME ABBEVILLE HIGH SCHOOL ACADEMY OF OUR LADY (GIRLS) (C ACADEMY OF THE SACRED HEART (G ACADEMY OF THE SACRED HEART (G ACADIANA HIGH SCHOOL AIRLINE HIGH SCHOOL ALBANY HIGH SCHOOL ALEXANDRIA SENIOR HIGH SCHOOL ALFRED M. BARBE HIGH SCHOOL AMITE HIGH SCHOOL ANACOCO HIGH SCHOOL ANGELS ACADEMY ARCADIA HIGH SCHOOL ARCHBISHOP CHAPELLE HIGH SCHOO ARCHBISHOP HANNAN HIGH SCHOOL( ARCHBISHOP RUMMEL SR. HIGH SCH ARCHBISHOP SHAW SR. HIGH SCHOO ARLINGTON PREPARATORY ACADEMY ASCENSION CHRISTIAN HIGH SCHOO ASCENSION DIOCESAN REGIONAL SC ASCENSION EPISCOPAL SCHOOL (AS ASSEMBLY CHRISTIAN SCHOOL (AG) ASSUMPTION HIGH SCHOOL ATLANTA SCHOOL AVOYELLES HIGH SCHOOL BAKER HIGH SCHOOL BASILE HIGH SCHOOL BASTROP HIGH SCHOOL BATON ROUGE INTERNATIONAL SCHOOL BATON ROUGE MAGNET HIGH SCHOOL BEAU CHENE HIGH SCHOOL BEEKMAN CHARTER SCHOOL BELAIRE HIGH SCHOOL BELL CITY HIGH SCHOOL BELLE CHASSE HIGH SCHOOL BENJAMIN FRANKLIN HIGH SCHOOL BEN'S FORD CHRISTIAN SCHOOL (B BENTON HIGH SCHOOL BERCHMANS ACADEMY OF THE SACRED HEART (C) BERWICK HIGH SCHOOL BETHANY CHRISTIAN SCHOOL BETHEL CHRISTIAN SCHOOL BETHEL CHRISTIAN SCHOOL (B) BISHOP MCMANUS SCHOOL BLOCK HIGH SCHOOL BOGALUSA HIGH SCHOOL BOLTON HIGH SCHOOL BONNABEL MAGNET ACADEMY HIGH S BOOKER T. WASHINGTON NEW TECHN BOSSIER HIGH SCHOOL BREAUX BRIDGE HIGH SCHOOL BRIARFIELD ACADEMY BRIGHTER HORIZON SCHOOL OF BAT BRIGHTON SCHOOL BROADMOOR SENIOR HIGH SCHOOL BROTHER MARTIN SR. HIGH SCHOOL BRUSLY HIGH SCHOOL BUCKEYE HIGH SCHOOL BUNKIE HIGH SCHOOL C.E. BYRD HIGH SCHOOL CABRINI HIGH SCHOOL (GIRLS) (C CADDO PARISH MAGNET HIGH SCHOO CALDWELL -

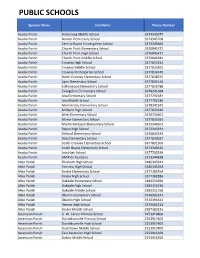

Public Schools

PUBLIC SCHOOLS Sponsor Name Site Name Phone Number Acadia Parish Armstrong Middle School 3373343377 Acadia Parish Branch Elementary School 3373345708 Acadia Parish Central Rayne Kindergarten School 3373343669 Acadia Parish Church Point Elementary School 3376845722 Acadia Parish Church Point High School 3376845472 Acadia Parish Church Point Middle School 3376846381 Acadia Parish Crowley High School 3377835313 Acadia Parish Crowley Middle School 3377835305 Acadia Parish Crowley Kindergarten School 3377834670 Acadia Parish North Crowley Elementary School 3377838755 Acadia Parish Egan Elementary School 3377834148 Acadia Parish Estherwood Elementary School 3377836788 Acadia Parish Evangeline Elementary School 3378241368 Acadia Parish Iota Elementary School 3377792581 Acadia Parish Iota Middle School 3377792536 Acadia Parish Mermentau Elementary School 3378241943 Acadia Parish Midland High School 3377833310 Acadia Parish Mire Elementary School 3378736602 Acadia Parish Morse Elementary School 3377835391 Acadia Parish Martin Petitjean Elementary School 3373349501 Acadia Parish Rayne High School 3373343691 Acadia Parish Richard Elementary School 3376843339 Acadia Parish Ross Elementary School 3377830927 Acadia Parish South Crowley Elementary School 3377831300 Acadia Parish South Rayne Elementary School 3373343610 Acadia Parish Iota High School 3377792534 Acadia Parish AMIKids Acadiana 3373344838 Allen Parish Elizabeth High School 3186345341 Allen Parish Fairview High School 3186345354 Allen Parish Kinder Elementary School 3377382454 Allen Parish -

School State 11TH STREET ALTERNATIVE SCHOOL KY 12TH

School State 11TH STREET ALTERNATIVE SCHOOL KY 12TH STREET ACADEMY NC 21ST CENTURY ALTERNATIVE MO 21ST CENTURY COMMUNITY SCHOOLHOUSE OR 21ST CENTURY CYBER CS PA 270 HOPKINS ALC MN 270 HOPKINS ALT. PRG - OFF CAMPUS MN 270 HOPKINS HS ALC MN 271 KENNEDY ALC MN 271 MINDQUEST OLL MN 271 SHAPE ALC MN 276 MINNETONKA HS ALC MN 276 MINNETONKA SR. ALC MN 276-MINNETONKA RSR-ALC MN 279 IS ALC MN 279 SR HI ALC MN 281 HIGHVIEW ALC MN 281 ROBBINSDALE TASC ALC MN 281 WINNETKA LEARNING CTR. ALC MN 3-6 PROG (BNTFL HIGH) UT 3-6 PROG (CLRFLD HIGH) UT 3-B DENTENTION CENTER ID 622 ALT MID./HIGH SCHOOL MN 917 FARMINGTON HS. MN 917 HASTINGS HIGH SCHOOL MN 917 LAKEVILLE SR. HIGH MN 917 SIBLEY HIGH SCHOOL MN 917 SIMLEY HIGH SCHOOL SP. ED. MN A & M CONS H S TX A B SHEPARD HIGH SCH (CAMPUS) IL A C E ALTER TX A C FLORA HIGH SC A C JONES HIGH SCHOOL TX A C REYNOLDS HIGH NC A CROSBY KENNETT SR HIGH NH A E P TX A G WEST BLACK HILLS HIGH SCHOOL WA A I M TX A I M S CTR H S TX A J MOORE ACAD TX A L BROWN HIGH NC A L P H A CAMPUS TX A L P H A CAMPUS TX A MACEO SMITH H S TX A P FATHEREE VOC TECH SCHOOL MS A. C. E. AZ A. C. E. S. CT A. CRAWFORD MOSLEY HIGH SCHOOL FL A. D. HARRIS HIGH SCHOOL FL A. -

Calcasieu Parish School Board Table of Contents

CALCASIEU PUCE PARISH SCHOOE m FILE) BOARD LAKE CHARLES, LOUISIANA COMPREHENSIVE ANNUAL FINANCIAL REPORT Under provisions of state law, this report is a public document A copy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and where appropriate, at the office of the parish clerk of court. Release Dat FOR THE FISCAL YEAR JULY 1, 2004 -JUNE 30, 2005 Prepared by Department of Management and Finance Calcasieu Parish School Board Table of Contents INTRODUCTORY SECTION Transmittal Letter i-ix GFOA Certificate of Achievement for Excellence in Financial Reporting xi ASBO Certificate of Excellence in Financial Reporting xii Calcasieu Parish School Board Officials xiii Organization Chart xiv FINANCIAL SECTION Statement Independent Auditors'Report 1-2 Required Supplemental Information Management's Discussion and Analysis (MD&A) 3-15 Basic Financial Statements: Government-wide Financial Statements (GWFS) Statement of Net Assets A 17 Statement of Activities B 18-19 Fund Financial Statements (FFS) Governmental Funds Balance Sheet C 21 Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets . D 22 Statement of Revenues, Expenditures, and Changes in Fund Balances E 23-24 Reconciliation of the Governmental Funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities F 25 Proprietary Funds Statement of Net Assets G 26 Statement of Revenues, Expenses, -

2020-2021 Ag Teacher Directory

2020-2021 Teachers Directory Table of Contents Louisiana FFA Maps ................................................................................................................................................................................. I-III State Staff .................................................................................................................................................................................................. IV State Officers ............................................................................................................................................................................................V-VI Area I ........................................................................................................................................................................................................1-6 District I ....................................................................................................................................................................................................1 Bienville Parish ..................................................................................................................................................................................1 Claiborne Parish .................................................................................................................................................................................1 Webster Parish ...................................................................................................................................................................................1 -

School District School Name Acadia Parish School District Acadia Parish Alt School Armstrong Middle School Branch Elementary

SCHOOL DISTRICT SCHOOL NAME ACADIA PARISH SCHOOL DISTRICT ACADIA PARISH ALT SCHOOL ARMSTRONG MIDDLE SCHOOL BRANCH ELEMENTARY SCHOOL CENTRAL RAYNE KINDERGARTEN CHURCH POINT ELEM SCHOOL CHURCH POINT HIGH SCHOOL CHURCH POINT MIDDLE SCHOOL CROWLEY HIGH SCHOOL CROWLEY KINDERGARTEN CROWLEY MIDDLE SCHOOL EGAN ELEMENTARY SCHOOL ESTHERWOOD ELEMENTARY SCHOOL EVANGELINE ELEMENTARY SCHOOL IOTA ELEMENTARY SCHOOL IOTA HIGH SCHOOL IOTA MIDDLE SCHOOL MARTIN PETITJEAN ELEM SCHOOL MERMENTAU ELEMENTARY SCHOOL MIDLAND HIGH SCHOOL MIRE ELEMENTARY SCHOOL MORSE ELEMENTARY SCHOOL NORTH CROWLEY ELEM SCHOOL RAYNE HIGH SCHOOL RICHARD ELEMENTARY SCHOOL ROSS ELEMENTARY SCHOOL SOUTH CROWLEY ELEM SCHOOL SOUTH RAYNE ELEM SCHOOL ALLEN PARISH SCHOOL DISTRICT ALLEN PARISH ALT SCHOOL ELIZABETH HIGH SCHOOL FAIRVIEW HIGH SCHOOL KINDER ELEMENTARY SCHOOL KINDER HIGH SCHOOL KINDER MIDDLE SCHOOL OAKDALE ELEMENTARY SCHOOL OAKDALE HIGH SCHOOL OAKDALE MIDDLE SCHOOL OBERLIN ELEMENTARY SCHOOL OBERLIN HIGH SCHOOL REEVES HIGH SCHOOL ASCENSION PARISH SCHOOL DIST ASCENSION PARISH ALT SCHOOL CENTRAL ELEMENTARY SCHOOL DONALDSONVILLE HIGH SCHOOL DONALDSONVILLE PRIMARY SCHOOL DUPLESSIS PRIMARY SCHOOL DUTCHTOWN HIGH SCHOOL DUTCHTOWN MIDDLE SCHOOL 1 DUTCHTOWN PRIMARY SCHOOL EAST ASCENSION HIGH SCHOOL G W CARVER PRIMARY SCHOOL GALVEZ MIDDLE SCHOOL GALVEZ PRIMARY SCHOOL GONZALES MIDDLE SCHOOL GONZALES PRIMARY SCHOOL LAKE ELEMENTARY SCHOOL LOWERY ELEMENTARY SCHOOL LOWERY INTERMEDIATE SCHOOL OAK GROVE PRIMARY SCHOOL PECAN GROVE PRIMARY SCHOOL PRAIRIEVILLE MIDDLE SCHOOL PRAIRIEVILLE PRIMARY SCHOOL -

2020-2021 Suicide Prevention Certified Schools A.A

2020-2021 Suicide Prevention Certified Schools A.A. Nelson Elementary Arthur F. Smith Middle Magnet School Abita Springs Elementary School Atlanta High School Abita Springs Middle School Audubon Charter Gentilly Abney Elementary School Audubon Charter School Abramson Science Academy Audubon Elementary School Acadian Elementary School Avoyelles High School Acadiana High School B Edward Boudreaux Middle School Airline K-12 School Baranco Elementary School Albany High School Barbe Elementary School Albany Lower Elementary School Barbe High School Albany Middle School Barkdull Faulk Elementary School Albany Upper Elementary School Basile High School Albert Cammon Middle School Baskin High School Alice Boucher Elementary School Bastrop High School Allemands Elementary School Baton Rouge Magnet High School Alternative Center for Education Bayou Black Elementary School Alton Elementary School Bayou Blue Elementary School Anacoco Elementary School Bayou Blue High School Anderson Middle School Bayou Blue Middle School Apollo Elementary School Bayou Boeuf Elementary School APPLE & Career Training Center Bayou Chicot Elementary School Arabi Elementary School Bayou Lacombe Middle School ARISE Academy Bayou Vista Elementary School Arlene Meraux Elementary School Bayou Woods Elementary Arnett Elementary School Beau Chene High School Arthur Ashe Charter School Beauregard Alternative Program Belfair Montessori Magnet BRCVPA Bell City K-12 Combination School Brentwood Elementary School Bellaire Elementary School BRFLAIM Bellaire Magnet High School Bricolage -

ACT Best Composite Scores for 2017-2018 Seniors by Parish

ACT Best Composite Scores for 2017-2018 Seniors by Parish The Louisiana Department of Education has modified and/or suppressed data reported to protect the privacy of students in compliance with the Family Educational Rights and Privacy Act (FERPA) codified at 20 U.S.C. 1232g. The strategies used to protect privacy vary and may include rounding or other techniques but do not substantially affect the general usefulness of the data. Because of the privacy protections, numerical and percentage totals may not add precisely to the sum of the row or column to which the total refers. ~ indicates statistically unreliable (i.e. Less than 10 students in a subgroup). N/A indicates scores not available. 2017-2018 ACT data were calculated using the Best Score methodology. Includes all 2017-2018 Seniors' Best ACT score. 2017-2018 Average District ID District Site Code Site Name 2017-2018 Student Count Composite Score 026 Jefferson Parish 026042 Haynes Academy School for Advanced Studies 92 29.8 302 Louisiana School for Math302006 Science & the ArtsLouisiana School for Math Science & the Arts 113 29.6 R36 Orleans Parish and RSDNOWBB001 Benjamin Franklin High School 193 29.3 026 Jefferson Parish 026105 Patrick F. Taylor Science & Technology Academy66 28.4 009 Caddo Parish 009012 Caddo Parish Magnet High School 243 27 026 Jefferson Parish 026107 Thomas Jefferson High School for Advanced Studies93 26.8 318001 LSU Laboratory School 318001 LSU Laboratory School 118 26.7 R36 Orleans Parish and RSDNOWBE001 Lusher Charter School 132 26.5 017 East Baton Rouge Parish 017008 Baton Rouge Magnet High School 318 26.3 334 New Orleans Center for Creative334001 Arts New Orleans Center for Creative Arts 51 24.7 028 Lafayette Parish 028053 Early College Academy 51 24.6 052 St. -

2019-2020 Teachers Directory Table of Contents

2019-2020 Teachers Directory Table of Contents Louisiana FFA Maps ................................................................................................................................................................................. I-III State Staff .................................................................................................................................................................................................. IV State Officers ............................................................................................................................................................................................V-VI Area I ........................................................................................................................................................................................................1-6 District I ....................................................................................................................................................................................................1 Bienville Parish ..................................................................................................................................................................................1 Claiborne Parish .................................................................................................................................................................................1 Webster Parish ...................................................................................................................................................................................1 -

School District No. 23 of Calcasieu Parish, Louisiana $8,070,000 GENERAL OBLIGATION REFUNDING BONDS, 2012 SERIES a SCHOOL DISTRICT NO

RATING: S&P “A+” REFUNDING ISSUE – BOOK ENTRY ONLY (See “MISCELLANEOUS-Bond Rating” herein) In the opinion of Bond Counsel, under existing laws and assuming continuous compliance by the School District and the Board with certain covenants designed to meet the requirements of the Internal Revenue Code of 1986, as amended (the “Code”), interest on the Bonds is excluded from gross income of the owners for Federal income tax purposes. In the opinion of Bond Counsel, the Bonds and the income therefrom are exempt from all taxation by the State of Louisiana or any political subdivision thereof. See “Tax Exemption” herein. $13,210,000 COMPOSITE OFFERING GENERAL OBLIGATION PUBLIC SCHOOL REFUNDING BONDS, 2012 SERIES SCHOOL DISTRICT NO. 23 OF CALCASIEU PARISH, LOUISIANA $8,070,000 GENERAL OBLIGATION REFUNDING BONDS, 2012 SERIES A SCHOOL DISTRICT NO. 23 OF CALCASIEU PARISH, LOUISIANA $5,140,000 GENERAL OBLIGATION REFUNDING BONDS, 2012 SERIES B SCHOOL DISTRICT NO. 23 OF CALCASIEU PARISH, LOUISIANA Dated: Date of Delivery Due: As shown on inside cover This Composite Offering of $13,210,000 General Obligation Refunding Bonds, 2012 Series (described above and herein) is comprised of two separate bond issues issued by School District No. 23 of Calcasieu Parish, Louisiana (the “School District”), namely $8,070,000 General Obligation Refunding Bonds, 2012 Series A (the “Series A Bonds”) and $5,140,000 General Obligation Refunding Bonds, 2012 Series B (the “Series B Bonds”). The Series A Bonds and Series B Bonds are herein collectively referred to as the “Bonds”. The School District is governed by the Calcasieu Parish School Board (the “Governing Authority” or the “Board”).