2014 Comprehensive Annual Financial Report for the State of Texas 1 2 2014 Comprehensive Annual Financial Report for the State of Texas February 27, 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

April 8, 2020 the Honorable Wayne Christian the Honorable Christi

April 8, 2020 The Honorable Wayne Christian The Honorable Christi Craddick The Honorable Ryan Sitton Railroad Commission of Texas P.O. Box 12967 Austin, Texas 78711-2967 Submitted via email to [email protected]. RE: Comments by Public Citizen on Verified complaint of Pioneer Natural Resources U.S.A. Inc. and Parsley Energy Inc to determine reasonable market demand for oil in the state of Texas Public Citizen appreciates the opportunity to provide these comments. We would welcome the opportunity to discuss our recommendations further. Please contact Texas office director Adrian Shelley at [email protected], 713-702-8063. I. Current Market Forces Demand A Cut in Production The Railroad Commission must act now to curtail production through proration. We join Environment Texas and others in calling for proration to occur based on company waste through flaring and other pollution emissions. Proration to curtail oil production in Texas is now necessary due to current market forces. Texas and the nation are experiencing historic surplus and low prices. Supply now exceeds demand and will continue to do so for the foreseeable future. There are a number of reasons why. a. Global supply surplus There is a global supply surplus caused by an ongoing war for market share between Saudi Arabia and Russia. Railroad Commissioner Ryan Sitton estimates a global market surplus of 10 to 15 percent, roughly 10 to 15 million barrels/day.1 Petitioners assert that a production surplus could overwhelm the handling, processing, and storage industries. This risk to certain industry participants is one reason petitioners ask for proration. -

Horner 1916-2008 Volume 116/ Summer 2008

BAYLOR UNIVERSITY SCHOOL OF LAW SUMMER 2008 Professor edwin P. Horner 1916-2008 VOLUME 116/ SUMMER 2008 Docket Call is published by the Baylor University School of Law for its alumni, faculty, staff, students, supporters and friends. The Baylor School of Law, established in 1849, was the first law school in Texas and one of the first west of the Mississippi River. Today, the school has more than 6,400 living alumni. It is accredited by the American Bar Association and is a member of the Association of American Law Schools. table of contents Faculty News Alumni News page 5 d 24 Articles Selected by 44 Paddling His Harold R. Cunningham Acting President, Baylor University Dean’s Message Baylor Law Professor a Own Canoe This issue of Docket Call Top Source for Estate Editor Planning Practitioners 48 Nelson Roach Julie Campbell Carlson pays tribute to Baylor Law icon page 7 Elected 2008 25 Law Professor’s Amicus President- Photographers A Message From Baylor Law Letter Holds Sway in Elect of Texas Robert Rogers, Matthew Minard Alumni Association President Texas Supreme Court Trial Lawyers Edwin P. Horner, Decision Association Design & Production ECCO Design & Communications, L.L.C. Dallas, Texas who passed away Feb. 1 26 Getting to Know Baylor’s 48 Baylor Lawyer Abelardo Valdez Receives page 8 Newest Faculty Baylor Distinguished Alumnus Award Contributing Writers Farewell to Fast Eddie Lea Burleson Buffington, Becky Beck-Chollett 30 Alumni Gather at Baylor Reception During 49 Law Alumna Priscilla Owen Honored for Julie Corley, Cortney Dale, Heather Creed at the age of 92 Annual Meeting of the State Bar of Texas Public Service with Price Daniel Award BAYLOR LAW SCHOOL FACULTY and who taught thousands page 12 50 Baylor Law Alum Elected President-Elect of the State Bar of Texas Brad Toben, Dean One Memorable Journey Leah W. -

Chairman Christi Craddick Commissioner David Porter Commissioner Ryan Sitton

Chairman Christi Craddick Commissioner David Porter Commissioner Ryan Sitton December 2016 Railroad Commission of Texas | June 27, 2016 (Change Date In First Master Slide) 11 RRC Mission Our mission is to serve Texas by our stewardship of natural resources and the environment, our concern for personal and community safety, and our support of enhanced development and economic vitality for the benefit of Texans. Railroad Commission of Texas | June 27, 2016 (Change Date In First Master Slide) 2 RRC History Established 1891 • Texas’ oldest regulatory agency • almost 100 years regulating oil & gas • Led by 3 statewide elected officials Railroad Commission of Texas | June 27, 2016 (Change Date In First Master Slide) 3 RRC Jurisdiction • Oil and natural gas industry • Intrastate pipelines, natural gas and hazardous liquid pipeline industry • Liquefied Petroleum Gas (LPG), Compressed Natural Gas (CNG), and Liquid Natural Gas (LNG) • Natural gas utilities • Coal and uranium surface mining operations Railroad Commission of Texas | June 27, 2016 (Change Date In First Master Slide) 4 Permian Basin Located in West Texas and southeastern New Mexico • More than 7,000 RRC fields in 59 counties • Roughly 250 miles wide and 300 miles long • Oil and natural gas production ranging to depths of five miles below the surface • Estimated to contain recoverable oil and natural gas resources exceeding what has been produced over the last 90 years Railroad Commission of Texas | June 27, 2016 (Change Date In First Master Slide) 5 6 Railroad Commission of Texas | -

The 2020 Election 2 Contents

Covering the Coverage The 2020 Election 2 Contents 4 Foreword 29 Us versus him Kyle Pope Betsy Morais and Alexandria Neason 5 Why did Matt Drudge turn on August 10, 2020 Donald Trump? Bob Norman 37 The campaign begins (again) January 29, 2020 Kyle Pope August 12, 2020 8 One America News was desperate for Trump’s approval. 39 When the pundits paused Here’s how it got it. Simon van Zuylen–Wood Andrew McCormick Summer 2020 May 27, 2020 47 Tuned out 13 The story has gotten away from Adam Piore us Summer 2020 Betsy Morais and Alexandria Neason 57 ‘This is a moment for June 3, 2020 imagination’ Mychal Denzel Smith, Josie Duffy 22 For Facebook, a boycott and a Rice, and Alex Vitale long, drawn-out reckoning Summer 2020 Emily Bell July 9, 2020 61 How to deal with friends who have become obsessed with 24 As election looms, a network conspiracy theories of mysterious ‘pink slime’ local Mathew Ingram news outlets nearly triples in size August 25, 2020 Priyanjana Bengani August 4, 2020 64 The only question in news is ‘Will it rate?’ Ariana Pekary September 2, 2020 3 66 Last night was the logical end 92 The Doociness of America point of debates in America Mark Oppenheimer Jon Allsop October 29, 2020 September 30, 2020 98 How careful local reporting 68 How the media has abetted the undermined Trump’s claims of Republican assault on mail-in voter fraud voting Ian W. Karbal Yochai Benkler November 3, 2020 October 2, 2020 101 Retire the election needles 75 Catching on to Q Gabriel Snyder Sam Thielman November 4, 2020 October 9, 2020 102 What the polls show, and the 78 We won’t know what will happen press missed, again on November 3 until November 3 Kyle Pope Kyle Paoletta November 4, 2020 October 15, 2020 104 How conservative media 80 E. -

The Honorable Ryan Sitton Texas Railroad Commissioner

APRIL APRIL2016 2016 Light, Tight Oil in the THE HONORABLE RYAN SITTON, TEXAS RAILROADPermian Delaware COMMISSIONER Basin: Recent DevelopmentsGENERAL MEETING P. 13 GENERAL MEETING P. 11 HIGH PERFORMANCE CERAMICS PERMIAN BASIN P. 21 ARTIFICIAL LIFT FOR THE LIFE OF WELLSDATA-DRIVEN IN UNCONVENTIONAL PLAYS ANDNORTHSIDE REDUCED P. 9 ORDER MODELS INCOST-EFFECTIVE RESERVOIR RECOVERY OPTIMIZATION OF WATERFLOODS MEMBERS IN TRANSITION RESERVOIRSIMULATION P. 16 RESERVOIR P. 28 INITIATIVE2016 SALARY (MIT) PRACTICAL HYDRAULIC FRACTURING THIRD SEMINAR SURVEYSERIES P. 27 STIMULATIONNORM IN PRODUCED DESIGN MODELS HIGHLIGHTS COMPLETIONSWATERS: BASICS& PRODUCTION OF P. 18 PETRO-TECH P. 23 PROBLEM AVOIDANCE WATER & WASTE MANAGEMENT P. 31 SPEGCS.ORG SPE-GCS CONNECT Accelerated Learning Tutorials (ALTs): CHAIR’S We have had great success with our first ALTs, which were introductions to gas lift systems (November), managed pressure CORNER drilling (January), and reservoir simulation (February). We have four more to go: introductions to flow assurance (April), PVT analysis (May), oilfield geomechanics (June), and nodal analysis (TBA). These one-day courses are proving to be an excellent means of rapidly immersing oneself in a topic. As the year progresses, I’ll advise on more initiatives. So, as always, watch this space… All the best! DR. IVOR ELLUL 2015 - 2016 SPE-GCS Chair “Thanks for a most informative workshop. All three topics were well on target and well received. Overall the workshop was s I write this, CERAWeek has just kicked off with an interesting array of key well planned and executed. As a webinar individuals imparting wisdom on the current state of the oil and gas industry and participant, I felt connected and engaged what will happen in the near and medium term. -

Rigged: the Oil and Gas Industry Bankrolls Its Own Regulators

Rigged: The Oil and Gas Industry Bankrolls Its Own Regulators “This whole election is being rigged.” –The Donald Trump The three sitting members of the misnamed Texas Railroad Commission conservatively took 60 percent of the more than $11 million that they raised in recent years from the oil and gas industry that they regulate. The No. 2 source of political funding for these commissioners was the Lawyers & Lobbyists sector, which accounts for another 7 percent of the commissioners’ cash. With many of these attorneys representing clients before the agency, the two industries pressing the most business before the commissioners supply 67 percent of their funding. Oil and gas interests alone also supplied 65 percent of the money reported by the candidate most likely to win this week’s Railroad Commission race. Money Raised by Current Commissioners (Since January 2010) Commissioner Year Itemized Oil & Gas Oil & Gas Fundraising (Party) Elected Contributions Amount Percent Period Christi Craddick (R) 2012 $4,874,193 $2,712,424 56% 7/2011 thru 6/2016 Ryan Sitton (R) 2014 $3,688,668 $2,166,202 59% 9/2013 thru 6/2016 David Porter (R) 2010 $2,558,551 $1,749,176 68% 1/2010 thru 6/2016 TOTALS $11,121,412 $6,627,802 60% This report analyzes the itemized campaign contributions of the three sitting commissioners and the four 2016 finalists seeking the seat of retiring Commissioner David Porter. Where appropriate, this study tracks money raised as far back as 2010, when Porter first ran for his seat. Long a major player in Texas politics, the energy industry has an especially outsized role in bankrolling its own regulators. -

VERTICAL TARGET June 18 2015 Layout 1

VOLUME 18, NO. 12 THE TIPRO TARGET June 18, 2015 DAVID PORTER UNANIMOUSLY ELECTED CHAIRMAN OF Texas TEXAS RAILROAD COMMISSION Independent Producers and During the Railroad Commission’s Open Meeting on June 9, 2015, David Porter was unanimously elected to serve as chairman of the state agency. Chairman Porter has served as Railroad Commissioner Royalty Owners since he was elected statewide by the people of Texas in November 2010. During his term at the Association commission, Chairman Porter has led several oil and gas initiatives. Upon taking office in 2011, Chairman Porter created the Eagle Ford Shale Task Force, the first of its kind at the Railroad Commission, to establish a forum that brings the community together to foster a productive and forward-looking dialogue regarding drilling activities in the Eagle Ford Shale. Later, in 2013, Chairman Porter also launched his Texas Natural Gas Initiative: a series of statewide events that bring stakeholders together to discuss business opportunities, challenges and regulatory barriers and solutions for natural gas conversion and infrastructure – focusing largely on the transportation and exploration and production sectors. In the last four years, Chairman Porter has been appointed to the Interstate Oil and Gas Compact Commission as the official representative of Texas and currently serves as second vice-president of the organization. In addition, he is an advisory board member for the Texas Journal of Oil, Gas, and Energy Law. From 2011-2014, Chairman Porter also served as the official representative on the Interstate Mining Compact Commission. “As Railroad Commissioners, it is our job to make sure industry produces efficiently and economically, and does so in the safest, most responsible manner possible. -

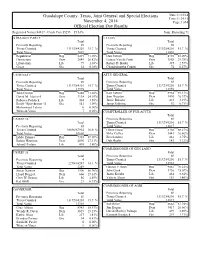

Gems Election Summary Report

Guadalupe County, Texas, Joint General and Special Elections Date:11/12/14 Time:11:34:15 November 4, 2014 Page:1 of 4 Official Election Day Results Registered Voters 84817 - Cards Cast 13253 15.63% Num. Reporting 71 STRAIGHT PARTY LT GOV Total Total Precincts Reporting 69 Precincts Reporting 69 Times Counted 13192/84201 15.7 % Times Counted 13192/84201 15.7 % Total Votes 7639 Total Votes 13056 Republican Rep 5497 71.96% Dan Patrick Rep 8759 67.09% Democratic Dem 2049 26.82% Leticia Van de Putte Dem 3888 29.78% Libertarian Lib 79 1.03% Robert D. Butler Lib 335 2.57% Green Gre 14 0.18% Chandrakantha Courtn Gre 74 0.57% US SENATE ATTY GENERAL Total Total Precincts Reporting 69 Precincts Reporting 69 Times Counted 13192/84201 15.7 % Times Counted 13192/84201 15.7 % Total Votes 12978 Total Votes 12959 John Cornyn Rep 9248 71.26% Ken Paxton Rep 8964 69.17% David M. Alameel Dem 3118 24.03% Sam Houston Dem 3490 26.93% Rebecca Paddock Lib 464 3.58% Jamie Balagia Lib 413 3.19% Emily "Spicybrown" S Gre 141 1.09% Jamar Osborne Gre 92 0.71% Mohammed Tahiro 0 0.00% Write-in Votes 7 0.05% COMPTROLLER OF PUB ACCTS Total US REP 15 Precincts Reporting 69 Total Times Counted 13192/84201 15.7 % Precincts Reporting 65 Total Votes 12817 Times Counted 10896/67954 16.0 % Glenn Hegar Rep 8750 68.27% Total Votes 10660 Mike Collier Dem 3443 26.86% Eddie Zamora Rep 7365 69.09% Ben Sanders Lib 481 3.75% Ruben Hinojosa Dem 2890 27.11% Deb Shafto Gre 143 1.12% Johnny Partain Lib 405 3.80% COMMISSIONER OF GEN LAND US REP 35 Total Total Precincts Reporting 69 Precincts Reporting 4 Times Counted 13192/84201 15.7 % Times Counted 2296/16247 14.1 % Total Votes 12932 Total Votes 2249 George P. -

July 2012 Republican Primary Runoff Election

Texas Secretary of State Hope Andrade Race Summary Report Unofficial Election Tabulation 2012 Republican Party Primary Runoff July 31, 2012 U. S. Senator Early Provisional 249 Total Provisional 948 Precincts 7,957 o 7,957 100.00 Early % Vote Total % Ted Cruz 291,040 52.92% 631,316 56.80% David Dewhurst 258,893 47.08% 480,165 43.20% Registered 13,065,42 Total Votes 549,933 4.21% Voting 1,111,481 8.51% Voting Total Number of Voters 1,139,782 U. S. Representative District 14 Multi County Precincts 282 o 282 100.00 Early % Vote Total % Felicia Harris 8,237 36.83% 13,765 37.23% Randy Weber 14,130 63.17% 23,212 62.77% Total Votes 22,367 36,977 U. S. Representative District 15 Multi County Precincts 272 o 272 100.00 Early % Vote Total % Dale A. Brueggemann 3,495 58.65% 6,398 57.30% Eddie Zamora 2,464 41.35% 4,767 42.70% Total Votes 5,959 11,165 U. S. Representative District 25 Multi County Precincts 192 o 192 100.00 Early % Vote Total % Wes Riddle 9,449 39.28% 19,210 42.04% Roger Williams 14,607 60.72% 26,487 57.96% Total Votes 24,056 45,697 11/10/2016 11:15 Page 1 of 7 Texas Secretary of State Hope Andrade Race Summary Report Unofficial Election Tabulation 2012 Republican Party Primary Runoff July 31, 2012 U. S. Representative District 34 Multi County Precincts 208 o 208 100.00 Early % Vote Total % Jessica Puente Bradshaw 2,321 51.98% 5,308 55.34% Adela Garza 2,144 48.02% 4,283 44.66% Total Votes 4,465 9,591 U. -

VERTICAL TARGET August 15, 2019 Layout 1

VOLUME 21, NO. 16 THE TIPRO TARGET August 15, 2019 Texas Independent TRUMP ADMINISTRATION FINALIZES MAJOR OVERHAUL OF ESA, WILL Producers and NOW WEIGH ECONOMIC BURDEN AS A FACTOR FOR LISTING DECISIONS Royalty Owners Association The Trump Administration on Monday, August 12th finalized big changes to the Endangered Species Act (ESA), which government officials promise will improve implementation of the federal policy and deliver greater transparency along with more efficient listing determinations. Regulatory changes also will allow economic cost of protecting a species to now be considered as part of the listing process, along with the best available scientific and commercial information. “The best way to uphold the ESA is to do everything we can to ensure it remains effective in achieving its ultimate goal—recovery of our rarest species. The Act’s effectiveness rests on clear, consistent and efficient implementation,” commented U.S. Interior Secretary David Bernhardt. “An effectively administered Act ensures more resources can go where they will do the most good: on-the-ground conservation.” First enacted in 1973, the ESA was passed into law more than 45 years ago to provide a framework for conservation and protection of endangered and threatened species and their habitats. Over the years, the ESA has become a vehicle for a barrage of frivolous legal petitions from activists seeking to deploy tactics called “sue and settle” to advance partisan agendas and prevent energy development. Although there has been talk in Washington for many years of updating the policy, past administrations have been unsuccessful in adopting substantial improvements to the Act. Now, new revisions from Interior’s U.S. -

March 4, 2014 Primary Results (Official)

SUMI1ARY REPORT 2014 PRIMRY ELECTION OFFICIAT TOTALS HILL COUNTY, TEXAS r,tARcH 4. 2014 RUN DATE:03/12114 01:23 Pll STATISTICS VOTES PERCENI PRECII{CTS COUNTED (OF 22) 22 100.00 REGISTERED VOTERS . TOTAL . 2L.7U BALTOTS CAST . TOTAL. 6,459 EALLOTS CAST . REPUELICN PARTY 6,0i0 93.05 EALLOTS CAST . DEI4OCMTIC PARTY M9 6.95 VOTER IURMUT - TOTAL 29.@ SUII{ARY REPORT 2OI4 PRIIORY ELECTIOTI OFFICIAL IOIALS HILL COI,NTY, TEXAS I{ARCH 4, 2014 RUN MIE:03/12114 01:23 Pll REPUBLICAI{ PARTY VOTES PERCET{T VOTES PERCEMI US Senator HILL CoUNrYIIID€ Cqmissioner of Agriculture HILL CoIJIrYUIDE VOTE FOR 1 VOTE FOR 1 John Cornyn. 3,738 67.39 Tommy tlerritt 1,001 19.80 Chnis ilapp 149 2.69 Joe Cotten 809 16.00 Curt Cleaver 66 1.19 J. Allen Carnes 930 18.40 Ken Cope. 119 2.L5 Sid ililler 1,288 25.M Dxayne Stoval I . 373 6.72 Eric opiel a. r,027 20.32 Reid Reasor. 49 .88 Linda Vega 248 4.47 Steve Stochan. 805 14.51 Rai lroad Cormissioner HILL C0UI{TYWIDE VOTE FOR 1 Wayne Christian 2,113 43.90 US Representative, DIST 25 HILL COIJI{TYI{IDE Ryan Sitton. 1,321 27.45 VOTE FOR 1 l,lalachi Boyul s. 370 7.69 Roger tlilliams. 4,378 100.00 Becky Berger 1,009 20.96 Governor HILL CoUl{TYilI DE Chief Justice, Supreme Court HILL CqJ TYI{IDE vorE FoR 1 VOTE FOR 1 Lisa Fritsch 3r2 5.54 Nathan Hecht 2,855 59-92 SECEDE Ki I gore. -

UNOFFICIAL RESULSTS REPUBLICAN PRIMARY Early 1 2 & 4 3 TOTAL FEDERAL PRESIDENT and VICE PRESIDENT

UNOFFICIAL RESULSTS REPUBLICAN PRIMARY Early 1 2 & 4 3 TOTAL FEDERAL PRESIDENT AND VICE PRESIDENT BILL WELD 0 0 0 0 0 BOB ELY 0 0 1 1 2 DONALD J TRUMP 97 36 78 36 247 ROQUE " ROCKY" DE LA FUENTE GUERRA 0 0 1 0 1 MATHEW JOHN MATERN 0 0 0 0 0 ZOLTAN G ISTVAN 0 0 0 0 0 JOE WALSH 0 0 1 0 1 UNCOMMITTED 2 2 0 1 5 TOTAL 99 38 81 38 256 UNITED STATES SENATOR VIRGIL BIERSCHWALE 0 2 5 0 7 MARK YANCY 4 3 9 5 21 JOHN ANTHONY CASTRO 7 5 7 2 21 JOHN CORNYN 76 19 46 22 163 DWAYNE STOVALL 6 3 1 1 11 TOTAL 93 32 68 30 180 UNITED STATES REPRESENTATIVE DIST 28 SANDRA WHITTEN 74 22 59 25 180 TOTAL 74 22 96 25 180 STATE RAILROAD COMMISSIONER JAMES "JIM" WRIGHT 54 23 48 18 143 RYAN SITTON 28 6 17 10 61 TOTAL 82 29 65 28 204 CHIEF JUSTICE, SUPREME COURT NATHAN HECHT 75 24 61 27 187 TOTAL 75 24 61 27 187 JUSTICE, SUPREME COURT, PL 6 JANE BLAND 74 23 61 27 185 TOTAL 74 23 61 27 185 JUSTICE SUPREME COURT, PL 7 JEFF BOYD 76 22 63 27 188 TOTAL 76 22 63 27 188 JUSTICE, SUPREME COURT, PL 8 BRETT BUSBY 72 20 63 27 182 TOTAL 72 20 63 27 182 JUDGE, COURT OF CRIMINAL APPEALS PL 3 GINA PARKER 38 11 25 11 85 BERT RICHARDSON 38 20 34 16 108 TOTAL 76 31 59 27 193 JUDGE, COURT OF CRIMINAL APPEALS PL 4 KEVIN PATRICK YEARY 72 20 63 27 182 TOTAL 72 20 63 27 72 JUDGE, COURT OF CRIMINAL APPEALS PL 9 DAVID NEWELL 72 20 62 27 181 TOTAL 72 20 62 27 181 STATE SENATOR, DIST 21 FRANK POMEROY 74 20 63 28 185 TOTAL 74 20 63 28 185 STATE REPRESENTATIVE DIST 31 MARIAN KNOWLTON 71 19 62 29 181 TOTAL 71 19 62 29 181 CHIEF JUSTICE, 4TH COURT OF APPEALS RENEE YANTA 73 19 63 27 182 TOTAL 73 19