1 in the Court of Chancery of the State of Delaware

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Facilitating a Hybrid College-Level Course Using Microblogging: a Case Study

Facilitating a Hybrid College-level Course Using Microblogging: A Case Study A dissertation presented to the faculty of The Patton College of Education of Ohio University In partial fulfillment of the requirements for the degree Doctor of Philosophy Tian Luo August 2014 ©2014 Tian Luo. All Rights Reserved. 2 This dissertation titled Facilitating a Hybrid College-level Course Using Microblogging: A Case Study by TIAN LUO has been approved for the Department of Educational Studies and The Patton College of Education by David R. Moore Associate Professor of Instructional Technology Renée A. Middleton Dean, The Patton College of Education 3 Abstract LUO, TIAN, Ph.D., August 2014, Curriculum and Instruction, Instructional Technology Facilitating a Hybrid college-level Course Using Microblogging: A Case Study (290 pp.) Director of Dissertation: David R. Moore Social media has become an increasingly growing phenomenon that arouses mounting interest as well as heated discussion concerning its varied definitions and practices for academic use. Recently, a common type of social media, microblogging tools such as Twitter, has garnered researchers and educators' mounting attention due to its prevailing usage among the younger generation. This study seeks to both examine student learning in the Twitter-supported learning environments and to understand the potential factors affecting student perceptions and participation. The researcher incorporated three major Twitter-based instructional activities into a hybrid course, namely, Exploring Hashtags, Discussion Topics, and Live Chats. Twitter was employed as a backchannel to enhance classroom interaction during lectures and student presentations in face-to-face settings. The participants were 24 college-level Teacher Education program students enrolled in a technology course at a large Midwestern University. -

New Appointments (India) S

GK POWER CAPSULE FOR IBPS CLERK MAINS 2015-16 government has approved the company’s raising Rs. 1,000 crore through tax free bonds, including Rs. 700 crore through public issue. 25) Current a/c deficit narrows to 1.2% of GDP in April-June. 26) The Employees Provident Fund Organisation (EPFO) increased the life insurance cover of its subscribers from 3.6 lakh to 6 lakh rupees. 27) The banks in Dakshina Kannada district conducted a mega credit camp to disburse loans under the MUDRA scheme of the Centre on September 28. 28) The World Bank has promised $30 billion financial assistance to the Railways. NEW APPOINTMENTS (INDIA) S. no Newly Appointed Post & Company 1. Subir Vithal Gokarn Executive Director on the board of the International Monetary Fund (IMF) 2. Justice Ajit Prakash Shah Ethics officer (ombudsman) at Board of Control for Cricket in India (BCCI). 3. Navtej Singh Sarna Indian High Commissioner to United Kingdom (UK) 4. V-Sivaramakrishnan (Siva) Managing Director, Oxford University Press India (OUPI) 5. Justice T S Thakur 43rd Chief Justice of India 6. Anil Kumar Jha Chairman-cum-Managing Director of Mahanadi Coalfields Ltd (MCL) 7. Deepak Singhal Executive Director of Reserve Bank of India. 8. Virender Mohan Khanna Maintenance Head of IAF 9. Harshavardhan Neotia President of FICCI. Note: He will succeed Jyotsna Suri 10. Nitish Kumar Chief Minister of Bihar (Fifth Time) 11. V Raja Vice-Chairman and Managing Director, Philips India 12. Vijay Keshav Gokhale India’s Ambassador to China. Note: He will replace Ashok Kantha 13. Zarin Daruwala India’s Chief Executive Officer at Standard Chartered Bank 14. -

Social Media

What is Social media? Social media is defined as "a group of Internet-based applications that build on the ideological and technological foundations of the World Wide Web, and that allow the creation and exchange of user content.“ (Wikipedia 2014) What is Facebook? Facebook is a popular free social networking website that allows registered users to create profiles, upload photos and video, send messages and keep in touch with friends, family and colleagues.(Dean,A.2014) History on facebook Facebook was launched in February 2004. It was founded by Mark Zuckerberg his college roommates and fellow Harvard University student Eduardo Saverin. The website's membership was initially limited by the founders to Harvard students, but was expanded to other colleges in the Boston area. By September 2006, to everyone of age 13 and older to make a group with a valid email address. Reasons for using Facebook It is a medium of finding old friends(schoolmates..etc) It is a medium of advertising any business It is a medium of entertainment Sharing your photos and videos Connecting to love ones What makes Facebook popular? The adding of photos News feed The “Like” button Facebook messenger Relationship status Timeline Some hidden features of Facebook File transfer over FB chat See who is snooping in your account An inbox you didn’t know you have You Facebook romance* Save your post for later What is Twitter? Twitter is a service for friends, family, and coworkers to communicate and stay connected through the exchange of quick, frequent messages. People post Tweets, which may contain photos, videos, links and up to 140 characters of text. -

March 24, 2021 Via First Class and Electronic Mail Jack Dorsey Chief

OFFICE OF THE ATTORNEY GENERAL CONNECTICUT william tong attorney general March 24, 2021 Via First Class and Electronic Mail Jack Dorsey Chief Executive Officer Twitter, Inc. 1355 Market St. San Francisco, CA 94103 Mark Zuckerberg Chairman & Chief Executive Officer Facebook, Inc. 1 Hacker Way Menlo Park, CA 94025 Re: Vaccine Disinformation Dear Messrs. Dorsey and Zuckerberg: As Attorneys General committed to protecting the safety and well-being of the residents of our states, we write to express our concern about the use of your platforms to spread fraudulent information about coronavirus vaccines and to seek your cooperation in curtailing the dissemination of such information. The people and groups spreading falsehoods and misleading Americans about the safety of coronavirus vaccines are threatening the health of our communities, slowing progress in getting our residents protected from the virus, and undermining economic recovery in our states. As safe and effective vaccines become available, the end of this pandemic is in sight. This end, however, depends on the widespread acceptance of these vaccines as safe and effective. Unfortunately, misinformation disseminated via your platforms has increased vaccine hesitancy, which will slow economic recovery and, more importantly, ultimately cause even more unnecessary deaths. A small group of individuals use your platforms to downplay the dangers of COVID-19 and spread misinformation about the safety of vaccines. These individuals lack medical expertise and are often motivated by financial interests. According to a recent report by the Center for Countering Digital Hate1, so-called “anti-vaxxer” accounts on Facebook, YouTube, Instagram, and Twitter reach more than 59 million followers. -

Broadcast and Audio Flag Hearing

S. HRG. 109–580 BROADCAST AND AUDIO FLAG HEARING BEFORE THE COMMITTEE ON COMMERCE, SCIENCE, AND TRANSPORTATION UNITED STATES SENATE ONE HUNDRED NINTH CONGRESS SECOND SESSION JANUARY 24, 2006 Printed for the use of the Committee on Commerce, Science, and Transportation ( U.S. GOVERNMENT PRINTING OFFICE 29–917 PDF WASHINGTON : 2006 For sale by the Superintendent of Documents, U.S. Government Printing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2250 Mail: Stop SSOP, Washington, DC 20402–0001 VerDate 0ct 09 2002 15:35 Sep 19, 2006 Jkt 029917 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 S:\WPSHR\GPO\DOCS\29917.TXT JACKF PsN: JACKF SENATE COMMITTEE ON COMMERCE, SCIENCE, AND TRANSPORTATION ONE HUNDRED NINTH CONGRESS SECOND SESSION TED STEVENS, Alaska, Chairman JOHN MCCAIN, Arizona DANIEL K. INOUYE, Hawaii, Co-Chairman CONRAD BURNS, Montana JOHN D. ROCKEFELLER IV, West Virginia TRENT LOTT, Mississippi JOHN F. KERRY, Massachusetts KAY BAILEY HUTCHISON, Texas BYRON L. DORGAN, North Dakota OLYMPIA J. SNOWE, Maine BARBARA BOXER, California GORDON H. SMITH, Oregon BILL NELSON, Florida JOHN ENSIGN, Nevada MARIA CANTWELL, Washington GEORGE ALLEN, Virginia FRANK R. LAUTENBERG, New Jersey JOHN E. SUNUNU, New Hampshire E. BENJAMIN NELSON, Nebraska JIM DEMINT, South Carolina MARK PRYOR, Arkansas DAVID VITTER, Louisiana LISA J. SUTHERLAND, Republican Staff Director CHRISTINE DRAGER KURTH, Republican Deputy Staff Director KENNETH R. NAHIGIAN, Republican Chief Counsel MARGARET L. CUMMISKY, Democratic Staff Director and Chief Counsel SAMUEL E. WHITEHORN, Democratic Deputy Staff Director and General Counsel LILA HARPER HELMS, Democratic Policy Director (II) VerDate 0ct 09 2002 15:35 Sep 19, 2006 Jkt 029917 PO 00000 Frm 00002 Fmt 5904 Sfmt 5904 S:\WPSHR\GPO\DOCS\29917.TXT JACKF PsN: JACKF C O N T E N T S Page Hearing held on January 24, 2006 ........................................................................ -

Twenty Questions on Twitter

Twenty Questions on Twitter Twenty questions on how to build your real estate business with Twitter.com by Natalie Danielson www.clockhours.com email: [email protected] A Washington State Approved Real Estate School for Clock Hour Education under R.C.W. 18.85. @clockhours Twenty Questions on Twitter Twenty Questions on how to build community and real estate relationships with Twitter.com Curriculum Session Major Objective Hours Topics 1 1. What is the history of Twitter.com? Understand the history, definition, ¼ hour 3. What is Twitter? and basics of the Twitter program as 5. Why Should I be on Twitter? it relates to the real estate industry 6. What is the Twitter Lingo? 2 5. Who follows who on Twitter? Identify some reasons to be on ½ hour 6. How do I Start a twitter Account? Twitter and the basics of 7. What are smart phone apps? communication on it. 8. What are desktop Applications to use? 9. How do I find people to follow on twitter? 3 10 How do I search keywords Discuss ways conversation happens 1 hour 11. What do I Tweet about? on twitter 12. What are hashtags? 13. How does Twitter connect with other sites? 4 14. How do you add links, photos and videos on Twitter? Learn about twitter applications that ½ hour 15. What are some common Twitter applications? make twitter more effective 16. What can you learn about the world on Twitter? including adding links 5 17. How much time does it take? Answer the most common questions 1/2 hour 18. Can Twitter help Real Estate agents build business? real estate agents have about blogs. -

G:\Chambers\MPT\OPINIONS\18-62 VAC-MPT Twitter Motion to Stay.Wpd

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE ) In re TWITTER, INC. SHAREHOLDER ) DERIVATIVE LITIGATION ) ) ) ) C.A. No. 18-62-VAC-MPT This Document Relates To: ) ) ALL ACTIONS. ) ) REPORT AND RECOMMENDATION I. INTRODUCTION This matter arises from plaintiffs Jim Porter, Ernesto Espinoza, and Francis Flemings’ (collectively, “Plaintiffs”) Verified Consolidated Shareholder Derivative Complaint1 against nominal defendant Twitter, Inc.. (“Twitter”) and defendants Richard Costolo, Anthony Noto, Jack Dorsey, Peter Fenton, David Rosenblatt, Marjorie Scardino, Evan Williams, Peter Chernin, and Peter Currie (collectively, “Defendants”), filed on April 19, 2017. The initial complaint was filed on October 24, 2016, followed by two other actions, with the three matters eventually consolidated and present operative complaint filed in the Northern District of California.2 The case was transferred to the 1 D.I. 33. 2 See D.I. 1, 21 and 33. In the interim between the filing of the initial complaint and the present operative amended complaint, the court entered an amended order which consolidated the three actions filed in the Northern District of California, appointed the lead plaintiff and lead counsel, and established a schedule to file a consolidated complaint. D.I. 11. As a result, 16-6136 (filed October 24, 2016), 16-6457 (filed November 4, 2016) and 16-6492 (filed November 8, 2016) were consolidated into 16-6136 (the “Derivative Action”). District of Delaware on January 8, 2018.3 The complaint alleges the issuance of false and misleading proxy statements in violation of Section 14(a) of the Securities Exchange Act of 1934 (the “Exchange Act”), breaches of fiduciary duties, unjust enrichment, corporate waste, and insider selling.4 On March 14, 2018, Defendants filed a motion to stay the Verified Consolidated Shareholder Derivative Complaint pending resolution of a related securities action in the Northern District of California.5 Presently before the court is Defendants’ motion to stay. -

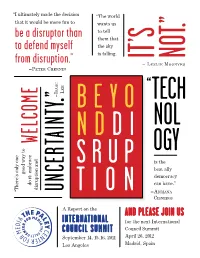

Be a Disruptor Than to Defend Myself from Disruption.”

“I ultimately made the decision “The world that it would be more fun to wants us be a disruptor than to tell them that to defend myself the sky is falling. from disruption.” IT’s NOT.” – Le s L i e Mo o n v e s –Pe t e r Ch e r n i n aac e e s i ” – L “ . BEYO TECH NOL WELCOME NDDI OGY SRUP is the best ally democracy can have.” disruption and UNCERTAINTY good way to do it: embrace “There’s only one TION –Ad r i A n A Ci s n e r o s A Report on the AND PLEASE JOIN US INTERNATIONAL for the next International COUNCIL SUMMIT Council Summit September 14, 15, 16, 2011 April 26, 2012 Los Angeles Madrid, Spain CONTENTS A STEP BEYOND DISRUPTION 3 | A STEP BEYOND DISRUPTION he 2011 gathering of The Paley Center for Me- Tumblr feeds, and other helpful info. In addi- dia’s International Council marked the first time tion, we livestreamed the event on our Web site, 4 | A FORMULA FOR SUCCESS: EMBRacE DISRUPTION in its sixteen-year history that we convened in reaching viewers in over 140 countries. Los Angeles, at our beautiful home in Beverly To view archived streams of the sessions, visit 8 | SNAPSHOTS FROM THE COCKTAIL PaRTY AT THE PaLEY CENTER Hills. There, we assembled a group of the most the IC 2011 video gallery on our Web site at http:// influential thinkers in the global media and en- www.paleycenter.org/ic-2011-la-livestream. -

TWITTER, INC. (Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE SECURITIES EXCHANGE ACT OF 1934 Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐ Check the appropriate box: ☐ Preliminary Proxy Statement ☐ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) ☒ Definitive Proxy Statement ☐ Definitive Additional Materials ☐ Soliciting Material Pursuant to §240.14a-11(c) or §240.14a-2 TWITTER, INC. (Name of Registrant as Specified In Its Charter) Payment of Filing Fee (Check the appropriate box): ☒ No fee required. ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ☐ Fee paid previously with preliminary materials. ☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: Table of Contents Table of Contents TWITTER, INC. -

“Over-The-Top” Television: Circuits of Media Distribution Since the Internet

BEYOND “OVER-THE-TOP” TELEVISION: CIRCUITS OF MEDIA DISTRIBUTION SINCE THE INTERNET Ian Murphy A dissertation submitted to the faculty at the University of North Carolina at Chapel Hill in partial fulfillment of the requirements for the degree of Doctor of Philosophy in the Department of Communication. Chapel Hill 2018 Approved by: Richard Cante Michael Palm Victoria Ekstrand Jennifer Holt Daniel Kreiss Alice Marwick Neal Thomas © 2018 Ian Murphy ALL RIGHTS RESERVED ii ABSTRACT Ian Murphy: Beyond “Over-the-Top” Television: Circuits of Media Distribution Since the Internet (Under the direction of Richard Cante and Michael Palm) My dissertation analyzes the evolution of contemporary, cross-platform and international circuits of media distribution. A circuit of media distribution refers to both the circulation of media content as well as the underlying ecosystem that facilitates that circulation. In particular, I focus on the development of services for streaming television over the internet. I examine the circulation paths that either opened up or were foreclosed by companies that have been pivotal in shaping streaming economies: Aereo, Netflix, Twitter, Google, and Amazon. I identify the power brokers of contemporary media distribution, ranging from sectors of legacy television— for instance, broadcast networks, cable companies, and production studios—to a variety of new media and technology industries, including social media, e-commerce, internet search, and artificial intelligence. In addition, I analyze the ways in which these power brokers are reconfiguring content access. I highlight a series of technological, financial, geographic, and regulatory factors that authorize or facilitate access, in order to better understand how contemporary circuits of media distribution are constituted. -

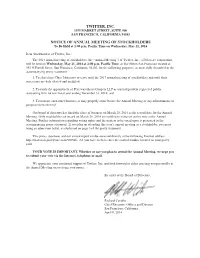

2014 Proxy Statement

TWITTER, INC. 1355 MARKET STREET, SUITE 900 SAN FRANCISCO, CALIFORNIA 94103 NOTICE OF ANNUAL MEETING OF STOCKHOLDERS To Be Held at 2:00 p.m. Pacific Time on Wednesday, May 21, 2014 Dear Stockholders of Twitter, Inc.: The 2014 annual meeting of stockholders (the “Annual Meeting”) of Twitter, Inc., a Delaware corporation, will be held on Wednesday, May 21, 2014 at 2:00 p.m. Pacific Time, at The Hilton San Francisco located at 333 O’Farrell Street, San Francisco, California, 94102, for the following purposes, as more fully described in the accompanying proxy statement: 1. To elect three Class I directors to serve until the 2017 annual meeting of stockholders and until their successors are duly elected and qualified; 2. To ratify the appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm for our fiscal year ending December 31, 2014; and 3. To transact such other business as may properly come before the Annual Meeting or any adjournments or postponements thereof. Our board of directors has fixed the close of business on March 28, 2014 as the record date for the Annual Meeting. Only stockholders of record on March 28, 2014 are entitled to notice of and to vote at the Annual Meeting. Further information regarding voting rights and the matters to be voted upon is presented in the accompanying proxy statement. If you plan on attending this year’s annual meeting as a stockholder, you must bring an admission ticket, as explained on page 3 of the proxy statement. This proxy statement and our annual report can be accessed directly at the following Internet address: http://materials.proxyvote.com/90184L. -

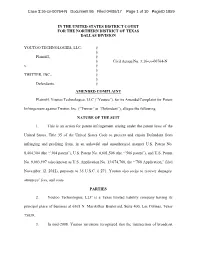

Case 3:16-Cv-00764-N Document 86 Filed 04/06/17 Page 1 of 10 Pageid 1859

Case 3:16-cv-00764-N Document 86 Filed 04/06/17 Page 1 of 10 PageID 1859 IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF TEXAS DALLAS DIVISION YOUTOO TECHNOLOGIES, LLC, § § Plaintiff, § § Civil Action No. 3:16-cv-00764-N v. § § TWITTER, INC., § § Defendants. § AMENDED COMPLAINT Plaintiff, Youtoo Technologies, LLC (“Youtoo”), for its Amended Complaint for Patent Infringement against Twitter, Inc. (“Twitter” or “Defendant”), alleges the following: NATURE OF THE SUIT 1. This is an action for patent infringement arising under the patent laws of the United States, Title 35 of the United States Code to prevent and enjoin Defendant from infringing and profiting from, in an unlawful and unauthorized manner U.S. Patent No. 8,464,304 (the “’304 patent”), U.S. Patent No. 8,601,506 (the “’506 patent”), and U.S. Patent No. 9,083,997 (also known as U.S. Application No. 13/674,768, the “’768 Application,” filed November 12, 2012), pursuant to 35 U.S.C. § 271. Youtoo also seeks to recover damages, attorneys’ fees, and costs. PARTIES 2. Youtoo Technologies, LLC is a Texas limited liability company having its principal place of business at 6565 N. MacArthur Boulevard, Suite 400, Las Colinas, Texas 75039. 3. In mid-2008, Youtoo inventors recognized that the intersection of broadcast Case 3:16-cv-00764-N Document 86 Filed 04/06/17 Page 2 of 10 PageID 1860 television and Social Networking was the next great horizon with respect to technology and communication. In order meet the growing public and corporate demand for a user- and network-friendly, reliable interactive television experience, Youtoo invested millions of dollars into the creation, design, and testing of its pioneering technology.