GTC-ONE-Minute-Brief-19.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Success Stories: Ideas for Potential Players SAINT-GOBAIN K.K

Success Stories: Ideas for Potential Players MFManufacturing Saint-Gobain as a group is number one worldwide in Sales / Services SAINT-GOBAIN K.K. industrial ceramics, plastics, abrasives, reinforcement Japan brings new vitality to centuries materials, refractory products, gypsum and cast iron of success pipe, number two in glass containers and number three in flat glass. Now among the world’s hundred leading industrial corporations, its workforce numbers more than 200,000, including subsidiaries and partner firms. Among the 55 countries in which the group is established, however, few are more important than Japan—one of the largest, most advanced economies on Earth, and one where competition in the material and high-technology markets is harshest. Although Saint- Gobain has been doing business in Japan since 1917, it has been particularly strong since the 1970s in merging with companies there in order to share technologies and distribution channels for flat glass, and other high- performance materials. The Japanese affiliate was formally established in 1975. Japan is also home to Saint-Gobain Asia-Pacific General Delegation Office, employing about 600 staff members in Saint Gobain K.K.’s headquarters in Tokyo, built in 2000. the fields of building and automotive glass, glass fiber, ceramics, plastics and abrasives, and providing leading- A worldwide leader in the materials and high-tech edge products and technical services. industries, Saint-Gobain is renowned as an innovator, producer and distributor of glass, ceramics, plastics, cast The construction sector has suffered as much as any in iron, and other materials. This multinational group has Japan’s post-bubble market and persistent economic been developing products for 340 years and now downturn. -

Nippon Sheet Glass Co., Ltd

Nippon Sheet Glass Co., Ltd. Strategy of Post-Transaction July 6, 2006 Combination creates a leading global player in a growth industry + (C) Nippon Sheet Glass Co., Ltd. All Rights Reserved. 2 Global Flat Glass Market Global Market ≅ 37 million tonnes (4.4 billion sq. m) Building Products 33 m tonnes - Automotive 4m tonnes Of which – 24 million = high quality float glass – 3 million = sheet – 2 million = rolled – 8 million = lower quality float (mostly China) Global Value At primary manufacture level ≅ €15 billion At processed level ≅ €50 billion (C) Nippon Sheet Glass Co., Ltd. All Rights Reserved. 3 Flat Glass- A Growth Industry 200 2005: 5.2% Glass Demand - 3.9% p.a. 150 2003: 4.2% 2005: 3.0% 2003: 2.1% 100 Real GDP - 2.6% p.a. Index (1991 = 100) (1991 Index 50 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 [1]: Global GDP has accelerated Calendar Year [2]: Glass demand has increased faster [3]: China is driving global growth Global Float/Sheet Demand Growth (C) Nippon Sheet Glass Co., Ltd. All Rights Reserved. 4 Glass Growth Drivers Buildings Automotive Energy Saving (Heating) Complexity Energy Saving (Cooling) – Curvature Safety – Surface Tolerance Solar Control Security Security Fire Protection Glazing System Acoustic Self-Cleaning Glass (C) Nippon Sheet Glass Co., Ltd. All Rights Reserved. 5 Global Flat Glass Industry Europe, China and North America together account for 75 per cent of global demand for glass. NSG+Pilkington, Asahi, Saint-Gobain, and Guardian, produce 61 per cent of the world's high quality float glass. -

'Making a Difference to Our World Through Glass Technology' to Our Shareholders

‘Making a difference to our world through glass technology’ Nippon Sheet Glass Co., Ltd. Head Office: Sumitomo Fudosan Mita Twin Building West Wing, 5-27, Mita 3-chome, Minato-ku, Tokyo 108-6321 Japan To our shareholders Telephone: +81-3-5443-9500 Contact: www.nsggroup.net/contact Nippon Sheet Glass Co., Ltd. 145th Fiscal Period Interim Report www.nsg.com 1 April 2010 – 30 September 2010 01 NSG GROUP To our shareholders NSG GROUP To our shareholders 02 Contents Consolidated financial highlights Message from the President and CEO Fiscal 2010 Fiscal 2011 01 Consolidated financial highlights On behalf of the NSG Group, I thank you for your continued support. Millions of yen Fiscal 2009 Fiscal 2010 interim period interim period 02 Message from the President and CEO I am pleased to present the interim report for the period ended 03 Interview with the President Net sales 739,365 588,394 292,989 293,689 30 September 2010. 06 Business summary by segment Operating income 1,908 (17,183) (16,222) 10,473 07 Review of operations The results for the first half of the financial year FY2011 reflect 09 Consolidated financial statements Ordinary income (12,259) (28,552) (24,743) 6,543 improving volumes, and in some cases prices, in our major 11 Management Net income (28,392) (41,313) (26,248) 15 markets. In addition, they reflect the benefits of the Group’s 12 Stock information Net income per share (yen) (42.49) (65.61) (41.00) (1.31) restructuring programs, which have helped to reduce overheads 13 Shareholder information and to improve operational efficiencies, together with important 14 Corporate data contributions by our joint ventures and associate companies. -

2019 Investment Stewardship Annual Report

2019 Investment Stewardship Annual Report August 2019 Annual Report Navigating long-term change – 3 Active the year in review 2018-2019 Investment Stewardship 4 stewardship: highlights creating long- Our achievements 5 Our principles, guidelines, priorities, 7 term value and commentaries The Investment Stewardship Engagement and voting case studies 10-22 Annual Report provides an • Board quality and effectiveness remain overview of BlackRock’s approach our primary focus • Corporate strategy and capital allocation to corporate governance and • Executive compensation stewardship in support of long- • Environmental risk and opportunities term value creation for our clients. • Human capital management as an In this report we provide practical investment issue examples of the BlackRock Spotlight on activism 23 Investment Stewardship (BIS) Engagement and voting statistics 24 team’s work over the year, Investor perspective and public policy 25 distilling some of the trends and Industry affiliations and memberships 28 company-specific situations reported in our regional quarterly Appendix reports. We emphasize the List of companies engaged 31 outcome of our engagements with BlackRock’s 2019 PRI assessment 38 companies, including some which report and score have spanned several years. We also provide examples of where we have contributed to the public discourse on corporate Our Annual Report reporting period is July 1, 2018 to June 30, 2019, representing the Securities and Exchange governance and investment Commission’s (SEC) 12-month reporting period for US mutual funds, including iShares. stewardship. Navigating long-term change – the year in review The adage “change is the only constant” has never been more true than in the past year. -

Glazing at the Tokyo Motor Show

Automotive glazing Glazing at the Tokyo Motor Show (first part) The first part of this report on the Tokyo Motor Show highlights the technological innovations achieved by Japanese automotive producers regarding environmentally friendly cars. The author then goes on to analyse in detail the glazing trends which emerged at the exhibition. The most evident of these was: the increased use of privacy glass for rear lateral and backlight windows, reduced UV penetration for solar control, water repellent coating on front lateral windows, and special combiners for HUD on the windscreen. Giovanni Manfré* MG CONSULT ntroduction At the Tokyo Motor Show (TMS), Current Japanese vehicle pro- automotive glazing trends were clearly revealed duction shows a decrease in the as strongly connected with the turn cars are domesticI market as opposed to an increase in taking. These trends can be summarized in the the foreign market. Japan has seen the following points for Japanese glassmakers: internationalization and globalization of its • from the solar control point of view, glazing production of car parts, including its is tending more and more towards UV automotive glazing. Some Japanese companies blocking and the use of privacy glasses, are working together with foreign firms: Asahi which have seen a great increase in Glass with Glaverbel, Nippon Sheet Glass with production. In addition, automakers are still Pilkington LOF, and Central Glass is looking very interested in heat insulation; for partnership to acquire foreign technologies. • water repellent glasses are currently the most Meanwhile, the imported car market in Japan is innovative as far as glazing is concerned, continuing to grow. -

List of Donor Companies: Business Sector Emergency Donation for Earthquake Victims in Central Java, Indonesia, on May 27, 2006 (In Alphabetical Order of Companies)

List of Donor Companies: Business Sector Emergency Donation for Earthquake Victims in Central Java, Indonesia, on May 27, 2006 (in alphabetical order of companies) As of August 25, 2006 Nippon Keidanren Total amount contributed: \1,621,520,000.- Nippon Keidanren has been instrumental in soliciting business sector funds when disasters hit hard various parts of the world in the past. On May 27, 2006, central part of Java Island, Indonesia, was struck by a heavy earthquake, claiming more than 5,000 human lives and injuring almost 40,000, creating over 400,000 refugees and causing damages to more than 500,000 houses. Believing that the damages there were extensive, Nippon Keidanren initiated fund raising activities and provided solicited funds and goods such as tents and water purifiers for Indonesian people through Red Cross and NPOs under the auspice of the Japan Platform. Following is the list of donor companies that provided funds and goods through Nippon Keidanren and / or independently. 1 ABB K.K. 40 BOSCH CORPORATION 79 DAIWA HOUSE INDUSTRY CO.,LTD. 2 ACOM CO.,LTD. 41 BRIDGESTONE CORPORATION 80 DAIWA SECURITIES GROUP INC. 3 ADEKA CORPORATION 42 BROTHER INDUSTRIES,LTD. 81 DAIWABO COMPANY LIMITED 4 ADVANEX INC. 43 BUNKYODO CO.,LTD. 82 DENKI KAGAKU KOGYO K.K. 5 ADVANTEST CORPORATION 44 BUSINESS CONSULTANTS,INC. 83 DENSO CORPORATION 6 AEON 45 CALBEE FOODS CO.,LTD. 84 DENTSU INC. 7 AICHI STEEL CORPORATION 46 Canon Group 85 DHC CORPORATION 8 AICHI TOKEI DENKI CO.,LTD. 47 CAPCOM CO.,LTD. 86 DOWA MINING COMPANY,LTD. 9 AIFUL CORPORATION 48 CASIO COMPUTER CO.,LTD. -

DOT No. MANUFACTURER NAME CITY STATE COUNTRY 1 SUPERGLASS S.A

DOT No. MANUFACTURER NAME CITY STATE COUNTRY 1 SUPERGLASS S.A. EL TALAR TIGRE BS.AS. ARGENTINA 2 J-DAK, INC. SPRINGFIELD TN UNITED STATES 3 SACOPLAST S.R.L. OTTIGLIO ALESSANDRIA ITALY 4 SOMAVER AIN SEBAA CASABNLANCA MOROCCO 5 JIANGUIN JINGEHENG HIGH-QUAL. DECORATING GLASS WORKS JIANGUIN JIANGSU PROVINCE CHINA 6 BASKENT GLASS COMPANY SINCAN ANKARA TURKEY 7 POLPLASTIC SPA DOLO VENEZIA ITALY 8 CEE BAILEYS #1 MONTEBELLO CA 9 VIDURGLASS MANBRESA BARCELONA SPAIN 10 VITRERIE APRIL, INC. P.A.T. MONREAL QUEBEC CANADA 11 SPECTRA INC. MILWAUKEE WI 12 DONG SHIN SAFETY GLASS CO., LTD. BOOKILMEON, JEONNAM KOREA 13 YAU BONG CAR GLASS CO., LTD. ON LOK CHUEN, NEW TERRITORIES HONG KONG 14 WITHDRAWN - SEE COMMENTS 15 LIBBEY-OWENS-FORD CO TOLEDO OHIO UNITED STATES 16 HAYES-ALBION CORPORATION JACKSON MISSISSIPPI UNITED STATES 17 PILKINGTON AUTOMOTIVE (UK) LTD. BIRMINGHAM ENGLAND 18 PPG INDUSTRIES PITTSBURGH PENNSYLVANIA UNITED STATES 19 PPG CANADA INC.,DUPLATE DIVISION OSHAWA ONTARIO CANADA 20 ASAHI GLASS CO LTD TOKYO JAPAN 21 CHRYSLER CORP DETROIT MICHIGAN UNITED STATES 22 GUARDIAN INDUSTRIES CORP AUBURN HILLS MICHIGAN UNITED STATES 23 NIPPON SHEET GLASS CO. LTD OSAKA JAPAN 24 AGC AUTOMOTIVE EUROPE SA GILLY BELGIUM 25 PILKINGTON AUTOMOTIVE DEUTSCHLAND GMBH WITTEN GERMANY 26 CORNING GLASS WORKS CORNING NEW YORK UNITED STATES 27 SAINT-GOBAIN SEKURIT-DEUTSCHLAND GMBH CO. KG AACHEN GERMANY 28 WITHDRAWN - SEE COMMENTS 29 WITHDRAWN - SEE COMMENTS 30 WITHDRAWN - SEE COMMENTS 31 WITHDRAWN - SEE COMMENTS 32 SAINT-GOBAIN SEKURIT BENELUX S.A. SAMBREVILLE BELGIUM 33 LAMINATED GLASS CORPORATION DETROIT MICHIGAN UNITED STATES 34 WITHDRAWN - SEE COMMENTS 35 PREMIER AUTOGLASS CORPORATION LANCASTER OHIO UNITED STATES 36 PILKINGTON SIV S.P.A., ITALY SAN SALVO (CHIETI) ITALY 37 SAINT-GOBAIN SEKURIT ITALIA S.R.L. -

NSG Group and the Flat Glass Industry 2011 NSG Group and the Flat Glass Industry 2011

NSG Group and the Flat Glass Industry 2011 NSG Group and the Flat Glass Industry 2011 Legal Notice This document is intended as a briefing on the glass industry and the position within it of the NSG Group’s businesses. The content of the publication is for general information only, and may contain non-audited figures. Every care has been taken in the preparation of this document, but Nippon Sheet Glass Co Ltd., accepts no liability for any inaccuracies or omissions in it. Nippon Sheet Glass Co Ltd. makes no representations or warranties about the information provided within the document and any decisions based on information contained in it are the sole responsibility of the user. No information contained in this document constitutes or shall be deemed to constitute an invitation to invest or otherwise deal in shares in Nippon Sheet Glass Co Ltd. © 2011 Nippon Sheet Glass Co., Ltd. 2 NSG Group and the Flat Glass Industry 2011 Introduction 04 Introductory note and definitions Contents 05 Executive summary Global flat glass industry and market structure Industry & Market structure 08 Total world market for flat glass 08 Routes to market 09 Industry economics 10 Global players and market shares 11 World float/sheet glass markets 16 Automotive markets Glass – a growth industry Glass industry growth 23 Global demand for flat glass 28 Growth in Building Products 30 Growth in Automotive NSG Group – a glass industry leader NSG Group Overview 37 Corporate overview 38 Business profile 42 Building Products overview 49 Automotive overview 55 Sustainability 58 Glass manufacture Manufacturing 63 NSG Group and associates' float lines NSG Group and the Flat Glass Industry 2011 3 Introductory Note and Definitions The objective of this publication is to provide The Pilkington brand mark background information on the world’s flat glass industry and, as an industry leader, the position within it of the NSG Group. -

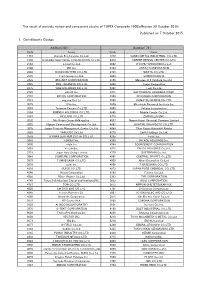

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Calling on the Japanese Government to Raise Its 2030 Renewable Energy Target to 40-50%

18th January 2021 Calling on the Japanese government to raise its 2030 renewable energy target to 40-50% With commitments by EU countries, Japan, South Korea, Canada, New Zealand, and with the United States intending to join this year, ‘carbon neutral by 2050’ has become a common goal of more than 120 countries around the globe. Key to meeting the goal is the promotion of a rapid and significant expansion of renewable energy along with improvements in energy efficiency. EU countries and U.S. states have already set progressive goals to be reached by 2030, ranging from 40-74% share in each electricity mix. In contrast, Japan’s target shares of renewable energy for fiscal 2030 electricity mix is 22- 24%. In order for Japan to meet its responsibilities to be one of the leaders in global efforts, the target needs to be much more ambitious. An ambitious target will stimulate renewable energy deployment, and Japanese companies will be able to play a greater role in the global business environment, where decarbonization is accelerating. It will enable Japanese companies more committed to the challenge of mitigating the climate crisis. We, as part of the global business community, call for the renewable energy target for fiscal 2030 to be revised from 22-24% to 40-50% in the next Strategic Energy Plan formulated this year. Signatories (alphabetical order) (Total 92 companies) ADVANTEST CORPORATION DAIICHI SANKYO COMPANY, LIMITED AEON CO., LTD. Daito Trust Construction Co., Ltd. Ajinomoto Co., Inc. Daiwa House Industry Co., Ltd. AMITA HOLDINGS CO., LTD. Eisai Co., Ltd. ANA HOLDINGS INC. -

Survey of Integrated Reports in Japan 2018

Survey of Integrated Reports in Japan 2018 Integrated Reporting Center of Excellence KPMG in Japan March 2019 home.kpmg/jp Message from global thought leaders In this, the fifth year this survey report has been issued, KPMG has solicited the observations of thought leaders on corporate reporting. Japanese businesses pride themselves on a longer-term focus compared to the rest of the world, where prioritizing short-term gains has too often become the norm. Focusing on long-term value creation and taking into account all of the resources an organization uses is the sustainable, profitable, and proven way to manage a business. Many Japanese businesses are just beginning to implement integrated thinking and reporting. The findings in this report show that senior management must take ownership to spread integrated thinking in their businesses – not just in accounting but in strategy, operations, marketing, and the rest of the company as well. This report makes me optimistic and excited for Japanese business leaders as they strive to think, act, and communicate in an integrated and sustainable way. Dominic Barton ― International Integrated Reporting Council, Chairman Integrated Reporting improves communication between companies and investors and where most effective, sets the stage for enhanced corporate value creation over the mid to long-term. Investors desire integrated reports which provide comprehensive information disclosure useful for making investment decisions. The International Corporate Governance Network (ICGN) has encouraged integrated reporting for many years. In 2015, ICGN s Disclosure and Transparency Committee ’ released Guidance on Integrated Business Reporting. The Guidance amplifies that strategic decisions should be based on factors that are broader than those reflected in the financial statements. -

To Our Shareholders Nippon Sheet Glass Co., Ltd

TO OUR SHAREHOLDERS NIPPON SHEET GLASS CO., LTD. 153RD FISCAL PERIOD INTERIM REPORT 1 APRIL 2018 – 30 SEPTEMBER 2018 Working together for another century of progress Securities Code: 5202 Summary of the First Half-Year of FY2019 NSG Group’s revenues and profits in the first two quarters improved from the previous year. Revenues and operating profits increased respectively by 5 percent year-on-year to ¥308.1 billion and by 1 percent to ¥17.9 billion. Profits attributable to owners of the parent significantly improved by 94 percent to ¥9.3 billion. The market environment remained brisk, particularly in Europe, thanks to which VA (value-added) products including those for solar glass application continue to show expansion. The turnaround of the results, including those of Automotive Glass in Europe and Technical Glass, have more than offset the increased costs of raw materials, etc., and have contributed to the improved results of the first two quarters of FY2019. Taking account of the business results that have continued to progress in line with our plan, the Board of Directors has resolved to pay centennial commemorative dividends (ten yen per share) as interim dividends, as scheduled. We will continue to make efforts to distribute dividends continually, as we adopt the basic policy of profit allocation that we declare dividends in a stable manner, with sustainable business results as the basis. MESSAGE FROM The Board has further resolved to redeem part of the THE PRESIDENT AND CEO Class A shares. The decision was made, with a view to help funding cost reduction, as well as considering that On behalf of the NSG Group, I sincerely our profits have been continuously improving and that our current financial condition has become generally stable.