Logistics Market Spotlight Q2 2020.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Logistics Property Handbook 4.0 Investment & Financing Keys Spain 2019

The Logistics Property Handbook 4.0 Investment & Financing Keys Spain 2019 June 2019 Financial Advisory I Real Estate @ 2019 Deloitte Financial Advisory Investment & Financing Market All time record of Take-up figures, where the 6 In spite of the 11% decrease in the logistics rd 3 ring reaches a share of 56% of the total absorbed surface: investment volume in Spain during 2018, the Take–Up: 950.000 sqm (7% YOY 2017-2018). logistics trend continues at highest “Prime Yield: 5.0% (-800bps YOY 2017-2018 and “levels in comparison with the recent years. -1,000bps YOY 2006-2018). Financial terms and conditions in 2018 Prime Rent: €6.60 sqm (6.4% YOY 2017-2018). have remained similar to 2017. Lease KPIs: Supply & Demand Sustainability in Catalonia 7 4A 59% increase of Take-up that encourage the Forecast for 2019 indicates that logistics is & Construction number of speculative projects as future supply: in a sharp rising trend. Despite the Spanish Sustainability has become a must economy shows signs of deceleration, it Take–Up: 715.000 sqm (59% YOY 2017-2018). in the current logistics market. Taking into “is well above the European average. Spain is still “Prime Yield: 5.0% (-700bps YOY 2017-2018 and account every relevant point for new attracting high levels of equity and remains as a -1,000bps YOY 2006-2018). “warehouse developments is key to avoid high attractive market. Prime Rent: €7.00 sqm (3.7% YOY 2017-2018). unexpected costs and leasing limitations. Lease KPIs: Market Supply & Demand Incoming 5in Valencia Trends Spain benefits from its privileged location where Increasing activity since Q1 2019 Take–Up figures 8 We believe that the traditional logistics two of the European leading corridors accounts for 60% of 2018 total leased area. -

Pozuelo De Alarcón, Boadilla Del Monte and Las Rozas De Madrid, Lead, Once Again, the List of Municipalities with the Highest Annual Average Net Income Per Capita

29 May 2019 Urban Indicators Edition 2019 Pozuelo de Alarcón, Boadilla del Monte and Las Rozas de Madrid, lead, once again, the list of municipalities with the highest annual average net income per capita Madrid and Barcelona concentrate the 10 neighborhoods with the highest income per capita in Spain Melilla registers 2.34 children per woman, the highest value, and San Cristóbal de la Laguna the lowest level with 0.97 The “Urban Indicators” project consists of a selection and adaptation of the content of the European “Urban Audit” project, currently known as "data collection for sub-national statistics (mainly cities)". It collects information on living conditions in the main cities of the European Union and the candidate countries. Annual average net income Considering the 405 municipalities with more than 20,000 inhabitants and the annual average net income per capita in 2016, the three cities with the highest income belonged to Comunidad de Madrid: Pozuelo de Alarcón (25.957 euros), Boadilla del Monte (19.702 euros) and Las Rozas de Madrid (19.40 euros). On the other hand, the cities with the lowest income per capita were Níjar (Almería), with 6.253 euros, Los Palacios y Villafranca (Sevilla), with 6.550 euros, and Alhaurín el Grande (Málaga), with 6.629 euros. Urban Indicators - Edition 2019 (1/9) List of municipalities according to average annual net income per habitant. Year 2016 Highest income Lowest income Pozuelo de Alarcón 25.957 Níjar 6.253 Boadilla del Monte 19.702 Palacios y Villafranca, Los 6.550 Rozas de Madrid, Las 19.340 -

Disposición 2295 Del BOE Núm. 39 De 2021

BOLETÍN OFICIAL DEL ESTADO Núm. 39 Lunes 15 de febrero de 2021 Sec. III. Pág. 17582 III. OTRAS DISPOSICIONES MINISTERIO DE LA PRESIDENCIA, RELACIONES CON LAS CORTES Y MEMORIA DEMOCRÁTICA 2295 Resolución de 9 de febrero de 2021, de la Subsecretaría, por la que se publica el Convenio entre la Mutualidad General de Funcionarios Civiles del Estado, el Instituto Social de las Fuerzas Armadas, la Mutualidad General Judicial y el Servicio de Salud de Castilla-La Mancha, para la prestación en zonas rurales de determinados servicios sanitarios a los mutualistas y demás beneficiarios adscritos a entidades de seguro de asistencia sanitaria concertada con dichas mutualidades. La Directora General de la Mutualidad General de Funcionarios Civiles del Estado, el Secretario General Gerente del Instituto Social de las Fuerzas Armadas, el Gerente de la Mutualidad General Judicial y la Directora Gerente del Servicio de Salud de la Comunidad Autónoma de Castilla-La Mancha, han suscrito un Convenio para la prestación en zonas rurales de determinados servicios sanitarios a los mutualistas y demás beneficiarios adscritos a entidades de seguro de asistencia sanitaria concertada con dichas mutualidades. Para general conocimiento, y en cumplimiento de lo establecido en el artículo 48.8 de la Ley 40/2015, de 1 de octubre, de Régimen Jurídico del Sector Público, dispongo la publicación en el «Boletín Oficial del Estado» del referido Convenio como anejo a la presente Resolución. Madrid, 9 de febrero de 2021.–El Subsecretario de la Presidencia, Relaciones con las Cortes y Memoria Democrática, Antonio J. Hidalgo López. ANEJO Convenio entre la Mutualidad General de Funcionarios Civiles del Estado, el Instituto Social de las Fuerzas Armadas, la Mutualidad General Judicial y el Servicio de Salud de Castilla-La Mancha para la prestación en zonas rurales de determinados servicios sanitarios a los mutualistas y demás beneficiarios adscritos a entidades de seguro de asistencia sanitaria concertada con dichas mutualidades 26 de enero de 2021. -

GUADALAJARA Municipio N.º Casos Nombre N.º Habitantes Semana 29

GUADALAJARA Municipio N.º Casos Semana 29 Semana 30 Nombre N.º Habitantes (19-25 julio) (26-1 agosto) Abánades 53 0 0 Ablanque 55 0 0 Adobes 35 0 0 Alaminos 58 0 0 Alarilla 137 0 0 Albalate de Zorita 930 0 2 Albares 513 0 2 Albendiego 50 0 0 Alcocer 328 0 0 Alcolea de las Peñas 14 0 0 Alcolea del Pinar 327 1 0 Alcoroches 127 0 0 Aldeanueva de 0 0 Guadalajara 86 Algar de Mesa 55 0 1 Algora 66 2 2 Alhóndiga 161 0 0 Alique 14 0 0 Almadrones 55 0 0 Almoguera 1.300 0 3 Almonacid de Zorita 696 1 2 Alocén 161 0 0 Alovera 12.860 27 15 Alustante 155 2 0 Angón 7 0 0 * El número de casos de cada semana refleja los nuevos casos positivos contabilizados en ese periodo de tiempo. No es un dato acumulado. GUADALAJARA Municipio N.º Casos Semana 29 Semana 30 Nombre N.º Habitantes (19-25 julio) (26-1 agosto) Anguita 155 0 0 Anquela del Ducado 46 0 0 Anquela del Pedregal 29 0 0 Aranzueque 358 0 3 Arbancón 149 1 4 Arbeteta 20 0 0 Argecilla 59 0 0 Armallones 54 0 0 Armuña de Tajuña 229 2 1 Arroyo de las Fraguas 21 0 0 Atanzón 97 0 0 Atienza 385 5 1 Auñón 134 0 2 Azuqueca de Henares 35.407 80 51 Baides 56 0 0 Baños de Tajo 18 0 0 Bañuelos 13 0 0 Barriopedro 15 0 0 Berninches 52 0 0 Bodera (La) 23 0 0 Brihuega 2.378 8 1 Budia 189 0 1 Bujalaro 50 0 0 Bustares 74 0 0 * El número de casos de cada semana refleja los nuevos casos positivos contabilizados en ese periodo de tiempo. -

Humanes De Madrid

MADRID HUMANES DE MADRID HORARIO DE FRANQUICIA: De 8 a 14 h y de 15:45 a 20 h. Sábados cerrado, sólo entregas domiciliarias. 902 300 400 RECOGIDA Y ENTREGAS EN LOCALIDADES SIN CARGO ADICIONAL DE KILOMETRAJE SERVICIOS DISPONIBLES Batres Griñón Serranillos del Valle SERVICIO URGENTE HOY/URGENTE BAG HOY. RECOGIDAS Y ENTREGAS, CONSULTAR CON SU FRANQUICIA. Cubas (Madrid) Moraleja de Enmedio SERVICIO URGENTE 8:30. RECOGIDAS: Mismo horario del Servicio Urgente 10. ENTREGAS EN DESTINO: El día laborable siguiente antes RECOGIDAS Y ENTREGAS (De Hoy para Hoy). En estas plazas y su área sin cargo adicional de las 8:30 h** (Consultar destinos). de kilometraje (consulte la página de la Franquicia). (+)Más de una frecuencia diaria. SERVICIO URGENTE 10. RECOGIDAS: Límite en esta Franquicia 20 h + MADRID * Sant Joan Despí Carolina, La destino Andorra, España, Gibraltar y Portugal. ENTREGAS EN + Alcalá de Henares * Sant Just Desvern Linares DESTINO: El día laborable siguiente a primera hora de la mañana en + Alcobendas * Sant Sadurní d’Anoia Martos + Alcorcón * Sant Vicenç de Castellet Úbeda Andorra, España, Gibraltar y Portugal. En esta Franquicia de 8 a 10 h*. Aranjuez * Sta. Coloma Gram. Villacarrillo SERVICIO URGENTE 12/URGENTE 14/DOCUMENTOS 14/ + Arganda del Rey * Sta. Margarida i els M. LEÓN URGENTE BAG14. RECOGIDAS: Mismo horario del Servicio Urgente + Boadilla del Monte * Sitges Bañeza, La + Collado-Villalba * Terrassa Cistierna 10. ENTREGAS EN DESTINO: El día laborable siguiente antes de las + Coslada * Tordera Ponferrada 12 h** (Urgente 12) o 14 h** (Urgente 14/Documentos 14/Urgente + Fuenlabrada * Torelló Valencia Don Juan BAG14) (Consultar destinos). + Getafe * Vic Villablino + Leganés * Viladecans LOGROÑO SERVICIO URGENTE 19. -

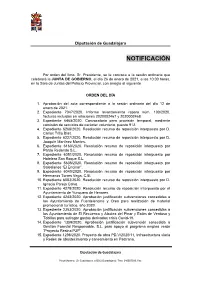

Notificación

Diputación de Guadalajara NOTIFICACIÓN Por orden del Ilmo. Sr. Presidente, se le convoca a la sesión ordinaria que celebrará la JUNTA DE GOBIERNO, el día 26 de enero de 2021, a las 10:00 horas, en la Sala de Juntas del Palacio Provincial, con arreglo al siguiente ORDEN DEL DÍA 1. Aprobación del acta correspondiente a la sesión ordinaria del día 12 de enero de 2021. 2. Expediente 7047/2020. Informe levantamiento reparo núm. 100/2020, facturas incluidas en relaciones 2020002467 y 2020002468. 3. Expediente 6465/2020. Convocatoria para provisión temporal, mediante comisión de servicios de carácter voluntario, puesto 912. 4. Expediente 6268/2020. Resolución recurso de reposición interpuesto por D. Carlos Trillo Blas. 5. Expediente 6227/2020. Resolución recurso de reposición interpuesto por D. Joaquín Martínez Montes. 6. Expediente 6160/2020. Resolución recurso de reposición interpuesto por Pardo Redondo S.L. 7. Expediente 6051/2020. Resolución recurso de reposición interpuesto por Hotelera San Roque S.L. 8. Expediente 5638/2020. Resolución recurso de reposición interpuesto por Salesianos “El Encinar”. 9. Expediente 6040/2020. Resolución recurso de reposición interpuesto por Hermanos Torres Vega, C.B. 10. Expediente 6083/2020. Resolución recurso de reposición interpuesto por D. Ignacio Pareja Calvo. 11. Expediente 4278/2020. Resolución recurso de reposición interpuesto por el Ayuntamiento de Yunquera de Henares. 12. Expediente 4243/2020. Aprobación justificación subvenciones concedidas a los Ayuntamiento de Fuentelencina y Orea para realización de material promocional turístico, año 2020. 13. Expediente 2353/2020. Aprobación justificación subvenciones concedidas a los Ayuntamiento de El Recuenco y Alcolea del Pinar y Eatim de Ventosa y Tobillos para sufragar gastos derivados crisis Covid-19. -

PLANO CALLE San Fernando De Henares

Daganzo de Arriba PLANO AjalvirCALLE Paracuellos de Jarama San Fernando de Henares Alcalá de Henares Torrejón de Ardoz Barajas Madrid Villalbilla San Blas - Canillejas Torres de la Alameda Coslada San Fernando de Henares Vicálvaro Mejorada del Campo Loeches Rivas-Vaciamadrid Velilla de San Antonio 2020 ESQUEMA DE DISTRIBUCIÓN DEL CALLEJERO POR PLANOS San Fernando de Henares Ajalvir Paracuellos de Jarama Alcalá de Henares Barajas Torrejón de Ardoz Madrid Mapa II Polígono de San Fernando de Henares Villalbilla Las Castellanas San Blas - Canillejas Torres de la Alameda Mapa IV Coslada Soto de Aldovea Mapa III San Fernando de Henares San Fernando de Henares Mapa I Vicálvaro Mejorada del Campo Loeches Rivas-Vaciamadrid Velilla de San Antonio 2020 San Fernando de Henares Indice de calles y su situación en el mapa Numeración Literal de Vía Desde Hasta Mapa Hojas Calle Adolfo Pérez Esquivel I E4 Calle Adolfo Pérez Esquivel 1 33 I E4 Calle Adolfo Pérez Esquivel 2 30 I E4 Calle Álava 1 3 I D4 Calle Álava 2 20 I D4 Calle de Albert Camus 1 63 I E4 Avda Albert Einstein I E5 Avda Albert Einstein 2 76 I E5 Calle de Albino Pérez Ayestarain I B2 Calle de Albino Pérez Ayestarain 1 11 I B3 Calle de Albino Pérez Ayestarain 2 10 I B3 Calle de Albino Pérez Ayestarain 40 40 I B2 Calle de Albino Pérez Ayestarain 41 43 I B2 Calle de Albino Pérez Ayestarain 66 70 I B2 Avda de Algorta 4 4 I E5 Avda de Algorta 6 14 I D5 Avda de Algorta 13 17 I E5 Avda de Algorta 27 31 I D5 Calle de los Alperchines I C2 Calle de los Alperchines 12 26 I C2 Calle de los Alperchines -

Calendario De Competición

Federación de Baloncesto de Madrid 19/20 29/07/2019 COMPETICIÓN: COMPETICIONES FEDERADAS FBM CATEGORÍA: 1ª División Nac. Masculina FASE: PRIMERA GRUPO: IMPAR CALENDARIO DE COMPETICIÓN EQUIPO POBLACIÓN PROV DÍA HORA COLOR COLOR CAMPO DE JUEGO 1 2 PINTOBASKET CORREA DENTAL Pinto Madrid D 00:00 NARANJA BLANCO PRINCIPES DE ASTURIAS, :00 PABELLON NOVUM ENERGY LICEO FRANCES Madrid Madrid S 20:00 AZUL BLANCO CAMPUS SUR UNIV. :00 POLITECNICA ADC BOADILLA Boadilla del Monte Madrid S 20:30 VERDE BLANCO REY FELIPE VI, PABELLON :00 NCS ALCOBENDAS Alcobendas Madrid D 00:00 ROJO AMARILL PEDRO FERRANDIZ, PABELLON :00 O COSLADA C.B. - PLURAL ASESORES Coslada Madrid S 19:00 BLANCO ROJO EL PLANTIO, PABELLON :00 INGESCASA BALONCESTO TRES Madrid Madrid S 20:30 MORADO BLANCO LA LUZ, PABELLON (Pista 3) CANTOS :00 BASKET VERITAS Madrid Madrid S 18:00 NEGRO AMARILL VERITAS, INSTITUTO :00 O TAJAMAR Madrid Madrid D 00:00 BLANCO ROJO TAJAMAR, COLEGIO :00 SAN AGUSTIN DEL GUADALIX San Agustín de Madrid D 00:00 NARANJA NEGRO SAN AGUSTIN GUADALIX, Guadalix :00 PABELLON C.D. LA PAZ Parla Madrid S 00:00 AMARILL VERDE FCO. JAVIER CASTILLEJO, :00 O PDVO. C.B. LAS ROZAS Rozas de Madrid, Madrid S 20:15 ROJO BLANCO ALFREDO ESPINIELLA, Las :00 PABELLON BALONCESTO TORRELODONES Torrelodones Madrid S 18:00 ROJO NEGRO TORRELODONES, PABELLON :00 grande JORNADA 1 29/09/2019 Cod. Partido Equipo Local Equipo Visitante Día Fecha partido Hora 32806 BALONCESTO - INGESCASA BALONCESTO sábado 28/09/2019 18:00 32807 BASKETTORRELODONES VERITAS - COSLADATRES CANTOS C.B. - PLURAL sábado 28/09/2019 18:00 32808 TAJAMAR - NCSASESORES ALCOBENDAS domingo 29/09/2019 00:00 32809 SAN AGUSTIN DEL GUADALIX - ADC BOADILLA domingo 29/09/2019 00:00 32810 C.D. -

Fiestas De San Isidro En Azuqueca De Henares

2 SALUDA DEL ALCALDE ueridas vecinas, queri- dos vecinos: QEs tiempo de Espigas, de Mayos, de compartir y de ce- lebrar. Solo quería desearos unas muy felices fiestas de San Isidro. Como siempre, las hemos organizado con cariño y con trabajo. Y lo mejor, con la colaboración de personas, asociaciones y colectivos que siempre están etc.- continúan siendo una ahí para hacer cada día una magnífica red de colabo- Azuqueca mejor. ración sobre la que tejer el Os invito a todas y a todos a mejor futuro para todas las participar en los actos organi- personas que han nacido en zados, a realizar un pequeño Azuqueca o han elegido esta parón en la actividad cotidia- ciudad para desarrollar su na y a disfrutar de la ciudad. proyecto de vida. Los parques y jardines lucen En San Isidro se elabora la espectaculares en esta época, mezcla perfecta entre la tra- estamos esforzándonos para dición de la Azuqueca de an- lograr que el mantenimiento taño, reivindicando el pasado urbano sea el adecuado y de- agrícola, labrador y apegado sarrollamos varias campañas a la riqueza de estas tierras de sensibilización para mejo- fértiles de la Campiña, con la rar la convivencia. Azuqueca más vanguardista. Quiero dar las gracias, una Así que disfrutemos de esa vez más, a todas y a todos suma que hace que Azuque- 3 los que nos ayudáis a que la ca sea un municipio con un ciudad funcione y que sea honorable pasado y con un ese lugar en el que todos vi- ilusionante futuro. vamos felices. Las asociacio- ¡Felices fiestas de San Isidro! nes de Azuqueca –mayores, culturales, clubes deporti- José Luis Blanco vos, casas regionales, ONG’s, Alcalde de Azuqueca de Henares PROGRAMA DE FIESTAS DE SAN ISIDRO EN AZUQUECA MAYO 2017 DOMINGO 07 9:30 h. -

Cadenza Document

PARO REGISTRADO SEGÚN SEXO, EDAD Y SECTOR DE ACTIVIDAD ECONÓMICA GUADALAJARA NOVIEMBRE 2019 SEXO Y EDAD SECTORES TOTAL HOMBRES MUJERES SIN AGRI- INDUS- CONS- SERVICIOS EMPLEO CULTURA TRIA TRUCCIÓN MUNICIPIOS <25 25 - 44 >=45 <25 25 - 44 >=45 ANTERIOR ABANADES 1 1 1 ABLANQUE 2 2 2 ADOBES 1 1 1 ALAMINOS 3 3 3 ALARILLA 8 1 2 3 2 1 1 6 ALBALATE DE ZORITA 69 7 23 17 22 3 4 3 59 ALBARES 20 1 4 7 1 2 5 3 1 3 13 ALBENDIEGO 4 2 1 1 4 ALCOCER 13 1 4 2 6 1 12 ALCOLEA DE LAS PEÑAS ALCOLEA DEL PINAR 9 1 1 2 3 2 1 8 ALCOROCHES 2 1 1 2 ALDEANUEVA DE GUADALAJ 1 1 1 ALGAR DE MESA 3 2 1 1 2 ALGORA 4 3 1 2 2 ALHONDIGA 6 3 1 2 6 ALIQUE ALMADRONES 2 1 1 1 1 ALMOGUERA 85 4 10 13 7 27 24 3 5 6 70 1 ALMONACID DE ZORITA 40 9 10 2 13 6 3 2 3 31 1 ALOCEN 1 1 1 ALOVERA 632 30 73 114 32 182 201 3 57 28 511 33 ALUSTANTE 9 2 2 2 3 9 ANGON ANGUITA 5 1 2 2 1 2 2 ANQUELA DEL DUCADO 2 1 1 2 ANQUELA DEL PEDREGAL 3 1 1 1 1 2 ARANZUEQUE 25 2 8 1 10 4 2 3 3 11 6 ARBANCON 12 2 5 1 4 1 2 9 ARBETETA ARGECILLA 3 2 1 3 ARMALLONES 2 2 2 ARMUÑA DE TAJUÑA 16 3 3 2 2 6 15 1 ARROYO DE LAS FRAGUAS ATANZON ATIENZA 13 2 2 6 3 1 3 3 6 AUÑON 1 1 1 AZUQUECA DE HENARES 2.171 102 313 380 99 651 626 14 201 138 1.664 154 BAIDES 5 1 2 2 2 1 2 BAÑOS DE TAJO BAÑUELOS BARRIOPEDRO BERNINCHES BODERA, LA BRIHUEGA 151 4 18 52 5 28 44 9 8 18 108 8 BUDIA 3 1 2 3 BUJALARO 3 2 1 3 BUSTARES CABANILLAS DEL CAMPO 556 23 87 97 19 127 203 13 45 35 423 40 CAMPILLO DE DUEÑAS 1 1 1 CAMPILLO DE RANAS 14 2 8 1 3 1 5 8 CAMPISABALOS 2 1 1 2 CANREDONDO 3 2 1 2 1 CANTALOJAS 4 2 2 3 1 CAÑIZAR 1 1 1 CARDOSO DE LA SIERRA, -

Memoria Resumen De Actividades De Centros Comarcales Y Brigada Verde Año 2017 Centro Comarcal De Cogolludo

MEMORIA RESUMEN DE ACTIVIDADES DE CENTROS COMARCALES Y BRIGADA VERDE AÑO 2017 CENTRO COMARCAL DE COGOLLUDO. ACTIVIDAD ALBAÑILERÍA Bustares 6027 Finalizada 29/08/2017 Enfoscando armario de la luz Ciruelas 3926 Finalizada 17/03/2017 Colocar 8-10 bloques de hormigón Cogolludo 5809 Finalizada 25/05/2017 Saneamiento Espinosa De Henares (Carrascosa De Henares) 6167 Finalizada 07/11/2017 Reparar bordillos y echar hormigón Galve De Sorbe 5715 Finalizada 13/03/2017 Reparar paredes de garaje Hiendelaencina 3804 Finalizada 25/01/2017 Reparar seis tapas de pozo Humanes 3881 Finalizada 17/02/2017 Hormigonar averías en cinco puntos Malaguilla 6077 Finalizada 26/09/2017 Hormigonar averías Ordial, El (La Nava De Jadraque E.L.M.) 5901 Finalizada 11/07/2017 Captación Pradena De Atienza 3870 Finalizada 24/01/2017 Alicatar baño en mal estado Pradena De Atienza 3902 Finalizada 24/01/2017 Reparar rejilla de sumidero Puebla De Valles 3910 Finalizada 01/03/2017 Hormigonar avería Puebla De Valles 3921 Finalizada 09/03/2017 Colocar zanca para poste madera Puebla De Valles 5907 Finalizada 13/07/2017 Avería saneamiento Robledillo De Mohernand. Sin Asignar 15/11/2017 Arreglar 3 arquetas del agua que están hundidas Robledo De Corpes 3839 Finalizada 13/02/2017 Reparar lavadero en mal estado Zarzuela De Jadraque 6065 Finalizada 18/05/2017 Quitar mocheta de cajetín de luz y sumidero filtra agua Servicio De Cooperación 5756 Finalizada 25/04/2017 Colocación puerta Servicio De Cooperación 6215 En Ejecución 22/11/2017 Muelle en centro comarcal MEMORIA RESUMEN DE ACTIVIDADES DE CENTROS COMARCALES Y BRIGADA VERDE AÑO 2017 CENTRO COMARCAL DE COGOLLUDO. -

Uaclalaj Ira

Prc virtoia c1e c -uaclalaJ ira, Comprende esta provincia los siguientes Municipios, por partidos judiciale s Partido de ,Atienza . Partido de Cifuentes. Albend lego . Miñosa (La) . lbónades . Padilla del Duendo . Alcolea de las Peñas . Navas de Jadraque . Ablanque . Peralveche . AlcerIo . Ordial (El) . Alanünos . Puerta (La) . Aldeanueva de Atienza . Pala neares . Arbeteta . Renales . Alpedroches Pdimaces de Jadraque . Armallones . Riba de Sa elites . Angón . Paredes de Sigdenza. Azañón . Ribarredonda . Atienza . Prádena de Atienza . Canales del Ducado . Ruguilla . Pañuelos . Rebollosa de Jadraque . Canredondo . Sacecorbo . tlodera, (La) . R-iba de Santiuste . Carrascosa de Tajo . Saelices de la Sal . Ius?.ares. Cereceda. Riofrio del Llano. Santa María del Espino . Cabezadas (Las) . Cifuentes . Robledo de Corpes . Sotillo (El) . C am p isá baioa . Cogolior, Romanillas de Atienza . (lantalojas . Sotoca de Tajo . San Andrés del Congosto Esplegares . Cereadülo . Sotodosos. Semillas . i ;argoles de abajo . Cincávillas . `i'urrecuadrada de los Va - Sienes, Gargoles de arriba . Condemios de abajo . Gualda lles. Sonaolinos . Condemios de arriba . Henche. Torrecuadradilla. Toba (La) . Congostrina . 1-tortezuela de Océn (La) Trillo. Tordeirábano. (lalve de Sorbe. Haertahernando . Valdelagua. lijados. Uaseueña de Bornova . Huertapelayo . Val de San García . Valdeleubo . Hiendelaencina . Hueto•s. Valtablado del Río . Valverde de los Arroyos . Hijes . In ;lemas (Las) . \l iana de Mondéjar , Iiuerce (La) . Veguillas . Murillejo. Villanueva de Alcorcón . Madrigal . Villacadima . Oeentejo . Villarejo de Medina . Medranda. Villares de Jadraque . OI er. Zaorejas . Miedos de Atienza . Zarzuela de Jadraaue. Partido de Brihuega . Partido de Cogoltudo. Ala Pajares . Arenilla . Rebollosa de Hita. Argeciila . Romancas . Atanzón . Sai? Andrés del Rey . AIeas . Membrillera . Balconete . Soianillos del Extremo . Almiruete . Mesones . Barriopedro , Taragudo . Alpedrete de la Sierra .