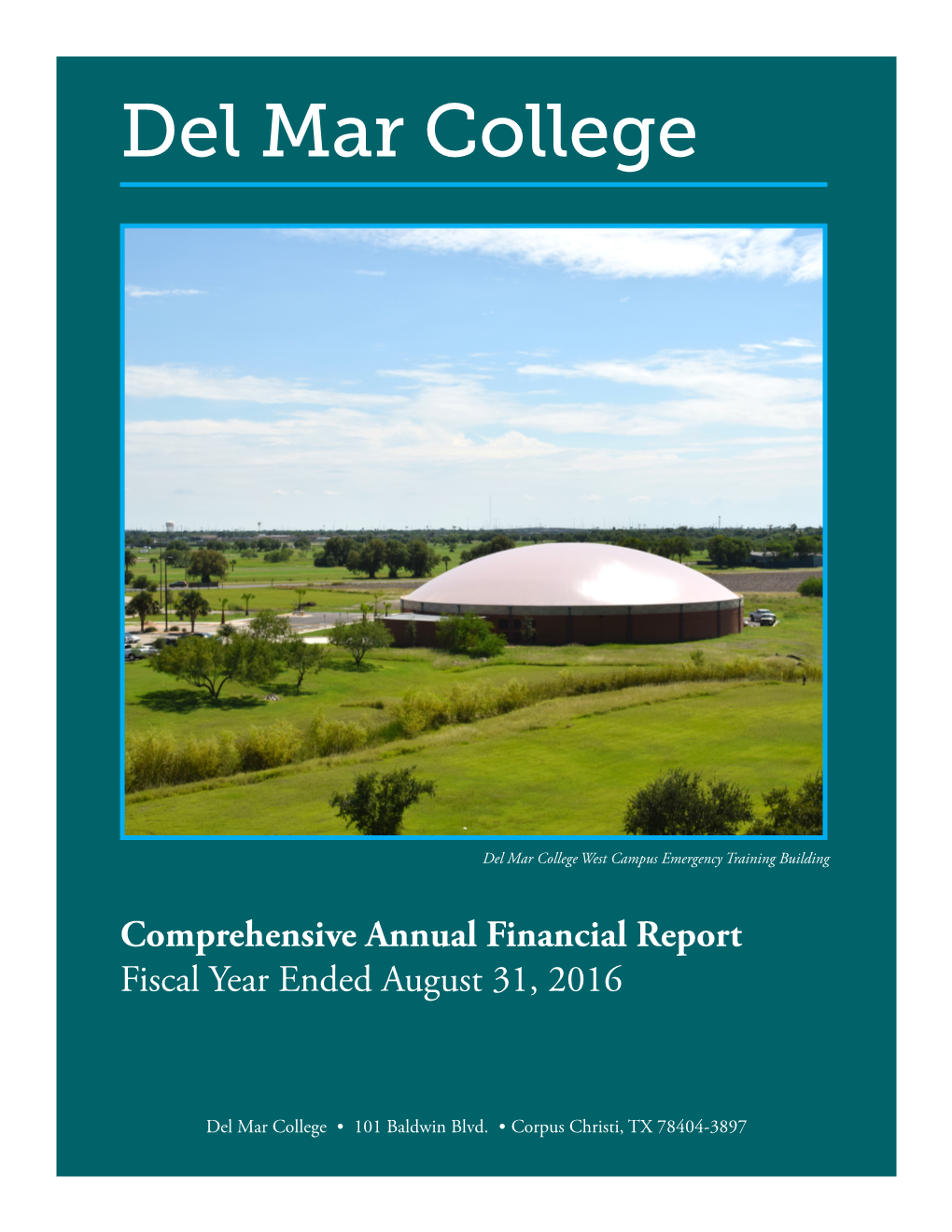

Comprehensive Annual Financial Report Fiscal Year Ended August 31, 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Flour Bluff Independent School District Check Register September 30, 2015

FLOUR BLUFF INDEPENDENT SCHOOL DISTRICT CHECK REGISTER SEPTEMBER 30, 2015 CHECK CHECK NUMBER VENDOR DATE AMOUNT GENERAL FUND 242578 CITY OF CORPUS CHRISTI 9/4/2015 150.00 242579 CITY OF CORPUS CHRISTI 9/4/2015 35.00 242580 CRENSHAW, JAMES 9/4/2015 270.25 242581 HOWARD, LANCE 9/4/2015 236.33 242582 JOURNAL MEDIA GROUP - CC CALLER TIMES 9/4/2015 263.88 242583 TASB INC 9/4/2015 1,400.00 242584 TEXAS SCHOOLS PUBLIC RELATIONS ASSOC 9/4/2015 175.00 242585 A+ COMPUTER SCIENCE 9/8/2015 1,295.00 242586 AMERICAN FOOTBALL COACHES ASSOCIATION 9/8/2015 60.00 242587 AUTOMATED BUSINESS SYSTEMS 9/8/2015 599.00 242588 BILL'S SPARKLING CITY CHARTER INC 9/8/2015 4,200.00 242589 BRAINPOP LLC 9/8/2015 5,170.50 242590 BUECHLER & ASSOCIATES PC 9/8/2015 7,750.00 242591 CALALLEN HIGH SCHOOL 9/8/2015 250.00 242592 CITY OF CORPUS CHRISTI-UTILITIES 9/8/2015 8,051.82 242593 CLELL WADE COACHES DIRECTORY INC 9/8/2015 56.85 242594 COLLETTE CONSULTING GROUP LLC 9/8/2015 3,000.00 242595 CORPUS CHRISTI ISD 9/8/2015 120.00 242596 CUMMINGS, CATRINA 9/8/2015 16.19 242597 DIVERSE DESIGN SOLUTIONS PLLC 9/8/2015 1,023.75 242598 EDUCATION ADVANCED INC 9/8/2015 1,500.00 242599 FENCING INC OF TEXAS 9/8/2015 923.00 242600 FIRETROL PROTECTION SYSTEMS INC. 9/8/2015 405.00 242601 FIRST 9/8/2015 225.00 242602 FRONTLINE TECHNOLOGIES GROUP INC 9/8/2015 13,416.00 242603 GAGGLE.NET, INC 9/8/2015 9,501.95 242604 GECKO MICROSOLUTIONS INC 9/8/2015 570.00 242605 GOWLAND STREALY MORALES & COMPANY PLLC 9/8/2015 6,000.00 242606 GULF COAST NUT & BOLT SUPPLY LLC 9/8/2015 154.95 242607 HANNES CONSTRUCTION -

Corpus Christi

Golf Texas A&M University - Corpus Christi Padre Isles Northshore Oso Beach Texas A&M University-Corpus Christi is a four-year university Country Club Country Club Golf Course that offers numerous bachelor, master and doctoral degrees in five colleges: Business, Education, Liberal Arts, Nursing & Health Sciences and Science & Engineering. L.E. Ramey Texas A&M University-Corpus Christi, located on its own 240-acre Sinton River Hills island, features state-of-the-art learning centers, support Golf Course Municipal Country facilities, student apartments and its own beach. Surrounded by Golf Course Club the Corpus Christi and Oso Bays, the campus is approximately ten miles from downtown Corpus Christi. Population Average Home Prices Del Mar College Corpus Corpus Nueces 12 County 2010 $152,200 Del Mar is a two-year community college that offers academic, Christi Christi MSA County Region 2011 $156,600 occupational and non-credit courses. Associate of Art, Science and 2012 $168,300 Applied Science degrees in over 50 university transfer majors are 2000 277,451 403,208 319,645 549,012 2013 $179,700 awarded at Del Mar, as well as Enhanced Skills Certificates and 2010 305,215 393,177 340,223 536,979 2014 $201,750 Certificates of Achievement in more than 80 occupational fields. 2013 316,381 442,600 352,107 546,877 Source: Texas A&M University Real Estate Center Both non-credit and credit students have Regional Age Distribution - 2013 access to classes, laboratories and the latest Age Group 2014 Building Permits Issued technology that upgrade their current skills, (City of Corpus Christi) 19 or Under 28.3% Corpus Christi prepare them for further study or train them for immediate employment in the Coastal Bend 20 – 29 14.3% New Residential 1,134 was ranked 5t h New Commercial 294 Most Desirable area. -

FLEXI-B Adult Single Fare

FARES WE’RE HERE Notes: (Exact Fare Required) TO SERVE YOU REGULAR FARES For Information and FLEXI-B Adult Single Fare.................. ......................... 75¢ Reservations Call: 361.749.4111 Reduced Fare * ............................................. 25¢ Reduced Fare * Off Peak .............................. 10¢ (Off peak hours are before 6 a.m., 9 a.m. to 3 p.m. & after 6 p.m. 602 North Staples Street on weekdays only) Corpus Christi, Texas 78401 PREMIUM SERVICE FARES 361.289.2712 FAX 361.903.3579 (Park & Ride/Express/Rural) N Mon-Fri 8am-5pm O Adult Single Fare ........................................ $1.25 I CCRTA Customer Service Center Reduced Fare * ............................................. 25¢ 602 North Staples Street #94 Port Aransas Shuttle ............................... 25¢ T Two hour time limit transfer included with single fare. 90 Corpus Christi, Texas 78401 A 361.883.2287 FAX 361.903.3400 will require difference in fare. M Mon-Fri 7am-6pm FLEXI - B Port Aransas R B-LINE FARES Hearing/Speech Impaired call 7-1-1 O to set up a Texas Relay Call. Regular Fare............................................... $1.25 Surcharge outside 3/4 mile ADA zone ........ $2.00 F The CCRTA Rideline FOR INFORMATION AND N (Automated Telephone) PASSES FLEXI-B RESERVATIONS I 361.289.2600 Day Pass .................................................... $1.75 CALL: 361.749.4111 T 7 Day Pass ................................................. $7.50 B-Line Paratransit Services 31 Day Pass ............................................. $30.00 N Scheduling 361.289.5881 Reduced Fare * (31 Day Pass)..................$11.00 Commuter 11 Trip Pass ............................ $12.50 A Vanpooling B-Line Pass...... ........................................ $50.00 T 1-800-VAN RIDE www.ccrta.org BUY PASSES ONLINE R POINTS OF INTEREST: You can now purchase your CCRTA bus passes O www.ccrta.org online and avoid the lines! Purchase 7, 11 and 31 Del Mar College P day passes on our website at www.ccrta.org. -

Geosciences DEPARTMENT of PHYSICS and Newsletter GEOSCIENCES VOLUME 1, ISSUE 4 DECEMBER 2007

Geosciences DEPARTMENT OF PHYSICS AND Newsletter GEOSCIENCES VOLUME 1, ISSUE 4 DECEMBER 2007 Program News Fall Geosciences Field Trip was successful Inside This Issue: Drs. John Buckley, Jae Yu and Tom McGehee led the Fall Fieldtrip to Central Texas to study Program News the Edwards Aquifer and Cave formations, ························· 1 Precambrian geology of the region, and climb Student News Enchanted Rock. ························· 2 Geosciences Club News ························· 4 Program Receives New Equipment In December the Geosciences Program will be receiving a thin-section Field Trip ························· 4 preparation machine from Army Corps of Engineers to be added to the rock room equipment. Also, Dr. James Carter (Economic Geologist, retired from Alumnus Report UTD) will be donating materials to the Geosciences Program to teach a graduate ························· 5 course in economic geology. Photo Gallery Geospatial Technology in Local High Schools and Community ························· 6 Colleges Five High School Principles at Calallen, H.M. King, Falfurias, Alice and Beeville Contact us / Editors have submitted letters of commitment to develop Geographic Information ························· 6 Systems at their High School. In addition, Coastal Bend College in Beeville and Alice are introducing GIS into their curriculum. With the help of Sam Cantu (Administrative Assistant) Drs. McGehee and Yu will develop the seven classes to be offered by Fall, 2008. Calallen High School Visited our Program Bruce Jonasen, Linda Hajek and five Earth and Space Science students from Calallen High School visited the campus to complete a GIS field exercise with Noe Saenz and Sam Cantu which was imported into a GIS. During their visit Jacob Hundl and members of the geology club conducted a laboratory review of rocks and minerals. -

Comprehensive Annual Financial Report Fiscal Year Ended August 31, 2015

Del Mar College Del Mar College historical photos selected from the 1940s - 1960s. Comprehensive Annual Financial Report Fiscal Year Ended August 31, 2015 Del Mar College • 101 Baldwin Blvd • Corpus Christi, TX 78404-3897 This page intentionally left blank. Comprehensive Annual Financial Report Fiscal Year Ended August 31, 2015 Prepared by John Johnson Comptroller Catherine West, CPA, Ed.D. Budget Officer and Director of Accounting Lenora Keas Vice President, Workforce Development and Strategic Initiatives Interim Provost and Vice President, Instruction and Student Services Del Mar College 101 Baldwin Blvd., Corpus Christi, Texas 78404-3897 www.delmar.edu Front cover photo: In recognition of 80 Years of Del Mar College history, a variety of photos from editions of the Cruiser yearbook. Clockwise from top left: East Campus entrance in 1941, Nursing student ca. 1940s, Students on campus in 1939, Student with teacher in 1966, West Campus entrance (then called Del Mar Technical Insti- tute) in 1960, construction of Memorial Classroom Building in 1942. Del Mar College COMPREHENSIVE ANNUAL FINANCIAL REPORT FISCAL YEAR ENDED AUGUST 31, 2015 Table of Contents Page No. INTRODUCTORY SECTION Transmittal Letter .......................................................................................................................... 1 Board of Regents and Administration .......................................................................................... 17 Certificate of Excellence in Financial Reporting ........................................................................ -

FY15-16 Del Mar College Distinguished Budget Document

Del Mar College Del Mar College historical photos selected from the 1940s - 1960s. Budget Document Fiscal Year 2015-2016 Del Mar College • 101 Baldwin Blvd • Corpus Christi, TX 78404-3897 Table of Contents Introductory Section ………………………………….… 1 Statistics Section ………………………………….….….. 46 Profile of the College …………………………...……...… 3 Revenues by Source …………………………………..….. 47 Vision, Mission, Core Values and Guiding Principles.…… 4 Program Expenses by Function …………………….….…. 48 Strategic Planning ……………………………………..…. 5 Net Assets ……………………………………………..…. 49 Board of Regents …………………………………….…... 8 Tuition and Fees ……………………………………..…… 50 Administration …………………………………………… 9 Assessed Value and Taxable Value of Property ………… 51 2015-2016 Budget Committee ……………………….….. 10 Property Tax Levies and Collections ………………..……. 52 Organization Chart …………………………………….…. 11 Principal Taxpayers …………………………………...….. 53 Budget Structure and Functions State Appropriations per FTSE and Contact Hour ….……. 54 Basis of Budgeting ……………………………….…... 12 Annual Contact Hours by Division ………………….…… 55 Revenue Sources ……………………………….…….. 13 Contact Hours Not Funded by State Appropriations ….…. 56 Expense Functions ……………………………………. 14 Ratios of Outstanding Debt …………………………….… 57 Expenditure Objects …………………………….…….. 15 Legal Debt Margin ………………………………….……. 58 Budget Development Process ……………………………. 16 Faculty, Staff, and Administrators Statistics …………..…. 59 Budget Calendar …………………………………………. 18 Enrollment Details ………………………………….……. 60 Student Profile ………………………………………..….. 61 Budget Section ……………………………………….…. -

Corpus Christi

1 2 EXPERIENTIAL EVOLUTION The 1-million-square-foot La Palmera is the result of a $50M transformation of the former Padre Staples Mall into a LEED-certified, contemporary shopping and dining destination. La Palmera continues its transformation as it adds retail, hospitality, restaurants and additional amenities. MARKET LEADER Located in Corpus Christi, Texas, La Palmera is the premier retail destination in the state’s Coastal Bend region, attracting close to 8 million visitors annually, and offering more than 100 retail and dining options. As the only super- regional mall within 140+ miles, La Palmera has maintained its position as a market leader in sales – seeing an increase of 58% since 2010. 3 DRIVE TIMES TO CORPUS CHRISTI Dallas Fort Worth 6.2 hours 6.1 hours El Paso 9 hours TEXAS Austin 3 hours San Antonio 2 hours Houston 3 hours Corpus Christi Laredo 2.3 hours McAllen 2.2 hours Brownsville 2.3 hours 4 OAKLAND, CA (#45) 426,410 TAMPA, FL (#48) 403,178 NEW ORLEANS, LA (#50) 396,766 LEXINGTON, KY (#59) 329,495 CORPUS CHRISTI, TX (#60) 329,408 PITTSBURGH, PA (#64) 302,908 ST. LOUIS, MO (#65) 300,991 ORLANDO, FL (#68) 297,243 PLANO, TX (#70) 294,478 DURHAM, NC (#74) 279,501 U.S. CITIES RANKED BY ST. PETERSBURG, FL (#76) 273,968 POPULATION SCOTTSDALE, AZ (#79) 266,961 (2019) 5 THREE CALIHAM RIVERS BEE 238 72 LIVE OAK 183 SEADRIFT 37 BEEVILLE 77 185 281 202 239 AUSTWELL 59 35 GEORGE WEST REFUGIO 181 MIKESKA SWINNEY SKIDMORE WOODSBORO SWITCH ARANSAS 359 HOLIDAY BEACH TYNAN MT LUCAS MATAGORDA 59 BONNIE VIEW LAMAR ISLAND WEST ST PAUL MATHIS LAKE CITY BAYSIDE COPANO VILLAGE SAN JOSE ISLAND 188 SAN PATRICIO JIM WELLS SINTON 188 37 ROCKPORT DUVAL TAFT SAN PATRICIO 77 ORANGE GROVE ODEM GREGORY 35 BLUNTZER 359 181 ARANSAS PASS 361 CALALLEN PORTLAND INGLESIDE 37 INGLESIDE 69E ON THE BAY PORT ARANSAS AGUA DULCE ROBSTOWN 44 SAN DIEGO Corpus Christi SOUTH PADRE ISLAND DR. -

Nueces County EARLY VOTING LOCATIONS

October 13 -16 (octubre 13-26) Nueces County 8:00 am - 5:00 pm October 17 (Sat) (octubre 17) 7:00 am - 7:00 pm 2020 General Election (elección general) October 19 - 23 (octubre 19 - 23) 8:00 am - 5:00 pm October 24 (Sat) (octubre 24) EARLY VOTING 7:00 am-7:00 pm October 26 - 30 (octubre 26 - 30) LOCATIONS 7:00 am - 7:00 pm (Locaciones Votación Anticipada) CORPUS CHRISTI ARMY DEPOT—NAS LONDON ISD MIDDLE/HIGH SCHOOL (Building 8, Hallway in front of Subway) (Library) Main Early Voting 308 Crecy St. Corpus Christi, TX 78419 1306 FM 43 Corpus Christi, TX 78415 Location CORPUS CHRISTI CHRISTIAN FELLOWSHIP MAGEE ELEMENTARY - STAR ANNEX (Fellowship Hall) (Building #3, Room C2 & C3) NUECES COUNTY 6602 S Staples St. Corpus Christi, TX 78413 4201 Calallen Dr. Corpus Christi, TX 78410 COURTHOUSE 901 Leopard St. DEAF AND HARD OF HEARING CENTER NEW LIFE CHURCH Corpus Christi, TX 78401 (Lobby) (at Sunrise Mall) 5151 McArdle Rd. Corpus Christi, TX 78411 5801 McArdle Rd. Corpus Christi, TX 78412 Special Sunday Hours at this location only PADRE ISLAND BAPTIST CHURCH DEL MAR COLLEGE October 18th & 25th (Heldenfels Administration Building) 14253 S. Padre Island Dr. Corpus Christi, TX 78418 12:00 pm - 5:00 pm 101 Baldwin Blvd. Corpus Christi, TX 78404 PORT ARANSAS COMMUNITY CENTER 408 N Alister St. Port Aransas, TX 78373 FLOUR BLUFF ISD (Transportation/Maintenance Building) TEXAS A&M UNIVERSITY ADKINS MIDDLE SCHOOL 2510 Waldron Rd. Corpus Christi, TX 78418 2402 Ennis Joslin Rd. Corpus Christi, TX 78414 CORPUS CHRISTI (O’Connor Building Room 135) 6300 Ocean Dr. -

Annual Reports

CITY OF CORPUS CHRISTI BOARDS, COMMISSIONS, COMMITTEES AND CORPORATIONS 2020 ANNUAL REPORTS TABLE OF CONTENTS Airport Board .......................................................................................... 1 Animal Care Advisory Committee…………………………………….4 Arts & Cultural Commission .................................................................. 7 Audit Committee..................................................................................... 10 Board of Adjustment ............................................................................... 13 Civil Service Board & Commission ....................................................... 16 Committee for Persons with Disabilities………………………………20 Construction Trade Advisory & Appeals Board .................................... 23 Commission on Children & Youth ......................................................... 26 Crime Control & Prevention District ..................................................... 29 Ethics Commission ................................................................................. 32 Island Strategic Action Committee ........................................................ 35 Landmark Commission ........................................................................... 39 Library Board .......................................................................................... 42 Marina Advisory Committee .................................................................. 45 Parks and Recreation Advisory Committee .......................................... -

PILOT SERVICE B-Line Pass

IMPORTANT INFORMATION FARES (Exact Fare Required) AT A GLANCE Notes: REGULAR FARES Adult Single Fare.................. ......................... 75¢ 602 North Staples Street Reduced Fare * ............................................. 25¢ Corpus Christi, Texas 78401 Reduced Fare * Off Peak .............................. 10¢ 361.289.2712 FAX 361.884.8101 (Off peak hours are before 6 a.m., 9 a.m. to 3 p.m. & after 6 p.m. Mon-Fri 8am-5pm on weekdays only) PREMIUM SERVICE FARES CCRTA Customer Service Center (Park & Ride/Express/Rural) 602 North Staples Street Adult Single Fare ........................................ $1.25 Corpus Christi, Texas 78401 Reduced Fare * ............................................. 25¢ 361.883.2287 FAX 361.883.1983 Mon-Fri 7am-6pm Two hour time limit transfer included with single fare. Crosstown66 Shuttle will require Limited Service Hearing/Speech Impaired call 7-1-1 Limited Stops to set up a Texas Relay Call. difference in fare. B-LINE FARES The CCRTA Rideline (Automated Telephone) Regular Fare............................................... $1.25 361.289.2600 Surcharge outside 3/4 mile ADA zone ........ $2.00 PASSES B-Line Paratransit Services Scheduling 361.289.5881 Day Pass .................................................... $1.75 7 Day Pass ................................................. $7.50 Vanpool 31 Day Pass ............................................. $30.00 1-800-VAN-4-WORK Reduced Fare * (31 Day Pass)..................$11.00 www.ccrta.org Commuter 11 Trip Pass ............................ $12.50 PILOT SERVICE B-Line Pass...... ........................................ $50.00 Holiday & Sunday Service BUY PASSES ONLINE The CCRTA operates a reduced level of service You can now purchase your CCRTA bus passes (sometimes no service) on certain holidays. online and avoid the lines! Purchase 7, 11 and 31 day passes on our website at www.ccrta.org. -

CCRTA System Map Cedar Pass Lipes High School Store

Chaparral Museum of Science and History ROUTES Broadway 76 STAPLES STREET STATION PORT AYERS STATION SOUTHSIDE STATION 3 NAS Shuttle (SEE BACK PANEL) WACO STAPLES 181 Whataburger Field 56 63 65 81 Flour Bluff(SEE BACK PANEL) 78 C 4 Oveal Williams City 15 37 Alameda LEOPARD AYERS 5 Senior Center Hall Nueces County NORTH BEACH/GREGORY Courthouse E SEE BACK PANEL 54 19 Santa Fe John 19 17 D F 6 6 Staples Street Station CCRTA ADMINISTRATION BUILDING B Winnebago 56 23 Hillcrest/Baldwin La Retama PORT 21 19 C G 26 12 Central Library 76 19 6 29 21 17 Kennedy Shoreline Kostoryz Nueces Bay 23 15 Palm Hulbirt A B C D 32 B H 37 H G F E A Comanche Tancahua CCPD/Municipal 25 29 A J 29 16 Morgan Court 27 28 29 23 78 12 16 Leopard 32 17 Carroll / Southside HEB HALL CITY CHRISTI CORPUS 21 Spohn Shoreline 37 Up River 17 Hospital MESTINA 19 Ayers Miller Staples MCARDLE High School Arboleda 37 Brownlee 21 28 Omaha 30 19th 23 Molina 12 Old Robstown 27 Morgan Santa Fe 25 Gollihar/Greenwood Hospital 23 37 26 Airline/Lipes Agnes Six Points Transfer Center Alameda Corpus Christi Spohn Medical Center ROBSTOWN / CALALLEN Zavala Memorial 27 Leopard Senior Center Hospital SEE BACK PANEL Baldwin Ayers Airport 28 Leopard/Omaha Baldwin Broadmoor Park Staples Navigation Senior Center 29 Staples 16 Del Mar HEB HEB College Del Mar College 30 Westside/Health Clinic 358 29SS West Campus 6 Port Lindale Carver Senior Center Texan TrailDriscoll Children’s Santa Fe 3 32 Southside Soledad Ocean US Social Hospital 5 Security Administration MacArthur Norton 34 Robstown North (SEE -

Scholarships Awarded Since 5-09-2018

D Scholarships Awarded Since 5-09-2018 Grant Date Scholarship Term Award Last Name First Name County High School Attending College Attending Notes 6/6/2018 Bean-Dirks Memorial Scholarship - George West Fall $ 1,000.00 Gallagher Taylor Jim Wells George West High School 6/6/2018 Bean-Dirks Memorial Scholarship - George West Fall $ 1,000.00 Hyde Catherine Live Oak George West High School 6/6/2018 Bean-Dirks Memorial Scholarship - George West Fall $ 1,000.00 Pawlik Alyson Live Oak George West High School 6/6/2018 Bean-Dirks Memorial Scholarship - George West Fall $ 1,000.00 Wasicek Julia Live Oak George West High School 6/6/2018 Bean-Dirks Memorial Scholarship - George West Fall $ 1,000.00 Wills Sahara Live Oak George West High School 6/6/2018 Cletis Dulin Memorial Scholarship Fall $ 1,000.00 Upton Franklin Refugio Refugio High School 6/6/2018 London PTO Scholarship Fall $ 1,000.00 Burkholder Hannah Nueces London ISD 6/6/2018 London PTO Scholarship Fall $ 1,000.00 Igwe Christabel Nueces London ISD 6/6/2018 Martha Mahany Memorial Athletic Scholarship 1 year $ 1,000.00 Johnson Jessica Nueces Calallen High School 6/6/2018 NCJLS-Homemaking Scholarship 4 years $ 3,500.00 Chisum Green Nueces Tuloso Midway High School 2020 high school graduate 6/6/2018 NCJLS-Homemaking Scholarship 4 years $ 2,500.00 Madeleine Gulding Nueces Homeschool 2020 high school graduate 6/6/2018 Nueces County Junior Livestock Show Scholarship 4 years $ 3,000.00 Brimhall Kaycee Nueces Calallen High School 6/6/2018 Nueces County Junior Livestock Show Scholarship 4 years $ 3,000.00