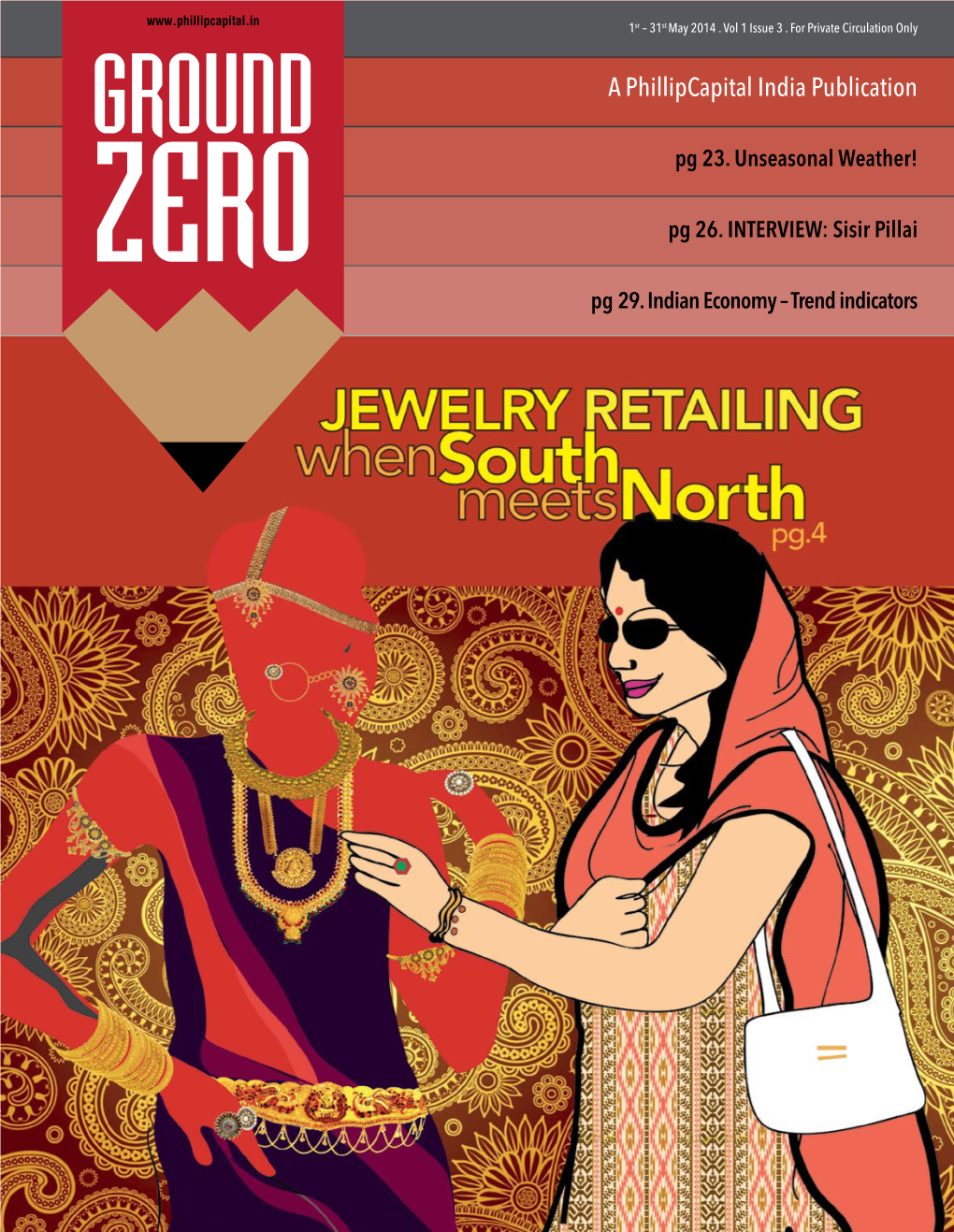

A Phillipcapital India Publication

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Kalyan Jewellers

Kalyan Jewellers https://www.indiamart.com/kalyan-jewellers/ The group derives its origins from textile retailing and wholesaling and has an experience of over 100 years in the trade. Kalyan branched out into the field of Jewellery retailing in the year 1993 by opening its first store in Thrissur. The ... About Us The group derives its origins from textile retailing and wholesaling and has an experience of over 100 years in the trade. Kalyan branched out into the field of Jewellery retailing in the year 1993 by opening its first store in Thrissur. The reason behind the Kalyan group's foray into business itself is quite unique and makes it interesting to read. The ancestors of the current management come from a pious background that comprised of priests, saints and advisors to kings. Hailing from the Tanjavur district of Tamilnadu, these ancestors had migrated to Kerala.The decision to start a business was taken in response to the call of one of the senior relatives of the clan, who was a Dewan to the Maharaja of Kochi, who believed 'Enterprise and business was necessary to create job opportunities and to make India self dependent'. He also believed that 'business should be fair with a social objective and not just for selfish motives'. The group still adheres to the founding principles of its forefathers and this explains the group's firm grounding in fair business practices and ethics. For more information, please visit https://www.indiamart.com/kalyan-jewellers/aboutus.html DIAMOND JEWELLERY SETS P r o d u c t s & S e r v i c e s Diamond Diamond Diamond Diamond GOLD JEWELRY P r o d u c t s & S e r v i c e s Gold Gold Gold Gold P r o OTHER PRODUCTS: d u c t s & S e r v i c e s Diamond Gold Platinum Platinum F a c t s h e e t Year of Establishment : 1993 Nature of Business : Wholesaler CONTACT US Kalyan Jewellers Contact Person: Anand A S Sreekrishna Building, West Palace Road Thrissur - 680022, Kerala, India https://www.indiamart.com/kalyan-jewellers/. -

MGL-INT-4-2016-UNPAID SHAREHOLDRS LIST AS on 31-03-2021.Xlsx

FOLIO-DEMAT ID NAME NETDIV DWNO MICR DDNO ADDRESS1 ADDRESS2 ADDRESS3 ADDRESS4 CITY PINCOD JH1 JH2 001221 DWARKA NATH ACHARYA 180000.00 16400029 5 JAG BANDHU BORAL LANE CALCUTTA 700007 000642 JNANAPRAKASH P.S. 1800.00 16400038 54773 POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 68056 MRS. LATHA M.V. 000691 BHARGAVI V.R. 1800.00 16400040 54775 C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 000902 SREENIVAS M.V. 1800.00 16400046 54781 SAI SREE, KOORKKENCHERY TRICHUR - 7 KERALA STATE MRS. RAJALAKSHMI SREENIVAS 001036 SANKAR T.C. 9000.00 16400052 54787 DAYA MANDIRAM TRICHUR - 4. KERALA MRS. MADHAVIKUTTY T.A. 002679 NARAYANAN P S 3600.00 16400074 54809 PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 002769 RAMLATH V E 1800.00 16400079 54814 ELLATHPARAMBIL HOUSE NATTIKA BEACH P O THRISSUR KERALA 002966 KUNHIRAMAN K 1800.00 16400098 54833 KADAVATH HOUSE OZHINHA VALAPPU (PO) (DIST) KARASAGOD 000000 003292 SURENDARAN K K 1692.00 16400113 54848 KOOTTALA (H) PO KOOKKENCHERY THRISSUR 000000 003427 JAYAPRAKASH P V 1692.00 16400118 54853 PULIPARAMBIL HOUSE VATANAPILLY THRISSUR 000000 003442 POOKOOYA THANGAL 1692.00 16400120 54855 MECHITHODATHIL HOUSE VELLORE PO POOKOTTOR MALAPPURAM 000000 1201910102051401 RAM PARKASH 4500.00 16400130 54865 HOUSE NO - 24 WARD NO-15 Pehowa 136128 001431 JITENDRA DATTA MISRA 10800.00 16400143 54878 BHRATI AJAY TENAMENTS 5 VASTRAL RAOD WADODHAV PO AHMEDABAD 382415 IN30047610042162 REKHA ANIL WAGLE 3510.00 16400151 54886 202 VINAYAK ANGAN OPP V I P SHOWROOM OLD PRABHADEVI ROAD PRABHADEVI MUMBAI 400025 ANIL VINAYAK WAGLE IN30047643177287 ANJANEYA SECURITIES SERVICES PRIVATE LIM 90000.00 16400152 54887 201 STAR APARTMENT A B NAGVEKAR MARG PRABHADEVI MUMBAI 400025 IN30021412035484 JUHI SAKHUJA 1800.00 16400156 54891 FLAT NO 12 1ST FLOOR WITS END HILL ROAD BANDRA WEST MUMBAI MAHARASHTRA 400050 001012 SHARAVATHY C.H. -

Kalyan Graphics Advances to Next Level with a New HP Latex 3600

SUCCESS STORY ALYAN Graphics is a unit of Kalyan Group, which is a holding company for the popular Kalyan Graphics brands like Kalyan Silks, Kalyan KJewellers, Kalyan Developers, Kalyan Sarees advances to next level with and Kalyan Collections. Founded on August 11, 2011 at Thrissur, this PSP has been a full-service signage solution provider, a new HP Latex 3600 producing a huge range of finest graphic applications, from outdoor billboards to By delivering finest graphic prints to meet the rapidly in-store backlit graphics. Recently the company made the decision to invest in changing demands from big corporate clients, Thrissur- HP Latex 3600 roll-to-roll printer in order based Kalyan Graphics has been a competent PSP in to keep pace with the growing demands the region. This PSP counts on improved competency for high-quality prints from big clients customers. and capability they have garnered after the adoption of “God has been kind to us, to reach the HP Latex 3600 roll-to-roll printer. TA SETHURAMAN, top position in the world of signage in the region, serving a host of big corporate Director, Kalyan Graphics, says the new HP Latex system clients who trust us for the quality of prints makes their dreams come true. we deliver and efficiency in service we provide,” says Sethuraman, adding that We used to dream of they are centrally located at Thrissur to delivering best of print easily connect with every city and town of quality in the region. Kerala and beyond. If demanded, Kalyan Today, everything and Graphics works for customers based in anything is possible other cities in Tamil Nadu and Karnataka, with HP Latex 3600,” viz Vellore, Coimbatore, Bengaluru, tells Sethuraman, Mangalore, etc. -

CSBL Unpaid Dividend, Refund Consolidated As on 22.09.2015.Xlsx

The Catholic Syrian Bank Limited Regd. Office, "CSB Bhavan", St. Mary's College Road, Thrissur 680020 Phone: 0487 -2333020, 6451640, eMail: [email protected] List of Unpaid Dividend as on 22.09.2015 (Dividend for the periods 2007-08 to 2013-14) FOLIO / DEMAT ID INITLS NAME ADDRESS LINE 1 ADDRESS LINE 2 ADDRESS LINE 3 ADDRESS LINE 4 PINCOD DIV.AMOUNT DWNO MICR PERIOD IEPF. TR. DATE A00350 ANTONY PALLANS HOUSE KURIACHARA TRICHUR, 30.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00385 ANNAMMA P X AKKARA HOUSE PANAMKUTTICHIRA OLLUR, TRICHUR DIST 150.00 5 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00398 ANTONY KUTTENCHERY HOUSE HIGH ROAD TRICHUR 1020.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00406 ANTONY KALLIATH HOUSE OLLUR TRICHUR DIST 27.00 9 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00409 ANTHONY PLOT NO 143 NEHRU NAGAR TRICHUR-6 120.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00643 ANTHAPPAN PADIKKALA HOUSE EAST FORT GATE TRICHUR 540.00 12 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00647 ANTHONY O K OLAKKENGAL HOUSE LOURDEPURAM TRICHUR - KERALA STATE. 680005 180.00 13 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00668 ANTHONISWAMI C/O INASIMUTHU MUDALIAR SONS 55 NEW STREET KARUR TAMILNADU 2100.00 14 2007-08 UNPAID DIVIDEND 25-OCT-2015 A00822 ANNA JACOB C/O J S MANAVALAN 5 V R NAGAR ADAYAR MADRAS - 600020 210.00 18 2007-08 UNPAID DIVIDEND 25-OCT-2015 A01072 ANTHONY VI/62 PALACE VIEW EAST FORT TRICHUR 4200.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A01077 ANTONY KOTTEKAD KUTTUR TRICHUR DIST 30.00 0 2007-08 UNPAID DIVIDEND 25-OCT-2015 A01103 ANTONY ELUVATHINGAL CHERUVATHERI -

Mgl-Di219-Unpaid Share Holders List As on 31-03-2020

DIVIDEND WARRANT FOLIO-DEMAT ID NAME MICR DDNO ADDRESS 1 ADDRESS 2 ADDRESS 3 ADDRESS 4 CITY PINCODE JH1 JH2 AMOUNT NO 001221 DWARKA NATH ACHARYA 220000.00 192000030 680109 5 JAG BANDHU BORAL LANE CALCUTTA 700007 000642 JNANAPRAKASH P.S. 2200.00 192000034 18 POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 68056 MRS. LATHA M.V. 000691 BHARGAVI V.R. 2200.00 192000035 19 C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 002679 NARAYANAN P S 2200.00 192000051 35 PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 002976 VIJAYA RAGHAVAN 2200.00 192000056 40 KIZHAKAYIL (H) KEEZHARIYUR P O KOVILANDY KHARRUNNISSA P M 000000 003124 VENUGOPAL M R 2200.00 192000057 41 MOOTHEDATH (H) SAWMILL ROAD KOORVENCHERY THRISSUR GEETHADEVI M V 000000 RISHI M.V. 003292 SURENDARAN K K 2068.00 192000060 44 KOOTTALA (H) PO KOOKKENCHERY THRISSUR 000000 003442 POOKOOYA THANGAL 2068.00 192000063 47 MECHITHODATHIL HOUSE VELLORE PO POOKOTTOR MALAPPURAM 000000 003445 CHINNAN P P 2200.00 192000064 48 PARAVALLAPPIL HOUSE KUNNAMKULAM THRISSUR PETER P C 000000 IN30611420024859 PUSHPA DEVI JAIN 2750.00 192000075 59 A-402, JAWAHAR ENCLAVE JAWAHAR NAGAR JAIPUR 302004 001431 JITENDRA DATTA MISRA 6600.00 192000079 63 BHRATI AJAY TENAMENTS 5 VASTRAL RAOD WADODHAV PO AHMEDABAD 382415 IN30177410163576 Rukaiya Kirit Joshi 2695.00 192000098 82 303 Anand Shradhanand Road Vile Parle East Mumbai 400057 000493 RATHI PRATAP POYYARA 2200.00 192000101 85 10,GREENVILLA,NETAJIPALKARMARG GHATKOPAR(WEST) MUMBAI MAHARASTRA 400084 MR. PRATAP APPUNNY POYYARA 001012 SHARAVATHY C.H. 2200.00 192000102 86 W/O H.L.SITARAMAN, 15/2A,NAV MUNJAL NAGAR,HOUSING CO-OPERATIVE SOCIETY CHEMBUR, MUMBAI 400089 1201090700097429 NANASAHEB BALIRAM SONAWANE 1606.00 192000114 98 2 PALLAWI HSG SOC. -

Fy2015164thinterimdividend.Pdf

FOLIO_DEMAT ID NAME DIVIDEND WARRANT MICR ADDRESS 1 ADDRESS 2 ADDRESS 3 ADDRESS 4 CITY PINCOD JH1 JH2 AMOUNT NO 001221 DWARKA NATH ACHARYA 180000.00 16400029 5 JAG BANDHU BORAL LANE CALCUTTA 700007 000642 JNANAPRAKASH P.S. 1800.00 16400038 54773 POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 68056 MRS. LATHA M.V. 000691 BHARGAVI V.R. 1800.00 16400040 54775 C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 000902 SREENIVAS M.V. 1800.00 16400046 54781 SAI SREE, KOORKKENCHERY TRICHUR - 7 KERALA STATE MRS. RAJALAKSHMI SREENIVAS 001036 SANKAR T.C. 9000.00 16400052 54787 DAYA MANDIRAM TRICHUR - 4. KERALA MRS. MADHAVIKUTTY T.A. 002679 NARAYANAN P S 3600.00 16400074 54809 PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 002769 RAMLATH V E 1800.00 16400079 54814 ELLATHPARAMBIL HOUSE NATTIKA BEACH P O THRISSUR KERALA 002966 KUNHIRAMAN K 1800.00 16400098 54833 KADAVATH HOUSE OZHINHA VALAPPU (PO) (DIST) KARASAGOD 000000 003292 SURENDARAN K K 1692.00 16400113 54848 KOOTTALA (H) PO KOOKKENCHERY THRISSUR 000000 003427 JAYAPRAKASH P V 1692.00 16400118 54853 PULIPARAMBIL HOUSE VATANAPILLY THRISSUR 000000 003442 POOKOOYA THANGAL 1692.00 16400120 54855 MECHITHODATHIL HOUSE VELLORE PO POOKOTTOR MALAPPURAM 000000 1201910102051401 RAM PARKASH 4500.00 16400130 54865 HOUSE NO - 24 WARD NO-15 Pehowa 136128 001431 JITENDRA DATTA MISRA 10800.00 16400143 54878 BHRATI AJAY TENAMENTS 5 VASTRAL RAOD WADODHAV PO AHMEDABAD 382415 IN30047610042162 REKHA ANIL WAGLE 3510.00 16400151 54886 202 VINAYAK ANGAN OPP V I P SHOWROOM OLD PRABHADEVI ROAD PRABHADEVI MUMBAI 400025 ANIL VINAYAK WAGLE IN30047643177287 ANJANEYA SECURITIES SERVICES PRIVATE LIM 90000.00 16400152 54887 201 STAR APARTMENT A B NAGVEKAR MARG PRABHADEVI MUMBAI 400025 IN30021412035484 JUHI SAKHUJA 1800.00 16400156 54891 FLAT NO 12 1ST FLOOR WITS END HILL ROAD BANDRA WEST MUMBAI MAHARASHTRA 400050 001012 SHARAVATHY C.H. -

MGL-Di220- UNPAID SHAREHOLDERS LIST AS ON

DIVIDEND WARRANT FOLIO-DEMAT ID INITLS NAME MICR ADDRESS 1 ADDRESS 2 ADDRESS 3 ADDRESS 4 CITY PINCODE JH1 JH2 AMOUNT NO 000540 SARITHA P.D. 2200.00 202000029 2785 POZHEKKADAVIL HOUSE P.O.KARAYAMUTTAM VALAPAD TRICHUR DIST. 000642 JNANAPRAKASH P.S. 2200.00 202000030 2786 POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 68056 MRS. LATHA M.V. 000691 BHARGAVI V.R. 2200.00 202000031 2787 C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 000995 NANDA KUMAR A.K. 22000.00 202000033 2789 SREERAM, XXX/219,THIRUVAMBADI POONKUNNAM TRICHUR - 2 KERALA MRS. AMMU NANDA KUMAR 001004 KARTHIKEYAN P.K. 2200.00 202000035 2791 PANIKKASSERY HOUSE, THRIPRAYAR POST NATTIKA TRICHUR DIST. KERALA STATE 001980 VALSALA SIVAPRAKASAN 11000.00 202000037 2793 THOTTUPURA HOUSE NATTIKA PO TRICHUR KERALA SIVAPRAKASAN T A 002564 SIMON P R 2200.00 202000038 2794 S/O RAPPAI PUTHOOR HOUSE KOTTAPADI P O THRISSUR 002679 NARAYANAN P S 2200.00 202000040 2796 PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 003539 RAJAN K C 2200.00 202000042 2798 C/O MODAPPILAI HOUSE PO.KANIMANGALAM THRISSUR NISHA RAJAN 002976 VIJAYA RAGHAVAN 2200.00 202000045 2801 KIZHAKAYIL (H) KEEZHARIYUR P O KOVILANDY KHARRUNNISSA P M 000000 003124 VENUGOPAL M R 2200.00 202000046 2802 MOOTHEDATH (H) SAWMILL ROAD KOORVENCHERY THRISSUR GEETHADEVI M V 000000 RISHI M.V. 003292 SURENDARAN K K 2068.00 202000048 2804 KOOTTALA (H) PO KOOKKENCHERY THRISSUR 000000 003397 HARIDAS D G 2068.00 202000049 2805 HARIDAS P G PANATE HOUSE KOTTAMKULAM PERINJANAM PO 000000 003442 POOKOOYA THANGAL 2068.00 202000051 2807 MECHITHODATHIL HOUSE VELLORE PO POOKOTTOR MALAPPURAM 000000 003445 CHINNAN P P 2200.00 202000052 2808 PARAVALLAPPIL HOUSE KUNNAMKULAM THRISSUR PETER P C 000000 IN30007910267776 VIJAY KHURANA 2750.00 202000053 2809 B 459 FIRST FLOOR NEW FREINDS COLONY NEW DELHI 110065 IN30065210146945 ASHA K. -

SIEMENS LIMITED List of Outstanding Warrants As on 18Th March, 2020 (Payment Date:- 14Th February, 2020) Sr No

SIEMENS LIMITED List of outstanding warrants as on 18th March, 2020 (Payment date:- 14th February, 2020) Sr No. First Name Middle Name Last Name Address Pincode Folio Amount 1 A P RAJALAKSHMY A-6 VARUN I RAHEJA TOWNSHIP MALAD EAST MUMBAI 400097 A0004682 49.00 2 A RAJENDRAN B-4, KUMARAGURU FLATS 12, SIVAKAMIPURAM 4TH STREET, TIRUVANMIYUR CHENNAI 600041 1203690000017100 56.00 3 A G MANJULA 619 J II BLOCK RAJAJINAGAR BANGALORE 560010 A6000651 70.00 4 A GEORGE NO.35, SNEHA, 2ND CROSS, 2ND MAIN, CAMBRIDGE LAYOUT EXTENSION, ULSOOR, BANGALORE 560008 IN30023912036499 70.00 5 A GEORGE NO.263 MURPHY TOWN ULSOOR BANGALORE 560008 A6000604 70.00 6 A JAGADEESWARAN 37A TATABAD STREET NO 7 COIMBATORE COIMBATORE 641012 IN30108022118859 70.00 7 A PADMAJA G44 MADHURA NAGAR COLONY YOUSUFGUDA HYDERABAD 500037 A0005290 70.00 8 A RAJAGOPAL 260/4 10TH K M HOSUR ROAD BOMMANAHALLI BANGALORE 560068 A6000603 70.00 9 A G HARIKRISHNAN 'GOKULUM' 62 STJOHNS ROAD BANGALORE 560042 A6000410 140.00 10 A NARAYANASWAMY NO: 60 3RD CROSS CUBBON PET BANGALORE 560002 A6000582 140.00 11 A RAMESH KUMAR 10 VELLALAR STREET VALAYALKARA STREET KARUR 639001 IN30039413174239 140.00 12 A SUDHEENDHRA NO.68 5TH CROSS N.R.COLONY. BANGALORE 560019 A6000451 140.00 13 A THILAKACHAR NO.6275TH CROSS 1ST STAGE 2ND BLOCK BANASANKARI BANGALORE 560050 A6000418 140.00 14 A YUVARAJ # 18 5TH CROSS V G S LAYOUT EJIPURA BANGALORE 560047 A6000426 140.00 15 A KRISHNA MURTHY # 411 AMRUTH NAGAR ANDHRA MUNIAPPA LAYOUT CHELEKERE KALYAN NAGAR POST BANGALORE 560043 A6000358 210.00 16 A MANI NO 12 ANANDHI NILAYAM -

SR NO First Name Middle Name Last Name Address

SR NO First Name Middle Name Last Name Address Pincode Folio Amount 1 AK AGRAWAL 110 D M C D COLONY AZADPUR DELHI 110033 0000000000CEA0018033 240.00 2 A K PARBHAKAR 8 SCHOOL BLOCK SHAKARPUR DELHI 110092 0000000000CEA0018043 750.00 3 A GROVER 2-A GOKHLE MARG LUCKNOW 226001 0000000000CEA0018025 645.00 4 A D KODILKAR 58/1861 NEHRUNAGAR KURLA EAST MUMBAI 400024 0000000000CEA0018011 1,125.00 5 A D KODILKAR BLDG NO 58 R NO 1861 NEHRU NAGAR KURLA EAST MUMBAI 400024 0000000000CEA0018012 180.00 6 A M RAJAPURKAR 11 CHANCHAL APPT SANGHVI NAGAR AUNDH PUNE 411007 0000000000CEA0018056 225.00 7 A M RAJAPURKAR 11 CHANCHAL APTS SANGHVI NAGAR AVNDH PUNE 411007 0000000000CEA0018057 240.00 8 A M RAJAPURKAR 11 CHANCHAL APTS SANGHVI NAGAR AUNDH PUNE 411007 0000000000CEA0018058 240.00 9 A GIRIDHAR 125 ANNAM GARDEN KAVADIGUDA HYDERABAD 500003 0000000000CEA0018021 255.00 10 A KARISHMA 125 ANNAM GARDENS KAVADIGUDA HYDERABAD 500003 0000000000CEA0018050 510.00 11 A MEGHNA 125 ANNAM GARDON KAVADIGUDA HYDERABAD 500003 0000000000CEA0018066 255.00 12 A VIKYAT 125 ANNAM GARDENS KAVADIGUDA HYDERABAD 500003 0000000000CEA0018106 255.00 13 A VINDHYA 125 ANNAM GARDENS KAVADIGUDA HYDERABAD 500003 0000000000CEA0018109 510.00 14 A SARADA FLAT NO 202 PREMIER COURT APPTS GOLKONDA X ROADS MUSHIRABAD HYDERABAD 500020 0000000000CEA0018089 750.00 15 A SRINIVASA RAO FLAT NO 202 KRISHNA ENCLAVE PLOT NO F-64 MADHURANAGAR HYDERABAD 500038 0000000000CEA0018092 240.00 16 A GAYATHRI C/O M MADHVESACHAR PLOT NO 41, MIG PHASE-I H NO 6-4-9, VANASTHALIPURAM HYDERABAD ANDHRA PRADESH 500070 0000000000CEA0018019 -

14Th Annual Report 2017 -- 2018

Confederation for Ayurvedic Renaissance -Keralam Limited 14th Annual Report 2017 -- 2018 III/671-KINFRA SMALL INDUSTRIES PARK, NALUKETTU ROAD KINFRA PARK P.O, PIN: 680309, KORATTY THRISSUR DISTRICT, KERALA Tele: [0480] 2735737 Fax: [0480] 2735837 E-mail:- [email protected] Web Site: www.carekeralam.com BOARD OF DIRECTORS CONFEDERATION FOR AYURVEDIC RENAISSANCE-KERALAM LIMITED Sri. P R Krishna Kumar (Chairman) Sri. Kunjupanicker Anilkumar (Vice Chairman) CONTENTS Sri. Hari N Namboothiri Sri. Eladath Thaikkattu Neelakandhanmooss Notice of Annual General Meeting……01 Sri. Balachandra Das M Chandrasekharan Nair Director’s Report………………………….05 Sri. Prasad Chirathilattu Ninan Sri. Ajay George Varghese Auditor’s Report ..………………………..32 Sri. Michael Joseph Sri. Ramanathan Devarajaiyer Balance Sheet……………………………..42 Sri. Kandamkulathy Pathrose Wilson Sri. Thanikkal Joy Verghese Statement of Profit & Loss……………..43 Sri. Janardanan Nair Muraleedharan Sri. Sunilkumar Surendran Nair Cash Flow Statement…………………….44 AUDITORS Note on Accounts…………………………45 M/s. Mahadevan & Sivarajan Chartered Accountants Route Map to the venue of AGM ……..73 10/491, Anugraha, Garden Street, College Road, Palakkad – 678001 Attendance Slip & Proxy form ………..74 REGISTERED OFFICE Confederation For Ayurvedic Renaissance- Keralam Limited CIN: U24233KL2004PLC017539 Kinfra Small Industries Park, Nalukettu Road, Koratty PO, Kerala – 680309 Email – [email protected] Website – www.carekeralam.com CONFEDERATION FOR AYURVEDIC RENAISSANCE-KERALAM LIMITED Registered Office - Kinfra Small -

Kalyan Silks Trichur Private Limited

June 29, 2017 Kalyan Silks Trichur Private Limited Summary of rated instruments Instruments* Rated amount Rating action (Rs. crore) Long term: Term loans 11.00 [ICRA]BBB+ (stable) / (revised from 38.8) re-affirmed Long term: Cash Credit 60.00 [ICRA]BBB+ (stable) / (revised from 95.0) re-affirmed Short term: Non-fund based 3.00 [ICRA]A2 / re-affirmed facilities Long / short term: Unallocated 24.0 [ICRA]BBB+ (stable) / (earlier nil) [ICRA]A2 re-affirmed *Instrument details are provided in Annexure-1 Rating action ICRA has re-affirmed the long-term rating of [ICRA]BBB+ (pronounced ICRA triple B plus)1 outstanding on the Rs. 11.0-crore2 (revised from Rs. 38.87 crore) term loans and Rs. 60.0-crore (revised from Rs. 95.0 crore) fund-based cash credit facilities of Kalyan Silks Trichur Private Limited (KSTPL). ICRA has also re-affirmed the short-term rating of [ICRA]A2 (pronounced as ICRA A two) outstanding on the Rs. 3.00-crore non-fund-based facilities and [ICRA]BBB+(stable) /[ICRA]A2 for Rs. 24.00 crore unallocated limit of the company. The outlook on the long-term rating is stable. Rationale The ratings consider the KSTPL’s strong operational profile marked by the established market and brand position in Kerala, its integrated nature of operations with retail and wholesale presence, and a diversified product portfolio. The ratings also derive comfort from the vast experience of the promoter in the textile retail industry and KSTLP’s financial profile characterised by stable earnings, and comfortable debt- protection metrics. The ratings, however, remain constrained by intense competitive pressures with limited entry barriers, and low current ratio due to high working capital requirements. -

Ac Name Ac Name2 Ac Addr1 Ac Addr2 Ac Addr3 Eapen Mathew a Anchuthayyil House Opp

AC_NAME AC_NAME2 AC_ADDR1 AC_ADDR2 AC_ADDR3 EAPEN MATHEW A ANCHUTHAYYIL HOUSE OPP. HEAD POST OFFICE, ALAPPUZHA JOSE U K CSB ALUVA MOOSA HAJI SAMIRA MANZIL ALUVA PIN 683 101 NALINI MANI PALLIPARAMBIL HOUSE ERUMATHALA P O COLONYPADY ALUVA ANNIE FRANCIES AMBALLUR, ALAGAPPANAGAR, THRISSUR ANTHAPPAN A D AKKARA HOUSE VARANDARAPPILLY ANTO N SON OF AUGUSTHY NELLANGRA HOUSE TRIKKUR ANTONY P D PANTHALOOKARAN HOUSE EARAVAKKAD BABY A O ATTOKARAN HOUSE IRINJALAKUDA BIJU K P KOLENGADAN HOUSE ALAGAPPANAGAR, THRISSUR CHAIRMAN SOCIAL WELFARE SOCIETY, ST.MARYS CHURCH-VENDORE, THRISSUR DIST CHANDRAN C K CHEERAMBAN HOUSE NENMANIKKARA THRISSUR DIST CHANDRAN U A S/O AYYAPPAN UTTOLY HOUSE KAVALLUR VARAKKARA P O DANADARAN T N THACHUPARAMBIL HOUSE MADAVAKKARA, P.O.CHITTISSERY DAVIS D AKKARA AKKARA HOUSE VARANDARAPPILLY TCR DEVAKEY V R MUTHRATHIPARAMBIL HOUSE CHITTISSERY TCR DEVASSY P L AMBALLUR TCR FRANCIS C JOSEPH CHAKRAMAKKAL HOUSE NEDUPUZHA P O GEORGE A A AKKARA HOUSE OLLUR GIRINDRA BABU THACHUPARAMBIL HOUSE MADAVAKKARA CHITTISSERY GOPI N K SON OF KUNJITTY NAMBARATH HOUSE VALANJA PADAM,PUDUKKA GOPINATHA MENON GOVARDHAN ALAGAPPANAGAR PO AMBALLUR GOVINDASWAMY K SREEKRISHNA TILE WORKS AMBALLUR INASU M O MUTHUPEEDIKA HOUSE VARAKKARACHONEDAN HOUSE P.O.PERAMBRA INDIRA K KURIYATHU HOUSE P.O.MUTTITHADI JACOB K P KAVALAKKAT HOUSE KATTOOR.P.O JAYA K B D/O K.T.BHASKARAN KANNAMKULANGARA HOUSE PAZHAI JOHNSON E D EDAKULATHUR HOUSE AGPA NAGR TCR JOSE A P ANTHIKKATT HOUSE VARANDRAPPILLY JOSE K O KALLUKKARAN HOUSE VENDORE-P.O.AGR JOSE V C VADAKKUMCHERY HOUSE KALLUR K C CHACKOCHAN