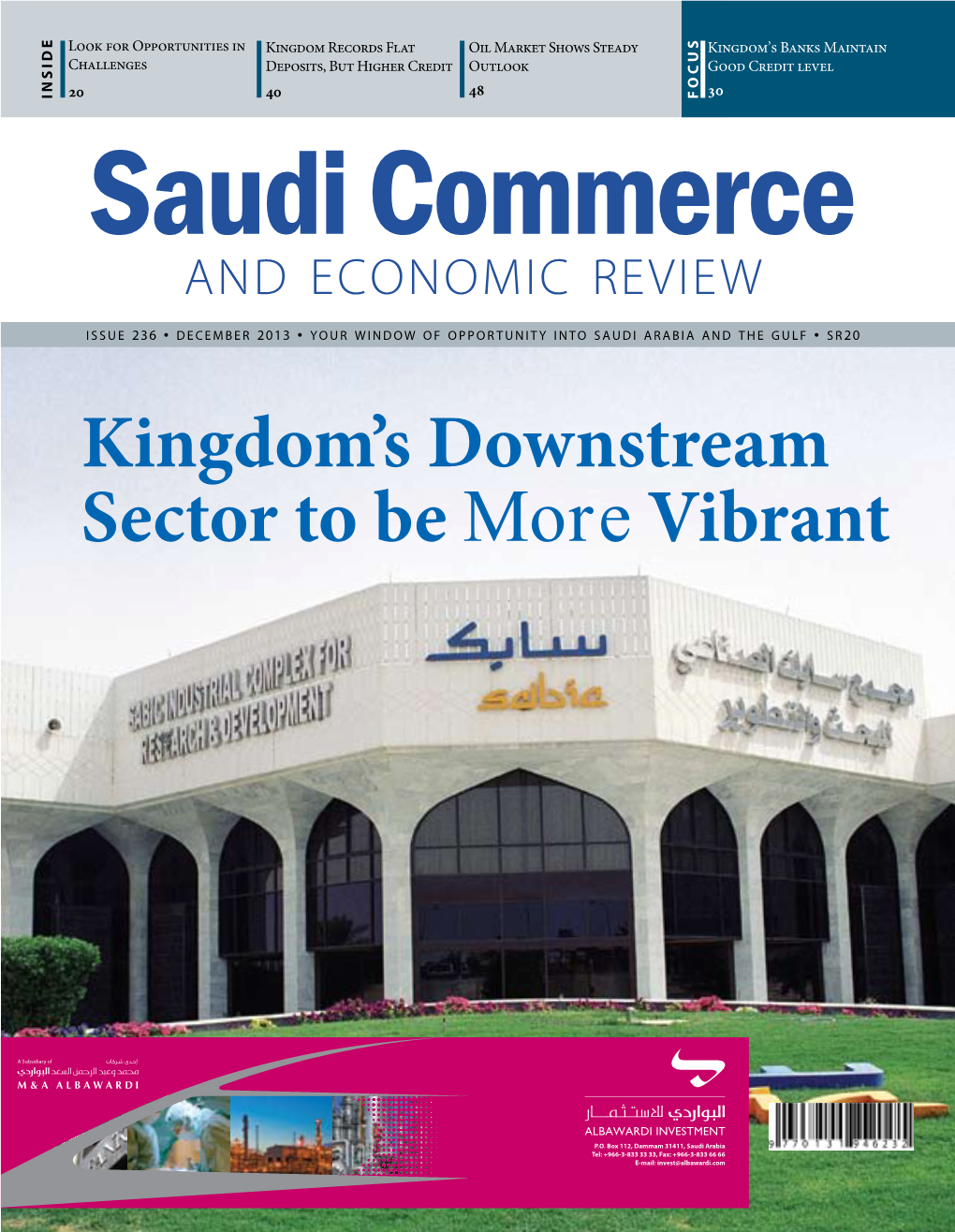

Kingdom's Downstream Sector to Be More Vibrant

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Recurrent Streptococcus Bovis Meningitis in Strongyloides Stercoralis Hyperinfection After Kidney Transplantation: the Dilemma in a Non-Endemic Area

Am. J. Trop. Med. Hyg., 90(2), 2014, pp. 312–314 doi:10.4269/ajtmh.13-0494 Copyright © 2014 by The American Society of Tropical Medicine and Hygiene Case Report: Recurrent Streptococcus bovis Meningitis in Strongyloides stercoralis Hyperinfection after Kidney Transplantation: The Dilemma in a Non-Endemic Area Taqi T. Khan,* Fatehi Elzein, Abdullah Fiaar, and Faheem Akhtar Institution Sections of Renal Transplant Surgery and Transplant Nephrology, Department of Nephrology and Transplantation, Division of Infectious Diseases and Histopathology, Departments of Medicine and Pathology, Riyadh Military Hospital, Riyadh 11159, Saudi Arabia. INTRODUCTION intravenous antibiotics with improvement in symptoms. This recipient had also received 10 mg dexamethasone 6 hourly Post transplant parasitic infections are a rarity and occur in 1 until S. bovis was discovered in the CSF. In view of the asso- around 2% of transplant recipients ; the intestinal helminth ciation of S. bovis with colonic cancer, he underwent a Strongyloides stercoralis (Ss) is found in contaminated soil in colonoscopy that was unremarkable and he was discharged hot and humid tropical and subtropical regions of Africa, home on his original triple immunosuppression. South and East Asia, and South America. Infective larvae He was readmitted after 3 weeks with fever, headache, from contaminated soil enter the host venous system from persistent vomiting, and neck pain, and a 20 kg weight loss. the skin to end up in the lungs and are then ingested into ° 2 He was febrile (38.5 C) with tachycardia and pallor with the GI tract by the pharynx where they mature into adults. mild signs of meningeal irritation. -

Security Council Distr

UNITED NATIONS S Security Council Distr. GENERAL S/AC.26/2002/7 13 March 2002 Original: ENGLISH UNITED NATIONS COMPENSATION COMMISSION GOVERNING COUNCIL REPORT AND RECOMMENDATIONS MADE BY THE PANEL OF COMMISSIONERS CONCERNING THE THIRD INSTALMENT OF “F2” CLAIMS S/AC.26/2002/7 Page 2 CONTENTS Paragraphs Page Introduction .........................................................................................................1 - 2 7 I. PROCEDURAL HISTORY ..............................................................................3 - 12 11 II. COMMON CONSIDERATIONS....................................................................13 - 38 12 A. Military operations, military costs and the threat of military action..........17 - 20 13 B. Payment or relief to others ....................................................................... 21 14 C. Salary and labour-related benefits..........................................................22 - 28 14 D. Verification and valuation........................................................................ 29 15 E. Other issues..........................................................................................30 - 38 15 III. THE CLAIMS ............................................................................................. 39 - 669 17 A. Saudi Ports Authority ...........................................................................39 - 93 17 1. Business transaction or course of dealing (SAR 270,397,424) .........41 - 49 17 2. Real property (SAR 9,753,500) .....................................................50 -

Economic and Social Council

UNITED NATIONS E Economic and Social Distr. GENERAL Council E/CN.4/1995/34 12 January 1995 Original: ENGLISH COMMISSION ON HUMAN RIGHTS Fiftieth session Item 10 (a) of the provisional agenda QUESTION OF THE HUMAN RIGHTS OF ALL PERSONS SUBJECTED TO ANY FORM OF DETENTION OR IMPRISONMENT, IN PARTICULAR: TORTURE AND OTHER CRUEL, INHUMAN OR DEGRADING TREATMENT OR PUNISHMENT Report of the Special Rapporteur, Mr. Nigel S. Rodley, submitted pursuant to Commission on Human Rights resolution 1992/32 CONTENTS Paragraphs Page Introduction ....................... 1- 4 4 I. MANDATE AND METHODS OF WORK ............ 5- 24 6 II. INFORMATION REVIEWED BY THE SPECIAL RAPPORTEUR WITH RESPECT TO VARIOUS COUNTRIES ......... 25-921 10 Algeria ...................... 26- 27 10 Angola ....................... 28 10 Argentina ..................... 29- 41 11 Bahrain ...................... 42- 50 12 Bangladesh ..................... 51- 57 14 Belgium ...................... 58- 60 15 Bolivia ...................... 61- 65 16 Brazil ....................... 66- 73 16 Bulgaria ...................... 74- 80 18 Burundi ...................... 81 20 Cameroon ...................... 82- 86 20 Chile ....................... 87- 88 21 GE.95-10085 (E) E/CN.4/1995/34 page 2 CONTENTS (continued) Paragraphs Page China...................... 89-128 21 Colombia .................... 129-137 27 Côte d’Ivoire ................. 138 29 Croatia..................... 139-140 29 Cuba ...................... 141-149 30 Cyprus ..................... 150-153 31 Czech Republic ................. 154 32 -

World Airliner Census 2015

WORLD AIRLINER CENSUS EXPLANATORY NOTES This census data covers all commercial jet and parentheses in the right-hand column. excluded, unless a confirmed end-user is known – in turboprop-powered transport aircraft in service or on On the Ascend database, an airliner is defined as which case the aircraft is shown against the airline firm order with airlines worldwide, excluding aircraft being “in service” if it is “active” (in other words concerned. Operators’ fleets include leased aircraft. that carry fewer than 14 passengers or equivalent accumulating flying hours). An aircraft is classified as cargo. It records the fleets of Western, Chinese-built “parked” if it is known to be inactive – for example, if and Russia/CIS/Ukraine-built airliners. it is grounded because of airworthiness requirements The tables have been compiled by Flightglobal or in storage – and when flying hours for three Abbreviations Insight using Flightglobal’s Ascend Fleets database. consecutive months are reported as zero. Aircraft AR: advance range (Embraer 170/190/195) The information is correct up to July 2015 and undergoing maintenance or awaiting conversion are C: combi or convertible excludes non-airline operators, such as leasing also counted as being parked. ER: extended range companies and the military. Aircraft are listed in The region is dictated by operator base and does ERF: extended range freighter (747 and 767) alphabetical order, first by manufacturer and then type. not necessarily indicate the area of operation. F: freighter Operators are listed by region, with any aircraft variant Options and letters of intent (where a firm contract LR: long range in brackets next to the operator’s name. -

Security Forces Thwarted Enemy S Nefarious Designs

Eye on the News [email protected] Truthful, Factual and Unbiased Vol:IX Issue No:324 Price: Afs.15 TUESDAY . JUNE 30 . 2015 -Saratan 09, 1394 HS www.afghanistantimes.af www.facebook.com/ afghanistantimeswww.twitter.com/ afghanistantimes Taliban kill 11 troops in Herat AT News Report KABUL: The Taliban militants in an armed ambush killed at least 11 Afghan National Army (ANA) CEO reacts angrily to the raid, asks NATO for explanation soldiers in which seven militants were also killed, in the western Herat province, officials said AT News Report Monday. The convoy of soldiers, made of pickup trucks, was at- KABUL: Hundreds of people tacked in Karukh district of west- protested on Monday against the ern Herat province yesterday US forces operation in Parwan province, which resulted in a huge morning, Ehsanullah Hayat, blast in an ammunition cache, leav- spokesman for the governor of the ing the residents in panic. Provin- province told Afghanistan Times. KABUL: Acknowledging that neg- of employees of the electronic ID cial police chief, Gen. Zaman Ministry of Defense in Kabul ligence was demonstrated in the department lost their jobs after Mamozai, said the American through a statement confirmed the distribution of electronic identity USAID and European Union (EU) troops raided a house of former incident and said seven militants cards, Chief Executive Officer suspended their funds to the de- jihadi commander, Ahmad Jan, in were also killed and five were in- (CEO) Abdullah Abdullah said he partment. The CEO expressed Bayan village of Charikar. The US jured the clash that lasted for sev- would take up the issue with the concerns about sacking of employ- troops discovered and blew an eral hours. -

SAUDI ARABIA @Religious Intolerance: the Arrest, Detention and Torture of Christian Worshippers and Shi'a Muslims

£SAUDI ARABIA @Religious intolerance: The arrest, detention and torture of Christian worshippers and Shi'a Muslims 1. INTRODUCTION Hundreds of men, women and children have been arrested and detained in Saudi Arabia since the Gulf Crisis in August 1990, most without charge or trial, solely for the peaceful expression of their religious beliefs. Scores have been subjected to torture, flogging or other cruel, inhuman or degrading treatment while in detention. In Saudi Arabia, where the vast majority of citizens are Sunni Muslims, both public and private non-Muslim religious worship is, in practice, banned. This ban is not limited to non-Muslims, however, as the public expression of Shi'a Muslim beliefs or the performance of their religious rites is strictly monitored and generally prohibited. In recent years a clear pattern of discrimination against religious minorities, particularly resident Christians and Saudi Arabian Shi'a Muslims, has emerged. Religious intolerance in the country appears to have become particularly acute after the Gulf Crisis of 1990-1991, as evidenced by a marked increase in the number of Christian worshippers being arrested and ill-treated solely for the peaceful expression of their religious beliefs. Members of the Christian faith in Saudi Arabia are, with very few exceptions, expatriate workers resident in the Kingdom for relatively short periods of time. During their stay in the country some form informal private worship groups. All non-Muslim worship, whether public or private, is banned in practice, and Christians meeting to worship are often the target of arrest, detention and torture or ill-treatment at the hands of Saudi Arabia's security and religious authorities. -

An Investigation of Self-Care Practice and Social Support of Patients with Type 2 Diabetes in Saudi Arabia

An Investigation of Self-Care Practice and Social Support of Patients with Type 2 Diabetes in Saudi Arabia Sabah Ismile Alsomali A thesis submitted in partial fulfilment of the requirements for the degree of Doctor of Philosophy University of Salford School of Health and Society November 2018 Table of Contents Dedication .............................................................................................................................. i Acknowledgements .............................................................................................................. ii List of Figures .................................................................................................................... iii List of Tables ...................................................................................................................... iii List of Appendices ............................................................................................................... iv List of Abbreviations .......................................................................................................... vi Abstract .............................................................................................................................. vii INTRODUCTION ............................................................................................................... 1 CHAPTER 1: THE RESEARCH CONTEXT: SAUDI ARABIA AND T2DM TRENDS ............................................................................................................................................ -

Curriculum Vitae BARRY GORDON, M.D., Ph.D. OFFICE Cognitive

Under Revision: September 28, 2020 Curriculum Vitae BARRY GORDON, M.D., Ph.D. OFFICE Cognitive Neurology/Neuropsychology Division Department of Neurology Johns Hopkins University School of Medicine 1629 Thames Street, Suite 350 Baltimore, MD 21231-3449 Telephone: 443-287-1702 Fax: 443-769-1280 E-mail: [email protected] Web page: http://web.jhu.edu/cognitiveneurology EDUCATION B.A., 1971 Pennsylvania State University, 1968-1969 Five-Year Cooperative Program in Medicine M.D., 1973 Thomas Jefferson University School of Medicine, 1969-1973 (Amplissimis Honoribus) M.A., 1980 Johns Hopkins University (Psychology) Ph.D., 1981 Johns Hopkins University (Psychology) POSTGRADUATE TRAINING 1973-1974 Medical Internship, New York Hospital/Cornell Medical Center 1974-1977 Neurology Residency, Johns Hopkins Hospital 1976-1977 Administrative Chief Resident in Neurology, Johns Hopkins Hospital 1978-1981 Doctoral Study, Department of Psychology, Johns Hopkins University FACULTY POSITIONS Current 2000- Therapeutic Cognitive Neuroscience Chair (Inaugural Holder) Professor of Neurology with Joint Appointment in Cognitive Science Cognitive Neurology/Neuropsychology, Department of Neurology Johns Hopkins University School of Medicine 1996- Professor, Department of Neurology 1988- Founding Member, Zanvyl Krieger Mind/Brain Institute Johns Hopkins University Prior 1990-1996 Associate Professor, Department of Neurology The Johns Hopkins University School of Medicine 1983-1988 Joint Appointment, Department of Psychology Johns Hopkins University 1978-1990 Assistant -

Traumatic Spinal Cord Injury in Saudi Arabia: an Epidemiological Estimate from Riyadh

Spinal Cord (2012) 50, 882–884 & 2012 International Spinal Cord Society All rights reserved 1362-4393/12 www.nature.com/sc ORIGINAL ARTICLE Traumatic spinal cord injury in Saudi Arabia: an epidemiological estimate from Riyadh SS Alshahri1,2, RA Cripps3, BB Lee2,4 and MS Al-Jadid5 Study design: Retrospective study. Objectives: To review traumatic spinal cord injury (TSCI) rates and epidemiology at the Riyadh Military Hospital (RMH) in Saudi Arabia and to hypothesise strategies for a more integrated approach to injury prevention in Saudi Arabia. Setting: RMH, Rehabilitation Division. Methods: A review was conducted of all patients with TSCI aged X14 years admitted to RMH from January 2003 to December 2008. Descriptive analysis was performed for age, gender, cause of TSCI, completeness and neurological level of the injury. Results: In all, 307 TSCI patients were admitted during this period: 88% were male, and their mean age was 29.5 years old (median 27, range 14–70). Of all TSCI patients, 52% had tetraplegia and 51% had a complete TSCI. Road traffic accidents (RTAs) were the main cause of TSCI (85%). Conclusions: TSCI in Saudi Arabia affects mainly the male population. The rate of RTAs caused by four-wheeled vehicles is the highest globally reported RTA statistic. Primary prevention strategies specific to the region should be developed to decrease the number of car accidents. The higher-than-expected rate of complete injuries may reflect practices in acute management and transport, and suggests that a review of the acute and integrated management of TSCI may also be necessary. Spinal Cord (2012) 50, 882–884; doi:10.1038/sc.2012.65; published online 10 July 2012 Keywords: Saudi Arabia; Middle East; spinal cord injury; epidemiology; road traffic accident; descriptive INTRODUCTION RTA deaths per million in Saudi Arabia (2007 data re-calculated by Traumatic spinal cord injury (TSCI) is catastrophic to individuals and the authors) compared to 152 in the United States and 95 in Australia the society. -

A Survey of the Attitude and Practice of Research Among Doctors in Riyadh Military Hospital Primary Care Centers, Saudi Arabia

[Downloaded free from http://www.jfcmonline.com on Saturday, June 02, 2012, IP: 41.238.142.47] || Click here to download free Android application for this journal M edical Education A survey of the attitude and practice of research among doctors in Riyadh Military Hospital primary care centers, Saudi Arabia Saad H. Al-Abdullateef Family and Community Medicine Department, Riyadh Military Hospital, Riyadh, Saudi Arabia Address for correspondence: Dr. Saad Hamad Al-Abdullateef, Riyadh Military Hospital, Family and Community Medicine Department, Riyadh11594, P.O Box 58092, Saudi Arabia. E-mail: [email protected] Objectives: To assess the attitude and practice of doctors in the Military Hospital Primary Care Centers in Riyadh (RMH) toward research and to identify the main barriers to conduct research. Materials and Methods: A cross-sectional study was conducted from March to April, 2010, at RMH primary care centers. The sample included all general practitioners (GPs) working in primary healthcare centers. A self-administered questionnaire was formulated from different sources and used as a tool for data collection.Results: The response rate was 75%. Among the respondents 96.9% agreed that research in primary care was important for different reasons. Most of the GPs had a positive attitude toward research: 68% had been influenced by research in their clinical practice and 66% had an interest in conducting research, and74.2% of the respondents had plans to do research in the future. Insufficient time was the most frequently cited barrier (83.5%) for participating ABSTRACT in research, followed by the lack of support (58.8%). Conclusions: Many of the GPs had a positive attitude toward research, but had no publications or plan for new research. -

Exhibitor Prospectus

THE 62ND INTERNATIONAL RESPIRATORY CONVENTION & EXHIBITION TABLE OF CONTENTS (CLICK TO NAVIGATE) u ABOUT AARC CONGRESS u ATTENDEE DEMOGRAPHICS u REASONS TO EXHIBIT u EXHIBIT HALL MAP/BOOTH PRICES u BOOTH ASSIGNMENT u APPLICATION/PAYMENT/CANCELLATION u EXHIBITOR FAQs u EXHIBITOR LIST ABOUT THE AARC CONGRESS 2016 SAN ANTONIO, TX • OCTOBER 15-18 (EXHIBITS OCTOBER 15, 16, 17) EXHIBIT DATES AND HOURS Meet the Profession’s Leaders, schedule A FIRST CLASS SATURDAY, OCTOBER 15 your 3-day sales call with nearly 6,000 EVENT 11:00 A.M.– 4:00 P.M. respiratory therapists in San Antonio. You’ll SUNDAY, OCTOBER 16 That Attracts Top 9:30 A.M.– 3:00 P.M. build lasting connections with new customers Respiratory Therapists MONDAY, OCTOBER 17 and reinforce existing relationships. 9:30 A.M.– 2:00 P.M. From All 50 United States, U.S. Territories, and 2016 HIGHLIGHTS Nearly 30 Countries. u Lectures lead attendees to exhibit hall — The Keynote lecture, Eagan lecture, Kittredge lecture, u HENRY B. GONZALEZ CONVENTION CENTER The AARC Congress offers an exciting venue and Tom Petty lecture will all send attendees to present advances in treatment, research, — is one of the favorites for Congress attendees. straight to the exhibit hall and your booth. cutting-edge technology, and education on Steps away from the River Walk, and it actually has pulmonary disease and injury. “A River that Runs through It.” This section of the u Closing Ceremony on day four — An event that charming San Antonio River Walk is aptly named, encourages attendees to stay through all four days “The Grotto.” and attend the last day of your exhibit. -

RASG-MID/6-WP/15 17/08/2017 International Civil Aviation Organization Regional Aviation Safety Group

RASG-MID/6-WP/15 17/08/2017 International Civil Aviation Organization Regional Aviation Safety Group - Middle East Sixth Meeting (RASG-MID/6) (Bahrain, 26-28 September 2017) Agenda Item 3: Regional Performance Framework for Safety SMS IMPLEMENTATION BY AIR OPERATORS (Presented by IATA) SUMMARY This paper provides the status of SMS implementation by Air operators registered in MID States and provides recommendation for the way forward to complete SMS implementation. Action by the meeting is at paragraph 3. REFERENCES - SST-3 Meeting Report 1. INTRODUCTION 1.1 Currently, implementation of safety management at the Service Provider level is variable, and is proving challenging to put in place the system as intended by Annex 19. 1.2 The MID-SST was established to support the RASG-MID Steering Committee (RSC) in the development, monitoring and implementation of Safety Enhancement Initiatives (SEIs) related to identified safety issues, including implementation of State Safety Programs (SSP) and Safety Management Systems (SMS). 2. DISCUSSION 2.1 The Third meeting of the MID Safety Support Team (MID-SST/3) held in Abu Dhabi, UAE, 10-13, recognized the need to monitor the status of SMS implementation by air operators, maintenance organizations and training organizations involved in flight training; in order to take necessary actions to overcome the challenges faced and to improve safety. 2.2 In this regard, the meeting agreed that IATA with the support of the ICAO MID Office will provide feedback and a plan of actions to address SMS implementation by air operators. RASG-MID/6-WP/15 - 2 - 2.3 The meeting may wish to note that Safety Management Systems (SMS) is an integral part of the IOSA program.