Wiedmann-Etal-OHI-2016-The-Role-Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

High Res. Dubai

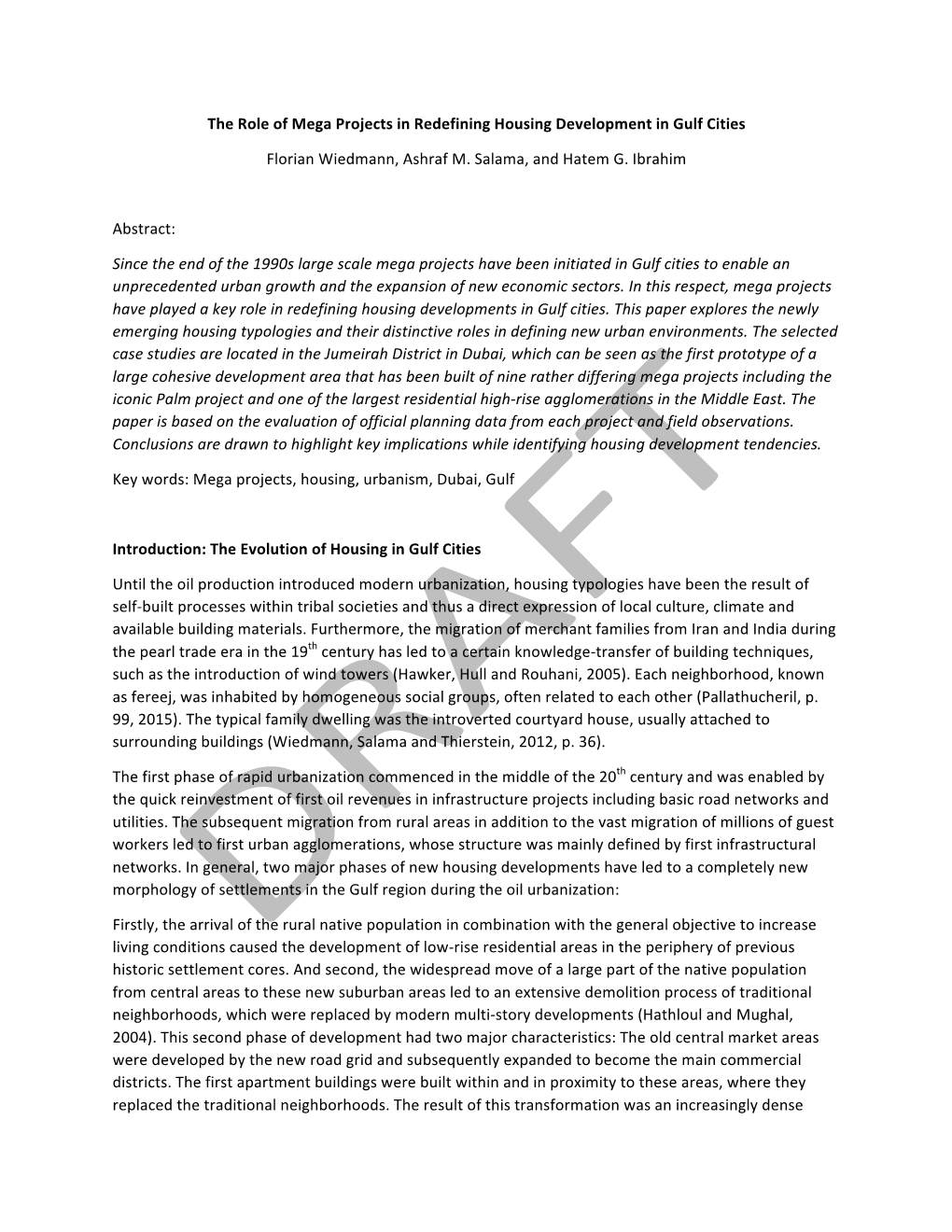

Al Ras Al Ras Map of Dubai Corniche The Palm Deira The World The Palm Jebel Ali W a t e r f r o n t Peninsula Riviera The Palm Jumeirah Spear Fishing DIVE CENTER Bali Marina Red Sea Downtown Atlantis Maledives South Africa Snorkler`s Cove A Palau Academy r Cayman Islands JEBEL ALI HARBOUR a DUBAI Madinat Al Arab West b Breakwater MARITIME East i Breakwater CITY Uptown Helicopter a Pad n Jebel Ali Golf Resort Dubai East G S & Spa u he Cart Club Hassah l ik f h Z Marina Reclamation aye DUBAI MARINA d Bund f R oad His Highness The Resort the Ruler`s Garden Great l Belize Container Terminal Golf Course JEBEL ALI PORT u Palm Barrier G Dubai Trump Int`l Reef Hassah Hotel & Tower Dry PORT RASHID Tanker Berth n Palace a Coaster Al Shindagha No. 1 A b i Berth Caltex r a Refinery Docks Boulevard Department of Exchange Air Products East Ports and Customs j Road halee Wharf Al K Heritage & Bin Diving Village Sh Al Arco Port Administration Al Shindagha Suroor Sheikh Saeed ind Dubai Beach Market Mosque House T a Dubai t u g e n h Dubai Marine e n a r Deira Fish, Meat & Diving Beach Resort t el Al Ghuba S Vegetable Market West Private & Spa Swedish iba Roa Centre d h a Consulate D92 l Emirates Island a H.H. The Rulers F AL MINA l Wharf Science Ban oad Deira Guesthouse A iyas R Club Bus Station Highland Hotel Al Khor Str. -

Brands to Riches Anthony Liddiard CEO RMAL Hospitality

Brands to riches: Anthony Liddiard CEO RMAL Hospitality 29/10/09 12:37 PM WELCOME Inspiring us - Mark Norris CLIENT PROFILE Brands to Riches - Anthony Liddiard LEADING STORIES Born to Fly - Michael Helling Hotelier, Madame Leo - Grace Leo Star Bright - Chris Durant Leveraging Good - Vicki Gordon Leader & Gentleman - Harry Murray MBE Tigers & Taj Mahal - Liam Lambert Design Control - Duncan Palmer ONE TO WATCH A Brilliant Move – Brian Williams NETWORKS HR in Hospitality – Jane Sunley BOOK CLUB A History of Modern Britain INSIDE PROFILE Africa Calling - Gina McAdam Leader Home | Profile Main Site | Print page | Mail a friend BRANDS TO RICHES April 2008 Edition of LEADER October 2008 Edition of LEADER In just two years, RMAL Hospitality March 2009 Edition of LEADER has managed to lure a fistful of world-class brands to the Middle East. It’s only the beginning, CEO Anthony Liddiard tells Leader. Link What else, apart from being bywords for quality, do wagamama, Fairmont, Trader Vic’s, Trader Vic’s Sign up for Profile LEADER Mai Tai Lounge, Frankie’s Italian Bar and Grill, and Marco Pierre White’s Steakhouse & Grill have in Leader common? In the UAE, they’re all part of Abu Dhabi- Journal based RMAL Hospitality’s growing portfolio of franchised restaurants and luxury hotels. Back Issues Name: Las Vegas grand dames MGM Grand and Bellagio will soon follow suit. ‘We’ve signed the contracts,’ E-Mail Address: says Anthony Liddiard, the 30-year hospitality veteran hand-picked by the giant Al Fahim Group to run RMAL Hospitality, their dedicated hotel and restaurant development business launched in 2007. -

Hospitality Projects 1

HOSPITALITY PROJECTS 1 Project Title Location Value (USD mm) Redevelopment of Gulf Hotel Abu Dhabi, UAE 500 Emirates Airlines Park Hotel Dubai, UAE 400 Taj Exotica Resort & Spa Dubai, UAE 325 Fairmont Hotel Abu Dhabi, UAE 300 Park Rotana Hotel Abu Dhabi, UAE 200 Rotana Hotel Baghdad, Iraq 150 Lagoona Beach Hotel Ajman, UAE 150 Ritz Carlton Hotel Doha, Qatar 135 Sea View Club Dubai, UAE 135 Djibouti Kempinski Hotel Djibouti, Africa 120 Mina Al Fajr Resort Fujairah, UAE 110 Seaview Resort Dubai, UAE 100 Al Raha Beach Sheraton Hotel Abu Dhabi, UAE 95 Westin Hotel Dubai, UAE 80 Grovesnor House Hotel Dubai, UAE 65 Marsa Shams Resort Syria 60 Centro Hotel Dubai, UAE 55 Hotel at Al Muraqqabat Street Dubai, UAE 55 Bonnington Hotel Dubai, UAE 45 Jumeirah Business Bay Hotel Dubai, UAE 45 Luxury Beach Resort Dubai, UAE 45 Holiday Inn Hotel Dubai, UAE 40 Hotel & Cinema Building Dubai, UAE 40 Le Meridien Aqah Hotel Fujairah, UAE 40 Link View Apartments Dubai, UAE 40 Movenpick Hotel at JBR Dubai, UAE 40 Royal Meridien (Abu Dhabi Grand) Abu Dhabi, UAE 40 Ibis & Novotel Hotels Dubai, UAE 35 Beach Hotel Abu Dhabi, UAE 30 Marriott Hotel Dubai, UAE 30 Sheraton Jumeirah Beach Dubai, UAE 25 Oasis Beach Hotel Dubai, UAE 23 Marriott Hotel Yemen 20 1 HOSPITALITY PROJECTS 2 Project Title Location Value (USD mm) Hill Hotel Abu Dhabi, UAE 17 Hilton Hotel Yemen 15 HEALTHCARE PROJECTS Project Title Location Value (USD mm) Al Zahra Hospital - Dubai Dubai, UAE 150 Corniche Paediatric Hospital Abu Dhabi, UAE 150 Al Zahra Hospital - Sharjah Sharjah, UAE 100 Sheikh Khalifa -

Dubai's 16Th Global Family Office Investment Summit October 2021

Under the High Patronage of His Excellency Dr. Thani Al Zeyoudi, Minister of State for Foreign Trade & Minister in charge of Talent Attraction and Retention at the United Arab Emirates Ministry of Economy. 16th Anniversary Ritossa Global Family Office Investment Summit 3-5 October 2021 Dubai, Waldorf Astoria Palm Jumeirah “World’s No. 1 Family Office Investment Conference, where World Leaders & Elite Family Office Investors Unite Together to Invest and Create A Brighter Future” Special Thank You to our High Patron His Excellency Dr. Thani Al Zeyoudi, Minister of State for Foreign Trade & Minister in charge of Talent Attraction and Retention at the UAE Ministry of Economy: "I am so proud to be honouring the glowing strategic direction of the Ministry Of Economy, UAE with H.E. Dr. Thani Al Zeyoudi, Minister of State for Foreign Trade as well as holding the position of Minister in charge of Talent Attraction and Retention at Ministry Of Economy, UAE. The UAE is cementing its position as the leading business destination at regional and global levels attracting incoming business partnerships and foreign investments. UAE's key areas of focus are Impact Investing, Renewable Energy, Healthcare, Education, Biotech, Fintech, Space, Real estate, Hospitality, and A.I. H.E. Dr. Thani bin Ahmed Al Zeyoudi is devoted to attracting the best talents and competencies to serve the strategic direction of the UAE. Thank you, Your Excellency, for providing us with your High Patronage and that of The Ministry of Economy and honouring our Conference with your active participation. Ritossa Family Office looks forward to our longterm friendship and collaboration." Sir Anthony Ritossa, Chairman of Ritossa Family Office & Host of Ritossa Global Family Office Investment Summits, UAE Personal message from our Distinguished Grand Ambassador for the 16th Ritossa Global Family Office Investment Summit: "It is an honour and a pleasure to be the 16th Ritossa Global Family Office Investment Grand Ambassador in Dubai on October 3-5, 2021. -

Almas Tower 1 Almas Tower

Almas Tower 1 Almas Tower Almas Tower ﺑﺮﺝ ﺍﻟﻤﺎﺱ The Almas Tower General information Status Complete Type Commercial Location Dubai, United Arab Emirates Coordinates 25°04′08.25″N 55°08′28.34″E Construction started 2005 Completed 2008 Opening 2009 Height [1] Architectural 360 m (1,181 ft) [1] Top floor 279.3 m (916 ft) Technical details [1] Floor count 74 (68 above ground, 5 basement floors) [1] Floor area 160,000 m2 (1,700,000 sq ft) [1] Lifts/elevators 35 Design and construction Owner Dubai Multi Commodities Centre [1] Architect Atkins Middle East [1] Developer Nakheel Properties [1] Main contractor Taisei Corporation Almas Tower 2 Diamond Tower) is a supertall skyscraper in JLT Free Zone Dubai, United Arab ﺑﺮﺝ ﺍﻟﻤﺎﺱ :Almas Tower (Arabic Emirates. Construction of the office building began in early 2005 and was completed in 2009 with the installation of some remaining cladding panels at the top of the tower. The building topped out at 360 m (1,180 ft) in 2008, becoming the third-tallest building in Dubai, after Emirates Park Towers and Burj Khalifa. Almas Tower has 74 floors, 70 of which are commercial alongside four service floors. The tower is located on its own artificial island in the centre of the Jumeirah Lakes Towers Free Zone scheme, the tallest of all the buildings on the development when completed. It was designed by Atkins Middle East, who designed most of the JLT Free Zone complex. The tower is being constructed by the Taisei Corporation of Japan in a joint venture with ACC (Arabian Construction Co.) who were awarded the contract by Nakheel Properties on 16 July 2005.[2] Dubai Multi Commodities Centre (DMCC), the owner of the tower, was the first to move in. -

EVERSENDAI CORPORATION BERHAD EVERSENDAI ENGINEERING FZE EVERSENDAI ENGINEERING LLC EVERSENDAI Offshore SDN BHD Plot No

Towering – Powering – Energising – Innovating Moving to New Frontiers MANAGEMENT SYSTEMS EXECUTIVE CHAIRMAN & GROUP MANAGING DIRECTOR’s MESSAGE TAN SRI A.K. NATHAN Moving To New Frontiers The history of Eversendai goes back to 1984 and As we move to new frontiers, we are certain we after three decades of unparalleled experience, will be able to provide our clients the certainty and engineering, technical expertise and a strong network comfort of knowing that their projects are in capable across various countries, we are recognised as a and experienced hands. These developments will leading global organisation in undertaking turnkey complement our vision, mission and core values and contracts; delivering highly complex projects with simultaneously allow us to remain one of the most innovative construction methodologies for high rise successful organisations in the Asian and Middle buildings, power & petrochemical plants as well as Eastern Region and beyond with corresponding composite and reinforced concrete building structures efficiency and reliability. in the Asian and Middle Eastern regions. The successful and timely completion of our projects We have a dedicated workforce of over 10,000 accompanied by soaring innovation, creativity and people and an impressive portfolio of more than 290 our aspiration to move to new frontiers have been the accomplished projects in over 14 different countries key drivers for achieving continuous growth through with 5 steel fabrication factories located in Malaysia, the years and we remain committed to these values. Dubai, Sharjah, Qatar and India, with an annual This stamps our firm intent to dominate the various capacity of 150,000 tonnes. With our state-of-the-art industries which we are involved in and also marks steel fabrication factories, we have constructed some the next phase in our development to be amongst the of the world’s most iconic landmark structures. -

Dubai & Abu Dhabi

GLM 2015-2016 BUILDING VISIONS WITH GLASS & STEEL DUBAI STUDY TRIP REPORT GLM 2015-2016 EDITORIAL NOTE wo days into our trip to Dubai, we paid a visit to the Juma Al-Majid Center for Culture and Heritage. One of the center’s main purposes is to document TDubai’s humble beginnings as a coastal village in the early 1950s and 60s. The black and white photographs on display present a different versionof the city, seemingly incompatible with the vertigo of glass and steel skyscrapers we have been immersed in over the last two days. We see photographs of the city’s creek bespeckled with wooden barges, and its fish market, a collection of small wooden stalls with palm-leaf thatching. It is now an integral part of Dubai’s mythology to present it as a city which has “emerged” from the desert practically overnight, flouting any clearsense of agency in its construction. But pragmatically, how does one plan and oversee the con- struction of such a large-scale project? What could have possibly guided Dubai’s builders other than that elusive sense of “vision”, which has now become an inte- gral part of the city’s discourse on its own development. It is no coincidence that the current Sheikh, Mohammed ben Rashid Al Maktoum’s 2012 memoir was titled “My Vision: Challenges in the Race for Excellence”. The notion of vision is equally at the heart of the 1968 British documentary “Fare- welll to Arabia” which documents the early days of Abu Dhabi’s Sheikh Zayed in power. In addition to the rare footage on life in 1960s Abu Dhabi it provides, the documentary draws a powerfully introverted portrait of Sheikh Zayed as a man at the crossroads of history, whose task is to selectively welcome western inno- vations into his kingdom. -

Hotel Intelligence Dubai

Hotels & Hospitality Group | May 2014 Hotel Intelligence Dubai 2 Hotel Intelligence: Dubai Table of Contents Contributors Market Snapshot 3 Sumati Murari Associate Dubai Continuous growth in hotel guest arrivals 4 [email protected] Passenger arrivals continue to rise 6 Dubai’s ambition vision for tourism 2020 6 Market preference for upscale accommodation 7 Rahul Kamalapurkar Analyst Dubai Expanding pipeline due to market recovery 8 [email protected] Hotel performance recovers after economic 11 downturn Hotel performance to remain strong 12 Jessica Jahns Head of Pan-EMEA Research [email protected] Alexander French Pan-EMEA Research Assistant [email protected] JLL’s Hotels & Hospitality Group serves as the hospitality industry’s global leader in real estate services for luxury, upscale, select service and budget hotels; timeshare and fractional ownership properties; convention centres; mixed-use developments and other hospitality properties. The firm’s 300 dedicated hotel and hospitality experts partner with investors and owner/operators around the globe to support and shape investment strategies that deliver maximum value throughout the entire lifecycle of an asset. In the last five years, the team completed more transactions than any other hotels and hospitality real estate advisor in the world totalling nearly USD 36 billion, while also completing approximately 4,000 advisory, valuation and asset management assignments. The group’s hotels and hospitality specialists provide independent and expert advice to clients, backed by industry-leading research. For more news, videos and research from JLL’s Hotels & Hospitality Group, please visit: www.jll.com/hospitality or download the Hotels & Hospi- tality Group’s iPhone app or iPad app from the App Store. -

DUBAI: WHOSE CITY? Authenticity; Continuity; Dubai; Durability; Gunilla ENHÖRNING Heritage; Identity; Sustainability

CCSCT 2009, Bo÷aziçi University, Istanbul, Turkey 2 the subheadings of Authenticity, Continuity, and Durability as the key factors underpinning the sound development of all cities. KEYWORDS DUBAI: WHOSE CITY? Authenticity; Continuity; Dubai; Durability; Gunilla ENHÖRNING Heritage; Identity; Sustainability. Chalmers University of Technology, Sweden [email protected] Brian J. SHAW The University of Western Australia, Australia [email protected] ABSTRACT As the world’s cities compete in an increasingly competitive and uncertain global financial cauldron, they seek to exploit elements of local identity to leverage ever greater investment shares. If such identity is absent or inadequate then, through necessity, it must be created. Authenticity is no longer a prerequisite for the celebration and commodification of local identity, as exemplified by the case of Dubai, now the largest city in the United Arab Emirates (UAE). The prevailing feature of Dubai’s rapid economic and social development has been the creation of a majority polyglot population, living and working in the Emirate without citizenship status and primordial local roots. In such an environment decision-making processes re- garding planning and matters of identity have taken on a top-down quality without the need to achieve a broad popular consensus. The city has become a captive of the moment, formulated after the needs and demands of developers with a celebration of the special and the spectacular rather than an emphasis on sustainability. Focusing on the latter, Swedish planners have stressed four starting points for city planning, these are the provision of an arena of free economy, main- taining an everyday milieu for most inhabitants, an emphasis on heri- tage retention, and as a place which creates and consumes resources. -

Arabian Gu Lf a R a Bi an Gulf

Map of Dubai The Palm Deira u/c 2009 The World u/c 2008 W a t e r f r o n t The Palm Jebel Ali The Palm Jumeirah The Crescent Kingdom Atlantis of Sheba S ub- Sea Tun nel Emerald Palace Kempinski M aritim e C en tre D r The iv Marina e District The Maritime Centre Dusit Harbour A Maritime Residences Seafarers Academy Club The Fronds Bonnington r Residence JEBEL ALI HARBOUR DUBAI a Industrial MARITIME N d Precinct a o R d i West j a M n i B d CITY e m h A Breakwater S b d a o R d ji East Taj Exotica a M in B d e m h Tanker i A Berth Breakwater No. 9 Helicopter a Harbour Pad Marina Offices Tanker n Residences Jebel Ali Berth Grandeur Golf Resort No. 7 Residences & Spa Dubai G Cart Club Hassah u Tanker l Marina f Berth No. 5 Royal Amwaj f His Highness Tanker the Ruler`s Garden Berth The Resort No. 3 l Golf Course Container Terminal S JEBEL ALI PORT The Fairmont Palm u he Hotel & Resort Shoreline ik Tanker Apartments h Berth G Dubai Za UAE No. 1 Jumeirah Al Fattan ye Palm Resort d Hassah Navy Dry Ro Palace ENOC Trump Int`l PORT RASHID ad Hotel & Tower n EPPCO a Coaster Al Shindagha A r a b i Docks Berth Department of ENOC The Palm Ports and Customs oad ENOC l Mina R Golden A Heritage & Sheikh Saeed Diving Village House Mile D92 Bin S A Al Shindagha h l Private Dubai Beach Port Administration Suroor in Shoreline Market Mosque dag Dubai Tu h Island Diving Al n a Deira Fish, Meat & Gh t n Apartments uba e e West Swedish iba e Vegetable Market Centre Ro r l Dubai Marine ad t S Consulate 1 AL MINA h 3A Wharf a D85 Beach Resort H.H. -

OBSERVER Dubai Residential Report Q2 2020 Market Overview

OBSERVER Dubai Residential Report Q2 2020 Market Overview Dubai’s residential sector faced a challenging second quarter, with social distancing measures, coupled with Covid-19’s economic impact, affecting market performance. Average apartment rents fell by 3.9% quarter-on-quarter (q-o-q) and 9.5% year-on-year (y-o-y), with average villa rents seeing more moderate declines of 2.6% q-o-q and 7.2% y-o-y. While social distancing policies broadly restricted the rental market over April, activity recovered in May, driven by tenants looking to reduce rental costs or take advantage of lower rents to upsize. The impact on residential prices was less pronounced, with the average price of recorded off-plan transactions seeing a slight uplift, while both new listing and completed unit prices fell. On average, Chestertons estimates that apartment and villa prices saw quarterly falls of 2.6% and 1.2%, respectively. A total of 5,233 residential units were sold over Q2, representing a quarterly decline of 45%, with corresponding transaction value falling by 40% to AED 9.06 billion. When looked at on a monthly basis, June transaction figures were encouraging and point towards more typical sales volumes over the third quarter. While clearly a testing period, there were also positives to draw from Q2. Developers held back new off-plan sales launches, a move that bodes well for more balanced supply and demand dynamics medium-term. Dubai also took a step towards greater market transparency, with the routine release of its official house price index, Mo’asher, likely to give rise to greater investor confidence. -

Delegate Registration Form

Delegate Registration Form Please complete the entire form! 4 EASY WAYS TO REGISTER Telephone +971 4 3539750 Fax +971 4 3539760 Email [email protected] Mail 405, Al Arif Business Bay, P.O. Box 126093, Dubai, United Arab Emirates � Mr � Ms Delegate Name Organization: Designation: Address: City: Postal code: Country: Telephone: Fax: Mobile: Email: For International Delegates: Arrival Date: Flight Number Departure Date: Flight Number Name of accompanying person/s: Registration fees: � Delegate Fees - US $ 400.00* (NET) per delegate (Fee includes entrance to the 2 day Forum including Lunch, Pre Conference networking cocktail on 16th February 09, Gala Dinner on 17th February 09 and launch of the Dubai Pearl Exchange on 18th February 09 ) � Accompanying Persons – Fee US $ 200.00* (NET) per person (Fee includes attendance at Pre Conference networking cocktail on 16th February 09, Gala Dinner on 17th February 09 and launch of the Dubai Pearl Exchange on 18th February 09 ONLY, otherwise full delegate fee is applicable) Special Fees: � Early bird (Booking before 15th November 2008) – Fee US $ 325.00* (NET) per delegate � Dubai Pearl Exchange Members - Fee US $ 300.00* (NET) per delegate � Corporate groups (minimum 5 delegates representing same company) – Fee US $ 325.00* (NET) per delegate * Rooms reserved for delegates at the Atlantis are to be booked directly with hotel on a first come first serve basis. The delegate fee does not include accommodation. Payment Options I Prefer To Pay By: � Bank Transfer: UAE Dirham or USD transfer to; Beneficiary: Dubai Pearl Exchange DMCC Account No. 021 699301 001 Account Name: Dubai Pearl Exchange DMCC HSBC Bank, Main Branch, P.O.