D2.3 Market Trends Analysis in Asia January 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Final Call for Papers

Final Call for Papers MOC2021 26th MICROOPTICS CONFERENCE http://moc2021.com/ Sponsored by The Japan Society of Applied Physics (JSAP) Organized by Microoptics Group, JSAP M C Technically co-sponsored by IEEE Photonics Society In cooperation with The Optical Society of Japan IEICE Electronics Society IEEE Photonics Society Japan Chapter IEEE Photonics Society Kansai Chapter The Chemical Society of Japan The Society of Polymer Science, Japan The Laser Society of Japan Optoelectronics Industry and Technology Development Association Japan Optomechatronics Association Japan Photonics Council Hamamatsu City Shizuoka University Sep. 26 (Sun.) - Sep. 29 (Wed.), 2021 Congress Center, ACT CITY Hamamatsu, Shizuoka, Japan May 10 (Mon.) Paper Deadline: April 23 (Fri.), 2021 PLENARY TALKS Dieter Bimberg, CIOMP, CAS / TU Berlin "Novel VCSEL Designs for the Next Generation of Photonic Systems" Federico Capasso, Harvard Univ. "Multifunctional Flat Optics" Tsutomu Hara, Hamamatsu Photonics "Exploring Photonics" Katsumi Kishino, Sophia Univ. "InGaN-Based Nanocolumn Optical Devices" INVITED TALKS Kuo-Ping Chen, National Chiao Tung Univ. "Structural Colors and Lasers by Lattice Resonance in Silicon Nitride Metasurfaces" Simon Fafard, Broadcom Semiconductors ULC "High Efficiency Photovoltaic Power Converters and Application to Optical Power Transmission" Harald Haas, Univ. Strathclyde "Recent Advancements in Optical Wireless Communications" Yuri Kivshar, Australian National Univ. "Metaphotonics and Metasurfaces Governed by Mie Resonances" Jan Meijer, Univ. Leipzig "Quantum Light Sources Using Color Centers in Diamond" Peter O'Brien, Tyndall National Institute "Photonics Packaging for Integrated Photonics, from Research to Pilot-Scale Manufacturing" Wolfgang Osten, Univ. Stuttgart "Optical Metrology and Sensing in Times of Digital Transition" Min Qiu, Westlake Univ. "Microscale Opto-Thermo-Mechanical Actuation in the Adhesive Regime" 2 Niels Quack, Ecole Polytech. -

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

Vol.11 No 16 August 30, 2019.Pmd

1 Nuclear, MissileNuclear, Missile & Space Digest & Space Digest Volume 11, Number 16 A Fortnightly Newsletter from the Indian Pugwash Society August 31, 2019 Convenor A. India Cabinet approves MoU between India and Tunisia on Cooperation in the Amb. Sujan R. Chinoy Exploration and Use of Outer Space for Peaceful Purposes ISRO announces Vikram Sarabhai Journalism Award in Space Science, Technology and Research 2-day exhibition on DAE Technologies: Empowering India through Technology, inaugurated in New Delhi Vikram lander will land on Moon as a tribute to Vikram Sarabhai from crores of Indians: PM Shri Narendra Modi Arms tangle Nuke plants' rescue jolts conservatives, environmentalist Earth as viewed by Chandrayaan-2: Isro shares 1st pictures Indian science has landmark moment at ITER, a global effort to create first- Executive Council ever nuclear fusion device Cdr. (Dr.) Probal K. Ghosh Chandrayaan 2: When will Lunar spacecraft reach Moon's orbit? ISRO reveals date Air Marshal S. G. Inamdar ISRO's new commercial arm gets first booking for launch (Retd.) ISRO's success is Vikram Sarabhai's lasting legacy Dr. Roshan Khanijo B. China Amb. R. Rajagopalan New port will host sea-based space launches Dr. Rajesh Rajagopalan Shanghai kicks off military recruitment, targeting college graduates Shri Dinesh Kumar China builds more powerful 'eyes' to observe the sun Yadvendra Commander of PLA Garrison in HK says violence 'totally intolerant' 7th Military World Games torch relay starts from Nanchang China's micro lunar orbiter crashes into Moon under control Russian deputy defense minister: China-Russian relations help safeguard international stability China opposes U.S. -

Photonics and Quantum Technology for Society 5.0 Research And

Cross-ministerial Strategic Innovation Promotion Program (SIP) Photonics and Quantum Technology for Society 5.0 Research and Development Plan August 8, 2019 Director General for Science, Technology, and Innovation Cabinet Office Contents OVERVIEW OF THE RESEARCH AND DEVELOPMENT PLAN ............................................. 4 1. SIGNIFICANCE AND TARGETS .................................................................................................... 4 2. RESEARCH AND DEVELOPMENT THEMES .................................................................................. 4 3. IMPLEMENTATION STRUCTURE ................................................................................................. 4 4. INTELLECTUAL PROPERTY MANAGEMENT ................................................................................ 4 5. ASSESSMENTS .......................................................................................................................... 5 6. HARVESTING STRATEGY .......................................................................................................... 5 1. SIGNIFICANCE AND TARGETS ............................................................................................ 6 (1) BACKGROUND AND DOMESTIC/OVERSEAS SITUATION ............................................................... 6 (2) SIGNIFICANCE AND POLITICAL IMPORTANCE ............................................................................ 6 (3) TARGETS AND GOALS ............................................................................................................ -

Orange Economy? Question 2

Launching an orange future Fifteen questions for getting to know the creative entrepreneurs of Latin America and the Caribbean Content How can we assure that creative entrepreneurships Question 1. 04 blossom in Latin America and the Caribbean? What is the orange economy? Question 2. 08 Understanding the importance of being creative Who are the creative entrepreneurs Question 3. 16 of Latin America and the Caribbean? Question 4. How can you learn how to launch an entrepreneurship? 19 Question 5. How are creative entrepreneurships like? 23 Question 6. Do creative entrepreneurships have a social impact? 32 Question 7. Where do creative entrepreneurs work? 37 Question 8. How are creative entrepreneurships financed? 62 How healthy are the creative entrepreneurships Question 9. 66 in Latin America and the Caribbean? Why do creative entrepreneurships fail Question 10. 70 and how often? What factors influence the happiness Question 11. 79 of creative entrepreneurs? How much do creative entrepreneurs understand Question 12. 83 about intellectual property? How could different social actors contribute Question 13. 88 to the growth of creative industries? How can we encourage creative entrepreneurship Question 14. 95 through a regional brand? What can we learn from laws that Question 15. 101 have supported creative industries? Stories & interviews 104 Data 128 Glossary 155 In order to learn how a creative entrepreneurship can flourish in Latin America and the Caribbean, first it is necessary to know the talent that will develop the projects. Launching an Orange Future, you will not only get to know what the creative entrepreneurs in the region are like, you will also get to know their perceptions, failures, successes as well as the health of their entrepreneurships. -

FAST RETAILING CO., LTD. Takeda Pharmaceutical Co., Ltd. Nisshin

ANNUAL REPORT OF PROXY VOTING RECORD REPORTING PERIOD: JULY 1, 2018 – JUNE 30, 2019 WisdomTree Japan Equity Index ETF (JAPN/JAPN.B) _________________________________________________________________________________________________________ FAST RETAILING CO., LTD. Meeting Date: 11/29/2018 Country: Japan Primary Security ID: J1346E100 Record Date: 08/31/2018 Meeting Type: Annual Ticker: 9983 Shares Voted: 50 Vote Proposal Text Proponent Mgmt Rec Instruction Elect Director Yanai, Tadashi Mgmt For For Elect Director Hambayashi, Toru Mgmt For For Elect Director Hattori, Nobumichi Mgmt For For Elect Director Shintaku, Masaaki Mgmt For For Elect Director Nawa, Takashi Mgmt For For Elect Director Ono, Naotake Mgmt For For Elect Director Okazaki, Takeshi Mgmt For For Elect Director Yanai, Kazumi Mgmt For For Elect Director Yanai, Koji Mgmt For For Appoint Statutory Auditor Tanaka, Akira Mgmt For For Appoint Statutory Auditor Kashitani, Takao Mgmt For For Takeda Pharmaceutical Co., Ltd. Meeting Date: 12/05/2018 Country: Japan Primary Security ID: J8129E108 Record Date: 10/19/2018 Meeting Type: Special Ticker: 4502 Shares Voted: 4,500 Vote Proposal Text Proponent Mgmt Rec Instruction Approve Issuance of Common Shares in Mgmt For For Preparation for Acquisition of Shire Plc Elect Director Ian Clark Mgmt For For Elect Director Olivier Bohuon Mgmt For For Elect Director Steven Gillis Mgmt For For Nisshin Steel Co., Ltd. Meeting Date: 12/10/2018 Country: Japan Primary Security ID: J57828105 Record Date: 09/30/2018 Meeting Type: Special Ticker: 5413 ANNUAL REPORT OF PROXY VOTING RECORD REPORTING PERIOD: JULY 1, 2018 – JUNE 30, 2019 WisdomTree Japan Equity Index ETF (JAPN/JAPN.B) _________________________________________________________________________________________________________ Nisshin Steel Co., Ltd. -

Chinese Space Law: Problems and Areas of Reforming Olga Yeshchuk1

Chinese Space Law: Problems and Areas of Reforming Olga Yeshchuk1 Doctor of Law, Associate Professor, Kherson State University (Kherson, Ukraine). E-mail: [email protected] https//orcid.org/0000-0002-7458-1595 Anna Vasina2 Graduate student at the Public Law Research Institute, Hangzhou Pendant Technology Co. Ltd (Zhejiang, China). E-mail: [email protected] https//orcid.org/0000-0003-2280-8556 In the article, we have determined that China is a leading, but the only space state that does not have a special space law. These activities are governed by the international norms-principles, international treaties and by-laws of the government. We consider that such a procedure for regulating legal relations in the space industry is illogical. We have revealed the contours of the future space law of China in the article. We’ve noted that the signing of a Memorandum of Understanding on Space Cooperation with Luxembourg will have a positive impact on the exploration and utilization of mineral resources from the Moon and asteroids by Chinese space companies. At the same time, we have concluded that without the adoption of a special space law, foreign investments in the Chinese space industry and space tourism will be constrained. Keywords: White paper, space, law, normative legal acts, legislation. Received: December 21, 2018; accepted: February 27, 2019 Advanced Space Law, Volume 3, 2019: 140-150. https://doi.org/10.29202/asl/2019/3/12 Introduction The problems of Chinese national space law is the central one, because China is a leading space power, but does not have its own national space law. -

Multilayered Polycrystallization in Single-Crystal YSZ by Laser-Shock

Journal of Physics D: Applied Physics PAPER • OPEN ACCESS Related content - Femtosecond laser-driven shock-induced Multilayered polycrystallization in single-crystal dislocation structures in iron Tomoki Matsuda, Tomokazu Sano, Kazuto YSZ by laser-shock compression Arakawa et al. - Femtosecond laser induced nanostructuring of zirconium in liquid To cite this article: Yasuhiko Nishimura et al 2015 J. Phys. D: Appl. Phys. 48 325305 confined environment Nisar Ali, Shazia Bashir, Umm-i-Kalsoom et al. - Analysis of laser shock waves and resulting surface deformations in an View the article online for updates and enhancements. Al–Cu–Li aluminum alloy P Peyre, L Berthe, V Vignal et al. Recent citations - Modification of single-crystalline yttria- stabilised zirconia induced by radiation heating from laser-produced plasma Yoshitaka Mori et al - Characterizing near-surface firn using the scattered signal component of the glacier surface return from airborne radio-echo sounding Anja Rutishauser et al - Amorphous nanostructuralization in HOPG by 1014 W cm-2 laser Yasuhiko NISHIMURA et al This content was downloaded from IP address 134.197.0.88 on 24/08/2019 at 00:47 IOP Journal of Physics D: Applied Physics Journal of Physics D: Applied Physics J. Phys. D: Appl. Phys. J. Phys. D: Appl. Phys. 48 (2015) 325305 (6pp) doi:10.1088/0022-3727/48/32/325305 48 Multilayered polycrystallization in 2015 single-crystal YSZ by laser-shock compression © 2015 IOP Publishing Ltd Yasuhiko Nishimura1,2, Yoneyoshi Kitagawa1, Yoshitaka Mori1, 3 3 3 4 JPAPBE Tatsumi Hioki -

JASIS 2019 Exhibitors

JASIS 2019 Exhibitors Elemental Scientic, Inc. A Elementar Japan K.K. a priori Inc. ELGA LabWater A&D Company, Limited ELIONIX INC. ACTAC.CO.,LTD Emerging Technologies Corporation. Acumentech Co., Ltd. entex inc. AD Science Inc. Eppendorf Co., Ltd. Advanced Energy Japan K.K. ERECTA International Corporation Advantec Toyo Kaisha, Ltd. ESPEC CORP. ADVANTEST CORPORATION ESPEC MIC CORP. Agilent Technologies Japan,Ltd. ETRI AINEX CO., LTD. Excimer,inc AIRIX Corp. Airtech Corporation AIVS Corporation F Alpha M.O.S. Japan K.K. Filgen, Inc. AMETEK Co, Ltd FLON CHEMICAL INC. AMR, Inc. FLON INDUSTRY CO., LTD. analytica-Messe Muenchen ForDx, Inc. Analytik Jena Japan Co., Ltd. Forum for Innovative Regenerative Medicine(FIRM) ANRITSU METER CO., LTD. FUJIKIN Incorporated Anton Paar Japan K.K. Fujitsu Limited Aomori Prefecture Quantum Science Center FUKUSHIMA INDUSTRIES CORP. APRO Science Institute, Inc. FUSO Co., Ltd. ARAM CORPORATION FUTA-Q,Ltd. AS ONE CORPORATION ASAHI KOHSAN Co.,Ltd Asahi Lab Commerce, Inc. G ASAHI LIFE SCIENCE CO.,LTD GASTEC CORPORATION ASAHI RUBBER INC. GC INSTRUMENTS ASAHI TECHNEION CO., LTD. GE Healthcare Japan Corporation ASCH JAPAN CO.,LTD GERSTEL K.K. ASI-AURORA GL Sciences Inc. ASICON Tokyo Ltd. Glass Expansion Pty. Ltd. Association for structure characterization Global Facility Center,HOKKAIDO UNIVERSITY ASTECH CORPORATION GTR TEC CORPORATION ATAGO CO., LTD. GVS Japan K.K. B H BAS Inc. hagataya.co.ltd BD Consulting L.L.C. Hakuto Co., Ltd. BeatSensing co.,ltd. HAMAMATSU PHOTONICS K.K. Beckman Coulter K.K. Hamilton Company Japan K.K. BEIJING LINGGONG TECHNOLOGY CO.,LTD Hanaichi UltraStructure Research Institute BETHL Co.,Ltd. -

Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017

Report of Activities Pursuant to Act 44 of 2010 Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017 Appendix D: Securities Held by Funds The Four Funds hold thousands of publicly and privately traded securities. Act 44 directs the Four Funds to publish “a list of all publicly traded securities held by the public fund.” For consistency in presenting the data, a list of all holdings of the Four Funds is obtained from Pennsylvania Treasury Department. The list includes privately held securities. Some privately held securities lacked certain data fields to facilitate removal from the list. To avoid incomplete removal of privately held securities or erroneous removal of publicly traded securities from the list, the Four Funds have chosen to report all publicly and privately traded securities. The list below presents the securities held by the Four Funds as of June 30, 2017. 1345 AVENUE OF THE A 1 A3 144A AAREAL BANK AG ABRY MEZZANINE PARTNERS LP 1721 N FRONT STREET HOLDINGS AARON'S INC ABRY PARTNERS V LP 1-800-FLOWERS.COM INC AASET 2017-1 TRUST 1A C 144A ABRY PARTNERS VI L P 198 INVERNESS DRIVE WEST ABACUS PROPERTY GROUP ABRY PARTNERS VII L P 1MDB GLOBAL INVESTMENTS L ABAXIS INC ABRY PARTNERS VIII LP REGS ABB CONCISE 6/16 TL ABRY SENIOR EQUITY II LP 1ST SOURCE CORP ABB LTD ABS CAPITAL PARTNERS II LP 200 INVERNESS DRIVE WEST ABBOTT LABORATORIES ABS CAPITAL PARTNERS IV LP 21ST CENTURY FOX AMERICA INC ABBOTT LABORATORIES ABS CAPITAL PARTNERS V LP 21ST CENTURY ONCOLOGY 4/15 -

R&Co Risk-Based Japan Index

Rothschild & Co Risk-Based Japan Index Indicative Index Weight Data as of June 30, 2021 on close Constituent Exchange Country Index Weight(%) McDonald's Holdings Co Japan L Japan 1.29 Idemitsu Kosan Co Ltd Japan 1.12 SoftBank Corp Japan 1.05 Nintendo Co Ltd Japan 0.86 Hitachi Metals Ltd Japan 0.83 Yakult Honsha Co Ltd Japan 0.82 Iwatani Corp Japan 0.81 ENEOS Holdings Inc Japan 0.79 FUJIFILM Holdings Corp Japan 0.78 KDDI Corp Japan 0.75 Toshiba Corp Japan 0.73 Calbee Inc Japan 0.73 Ajinomoto Co Inc Japan 0.72 Eisai Co Ltd Japan 0.72 Nissin Foods Holdings Co Ltd Japan 0.71 Morinaga Milk Industry Co Ltd Japan 0.70 Japan Tobacco Inc Japan 0.66 H.U. Group Holdings Inc Japan 0.66 JCR Pharmaceuticals Co Ltd Japan 0.64 MEIJI Holdings Co Ltd Japan 0.64 Yamazaki Baking Co Ltd Japan 0.63 Chugoku Electric Power Co Inc/ Japan 0.63 Nippon Gas Co Ltd Japan 0.63 PeptiDream Inc Japan 0.62 Chubu Electric Power Co Inc Japan 0.62 Seven & i Holdings Co Ltd Japan 0.62 FP Corp Japan 0.61 Pola Orbis Holdings Inc Japan 0.61 Lion Corp Japan 0.61 Shiseido Co Ltd Japan 0.60 Nippon Telegraph & Telephone C Japan 0.60 Nichirei Corp Japan 0.59 Japan Post Bank Co Ltd Japan 0.59 Kobayashi Pharmaceutical Co Lt Japan 0.59 Anritsu Corp Japan 0.58 Skylark Holdings Co Ltd Japan 0.58 Kyowa Kirin Co Ltd Japan 0.58 Lawson Inc Japan 0.58 Suntory Beverage & Food Ltd Japan 0.57 Kinden Corp Japan 0.57 MS&AD Insurance Group Holdings Japan 0.56 Shimano Inc Japan 0.56 Mitsubishi Corp Japan 0.56 Zensho Holdings Co Ltd Japan 0.56 Tokai Carbon Co Ltd Japan 0.56 Japan Post Holdings Co Ltd -

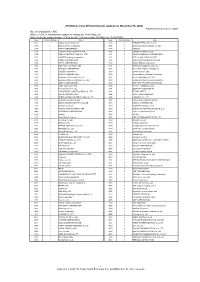

"JPX-Nikkei Index 400"

JPX-Nikkei Index 400 Constituents (applied on November 30, 2020) Published on November 9, 2020 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3086 1 J.FRONT RETAILING Co.,Ltd. 1333 1 Maruha Nichiro Corporation 3088 1 Matsumotokiyoshi Holdings Co.,Ltd. 1605 1 INPEX CORPORATION 3092 1 ZOZO,Inc. 1719 1 HAZAMA ANDO CORPORATION 3107 1 Daiwabo Holdings Co.,Ltd. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3116 1 TOYOTA BOSHOKU CORPORATION 1721 1 COMSYS Holdings Corporation 3141 1 WELCIA HOLDINGS CO.,LTD. 1766 1 TOKEN CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3167 1 TOKAI Holdings Corporation 1802 1 OBAYASHI CORPORATION 3197 1 SKYLARK HOLDINGS CO.,LTD. 1803 1 SHIMIZU CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1808 1 HASEKO Corporation 3288 1 Open House Co.,Ltd. 1812 1 KAJIMA CORPORATION 3289 1 Tokyu Fudosan Holdings Corporation 1820 1 Nishimatsu Construction Co.,Ltd. 3291 1 Iida Group Holdings Co.,Ltd. 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3349 1 COSMOS Pharmaceutical Corporation 1824 1 MAEDA CORPORATION 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1860 1 TODA CORPORATION 3382 1 Seven & I Holdings Co.,Ltd. 1861 1 Kumagai Gumi Co.,Ltd. 3391 1 TSURUHA HOLDINGS INC. 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3401 1 TEIJIN LIMITED 1881 1 NIPPO CORPORATION 3402 1 TORAY INDUSTRIES,INC.