Affordable Housing & CIL Development Viability Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cabinet Date Wednesday 25 May 2011 Time 9.30 Am Venue Council Chamber

Cabinet Date Wednesday 25 May 2011 Time 9.30 am Venue Council Cham ber - Council Offices, Spennymoor Public Question and Answer Session 9.30 a.m. to 10.00 a.m. An opportunity for local people to have a 30 minutes informal question and answer session with Cabinet Members. Cabinet Business 10.00 a.m. onwards Part A Items during which the Press and Public are welcome to attend. Members of the Public can ask questions with the Chairman's agreement. 1. Minutes of the Meetings held on 13 April and 21 April 2011 (Pages 1 - 8) 2. Declarations of interest, if any. Key Decisions 3. Partnership Agreement with County Durham and Darlington Foundation Trust for the Provision of Integrated Children's Services - Report of Corporate Director, Children and Young People's Services [Key Decision CYPS/04/10] (Pages 9 - 14) 4. Amendments to the Home-School / College Transport Policy - Report of Corporate Director Children and Young People's Services [ Key Decision CYPS/3/11] [MTFP Decision CYPS15(a) and (b)] (Pages 15 - 144) Ordinary Decisions 5. Review of Infrastructure Support to the Voluntary and Community Sector in County Durham - Report of Assistant Chief Executive (Pages 145 - 152) 6. County Durham Partnership Update Report - Report of Assistant Chief Executive (Pages 153 - 164) 7. Implications for Durham County Council of the Government's Policy Programme - Report of Assistant Chief Executive (Pages 165 - 194) 8. Data Protection Policy - Report of Assistant Chief Executive (Pages 195 - 228) 9. Implementing "Fulfilling and Rewarding Lives" - the Statutory Guidance for Local Authorities and NHS Bodies regarding the implementation of the Autism Act (2009) - Joint Report of Corporate Director Adults, Wellbeing and Health and Corporate Director, Children and Young People's Services (Pages 229 - 236) 10. -

Local Plan Submission Draft Published Version County Durham Plan Contents

Contents Foreword 5 1 Introduction 1 The Localism Act and the National Planning Policy Framework 1 Neighbourhood Plans 2 Developing the Local Plan 3 Cross Boundary Working - The Duty to Cooperate 4 Policy Delivery Areas 4 Supporting Documents and Evidence Base 5 Census 2011 6 Sustainability Appraisal 7 Habitat Regulation Assessment 7 Rural Proofing 8 Equality Impact Assessment 8 Health Impact Assessment 8 Monitoring and Implementation 8 Stages of Plan Preparation and Next Steps 9 How do you Get Involved 10 2 County Durham Context 13 Strategic Context 14 Regeneration Statement 15 Challenges 15 3 The Vision for County Durham 20 Vision 20 Objectives 22 Policy 1 - Sustainable Development 23 Local Plan Submission Draft Published Version County Durham Plan Contents 4 Core Policies 28 Policy 2 - Spatial Approach 28 Policy 3 - Quantity of Development 32 Policy 4 - Distribution of Development 36 Policy 5 - Developer Contributions 45 Policy 6 - Durham City 48 Policy 7 - Aykley Heads 53 Policy 8 - Durham City Strategic Housing Sites 56 Western and Northern Relief Roads 61 Policy 9 - Western Relief Road 64 Policy 10 - Northern Relief Road 66 Durham City Delivery 67 Policy 11 - Other Strategic Sites 70 Executive Housing 73 Policy 12 - Executive Housing Allocation 73 Policy 13 - Other Executive Housing Proposals 74 Policy 14 - Green Belt 76 5 General Development Principles 82 Policy 15 - Development on Unallocated Sites 82 Policy 16 - Sustainable Design in the Built Environment 83 Policy 17 - Exception Sites 87 Policy 18 - Local Amenity 90 Policy 19 -

County Durham Settlement Study September 2017 Planning the Future of County Durham 1 Context

County Durham Plan Settlement Study June 2018 Contents 1. CONTEXT 2 2. METHODOLOGY 3 3. SCORING MATRIX 4 4. SETTLEMENTS 8 County Durham Settlement Study September 2017 Planning the future of County Durham 1 Context 1 Context County Durham has a population of 224,000 households (Census 2011) and covers an area of 222,600 hectares. The County stretches from the North Pennines Area of Outstanding Natural Beauty (AONB) in the west to the North Sea Heritage Coast in the east and borders Gateshead and Sunderland, Northumberland, Cumbria and Hartlepool, Stockton, Darlington and North Yorkshire. Although commonly regarded as a predominantly rural area, the County varies in character from remote and sparsely populated areas in the west, to the former coalfield communities in the centre and east, where 90% of the population lives east of the A68 road in around half of the County by area. The Settlement Study 2017 seeks to provide an understanding of the number and range of services available within each of the 230 settlements within County Durham. (a) Identifying the number and range of services and facilities available within a settlement is useful context to inform decision making both for planning applications and policy formulation. The range and number of services within a settlement is usually, but not always, proportionate to the size of its population. The services within a settlement will generally determine a settlement's role and sphere of influence. This baseline position provides one aspect for considering sustainability and should be used alongside other relevant, local circumstances. County Durham a 307 Settlements if you exclude clustering 2 Planning the future of County Durham County Durham Settlement Study September 2017 Methodology 2 2 Methodology This Settlement Study updates the versions published in 2009 and 2012 and an updated methodology has been produced following consultation in 2016. -

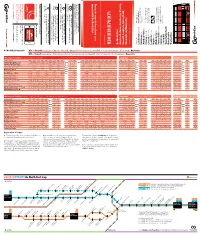

X30 | X31 | X 70 |

simplygo.com deals on Get exclusive everyone. cheaper and easier for the key smartcard the key be simpler! with us couldn’t Buying tickets simplygo.com/tickets and log on to Check out the options below everyone. for of tickets a range have We with Go North East money and save travel to ways Fantastic makes travelling travelling makes the key the key 130 simplygo.com /thekey town or city. town outside of your journey on a longer travel Choose the local area. in your the day throughout The a single fare. for or city local town your The and full time students. under 18s for travel on unlimited savings Our unique area. your within travel on unlimited save you more With smartcard DaySaver Saver X71 Buzzfare | for more information. more for ticket allows you to travel in travel to you allows ticket Get Around Cheap Day Return Cheap Day Buses run up to Buses run up to 15 minutes every » Sunniside » Gateshead Newcastle ramp access find You’ll bus and travel on every on board. advice safety VENTURE Including Lanchester, buses between Houses Burnhope, Quaking and Stanley. gives you unlimited travel travel unlimited you gives , the more you travel, the travel, you , the more simplygo.com and go. show Simply buy, mobile. your – m-ticket the m-ticket app the m-ticket X70 | simplygo.com X31 ticket offers big offers ticket X70 X71 X70 your bus ticket on bus ticket your X71 X30 X31 X30 /m-ticket X70 X71 X70 X31 for return return for X70 X71 X70 | X30 X31 X70 X70 /tickets Go North East X30 Bus times from 27 July 2014 27 Bus times from Burnhope Annfield -

Development Control Committee 13 11 08

Civic Centre , Medomsley Road, Consett, Co Durham. DH8 5JA Tel: 01207 218000 Fax: 01207 218200 www.derwentside.gov.uk Development Control Committee Councillors: J. I. Agnew (Chair), R. Alderson, A. Atkinson, M. Campbell, H. Christer, T. Clark (Vice-Chair), B. Cook, G. Coulson, R. Ellis, B. Gray, P. D. Hughes, D. Hume, D. Lavin, O. Milburn, T. Pattinson, S. J. Rothwell, A. Shield, E. Turner, A. Watson O.B.E, T. Westgarth, J. Williams, M. Wotherspoon, R. Young Dear Councillor, Your attendance is invited at a meeting of the Development Control Committee to be held in the Council Chamber, Civic Centre, Consett on 13th November 2008 at 2.00 p.m. for consideration of the undernoted agenda. MIKE CLARK Chief Executive Officer Agenda 1. APOLOGIES FOR ABSENCE To receive any apologies for absence. 2. DECLARATIONS OF INTEREST To receive any disclosure by Members of personal interests in matters ont he agenda, identify the item on the agenda, the nature of any interest and whether the Member regards the interest as prejudicial under the terms of the Code of Conduct. 3. MINUTES To approve the minutes of the following meetings as a correct record: Development Control Committee - 23rd October 2008 (Herewith 'A') Site Visit - 3rd November 2008 (Herewith 'B') Attached Documents: MINUTES (A) MINUTES (B) 4. APPEAL DECISIONS To consider the report of the Director of Environmental Services (Herewith 'C') Attached Documents: APPEAL DECISIONS (C) 5. PLANNING APPLICATIONS To consider the report of the Director of Environmental Services (Herewith 'D') Attached Documents: PLANNING APPLICATIONS (D) Agenda prepared by Lucy Stephenson, Democratic Services Tel: (01207) 218249 Email: [email protected] Date: 4th November 2008 A DEVELOPMENT CONTROL COMMITTEE Minutes of a meeting of the Development Control Committee meeting held in the Council Chamber, Civic Centre, Consett on Thursday 23rd October 2008 at 2.00 p.m. -

Final Recommendations on the Future Electoral Arrangements for Derwentside in County Durham

LOCAL GOVERNMENT COMMISSION FOR ENGLAND FINAL RECOMMENDATIONS ON THE FUTURE ELECTORAL ARRANGEMENTS FOR DERWENTSIDE IN COUNTY DURHAM Report to the Secretary of State for the Environment, Transport and the Regions October 1998 LOCAL GOVERNMENT COMMISSION FOR ENGLAND LOCAL GOVERNMENT COMMISSION FOR ENGLAND This report sets out the Commission’s final recommendations on the electoral arrangements for Derwentside in County Durham. Members of the Commission are: Professor Malcolm Grant (Chairman) Helena Shovelton (Deputy Chairman) Peter Brokenshire Professor Michael Clarke Pamela Gordon Robin Gray Robert Hughes Barbara Stephens (Chief Executive) ©Crown Copyright 1998 Applications for reproduction should be made to: Her Majesty’s Stationery Office Copyright Unit The mapping in this report is reproduced from OS mapping by The Local Government Commission for England with the permission of the Controller of Her Majesty’s Stationery Office, © Crown Copyright. Unauthorised reproduction infringes Crown Copyright and may lead to prosecution or civil proceedings. Licence Number: GD 03114G. This report is printed on recycled paper. ii LOCAL GOVERNMENT COMMISSION FOR ENGLAND CONTENTS page LETTER TO THE SECRETARY OF STATE v SUMMARY vii 1 INTRODUCTION 1 2 CURRENT ELECTORAL ARRANGEMENTS 3 3 DRAFT RECOMMENDATIONS 7 4 RESPONSES TO CONSULTATION 9 5 ANALYSIS AND FINAL RECOMMENDATIONS 11 6 NEXT STEPS 23 APPENDIX A Final Recommendations for Derwentside: Detailed Mapping 25 LOCAL GOVERNMENT COMMISSION FOR ENGLAND iii iv LOCAL GOVERNMENT COMMISSION FOR ENGLAND Local Government Commission for England 20 October 1998 Dear Secretary of State On 14 October 1997 the Commission began a periodic electoral review of Derwentside under the Local Government Act 1992. We published our draft recommendations in April 1998 and undertook an eight- week period of consultation. -

Durham County Council LA 100019779

C D E F G H J K Index of places served Index of places of interest South Shields West Jesmond Howden Barnard Castle .................................................... D7 Killhope Lead Mining Centre ............................ A4 Newcastle Hadrian Percy South Shields Road Main County Durham A L Eldon Square 20 50 50A Beamish Museum ................................................ F2 Low Force ............................................................ B5 Wallsend Annfield Plain ................................................ F3 Lanchester .................................................... E3 Binchester Roman Fort .................................... 6 6A 21 25 28 28A F5 Lumley Castle........................................................ G3 Jesmond Arnison Centre ............................................ G3 Lanehead ........................................................ A4 Bowes Museum, The............................................ D7 Net Park ................................................................ H5 45 X9 X10 X12 X21 X30 Chichester Aycliffe ............................................................ G6 Langdon Beck................................................ B5 Public Transport Map Causey Arch ........................................................ F2 Pow Hill Country Park ........................................ D3 X31 X32 X45 X46 X70 X71 Aycliffe Industrial Estate ........................ G6 Langley Moor ................................................ G4 Walkergate De Vere Staley Hall Hotel ............................... -

Derwentside Local Plan Saved Policies

Foreword Background The 2004 planning reform introduced a new planning policy framework across the country. Furthermore Local Government reorganisation has resulted in the amalgamation of the 7 former Durham District and Borough Authorities with Durham County Council. As a result the new unitary council, Durham County Council as sole Local Planning Authority for County Durham, is preparing a new plan for the district known as the Local Development Framework. This new plan will transitionally replace the existing 9 adopted Local Plans. The new planning system made provision for the existing Local Plans to be ‘saved’ for an initial three year period. This is to ensure that they remained a material consideration for the determination of planning applications and to safeguard against a policy vacuum. This initial three year period ended on 27th September 2007. As the former Council’s of County Durham were still in the early stages of preparing the new plan for their respective areas an application was made directly to the Secretary of State for Communities and Local Government to ‘save’ the Local Plan policies still considered necessary for a further three years. Each former Council’s application was successful as a result directions were served on each Council confirming all policies to be saved and extending their life for a further three years. These policies can therefore continue to be used in the determination of planning applications. The remaining policies expired on 27 th September 2007; they were effectively deleted on this date. To make the application to the Secretary of State for Communities and Local Government, the Councils had to follow a strict protocol. -

LTP3 Appendices Document

Local Transport Plan 3 Appendices LTP3 Appendices Document A LTP3 Policies & Daughter Strategies 4 B Performance Indicators 36 C Minor Schemes Review 42 D Settlements 50 E Community Transport Providers 54 F Regeneration Statement Summary 58 G Sustainable Community Strategy (SCS) Summary 62 H County Durham Plan 66 I Durham City 68 J Durham Coast Line - New Station Outline Case 72 K East Durham Link Road - Remaining Stage Outline Case 76 L The Leamside Line 80 M The Weardale Line Concept 84 LTP3 Appendices Document Durham County Council LTP3 Appendices Document A .0 LTP3 Policies & Daughter Strategies Durham County Council 3 LTP3 Appendices Document A.0.1 In seeking to provide a comprehensive transport policy base for the information of the public and stakeholders, LTP3 also refers to other ancillary policies contained in daughter strategies and action plans, etc. that continue to be applied. Table A.0.1 lists the policies contained within LTP3 together with those of other associated plans and strategies. The policies which form the policy base of this local transport plan, together with their preambles, are laid out in numerical order within this Appendix. Table A.0.1 Strategies and related Policies Policy Number Topic Local Transport Plan 3 1 Corridor Improvements 2 Cross Boundary Connections 3 Electric Vehicles and Charging Points 4 Traffic Management 5 New Road Infrastructure 6 Climate Change & Carbon Emissions 7 Attitude Change 8 Freight 9 Road Charging and Workplace Parking 10 Demand Management 11 Road Safety 12 Speed Management 13 -

Dm/17/00097/Fpa

Planning Services COMMITTEE REPORT APPLICATION DETAILS APPLICATION NO: DM/17/00097/FPA Full planning permission for the erection of 75 houses, FULL APPLICATION DESCRIPTION: including associated access, infrastructure and open space NAME OF APPLICANT: Barratt Homes North East Land To The West Of ADDRESS: Syke Road Burnopfield ELECTORAL DIVISION: Burnopfield and Dipton Steve France, Senior Planning Officer CASE OFFICER: Telephone: 03000 264871 [email protected] DESCRIPTION OF THE SITE AND PROPOSALS The Site 1. The application site is 2.09 hectares of land to the west of Syke Road, the connecting road between Burnopfield and Pickering Nook. The site is next to the Lintz area of Burnopfield, which is described as a ‘local service centre’ in the County Durham Settlement Study, 2012. The nearest main towns are Consett, 4.7 miles to the south-west and Stanley 2.6 miles to the south east. 2. The site is located on the south side of the village, where the adjacent housing areas are, with one small exception at the western part of the site, local authority built. The exception is a small development of ten dwellings arranged in two terraces that has been erected by the applicant, incorporating communal parking areas. Mid-linked two story dwellings to the north face away from the site, with-on-street parking along their rear boundaries. A small number of existing properties on the north boundary look across the top part of the site. The existing estate benefits from large areas of open space, including formal play provision, football and cricket pitches. 3.