2006 C H Ic A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

) ) LT 152009 ) Pollution Control Board ) ) ) ) ) ) ) ) ) ) ) ) ) )

BEFORE THE ILLINOIS POLLUTION CONTROL BOARD CEVE CLERK’S OFFICE PEOPLE OF THE STATE OF ILLINOIS ) LT ) 152009 Complainant, ) STATE OF ILLINOIS Pollution Control Board v. ) PCBNo. 10-9 ) (Enforcement - Land, Cost Recovery) WASTE HAULING LANDFILL, INC., JERRY ) CAMFIELD, A.E. STALEY MANUFACTURING ) CO., ARCHER DANIELS MIDLAND, INC., ) ARAMARK UNIFORM SERVICES, INC., BELL ) SPORTS, INC., BORDEN CHEMICAL CO., ) BRIDGESTONE/FIRESTONE, INC., CLIMATE ) CONTROL, INC., CATERPILLAR INC., COMBE ) LABORATORIES, INC., GENERAL ELECTRIC ) RAILCAR SERVICES CORPORATION, P & H ) MANUFACTURING, INC., TRINITY RAIL ) GROUP, INC., TRIPLE S REFINING ) CORPORATION, and ZEXEL ILLINOIS, INC., ) ) Respondents. ) ) NOTICE OF FILING TO: John T. Therriault, Assistant Clerk Carol Webb, Hearing Officer Illinois Pollution Control Board Illinois Pollution Control Board James R. Thompson Center 1021 North Grand Avenue East Suite 11-500 P.O. Box 19274 100 West Randolph Street Springfield, IL 62794-9274 Chicago, IL 60601 SEE ATTACHED SERVICE LIST Matthew J. Dunn, Chief James L. Morgan, Sr. Assistant Attorney General Environmental Bureau Environmental Enforcement/Asbestos Litigation Division 500 South Second Street Springfield, IL 62706 PLEASE TAKE NOTICE that on this date I have filed with the Office of the Clerk of the Pollution Control Board the Appearance of Jeffrey J. Freeman, a copy of which is herewith served upon you. Dated: October 14, 2009 TRIPLE S REFINING CORPORATION By: Jeffrey J. Freeman KIRKLAND & ELLIS LLP 300 North LaSalle Telephone: (312) 862-2000 Facsimile: (312) 862-2200 2 BEFORE THE ILLINOIS POLLUTION CONTROL BOARD PEOPLE OF THE STATE OF ILLINOIS ) ) Complainant, ) ) v. ) PCBNo. 10-9 ) (Enforcement - Land, Cost Recovery) WASTE HAULING LANDFILL, INC., JERRY ) CAMFIELD, A.E. -

FOR IMMEDIATE RELEASE July 18, 2014 CONTACT

FOR IMMEDIATE RELEASE July 18, 2014 CONTACT: Mayor’s Press Office 312.744.3334 [email protected] MAYOR EMANUEL ANNOUNCES THE SECOND EXPANSION OF RETROFIT CHICAGO’S COMMERCIAL BUILDINGS INITIATIVE 16 additional facilities commit to 20 percent energy efficiency improvement within five years; current participants have achieved seven percent energy reduction to-date Marking another milestone in the City’s efforts to accelerate energy efficiency, Mayor Rahm Emanuel today announced the further expansion of Retrofit Chicago’s Commercial Buildings Initiative. The new building participants, including 11 higher education facilities, four commercial office buildings, and one cultural institution, have committed to at least 20 percent energy efficiency improvement within five years. This announcement expands the total program reach to 48 buildings and 37 million square feet, making Retrofit Chicago’s Commercial Buildings Initiative one of the largest private sector voluntary efficiency programs in the country. “Retrofit Chicago participants are leading a rising private sector energy movement that demonstrates how efficiency makes good business sense and good sense for our environment,” said Mayor Emanuel. “These buildings’ operational and capital improvements are saving money, reducing carbon emissions, creating 21st century jobs, and lowering the cost of doing business in Chicago.” To-date, current program participants have collectively achieved a seven percent reduction in total source energy use, with accompanying annual energy cost savings of $2.5 million and greenhouse gas emissions reductions equivalent to removing 5,800 cars from the road. Upon reaching the 20 percent improvement target, all 48 building participants have potential to save more than 150 million kilowatt-hours of electricity per year, while creating hundreds of local jobs in the growing clean energy economy. -

FOR IMMEDIATE RELEASE March 6, 2013 CONTACT

FOR IMMEDIATE RELEASE March 6, 2013 CONTACT: Mayor’s Press Office 312.744.3334 [email protected] MAYOR EMANUEL ANNOUNCES RETROFIT CHICAGO: COMMERCIAL BUILDINGS INITIATIVE DOUBLES IN SIZE Including new office, hotel, large residential, institutional properties; total program reach to over 28 million square feet Today Mayor Emanuel announced 18 new participants in Retrofit Chicago’s Commercial Buildings Initiative, bringing the program’s total reach to over 28 million square feet. This doubles the 14 million square feet represented by the program’s founding 14 participants. The Commercial Buildings Initiative was launched on June 5 by Mayor Emanuel and U.S. Secretary of Energy Dr. Steven Chu. “This expansion of Retrofit Chicago’s Commercial Buildings Initiative highlights the leadership of commercial building owners, managers, and tenants in making Chicago a center of building efficiency and a place where companies are maximizing their ability to compete,” said Mayor Emanuel. “These participants understand that in the modern economic environment, it is critical to operate at maximum efficiency. The commitments that have been made by these 32 organizations will create jobs and foster growth throughout Chicago’s economy, while improving our environment as well.” Energy efficiency and clean energy comprise one of seven focus areas outlined in Sustainable Chicago 2015, a three-year roadmap to drive sustainability through city operations, in residents’ day-to-day lives, and across our economy. The Commercial Buildings Initiative is one component of Retrofit Chicago – the City’s cross-sector effort to accelerate energy efficiency in buildings – which also includes energy efficiency efforts in municipal and residential buildings. -

Buckingham Senior Living Community, Inc

Case 21-32155 Document 202 Filed in TXSB on 08/18/21 Page 1 of 128 IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION IN RE: § § CASE NO. 21-32155 (MI) BUCKINGHAM SENIOR LIVING § COMMUNITY, INC.1 § CHAPTER 11 § Debtor. § § AFFIDAVIT OF SERVICE I, Victoria X. Tran, depose and say that I am employed by Stretto, the claims and noticing agent for the Debtors in the above-captioned case. On August 16, 2021, at my direction and under my supervision, employees of Stretto caused the following documents to be served via first-class mail on the service list attached hereto as Exhibit E: former refund • [Customized] Former Resident Notice of Entry of Order Establishing Bar Dates for Filing Proofs of Claim (attached hereto as Exhibit A) • [Customized] Proof of Claim Official Form 410 • Proof of Claim Form Instructions (attached hereto ad Exhibit D) Furthermore, on August 16, 2021, at my direction and under my supervision, employees of Stretto caused the following documents to be served via first-class mail on the service list attached hereto as Exhibit F: Current Res • [Customized] Current Resident Notice of Entry of Order Establishing Bar Dates for Filing Proofs of Claim (attached hereto as Exhibit B) • [Customized] Proof of Claim Official Form 410 • Proof of Claim Form Instructions (attached hereto ad Exhibit D) Furthermore, on August 16, 2021, at my direction and under my supervision, employees of Stretto caused the following documents to be served via first-class mail on the service list attached hereto as Exhibit G: Matrix & Standard Schd. -

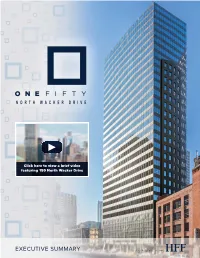

150 North Wacker Drive

Click here to view a brief video featuring 150 North Wacker Drive EXECUTIVE SUMMARY Holliday Fenoglio Fowler, L.P. (“HFF”) Holliday Fenoglio Fowler, L.P. (“HFF”) is pleased to present the sale of the 100% fee simple interest in 150 North Wacker Drive (the “Property”) located in the heart of Chicago’s Central Business District’s (“CBD”) most desirable submarket, the West Loop. The 31-story office tower is located one block east of Chicago’s Ogilvie Transportation Center on Wacker Drive – the home to many of Chicago’s most prestigious firms. The Property, consisting of 246,613 rentable square feet (“RSF”), is currently 91.9% leased and offers a significant mark to market opportunity in a best-in-class location on Wacker Drive. The Property is easily accessible via three major highways and the Chicago Transit Authority’s (“CTA”) transit and bus system, yet is still located in one of the most walkable areas of the city. Given the extensive common area renovations and recent leasing momentum, 150 North Wacker is a truly unique investment opportunity to acquire a rare asset with a premier Wacker Drive address and significant upside potential. KEY PROPERTY STATISTICS Location: 150 North Wacker Submarket: West Loop Total Rentable Area: 246,613 RSF Stories: 31 Percent Leased: 91.9% Weighted Average Lease Term: 4.0 Years Date Completed/Renovated: 1970/2002/2015 Average Floor Plates: 9,300 RSF Finished Ceiling Height: 8'9'' Slab to Slab Ceiling Height: 11'8'' Architect: Joel R. Hillman Parking: 134 Parking Stalls; Valet facilitates up to 160 Vehicles Transit Score: 100 Walk Score: 98 2 EXECUTIVE SUMMARY INVESTMENT HIGHLIGHTS NO. -

Illinois Pollution Control Board

Electronic Filing - Received, Clerk's Office, June 25, 2008 BEFORE THE ILLINOIS POLLUTION CONTROL BOARD IN THE MATTER OF: ) ) WATER QUALITY STANDARDS AND ) EFFLUENT LIMITATIONS FOR THE ) R08-9 CHICAGO AREA WATERWAY SYSTEM ) (Rulemaking - Water)· AND THE LOWER DES PLAINES RIVER: ) PROPOSED AMENDMENTS TO 35 Ill. ) Adm. Code Parts 301, 302, 303 and 304. ) NOTICE OF FILING To: see attached Service List PLEASE TAKE NOTICE that on the 25 th Day ofJune, 2008, I filed with the Office of the Clerk ofthe Illinois Pollution Control Board the attached Response of Environmental Law and Policy Center, Friends ofthe Chicago River, Sierra Club (Illinois Chapter), Natural Resources Defense Council and Openlands to the Metropolitan Water Reclamation District of Greater Chicago's Motion To Stay, a copy ofwhich is hereby served upon you. By:!!t~~- Dated: June 25, 2008 Environmental Law and Policy Center 35 East Wacker Drive, Suite 1300 Chicago, IL 60601-2110 312-795-3747 Electronic Filing - Received, Clerk's Office, June 25, 2008 CERTIFICATE OF SERVICE I, Albert Ettinger, the undersigned attorney, hereby certify that I have served the attached Response to the Metropolitan Water Reclamation District of Greater Chicago's Motion To Stay, on all parties ofrecord (Service List attached), by depositing said documents in the United States Mail, postage prepaid, from 35 East Wacker Drive, Suite 1300, Chicago, Illinois before the hour of5:00 p.m., on this 25 th Day ofJune, 2008. ~~ Electronic Filing - Received, Clerk's Office, June 25, 2008 Service List Richard J. Kissel and Roy M. Harsch Bernard Sawyer and Thomas Granto Drinker, Biddle, Gardner, Carton Metropolitan Water Reclamation District 191 N. -

Market Impact Analysis Psc Ref#:409444

PSC REF#:409444 Public Service Commission of Wisconsin RECEIVED: 04/15/2021 2:05:23 PM MARKET IMPACT ANALYSIS KOSHKONONG SOLAR ENERGY CENTER DANE COUNTY, WISCONSIN April 13, 2021 Koshkonong Solar Energy Center LLC c/o Invenergy LLC One South Wacker Drive – Suite 1800 Chicago, Illinois 60606 Attention: Aidan O’Connor, Associate - Renewable Development Subject: Market Impact Analysis Koshkonong Solar Energy Center Dane County, Wisconsin Dear Mr. O’Connor, In accordance with your request, the proposed development of the Koshkonong Solar Energy Center in Dane County, Wisconsin, has been analyzed and this market impact analysis has been prepared. MaRous & Company has conducted similar market impact studies for a variety of clients and for a number of different proposed developments over the last 39 years. Clients have ranged from municipalities, counties, and school districts, to corporations, developers, and citizen’s groups. The types of proposals analyzed include commercial developments such as shopping centers and big-box retail facilities; religious facilities such as mosques and mega-churches; residential developments such as high- density multifamily and congregate-care buildings and large single-family subdivisions; recreational uses such as skate parks and lighted high school athletic fields; and industrial uses such as waste transfer stations, landfills, and quarries. We also have analyzed the impact of transmission lines on adjacent residential uses and a number of proposed natural gas-fired electric plants in various locations. MaRous & Company has conducted numerous market studies of energy-related projects. The solar- related projects include the following by state: ⁘ Wisconsin - Badger Hollow Solar Farm in Iowa County, Paris Solar Energy Center in Kenosha County, Darien Solar Energy Center in Rock County and Walworth County, and Grant County Solar in Grant County. -

Illinois Pollution Control Board

Electronic Filing - Received, Clerk's Office, October 20, 2008 BEFORE THE ILLINOIS POLLUTION CONTROL BOARD IN THE MATTER OF: ) ) WATER QUALITY STANDARDS AND ) R08-9 EFFLUENT LIMITATIONS FOR THE ) (Rulemaking - Water) CHICAGO AREA WATERWAY SYSTEM ) AND THE LOWER DES PLAINES RIVER: ) PROPOSED AMENDMENTS TO 35 Ill. ) Adm. Code Parts 301, 302, 303 and 304 ) NOTICE OF FILING To: ALL COUNSEL OF RECORD (Service List Attached) PLEASE TAKE NOTICE that on the 20th day of October, 2008, I electronically filed with the Office of the Clerk of the Illinois Pollution Control Board, Metropolitan Water Reclamation District of Greater Chicago’s Motion to Allow Oral Statement of Thomas Granato. Dated: October 20, 2008 METROPOLITAN WATER RECLAMATION DISTRICT OF GREATER CHICAGO By: /s/ David T. Ballard One of Its Attorneys Fredric P. Andes David T. Ballard BARNES & THORNBURG LLP Suite 4400 One North Wacker Drive Chicago, Illinois 60606 (312) 357-1313 [This filing submitted on recycled paper as defined in 35 Ill. Adm. Code 101.202] Electronic Filing - Received, Clerk's Office, October 20, 2008 PROOF OF SERVICE The undersigned, a non-attorney, certifies, under penalties of perjury pursuant to 735 ILCS 5/1-109, that I caused a copy of the forgoing, Notice of Filing of Metropolitan Water Reclamation District of Greater Chicago’s Motion to Allow Oral Statement of Thomas Granato, to be served via First Class Mail, postage prepaid, from One North Wacker Drive, Chicago, Illinois, on the 20th day of October, 2008, upon the attorneys of record on the attached Service List. /s/ Barbara E. Szynalik Barbara E. Szynalik [This filing submitted on recycled paper as defined in 35 Ill. -

2021 ROSTER © 2021 Federation of Defense & Corporate Counsel, Inc

2021 ROSTER © 2021 Federation of Defense & Corporate Counsel, Inc. FEDERATION OF DEFENSE & CORPORATE COUNSEL FDCC OFFICERS SENIOR DIRECTORS DIRECTORS PRESIDENT LAUREN S. CURTIS TIFFANY ALEXANDER MICHAEL T. GLASCOTT Traub Lieberman Straus Tanenbaum Keale LLP Goldberg Segalla, LLP & Shrewsberry LLP Berwyn, PA Buffalo, NY St. Petersburg, FL 610-601-4608 716-844-3413 727-898-8100 [email protected] [email protected] [email protected] SEAN C. GRIFFIN PRESIDENT-ELECT HEIDI G. GOEBEL Dykema Gossett, PLLC ROBERT L. CHRISTIE Goebel Anderson, P.C. Washington, DC Christie Law Group, PLLC Salt Lake City, UT 202-906-8703 Seattle, WA 801-441-9393 [email protected] 206-957-9669 [email protected] [email protected] R. JEFFREY KELSEY MARC H. HARWELL Federal Express Corporation SECRETARY-TREASURER Harwell Law Group PLLC Memphis, TN HOWARD A. MERTEN Chattanooga, TN 901-434-8563 Partridge, Snow & Hahn 423-505-5595 [email protected] Providence, RI [email protected] 401-861-8277 AMY L. MILETICH [email protected] JENNIFER E. JOHNSEN Miletich PC Gallivan, White & Boyd, PA Denver, CO 80202 BOARD CHAIR Greenville, SC 303-825-5500 ELIZABETH F. LORELL 864-271-9580 [email protected] Gordon & Rees LLP [email protected] Florham Park, NJ FRANCISCO RAMOS, JR. 973-549-2506 CRAIG A. MARVINNEY Clarke Silverglate, P.A. [email protected] Walter & Haverfield, LLP Miami, FL Cleveland, OH 305-347-1544 EXECUTIVE DIRECTOR 216-928-2889 [email protected] BERND G. HEINZE [email protected] 610 Freedom Business Center, HEATHER SANDERSON Suite 110 DAVID M. NICHOLAS Sanderson Law King of Prussia, PA 19406 TE Connectivity Corporation Calgary, Alberta 610-992-0022 Middletown, PA 403-837-2508 [email protected] 717-985-2261 [email protected] [email protected] MARISA TRASATTI JOHNSON L. -

FOR IMMEDIATE RELEASE Contact: Jaclynne Madden April 4, 2017 BOMA/Chicago Phone: 312-870-9608 [email protected]

FOR IMMEDIATE RELEASE Contact: Jaclynne Madden April 4, 2017 BOMA/Chicago Phone: 312-870-9608 [email protected] BOMA North Central Region Announces 2017 TOBY Award Winners (CHICAGO, IL — April 4, 2017) The North Central Region of the Building Owners and Managers Association (BOMA) announced that 12 properties have won the regional competition of The Outstanding Building of the Year (TOBY) Award. The North Central Region includes Illinois, Indiana, Michigan, Ohio and Kentucky. This year, 16 properties competed in 12 TOBY categories from BOMA/Chicago, BOMA Columbus, BOMA Indianapolis, BOMA/Metro Detroit and BOMA/Suburban Chicago. In the commercial real estate industry, the TOBY Award is the most prestigious and comprehensive award of its kind, recognizing excellence in office building management and operations in specific categories of building size or type. All regional winners first won on the local level after thorough building inspections and a rigorous written application process. Written applications were then judged on the regional level. Applicants were judged on tenant relations, commitment to environmental sustainability, emergency preparedness, budgeting, work order systems, security standards, staff experience and continuing education opportunities. The regional winners will now proceed to the international competition. International winners will be announced live on June 27 at the TOBY Awards Banquet as part of the BOMA International 2017 Every Building Conference and Expo in Nashville, Tennessee. “Winning the TOBY award not only sets a building apart from others, but it is a true testament to the commitment, hard work and dedication of the property management teams to be the best of the best in all aspects of their building. -

IN the CIRCUIT COURT of COOK COUNTY, COUNTY DEPARTMENT, CHANCERY DIVISION 4)/3 4 0, 6 ) JAMES DARBY and PATRICK BOVA, Et ) ,19.? Al.,� ) 0

IN THE CIRCUIT COURT OF COOK COUNTY, COUNTY DEPARTMENT, CHANCERY DIVISION 4)/3 4 0, 6 ) JAMES DARBY and PATRICK BOVA, et ) ,19.? al., ) 0. Plaintiffs, ) ' ) Case No. 12 CH 19718 . v. ) The Honorable Judge Sophia Hall ) DAVID ORR, in his official capacity as ) Cook County Clerk, ) Defendant. ) TANYA LAZARO and ELIZABETH "LIZ" ) MATOS, et al., ) Plaintiffs, ) ) Case No. 12 CH 19719 v. ) The Honorable Judge Sophia Hall ) DAVID ORR, in his official capacity as ) Cook County Clerk, ) Defendant. ) STATE OF ILLINOIS, ex rel. Lisa ) Madigan, Attorney General of the ) State of Illinois, ) Intervenor, ) ) CHRISTIE WEBB, in her official capacity ) as Tazewell County Clerk, and KERRY ) HIRTZEL, in his official capacity as ) Effingham County Clerk, DANIEL S. ) KUHN, in his official capacity as Putnam ) County Clerk, PATRICIA LYCAN, in her ) official capacity as Crawford County Clerk, ) BRENDA BRITTON, in her official ) capacity as Clay County Clerk, ) Intervenors. ) ) NOTICE OF MOTION FOR PLAINTIFFS' MOTION FOR LEAVE TO FILE BRIEF IN EXCESS OF FIFTEEN PAGES, INSTANTER TO: See attached service list PLEASE TAKE NOTICE that on Aprd 101 t013 , at 10 001, or as soon thereafter as counsel may be heard, I shall appear before the Honorable Sophia Hall, or any Judge sitting in her stead, in the courtroom usually occupied by her, located at Room 2301, Richard J. Daley Center, 50 W. Washington St., Chicago, Illinois 60602, and present Plaintiffs' Motion for Leave to File Brief in Excess of Fifteen Pages, Instanter, a copy of which is attached hereto. 1 Respectfully submitted, Emily Nic rfl, P.C. John A. Knight (Attorney No. -

ACTIVE COOK COUNTY LOBBYISTS and CLIENTS X MEANS INACTIVE CLIENT December 9, 2009

ACTIVE COOK COUNTY LOBBYISTS AND CLIENTS X MEANS INACTIVE CLIENT December 9, 2009 DAVID A. ABEL AT&T ILLINOIS William Blair & Company, LLC 225 West Randolph Street - Suite 27B 222 W. Adams St. Chicago, IL 60606 Chicago, IL 60606 (312) 727-5517 (312) 236-1600 WILLIAM J.P. BANKS 1838 N Neva Ave DEREK ALBERT Chicago, IL 60707 Albert and Associates (773) 450-3378 18920 Stonewater Blvd X G. MEECE & ASSOCIATES Northville TWP, MI 48168 X MONTALBANO HOMES (248) 349-4834 MWH-AMERICAS INC ARAMARK SERVICE MASTER x TOLL BROTHERS LINEBARAGER GOGGAN BLAIR AND SAMPSON CORNELL BARNETT ALLAN R. AMBROSE ComEd The Northern Trust Company /M9 P.S. Friedman 1 Financial Place, 440 LaSalle, Suite 3300 50 South LaSalle St - B-12 Chicago, IL 60605 Chicago, IL 60603 (312) 394-4049 (312) 557-0945 COMED NORTHERN TRUST CORPORATION MYLES D. BERMAN ADRIENNE ARCHIA (See Foley & Lardner LLP) Rice Financial Products Company 321 N. Clark Street, Suite 2800 208 S. LaSalle St. NE, Suite 1338 CHICAGO, IL 60610 Chicago, IL 60604 (312) 832-4722 (312) 855-9230 CHARLES BERNARDINI KYM ARNONE (See Ungaretti & Harris LLP) Barclays Capital Inc. 70 West Madison # 3500 745 Seventh Ave Chicago, IL 60602 New York, NY 10019 (312) 977-4400 (212) 526-6332 Barclays Capital Inc BRIAN A. BERNARDONI Chicago Associaton of Realtors DOUG ARNOT 200 South Michigan Ave - Suite 400 (See Chicago 2016) Chicago, IL 60604 200 E. Randolph # 2016 (312) 214-5528 Chicago, Il 60601 (312) 861-4800 ACTIVE COOK COUNTY LOBBYISTS AND CLIENTS X MEANS INACTIVE CLIENT December 9, 2009 DAVID A. BONOMA WALLACE BRADLEY David A.