Booms and Busts with Dispersed Information

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Twenty-Five Years of Unemployment Insurance in the United States

some of the highlights of the many developments More and more the programs have stressed the in these programs. preventive aspects of their services. The three programs have some things in com- All have consistently struggled to improve the mon. In all of them, the most consistent trend quality and skills of the workers as well as their has been toward broadening the services to meet numbers. Often only the high purposes and the needs of special groups of children. strong will of those administering and carrying All three programs consistently have carried on the services have made it possible to keep serv- the torch for higher standards of care and serv- ices from eroding in quality. ices of better quality. The programs have been responsive to new The three programs have reached out to hard- knowledge, new treatment, and new facilities. to-serve groups--children in isolated areas, chil- They have kept their services in tune with the dren with special problems, children requiring changing pace and circumstances in the lives of specialized services. families and children in the Nation. Twenty-five Years of Unemployment Insurance J in the United States by R. GORDON WAGENET* INTEREST IN UNEMPLOYMENT insurance THE FEDERAL-STATE SYSTEM legislation in the United States first appeared The Social Security Act did not establish a long before the enactment of the Social Security system of unemployment insurance in the United Act, but it took the most severe depression in the States. It provided an inducement to the States Nation’s history and the encouragement of State to enact unemployment insurance laws. -

Large Shocks in US Macroeconomic Time Series

Large shocks in U.S. macroeconomic time series: 1860–1988 Olivier Darné, Amélie Charles To cite this version: Olivier Darné, Amélie Charles. Large shocks in U.S. macroeconomic time series: 1860–1988. 2009. hal-00422502 HAL Id: hal-00422502 https://hal.archives-ouvertes.fr/hal-00422502 Preprint submitted on 7 Oct 2009 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. EA 4272 WorkingPaper Large shocks in U.S. macroeconomic time series: 1860–1988 Document de Travail Olivier DARNE (*) Amélie CHARLES (**) 2009/24 (*) LEMNA, Université de Nantes (**) Audencia Nantes, School of Management Laboratoire d’Economie et de Management Nantes-Atlantique Université de Nantes Chemin de la Censive du Tertre – BP 52231 44322 Nantes cedex 3 – France www.univ-nantes.fr/iemn-iae/recherche Tél. +33 (0)2 40 14 17 19 – Fax +33 (0)2 40 14 17 49 Large shocks in U.S. macroeconomic time series: 1860–1988 Olivier DARNÉ ∗ and Amélie CHARLES † Abstract In this paper we examine the large shocks due to major economic or financial events that affected U.S. macroeconomic time series on the pe- riod 1860–1988, using outlier methodology. -

31St Annual Report of the Bank for International Settlements

BANK FOR INTERNATIONAL SETTLEMENTS THIRTY-FIRST ANNUAL REPORT 1st APRIL 1960 — 31st MARCH 1961 BASLE 12th June 1061 TABLE OF CONTENTS Page Introduction i Part I - Problems of Economic and Financial Policy in 1960-61 . 3 The United States: the recession (p. 5), anti-recession measures (p. 8), the dilemma of monetary policy (p. 11), the new Administration's policy approach (p. 11); Germany: the boom (p. 13), monetary policy (p. 15)', Italy: the rules of the game (p. 17); the Netherlands: multiple restraint (p. 19); Switzerland: capital exports (p. 21); the United Kingdom: longer-term problems (p. 23), balance of payments (p. 24), economic growth (p. 26); France: balanced growth (p. 28); the international payments position (p. 29): the basic imbalance (p. 30), short-term capital flows (p. 31) Part II - Survey of Economic and Monetary Developments .... 33 I. The Formation and Use of the National Product . 33 Industrial production (p. 33); productivity gains (p. 36); structural economic changes in the last decade (p. 37); economic cycles in the last decade (p. 40); sources of demand and available resources (p. 42); saving and investment by sectors (p. 47) II. Money, Credit and Capital Markets 53 Monetary policy and the structure of interest rates: discount rate policy (P- 54) > reserve requirements (p. $6), debt management and open-market operations (p. 57); the control of liquid assets and the flow of bank credit (p. 60); capital-market activity (p. 62); credit developments in individual countries: the United States (p. 64), the United Kingdom (p. 67), France (p. 70), Germany (p. 73), the Netherlands (p. -

Insights from the Federal Reserve's Weekly Balance Sheet, 1942-1975

SAE./No.104/May 2018 Studies in Applied Economics INSIGHTS FROM THE FEDERAL RESERVE'S WEEKLY BALANCE SHEET, 1942-1975 Cecilia Bao and Emma Paine Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise Insights from the Federal Reserve’s Weekly Balance Sheet, 1942 -1975 By Cecilia Bao and Emma Paine Copyright 2017 by Cecilia Bao and Emma Paine. This work may be reproduced or adapted provided that no fee is charged and the original source is properly credited. About the Series The Studies in Applied Economics series is under the general direction of Professor Steve H. Hanke, co-director of the Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise ([email protected]). The authors are mainly students at The Johns Hopkins University in Baltimore. Some performed their work as research assistants at the Institute. About the Authors Cecilia Bao ([email protected]) and Emma Paine ([email protected]) are students at The Johns Hopkins University in Baltimore, Maryland. Cecilia is a sophomore pursuing a degree in Applied Math and Statistics, while Emma is a junior studying Economics. They wrote this paper as undergraduate researchers at the Institute for Applied Economics, Global Health, and the Study of Business Enterprise during Fall 2017. Emma and Cecilia will graduate in May 2019 and May 2020, respectively. Abstract We present digitized data of the Federal Reserve System’s weekly balance sheet from 1942- 1975 for the first time. Following a brief account of the central bank during this period, we analyze the composition and trends of Federal Reserve assets and liabilities, with particular emphasis on how they were affected by significant events during the period. -

Essays in Macroeconomic History and Policy by Jeremie

Essays in Macroeconomic History and Policy by Jeremie Cohen-Setton A dissertation submitted in partial satisfaction of the requirements for the degree of Doctor of Philosophy in Economics in the Graduate Division of the University of California, Berkeley Committee in charge: Professor Barry Eichengreen, Chair Professor Christina Romer Associate Professor Yuriy Gorodnichenko Professor Andrew Rose Summer 2016 Essays in Macroeconomic History and Policy Copyright 2016 by Jeremie Cohen-Setton 1 Abstract Essays in Macroeconomic History and Policy by Jeremie Cohen-Setton Doctor of Philosophy in Economics University of California, Berkeley Professor Barry Eichengreen, Chair The Making of a Monetary Union: Evidence from the U.S. Discount Market 1914-1935 The decentralized structure of the Federal Reserve gave regional Reserve banks a large degree of autonomy in setting discount rates. This created repeated and continued periods of non- uniform discount rates across the 12 Federal Reserve districts. Commercial banks did not take full advantage of these differentials, reflecting the effectiveness of qualitative restrictions on the use of discount window liquidity in limiting the geographical movement of funds. While the choice of regional autonomy over complete financial integration was reasonable given the characteristics of the U.S. monetary union in the interwar period, the Federal Reserve failed to use this autonomy to stabilize regional economic activity relative to the national average. The diagnosis that the costs of decentralization outweighed the gains from regional differentiation motivated reforms that standardized and centralized control of Reserve bank discount policies. Supply-Side Policies in the Depression: Evidence from France The effects of supply-side policies in depressed economies are controversial. -

Erie and Crisis:Region Faces Unique Opportunity to Reimagine Itself

Erie & Crisis: Region Faces Unique Opportunity to Reimagine Itself By Andrew Roth, Judith Lynch, Pat Cuneo, Ben Speggen, Angela Beaumont, and Colleen Dougherty Edited by Ferki Ferati MAY 2020 A Publication of The Jefferson Educational Society 2 FOREWORD pen any newspaper, browse news websites and social platforms, or turn Oon the television to any news channel at any given point during the day and you will find that COVID-19 continues to dominate discussion globally. What you will also find is that information and updates are changing more often than not from minute-to-minute rather than week-to-week – so much so that it makes it almost impossible for leaders to make rational and sustainable decisions in real time. How can decisions be made when we do not know what is on the other side of the mountain? Is COVID-19 beatable, or is it here to stay, like HIV? Will a vaccine take six months, a year, or longer? No one seems to know these answers for certain. When facing these kinds of difficult decisions, we must draw back to not only understand but, as John Quincy Adams said, “to embrace… that who Jefferson President Dr. Ferki Ferati we are is who we were.” That means we need to look at past experiences to inform the present and the uncertain future. This essay, written by members of the Jefferson’s team, including Scholars-in-Residence Drs. Judith Lynch and Andrew Roth, is an attempt to look at COVID-19 through the lens of past experiences and make recommendations for the future. -

Down Market Battle Plan

The Shape of Recovery: What’s Next? Panelists Leon LaBrecque Matt Pullar JD, CPA, CFP®, CFA Vice President, Private Client Chief Growth Officer Services 248.918.5905 216.774.1192 [email protected] [email protected] 2 As an independent financial services firm, our About Sequoia salaried, non-commission professionals have Financial Group access to a variety of solutions and resources and our recommendations are based solely on what works best for you, not us. 3 1. What are we monitoring? 2. What are we hearing from our Financial investment partners? Market Update 3. What are we recommending? 4 COVID-19: U.S. Confirmed Cases and Fatalities S o urce: Johns Hopkins CSSE, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of June 30, 2020. 5 Consumer Sentiment Index S o urce: CONSSENT Index (University of Michigan Consumer Sentiment Index) Copyright 2020 Bloomberg Finance L.P. 17-Jul-2020 6 COVID-19: Fatalities S o urce – New York Times https://static01.nyt.com/images/2020/0 7/20/multimedia/20-MORNING- 7DAYDEATHS/20-MORNING- 7DAYDEATHS-articleLarge.png 7 High-Frequency Economic Activity S o urce: Apple Inc., FlightRadar24, Mortgage Bankers Association (MBA), OpenTable, STR, Transportation Security Administration (TSA), J.P. Morgan Asset Management. *Driving directions and total global flights are 7- day moving averages and are compared to a pre-pandemic baseline. Guide to the Markets – U.S. Data are as of June 30, 2020. 8 S&P 500 Index at Inflection Points S o urce: Compustat, FactSet, Federal Reserve, Standard & Poor’s, J.P. -

Read the Full PDF

Job Name:2222118 Date:15-04-17 PDF Page:2222118pbc.p1.pdf Color: Cyan Magenta Yellow Black THE SWEDISH INVESTMENT RESERVE A Device for Economic Stabilization? By MARTIN SCHNITZER The "new economics" as pursued by the Kennedy and Johnson Administrations reflects the belief that economic stability-full em ployment without inflation-can be achieved through the use of fine-tuning adjustments on the country's fiscal and monetary ma chinery. These adjustments include the 1964 tax cut, the suspension of the investment credit in 1966, and its recent restoration in 1967. The rationale for the use of fine-tuning adjustments, or "push button" fiscal policy, is that the level of aggregate demand can pre sumably be nudged in the direction that is consonant with the desired level of economic activity. Detractors of the "new economics," however, cite several reasons to doubt its effectiveness: 1. Forecasting is still not sufficiently precise and accurate to indicate the most propitious time to use "push button" fiscal policy. 2. Time lags can defeat the purposes of rapid implementation of fiscal and monetary policy. 3. Politics can affect even the most precise and well-planned economic policy. The recent delay in restoring the investment credit is an example. 4. Erratic fiscal policy measures can introduce instability rather than stability into the economy through adverse effects on business and consumer-spending decisions. Sweden has used two interesting devices which are relevant to any analysis of the "new economics." 'One measure, the investment reserve, is well known as a public policy instrument, and is designed to regulate or '~smooth out" investment over the business cycle; the other measure, a direct tax on investment, was used on several occasions during the 1950s. -

An Overview of Financial Crises in Us

ISSN 1822-6515 ISSN 1822-6515 EKONOMIKA IR VADYBA: 2009. 14 ECONOMICS & MANAGEMENT: 2009. 14 AN OVERVIEW OF FINANCIAL CRISES IN U.S. Audrius Dzikevicius1, Mantas Zamzickas2 Vilnius Gediminas Technical University, Lithuania [email protected], [email protected] Abstract In this article, most severe U.S. recessions from the Great depression to Dot–com bubble were revealed and analyzed. The most grounded explanation for these economic downturns comes from Austrian business cycle theory. Firstly, U.S. Federal Reserve Board intervenes to the financial market and cuts interest rates to stimulate borrowing from the banking system. This expansion of credit causes an expansion of the supply of money through the money creation process in a fractional reserve banking system. This artificial process leads to an unsustainable monetary boom and it results in widespread malinvestments. Later, when inflation accelerates and it causes a burst of financial and real estate bubbles, Federal Reserve Board increases interest rates. A credit crunch or recession occurs when credit creation cannot be sustained. A history and main causes of financial crises show that financial booms and severe busts can be avoided if the lessons from the history would be learned and, most-likely, U.S. and other industrialized countries would return to the gold standard and let free market do its job. Keywords: financial crises, recessions, Austrian business cycles theory, malinvestments, gold standard. Introduction Financial crisis is widely known term which is used when financial institutions or investment assets suddenly lose a large part of their value. In the 19th and 20th centuries most of the financial crises and recessions were associated with panic in the banking sector. -

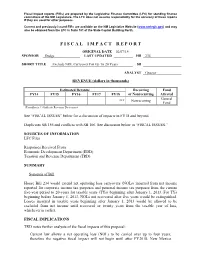

F I S C a L I M P a C T R E P O

Fiscal impact reports (FIRs) are prepared by the Legislative Finance Committee (LFC) for standing finance committees of the NM Legislature. The LFC does not assume responsibility for the accuracy of these reports if they are used for other purposes. Current and previously issued FIRs are available on the NM Legislative Website (www.nmlegis.gov) and may also be obtained from the LFC in Suite 101 of the State Capitol Building North. F I S C A L I M P A C T R E P O R T ORIGINAL DATE 02/07/14 SPONSOR Dodge LAST UPDATED HB 234 SHORT TITLE Exclude NOL Carryover For Up To 20 Years SB ANALYST Graeser REVENUE (dollars in thousands) Estimated Revenue Recurring Fund FY14 FY15 FY16 FY17 FY18 or Nonrecurring Affected General *** Nonrecurring Fund (Parenthesis ( ) Indicate Revenue Decreases) See “FISCAL ISSUES” below for a discussion of impacts in FY18 and beyond. Duplicates SB 156 and conflicts with SB 106. See discussion below in “FISCAL ISSUES.” SOURCES OF INFORMATION LFC Files Responses Received From Economic Development Department (EDD) Taxation and Revenue Department (TRD) SUMMARY Synopsis of Bill House Bill 234 would extend net operating loss carryovers (NOLs) incurred from net income reported for corporate income tax purposes and personal income tax purposes from the current five-year period to 20-years for taxable years (TYs) beginning after January 1, 2013. For TYs beginning before January 1, 2013, NOLs not recovered after five years would be extinguished. Losses incurred in taxable years beginning after January 1, 2013 would be allowed to be excluded from net income until recovered or twenty years from the taxable year of loss, whichever is earlier. -

Research Publications RP-08

penditures, and so approach a balance d system were sharply reduced in calenda r budget with some surplus for debt re- 1955 to negative amounts. The increase duction (see Appendix I) . in the money supply was held to minima l levels through 1956 (about one percent Substantial emphasis on monetary over the year), and both short- and policy, both of a general nature and con - ,long-term interest rates rose sharpl y sideration, at least, of specific control s ( Chart 2) . ( over consumer credit), was also char- acteristie of this period, One major issue of this period con- cerned the causes of the inflation tha t Assorted policies to promote economic was occurring. On the one hand, many , growth included measures to strengthe n argued that with an unemployment rate competition, promote thrift, and im- of 4 percent or more, it was not excessive prove human and natural resources . aggregate demand that was causing in - Such recommendations can be found i n ~flation, but rather the "cost-push" of all the. Economic Reports of :-the Presi- rising wage rates and "administere d dent. prices." It was also argued that the rela- it is evident from Table 2 that in the tively high level of unemployment wa s 1955-57 expansion the total effect o f a reflection of "structural unemploy- ,Federal government finances as reflected ment" unemployment attributable t o in the cash budget was restrictive, an d such things as geographical and occupa- more so than had been expected. During tional immobility in the labor force — ...the early part of the expansion (fisca l so that increased aggregate demand was 1956) the actual surplus far exceede d not the appropriate cure . -

FOMC Meeting Minutes

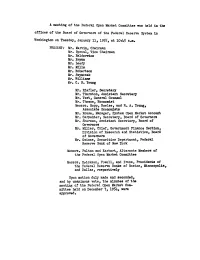

A meeting of the Federal Open Market Committee was held in the offices of the Board of Governors of the Federal Reserve System in Washington on Tuesday, January 11, 1955, at 10:45 a.m. PRESENT: Mr. Martin, Chairman Mr. Sproul, Vice Chairman Mr. Balderston Mr. Bryan Mr. Leedy Mr. Mills Mr. Robertson Mr. Szymczak Mr. Williams Mr. C. S. Young Mr. Riefler, Secretary Mr. Thurston, Assistant Secretary Mr. Vest, General Counsel Mr. Thomas, Economist Messrs. Bopp, Roelse, and R. A. Young, Associate Economists Mr. Rouse, Manager, System Open Market Account Mr. Carpenter, Secretary, Board of Governors Mr. Sherman, Assistant Secretary, Board of Governors Mr. Miller, Chief, Government Finance Section, Division of Research and Statistics, Board of Governors Mr. Gaines, Securities Department, Federal Reserve Bank of New York Messrs. Fulton and Earhart, Alternate Members of the Federal Open Market Committee Messrs. Erickson, Powell, and Irons, Presidents of the Federal Reserve Banks of Boston, Minneapolis, and Dallas, respectively Upon motion duly made and seconded, and by unanimous vote, the minutes of the meeting of the Federal Open Market Com mittee held on December 7, 1954, were approved. 1/11/55 -2- Upon motion duly made and seconded, and by unanimous vote, the actions of the executive committee of the Federal Open Market Committee as set forth in the min utes of the meeting of the executive com mittee held on December 7, 1954, were ap proved, ratified, and confirmed. Before this meeting there had been sent to the members of the Committee a report of open market operations prepared at the Federal Re serve Bank of New York covering the period December 7, 1954, to January 6, 1955, inclusive, and at this meeting there was distributed a supple mentary report covering commitments executed January 7 to January 10, 1955, inclusive.