Reply Studies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The BG News April 20, 1990

Bowling Green State University ScholarWorks@BGSU BG News (Student Newspaper) University Publications 4-20-1990 The BG News April 20, 1990 Bowling Green State University Follow this and additional works at: https://scholarworks.bgsu.edu/bg-news Recommended Citation Bowling Green State University, "The BG News April 20, 1990" (1990). BG News (Student Newspaper). 5076. https://scholarworks.bgsu.edu/bg-news/5076 This work is licensed under a Creative Commons Attribution-Noncommercial-No Derivative Works 4.0 License. This Article is brought to you for free and open access by the University Publications at ScholarWorks@BGSU. It has been accepted for inclusion in BG News (Student Newspaper) by an authorized administrator of ScholarWorks@BGSU. ARTS IN APRIL BG NETTERS VICTORIOUS International and ethnic Falcons prevail 6-3 artworks presented Friday Mag ^ over tough Wooster club Sports The Nation *s Best College Newspaper Friday Weather Vol.72 Issue 116 April 20,1990 Bowling Green, Ohio High 67* The BG News Low 49° BRIEFLY Hostage release postponed Erosion In Damascus. Syrian Foreign Minis- by Rodeina Kenaan "The United States ter Farouk al-Sharaa said his govern- Associated Press writer ment has "been exerting a great deal of of ozone CAMPUS does not knuckle under influence" to secure the hostage BEIRUT, Lebanon — Pro-Iranian to demands." release by Sunday. He would not elab- Beta rescheduled: The 27th kidnappers said Thursday they post- -George Bush, orate. layers annual Beta 500 race has been poned indefinitely the release of an President Bush said the United rescheduled for this Sunday at noon. American hostage because the United CJ.S. -

Cablevision Systems Corporation Reports Third Quarter 2008 Results

FOR IMMEDIATE RELEASE CABLEVISION SYSTEMS CORPORATION REPORTS THIRD QUARTER 2008 RESULTS Bethpage, N.Y., November 6, 2008 - Cablevision Systems Corporation (NYSE:CVC) today reported financial results for the third quarter ended September 30, 2008. Third quarter consolidated net revenue grew 15.4% to $1.745 billion compared to the prior year period, reflecting solid revenue growth in Telecommunications Services, Rainbow and Madison Square Garden as well as the addition of Newsday and Sundance in the 2008 results. Consolidated adjusted operating cash flow (“AOCF”) 1 increased 16.3% to $575.0 million and consolidated operating income grew 39.2% to $281.3 million, both compared to the prior year period. Operating highlights for third quarter 2008 include: • Cable Television net revenue growth of 9.8% and AOCF growth of 13.6% as compared to the third quarter of 2007 • Quarterly addition of nearly 96,000 Revenue Generating Units (“RGU”) • Average Monthly Revenue per Basic Video Customer (“RPS”) of $133.11 in the third quarter of 2008 • Optimum Lightpath net revenue growth of 13.4% and AOCF growth of 37.2% as compared to the third quarter of 2007 Cablevision President and CEO James L. Dolan commented: "For the third quarter, Cablevision reported double-digit increases in revenue and AOCF, despite the current economic conditions. This growth was fueled in part by the ongoing strength of our core businesses as the company's cable operations, Madison Square Garden and Rainbow all generated solid revenue growth for the quarter. Cablevision continued to grow its industry-leading penetration rates for high-speed data and voice, while our digital video service reached an unprecedented penetration rate of 90 percent. -

Wing Commander II, Your Goal Is to Defeat the Kilrathi Enemy

Wing Commander TM II USER MANUAL PLAY HUNDREDS OF THE GREATEST GAMES EVER MADE, VISIT WWW.GAMETAP.COM AND GET YOUR FREE TRIAL NOW! GameTap is pleased to oer an online library of original game manuals. We have made these manuals available to create a more complete gaming experience -- and because some of them are pretty entertaining. Be aware that the representations, warranties, and guarantees (including replacement options) made in these manuals are no longer valid, and that GameTap and the original publisher are not responsible for honoring them. Control information for a PC title will, in most cases, accurately reect the game’s controls within GameTap. Please note that game controller instructions for console games won’t be correct. Feel free to ignore any installation instructions -- GameTap handles all the complex stu for you. Finally, please do not call the phone numbers that occasionally appear in the manuals. We're not sure anyone will pick up. If you do have questions about games within the GameTap service, please contact Customer Support at gametap.com. wc2_1 Page 1 of 2 C O N T E N T S PLAY GUIDE .....................................................2 Alternate Camera Views ......................12 The Story So Far….......................................2 Improved Target Starting the Game.........................................2 Tracking System .............................12 Transferring Characters ............................3 Jumping Out.......................................12 Creating a New Character ........................3 -

Television Broadcasters'adoption of Digital

TELEVISION BROADCASTERS’ ADOPTION OF DIGITAL MULTICAST AND ANCILLARY SERVICES: AN ANALYSIS OF THE PRIMARY CORE, SUPPORTING, AND ENVIRONMENTAL DRIVERS By TODD ANDREW HOLMES A THESIS PRESENTED TO THE GRADUATE SCHOOL OF THE UNIVERSITY OF FLORIDA IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS IN MASS COMMUNICATION UNIVERSITY OF FLORIDA 2008 1 © 2008 Todd Andrew Holmes 2 To all who have inspired my intellectual curiosity and academic pursuits, and to all who have supported me in reaching this milestone 3 ACKNOWLEDGMENTS First and foremost, I would like to thank my chair, Dr. Ostroff, for the enormous amount of time and guidance he gave to me in helping me to complete this research study. His support and direction were absolutely critical in the successful completion of this paper. I also would like to thank the members of my committee, Dr. Chan-Olmsted and Dr. Brown, for their thoughts and ideas concerning my research topic. Second, I would like to thank the nine television executives who took time out of their busy schedules to meet with me and who very openly and willingly shared with me their thoughts on the research topic. Their help was absolutely vital to the completion of this study. Third, I would like to thank my parents who continued to keep me moving along on the thesis through their inquiries and encouragement. Their own academic achievements have continued to inspire me throughout this process. Lastly, special thanks go to all my friends, the Gator Guzzlers and many others, who heard me talk about this thesis for months and with whom I had to skip out on a lot of activities. -

Cablevision Systems Corporation Reports Fourth Quarter and Full Year 2008 Results

FOR IMMEDIATE RELEASE CABLEVISION SYSTEMS CORPORATION REPORTS FOURTH QUARTER AND FULL YEAR 2008 RESULTS Bethpage, N.Y., February 26, 2009 - Cablevision Systems Corporation (NYSE:CVC) today reported financial results for the fourth quarter and full year ended December 31, 2008. Fourth quarter consolidated net revenues grew 11.4% to $2.052 billion compared to the prior year period, reflecting solid revenue growth in Telecommunications Services, Rainbow and the addition of Newsday and Sundance in the 2008 results. Consolidated adjusted operating cash flow (“AOCF”) 1 was essentially flat (down 0.9% to $604.7 million) compared to the prior year period, and consolidated operating income (which includes impairment charges of $402.4 million at Newsday and $41.0 million at VOOM HD) decreased to an operating loss of $136.5 million. For full year 2008, consolidated net revenues increased 11.5% to $7.230 billion, reflecting revenue growth in Cable Television, Rainbow and Madison Square Garden as well as the addition of Newsday and Sundance in the 2008 results. Consolidated AOCF grew 10.1% to $2.298 billion and consolidated operating income decreased 24.3% to $689.7 million for full year 2008. (Full year 2008 operating income was unfavorably impacted by the impairment charges noted above.) Operating highlights for the fourth quarter and full year 2008 include: • Cable Television net revenue growth of 7.4% and 9.1% and AOCF growth of 4.1% and 10.7% for the fourth quarter and full year, respectively • Revenue Generating Units (“RGU”) additions of 100,500 and 653,400 for the fourth quarter and full year, respectively • Average Monthly Revenue per Basic Video Customer (“RPS”) of $134.85 in the fourth quarter of 2008 • Full year Consolidated Free Cash Flow from Continuing Operations1 of $507.5 million Cablevision President and CEO James L. -

Abstract a Case Study of Cross-Ownership Waivers

ABSTRACT A CASE STUDY OF CROSS-OWNERSHIP WAIVERS: FRAMING NEWSPAPER COVERAGE OF RUPERT MURDOCH’S REQUESTS TO KEEP THE NEW YORK POST by Rachel L. Seeman Media ownership is an important regulatory issue that is enforced by the Federal Communications Commission. The FCC, Congress, court and public interest groups share varying viewpoints concerning what the ownership limits should be and whether companies should be granted a waiver to be excused from the rules. News Corporation is one media firm that has a history of seeking these waivers, particularly for the New York Post and television stations in same community. This study conducted a qualitative framing analysis of news articles from the New York Times and the Wall Street Journal to determine if the viewpoints expressed by the editorial boards were reflected in reports on News Corp.’s attempt to receive cross-ownership waivers. The analysis uncovered ten frames the newspapers used to assist in reporting the events and found that 80% of these frames did parallel the positions the paper’s editorial boards took concerning ownership waivers. A CASE STUDY OF CROSS-OWNERSHIP WAIVERS: FRAMING NEWSPAPER COVERAGE OF RUPERT MURDOCH’S REQUESTS TO KEEP THE NEW YORK POST A Thesis Submitted to the Faculty of Miami University in partial fulfillment of the requirements for the degree of Master of Arts Department of Communications by Rachel Leianne Seeman Miami University Oxford, OH 2009 Advisor: __________________________________ (Dr. Bruce Drushel) Reader: __________________________________ (Dr. Howard -

Beatles Rock Band and the Commodification of Nostalgia

Loading… The Journal of the Canadian Game Studies Association Vol 6(10): 71-90 http://loading.gamestudies.ca When I’m Sixty-Four: Beatles Rock Band and the Commodification of Nostalgia Jaigris Hodson York/Ryerson Universities [email protected] Abstract In 2009, only a few months after the game’s release, the popular trade magazine Advertising Age declared Beatles Rock Band (2009) one of America’s hottest brands ("America's hottest brands", 2009). This is quite a feat for a video game, and begs that we consider the reasons for the game’s success as well a the potential social consequences of this game as well as similar popular games. There are two major elements at work in the creation of Beatles Rock Band as a successful brand, and this paper conducts qualitative, participant-observation research in order to provide an analysis of the game that identifies both of them. First, the paper explores the Beatles as a brand that continues to provide emotional and spiritual value for consumers, and how the feelings associated with this brand have developed intertextually since the band first gained international popularity in 1962. Second, this paper will show how Beatles Rock Band can be viewed as a documentary game, and how, in portraying history, it also rewrites it in order to capitalize on a romanticized ideal of 1960s culture. This paper will show the ways that Beatles Rock Band draws on previous commercial texts associated with the Beatles brand to create a hyperreal fiction based on historic people and events. These texts help to connect people in fan communities that serve the commercial purposes of the game marketers. -

Testimony of Gene Kimmelman, Senior Director for Advocacy and Public Policy, Consumers Union

Testimony of Gene Kimmelman, Senior Director for Advocacy and Public Policy, Consumers Union Before the Antitrust, Competition Policy and Consumer Rights Subcommittee of the Senate Judiciary Committee On News Corp./DirecTV Merger June 18, 2003 Washington Office 1666 Connecticut Avenue, N.W. Suite 310 • Washington, D.C. 20009-1039 (202) 462-6262 • fax (202) 265-9548 • http://www.consumersunion.org SUMMARY Consumers Union1 welcomes this opportunity to testify before the Senate Antitrust, Competition Policy and Consumer Rights Subcommittee regarding the proposed merger between the News Corporation (“News Corp.”) and Hughes Electronics Corporation’s satellite television unit DIRECTV (“DirecTV”). Given the current concentration in the media marketplace, as well as the further concentration that will result from the Federal Communications Commission’s (FCC’s) recent relaxation of media ownership rules, we believe that the proposed merger between network and cable giant News Corp. and DirecTV, the largest direct broadcast satellite (DBS) service provider, will further increase prices for consumers and decrease the diversity of voices in the media marketplace. Today, consumers are not receiving the fruits that a competitive cable and satellite marketplace should deliver, and consumers are likely to suffer further harm if antitrust officials do not impose substantial conditions on the proposed deal between News Corp. and DirecTV. Since passage of the 1996 Telecommunications Act, cable rates have risen over 50%,2 and FCC data show that satellite competition is not creating downward pressure on cable rates. Despite the promise for more diversity from new technologies such as the Internet and satellite, a mere five media companies control nearly the same prime time audience shares as the Big Three networks did 40 years ago.3 Unfortunately, the market for news production and distribution is becoming more concentrated. -

Illegal File Sharing

ILLEGAL FILE SHARING The sharing of copyright materials such as MUSIC or MOVIES either through P2P (peer-to-peer) file sharing or other means WITHOUT the permission of the copyright owner is ILLEGAL and can have very serious legal repercussions. Those found GUILTY of violating copyrights in this way have been fined ENORMOUS sums of money. Accordingly, the unauthorized distribution of copyrighted materials is PROHIBITED at Bellarmine University. The list of sites below is provided by Educause and some of the sites listed provide some or all content at no charge; they are funded by advertising or represent artists who want their material distributed for free, or for other reasons. Remember that just because content is free doesn't mean it's illegal. On the other hand, you may find websites offering to sell content which are not on the list below. Just because content is not free doesn't mean it's legal. Legal Alternatives for Downloading • ABC.com TV Shows • [adult swim] Video • Amazon MP3 Downloads • Amazon Instant Video • AOL Music • ARTISTdirect Network • AudioCandy • Audio Lunchbox • BearShare • Best Buy • BET Music • BET Shows • Blackberry World • Blip.fm • Blockbuster on Demand • Bravo TV • Buy.com • Cartoon Network Video • Zap2it • Catsmusic • CBS Video • CD Baby • Christian MP Free • CinemaNow • Clicker (formerly Modern Feed) • Comedy Central Video • Crackle • Criterion Online • The CW Video • Dimple Records • DirecTV Watch Online • Disney Videos • Dish Online • Download Fundraiser • DramaFever • The Electric Fetus • eMusic.com -

Federal Register/Vol. 85, No. 103/Thursday, May 28, 2020

32256 Federal Register / Vol. 85, No. 103 / Thursday, May 28, 2020 / Proposed Rules FEDERAL COMMUNICATIONS closes-headquarters-open-window-and- presentation of data or arguments COMMISSION changes-hand-delivery-policy. already reflected in the presenter’s 7. During the time the Commission’s written comments, memoranda, or other 47 CFR Part 1 building is closed to the general public filings in the proceeding, the presenter [MD Docket Nos. 19–105; MD Docket Nos. and until further notice, if more than may provide citations to such data or 20–105; FCC 20–64; FRS 16780] one docket or rulemaking number arguments in his or her prior comments, appears in the caption of a proceeding, memoranda, or other filings (specifying Assessment and Collection of paper filers need not submit two the relevant page and/or paragraph Regulatory Fees for Fiscal Year 2020. additional copies for each additional numbers where such data or arguments docket or rulemaking number; an can be found) in lieu of summarizing AGENCY: Federal Communications original and one copy are sufficient. them in the memorandum. Documents Commission. For detailed instructions for shown or given to Commission staff ACTION: Notice of proposed rulemaking. submitting comments and additional during ex parte meetings are deemed to be written ex parte presentations and SUMMARY: In this document, the Federal information on the rulemaking process, must be filed consistent with section Communications Commission see the SUPPLEMENTARY INFORMATION 1.1206(b) of the Commission’s rules. In (Commission) seeks comment on several section of this document. proceedings governed by section 1.49(f) proposals that will impact FY 2020 FOR FURTHER INFORMATION CONTACT: of the Commission’s rules or for which regulatory fees. -

* (Asterisk) in Google, 6 with Group Syntax, 215 in Name

CH27_228-236_Index.qxd 7/14/04 2:48 PM Page 229 INDEXINDEX * (asterisk) Applied Power, Principle of, brand names, 86–88 in Google, 6 102–106 Brooklyn Public Library, 119 with group syntax, 215 area codes, 169–170. See also browsers, 22–40 in name searches, 75 phone number searches bookmarklets with, 34–36 as wildcard, 6 art. See images gadgets for, 36–39 + (plus sign), 4–5. See also askanexpert.com, 93 iCab, 24 Boolean modifiers Ask Jeeves, 17–18 Internet Explorer, 23 – (minus sign), 4–5. See also for Kids, 210 listing, 25 Boolean modifiers toolbar, 32–33 Lynx, 24 | (pipe symbol), 5 associations Mozilla, 23 experts in, 91–93 Netscape, 23 finding, 92–93 Opera, 24 A audio, 154–163 plugins for, 27–29 finding, 159–160 Safari, 24–25 About.com, genealogy at, formats, 154–156 search toolbars with, 29–33 179–180 fun sites for, 162–163 security with, 25–26 address searches playing, 156–158 selecting, 25 driving directions and, 173 search engines/directories specialty toolbars with, 33 names in, 76–77 for, 160–162 speed optimization with, reverse lookups, 168–169 software sources, 158 26–27 229 for things/sites, 78 AU format, 155 turning off auto-password zip code helpers and, 172 reminders in, 26 AIFF format, 155 turning off Java in, 26 ALA Great Web Sites, 210 B turning off pop-ups in, 26 All Experts, 93–94 turning off scripting in, 25 AllPlaces, 134 Babelfish, 227 browser sniffer, 36–37 AlltheWeb, 160 BBB database, 195, 198 Bureau of Consumer Protection, almanacs, 186 Better Business Bureau, 195, 198 195 AltaVista, 148 biographical information, -

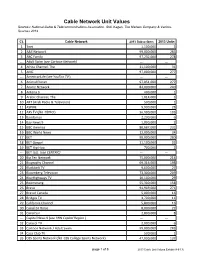

Cable Network Unit Values Sources: National Cable & Telecommunications Association, SNL Kagan, the Nielsen Company & Various Sources 2013

Cable Network Unit Values Sources: National Cable & Telecommunications Association, SNL Kagan, The Nielsen Company & Various Sources 2013 Ct. Cable Network 2013 Subscribers 2013 Units 1 3net 1,100,000 3 2 A&E Network 99,000,000 283 3 ABC Family 97,232,000 278 --- Adult Swim (see Cartoon Network) --- --- 4 Africa Channel, The 11,100,000 31 5 AMC 97,000,000 277 --- AmericanLife (see YouToo TV ) --- --- 6 Animal Planet 97,051,000 277 7 Anime Network 84,000,000 240 8 Antena 3 400,000 1 9 Arabic Channel, The 1,014,000 3 10 ART (Arab Radio & Television) 500,000 1 11 ASPIRE 9,900,000 28 12 AXS TV (fka HDNet) 36,900,000 105 13 Bandamax 2,200,000 6 14 Bay News 9 1,000,000 2 15 BBC America 80,687,000 231 16 BBC World News 12,000,000 34 17 BET 98,000,000 280 18 BET Gospel 11,100,000 32 19 BET Hip Hop 700,000 2 --- BET Jazz (see CENTRIC) --- --- 20 Big Ten Network 75,000,000 214 21 Biography Channel 69,316,000 198 22 Blackbelt TV 9,600,000 27 23 Bloomberg Television 73,300,000 209 24 BlueHighways TV 10,100,000 29 25 Boomerang 55,300,000 158 26 Bravo 94,969,000 271 27 Bravo! Canada 5,800,000 16 28 Bridges TV 3,700,000 11 29 California Channel 5,800,000 16 30 Canal 24 Horas 8,000,000 22 31 Canal Sur 2,800,000 8 --- Capital News 9 (see YNN Capital Region ) --- --- 32 Caracol TV 2,000,000 6 33 Cartoon Network / Adult Swim 99,000,000 283 34 Casa Club TV 500,000 1 35 CBS Sports Network (fka CBS College Sports Network) 47,900,000 137 page 1 of 8 2013 Cable Unit Values Exhibit (4-9-13) Ct.