A Social Divide in the City

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

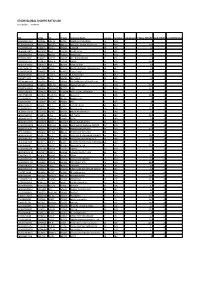

STOXX GLOBAL SHARPE RATIO 100 Selection List

STOXX GLOBAL SHARPE RATIO 100 Last Updated: 20200918 ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) Rank (FINAL)Rank (PREVIOUS) AU000000MIN4 B17ZL56 MIN.AX B17ZL5 MINERAL RESOURCES AU AUD Y 3 1 AU000000FMG4 6086253 FMG.AX 608625 Fortescue Metals Group Ltd. AU AUD Y 18.7 2 CH0267291224 BVSS671 SRCG.S CH501Z SUNRISE CH CHF Y 3.4 3 GB00B06QFB75 B06QFB7 IGG.L B06QFB IG GRP HLDG GB GBP Y 3.3 4 AU000000JBH7 6702623 JBH.AX 670262 JB Hi-Fi Ltd. AU AUD Y 3.6 5 SE0000862997 7240371 BILL.ST 724037 BILLERUDKORSNAS SE SEK Y 2.6 6 US00287Y1091 B92SR70 ABBV.N US20SG ABBVIE US USD Y 118.2 7 GB00B18V8630 B18V863 PNN.L 082699 PENNON GRP GB GBP Y 4.7 8 LU1072616219 BMTRW10 BMEB.L GB40FA B&M EUROPEAN VALUE RETAIL GB GBP Y 4.5 9 AU0000030678 BYWR0T5 COL.AX AU80Q2 Coles Group AU AUD Y 14.6 10 GB00B02J6398 B02J639 ADML.L 926294 ADMIRAL GRP GB GBP Y 7 11 JE00B5TT1872 B5TT187 CEY.L GB60EB CENTAMIN GB GBP Y 2.7 12 PTEDP0AM0009 4103596 EDP.LS 524918 EDP ENERGIAS DE PORTUGAL PT EUR Y 12 13 AU000000WES1 6948836 WES.AX 694883 Wesfarmers Ltd. AU AUD Y 33.3 14 DE000ENAG999 4942904 EONGn.DE 492752 E.ON DE EUR Y 22.2 15 US5007541064 BYRY499 KHC.OQ US20MA KRAFT HEINZ COMPANY US USD Y 9.5 16 US6937181088 2665861 PCAR.OQ PCAR Paccar Inc. US USD Y 24.8 17 JP3768600003 6414401 1808.T 641440 Haseko Corp. JP JPY Y 3.4 18 IT0003128367 7144569 ENEI.MI 579802 ENEL IT EUR Y 59 19 GB00B1FH8J72 B1FH8J7 SVT.L 079851 SEVERN TRENT GB GBP Y 6.3 20 AU000000RIO1 6220103 RIO.AX 622010 Rio Tinto Ltd. -

Phoenix Group Holdings

PROSPECTUS DATED 25 SEPTEMBER 2020 Phoenix Group Holdings plc (incorporated with limited liability in England and Wales with registered number 11606773) £5,000,000,000 Euro Medium Term Note Programme Under the Euro Medium Term Note Programme described in this Prospectus (the “Programme”) Phoenix Group Holdings plc (“Phoenix” or “PGH” or the “Issuer”), subject to compliance with all relevant laws, regulations and directives, may from time to time issue notes (the “Notes”). The Notes may be issued (i) as dated unsubordinated notes (“Senior Notes”), (ii) as dated subordinated notes with terms capable of qualifying as Tier 3 Capital (as defined in “Terms and Conditions of the Tier 3 Notes”) (“Tier 3 Notes”), (iii) as dated subordinated notes with terms capable of qualifying as Tier 2 Capital (as defined in “Terms and Conditions of the Tier 2 Notes”) (“Dated Tier 2 Notes”) or as undated subordinated notes with terms capable of qualifying as Tier 2 Capital (as defined in “Terms and Conditions of the Tier 2 Notes”) (“Undated Tier 2 Notes” and, together with the Dated Tier 2 Notes, the “Tier 2 Notes”). The Tier 2 Notes and the Tier 3 Notes are referred to collectively in this Prospectus as the “Subordinated Notes”. The aggregate nominal amount of Notes outstanding will not at any time exceed £5,000,000,000 (or the equivalent in other currencies). Payments of interest and principal under the Subordinated Notes may be subject to optional or mandatory deferral in accordance with the terms of the relevant Series (as defined herein) of Subordinated Notes. This Prospectus has been approved by the United Kingdom Financial Conduct Authority (the “FCA”), as competent authority under Regulation (EU) 2017/1129 (the “Prospectus Regulation”) as a base prospectus (the “Prospectus”) for the purposes of the Prospectus Regulation. -

Introduction to the Sage Group Plc

Introduction to The Sage Group plc December 2013 An introduction to The Sage Group plc 1 Our vision Our vision is to be recognised as the most valuable supporter of small and medium sized companies by creating greater freedom for them to succeed. An introduction to The Sage Group plc 2 What we do We provide small and medium sized Businesses come in all shapes and sizes organisations with a range of easy-to-use and while every one of our customers is unique they have common technology business management software and needs - for simple, secure and smart services - from accounting and payroll, to solutions that reduce complexity and risk. enterprise resource planning, customer When they have problems that need relationship management and payments. resolving, they want to speak to a real person – someone they can trust. So we make sure we’re always there to listen and help. Our customers receive continuous advice and support through our global network of local experts to help them solve their business problems, giving them the confidence to achieve their business ambitions. An introduction to The Sage Group plc 3 Key facts about our organisation Market Finances Customers ‒ Global company with over ‒ Revenue of £1,376.1m** ‒ Provide advice to 12,700 employees* million for FY2013* customers through 1.9 ‒ Over 6 million customers ‒ Organic revenue growth of million support contracts* worldwide* 4% for 2013 (2012: 2%)* ‒ Manage around 36,000 ‒ One of the market ‒ EBITA £375.8m* customer calls each day* leaders in the UK, North ‒ Market capitalisation of ‒ Work with 22,600 reseller America, Europe, South approximately £4 billion* partners and more than Africa, Asia and Brazil 40,000* accountants ‒ More than 40 acquisitions since 1991 worldwide An introduction to The Sage Group plc *Data for financial year ending September 2013 4 ** Statutory revenue How we started An introduction to The Sage Group plc 5 How we work Our business is guided by our five principles which shape everything we do and how we do it. -

Robert W. Stirling

Robert W. Stirling Partner, London Insurance; Financial Institutions Robert Stirling focuses on insurance and asset management matters, as well as the regula- tory issues involved in transactional work and the insurance sector generally. He advises on public and private acquisitions, private equity investments, portfolio and other risk transfers, share offerings and asset disposals. Mr. Stirling also has handled numerous representations for clients such as Phoenix Group, Mitsui Sumitomo Insurance Co., Endurance Specialty Holdings, Prudential plc, Marsh and TDR Capital. Mr. Stirling is recognised as a leading individual in non-contentious insurance in Best Lawyers in the UK, IFLR1000, The Legal 500 UK and Chambers UK, which cites his “sophisticated transactional insurance practice” and quotes clients saying: “He has gravitas, he’s pragmatic and he can think his way out of difficult problems. He’s a standout.” Prior to joining Skadden in 2014, Mr. Stirling was head of the non-contentious insurance T: 44.20.7519.7051 practice at a Magic Circle firm. F: 44.20.7072.7051 [email protected] Mr. Stirling also has advised financial institutions on transactional and regulatory matters, including Barclays Capital, BNP Paribas and Credit Suisse. His recent representations include advising: Education University of Cambridge - Phoenix Group Holdings in its: The College of Law, Guildford • £2.9 billion acquisition of Standard Life Assurance Limited from Standard Life Aber- deen plc; and Bar Admissions • acquisition of Abbey Life from Deutsche Bank AG for £935 million, in respect of the Solicitor of the Supreme Court transaction documentation and the connected rights issue; of England and Wales - The Travelers Companies, Inc. -

Monthly Performance Review Enhanced Income Fund W Income Shares 31 August 2021

MPR.en.xx.20210831.GB00B87HPZ94.pdf For Investment Professionals Only FIDELITY INVESTMENT FUNDS MONTHLY PERFORMANCE REVIEW ENHANCED INCOME FUND W INCOME SHARES 31 AUGUST 2021 Portfolio manager: Michael Clark, David Jehan, Rupert Gifford Performance over month in GBP (%) Performance for 12 month periods in GBP (%) Fund 2.0 Market index 2.7 FTSE All Share Index Market index is for comparative purposes only. Source of fund performance is Fidelity. Basis: bid-bid with income reinvested, in GBP, net of fees. Other share classes may be available. Please refer to the prospectus for more details. Fund Index Market Environment UK equities continued to advance, recording a seventh straight monthly gain in August. Sentiment remained buoyant, propelled by a spate of merger and acquisition (M&A) activity, alongside expectations for continued earnings strength. The Bank of England kept its monetary policy unchanged, but warned of a more pronounced period of above-target inflation in the near term. Meanwhile, the pace of economic activity remains solid in the UK despite a modest deceleration over the month. While the flash PMI reading remained above the 50 mark that suggest growth, staffing shortages and supply bottlenecks kept a lid on activity levels. Authorities finally lifted the last of the domestic COVID-19 restrictions during the month. Almost all sectors posted positive returns, with technology, real estate, industrials and consumer discretionary the largest gainers. Conversely, materials and consumer staples lagged the market. Fund Performance The fund delivered 2.0%, while the index was up by 2.7% in August. UK equities continued to advance, and the fund lagged due to its defensive bias. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

FT UK 500 2011 A-Z Company UK Rank 2011 3I Group 94 888 Holdings 485 Abcam 250 Aberdeen Asset Management 109 Admiral Group 72 A

FT UK 500 2011 A-Z UK rank Company 2011 3I Group 94 888 Holdings 485 Abcam 250 Aberdeen Asset Management 109 Admiral Group 72 Advanced Medical Solutions 488 Aegis Group 127 Afren 138 African Barrick Gold 118 African Minerals 131 Aggreko 69 Albemarle & Bond 460 Allied Gold 306 Amec 75 Amerisur Resources 426 Amlin 124 Anglo American 11 Anglo Pacific Group 327 Anglo-Eastern Plantations 370 Anite 445 Antofagasta 29 Aquarius Platinum 136 Archipelago Resources 346 Arm Holdings 42 Ashley (Laura) 476 Ashmore 112 Ashtead Group 206 Asian Citrus 263 Asos 171 Associated British Foods 41 Assura 449 Astrazeneca 12 Atkins (WS) 240 Aurelian Oil & Gas 334 Autonomy 76 Avanti Communications 324 Aveva 192 Avis Europe 326 Aviva 31 Avocet Mining 287 Axis-Shield 469 AZ Electronic Materials 199 Babcock International 117 Bae Systems 35 Bahamas Petroleum 397 Balfour Beatty 111 Barclays 16 Barr (AG) 289 Barratt Developments 197 BBA Aviation 209 Beazley 257 Bellway 216 Bellzone Mining 292 Berendsen 222 Berkeley 160 Betfair Group 202 BG Group 8 BHP Billiton 7 Big Yellow Group 308 Blinkx 344 Bodycote 259 Booker 213 Boot (Henry) 478 Borders & Southern Petroleum 378 Bovis Homes Group 268 Bowleven 220 BP 4 Brammer 351 Brewin Dolphin 319 British American Tobacco 9 British Land 61 British Sky Broadcasting 27 Britvic 210 Brown (N) 237 BT Group 28 BTG 235 Bunzl 107 Burberry 59 Bwin Party Digital Entertainment 223 Cable & Wireless Communications 181 Cable & Wireless Worldwide 158 Cairn Energy 49 Caledon Resources 380 Camellia 389 Cape 270 Capita 66 Capital & Counties Properties -

The Sage Group Plc an Introduction

The Sage Group plc An introduction February 2016 What we do Sage is the market leader for integrated accounting, payroll and payment systems, supporting the ambition of the world’s entrepreneurs. Sage began as a small business in the UK 35 years ago and over 13000 colleagues now support millions of entrepreneurs across 23 countries as they power the global economy. We reinvent and simplify business accounting through brilliant technology, working with a thriving community of entrepreneurs, business owners, tradespeople, accountants, partners and developers. And as a FTSE 100 business, we are active in supporting our local communities and invest in making a real difference through the philanthropy of the Sage Foundation. The Sage Group plc - an introduction 2 Key facts about our organization Market Finances Customers Global company with over Revenue of 13,000 £1.4bn 3m employees • One of the market leaders • Organic revenue growth of • Supporting customers, in the UK, North America, 6% for 2015 (2014: 5%)* managing over 30,000 calls Europe, South Africa, Asia • Organic operating profit each day and Brazil £380m* • Ecosystem including 100,000 • Local presence in 23 • Market capitalization of c. accountants globally countries globally £6bn The Sage Group plc - an introduction * Data for financial year ending 30 September 2015 3 How we started 1981 2005 2015 Entered the Polish market Sage founded in Newcastle Launch of upon Tyne by David Goldman, 1989 Sage Live Paul Muller and Graham Wylie 1999 2008 Listed on the London Stock and Sage Became -

Monthly Professional Factsheet Uk Opportunities Fund a Income Shares 31 August 2021

pro.en.xx.20210831.GB00BGV1T511.pdf UK Opportunities Fund A Income Shares For Investment Professionals Only FIDELITY INVESTMENT FUNDS 2 MONTHLY PROFESSIONAL FACTSHEET UK OPPORTUNITIES FUND A INCOME SHARES 31 AUGUST 2021 Strategy Fund Facts Leigh Himsworth identifies specific areas of the market that he believes are capable of Launch date: 01.09.11** delivering consistent growth. Within these themes, he employs disciplined cash flow Portfolio manager: Leigh Himsworth analysis to seek out companies capable of delivering earnings growth without Appointed to fund: 01.09.11 materially increasing their risk profile. On this basis, Leigh builds a high conviction Years at Fidelity: 7 portfolio of quality growth companies. Each holding in the portfolio has a weighting that Fund size: £602m allows it to make a meaningful contribution to performance. Risk management takes Number of positions in fund*: 55 into account factors that could impact a number of companies in the portfolio. Fund reference currency: UK Sterling (GBP) Fund domicile: United Kingdom Fund legal structure: OEIC Management company: FIL Investment Services (UK) Limited Capital guarantee: No Portfolio Turnover Cost (PTC): 0.48% Portfolio Turnover Rate (PTR): 182.08% *A definition of positions can be found on page 3 of this factsheet in the section titled “How data is calculated and presented.” Objectives & Investment Policy Share Class Facts • The fund aims to increase the value of your investment over a period of 5 years or Other share classes may be available. Please refer to the prospectus for more details. more. • The fund will invest at least 70% in shares (and their related securities) of a blend of Launch date: 15.05.19 different sized UK companies. -

Wolters Kluwer Governance Roadshow

Wolters Kluwer Governance Roadshow Selection & Remuneration Committee of the Supervisory Board of Wolters Kluwer November 2020 Governance Roadshow, November 2020 1 Forward-looking statements This presentation contains forward-looking statements. These statements may be identified by words such as "expect", "should", "could", "shall", and similar expressions. Wolters Kluwer cautions that such forward-looking statements are qualified by certain risks and uncertainties that could cause actual results and events to differ materially from what is contemplated by the forward-looking statements. Factors which could cause actual results to differ from these forward-looking statements may include, without limitation, general economic conditions, conditions in the markets in which Wolters Kluwer is engaged, behavior of customers, suppliers and competitors, technological developments, the implementation and execution of new ICT systems or outsourcing, legal, tax, and regulatory rules affecting Wolters Kluwer's businesses, as well as risks related to mergers, acquisitions and divestments. In addition, financial risks, such as currency movements, interest rate fluctuations, liquidity and credit risks could influence future results. The foregoing list of factors should not be construed as exhaustive. Wolters Kluwer disclaims any intention or obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Growth rates are cited in constant currencies unless otherwise noted. Governance Roadshow, November 2020 2 Agenda Wolters Kluwer NV - Selection & Remuneration Committee Current remuneration policy and how it links to strategy Remuneration consultation Proposed changes Proposed ESG measures in STIP Current policy versus proposed changes Next steps Appendix Governance Roadshow, November 2020 3 Selection & Remuneration Committee The Selection & Remuneration Committee is responsible for Executive Board succession planning and remuneration policy Frans Cremers Jeanette Horan Ann Ziegler . -

Factset-Top Ten-0521.Xlsm

Pax International Sustainable Economy Fund USD 7/31/2021 Port. Ending Market Value Portfolio Weight ASML Holding NV 34,391,879.94 4.3 Roche Holding Ltd 28,162,840.25 3.5 Novo Nordisk A/S Class B 17,719,993.74 2.2 SAP SE 17,154,858.23 2.1 AstraZeneca PLC 15,759,939.73 2.0 Unilever PLC 13,234,315.16 1.7 Commonwealth Bank of Australia 13,046,820.57 1.6 L'Oreal SA 10,415,009.32 1.3 Schneider Electric SE 10,269,506.68 1.3 GlaxoSmithKline plc 9,942,271.59 1.2 Allianz SE 9,890,811.85 1.2 Hong Kong Exchanges & Clearing Ltd. 9,477,680.83 1.2 Lonza Group AG 9,369,993.95 1.2 RELX PLC 9,269,729.12 1.2 BNP Paribas SA Class A 8,824,299.39 1.1 Takeda Pharmaceutical Co. Ltd. 8,557,780.88 1.1 Air Liquide SA 8,445,618.28 1.1 KDDI Corporation 7,560,223.63 0.9 Recruit Holdings Co., Ltd. 7,424,282.72 0.9 HOYA CORPORATION 7,295,471.27 0.9 ABB Ltd. 7,293,350.84 0.9 BASF SE 7,257,816.71 0.9 Tokyo Electron Ltd. 7,049,583.59 0.9 Munich Reinsurance Company 7,019,776.96 0.9 ASSA ABLOY AB Class B 6,982,707.69 0.9 Vestas Wind Systems A/S 6,965,518.08 0.9 Merck KGaA 6,868,081.50 0.9 Iberdrola SA 6,581,084.07 0.8 Compagnie Generale des Etablissements Michelin SCA 6,555,056.14 0.8 Straumann Holding AG 6,480,282.66 0.8 Atlas Copco AB Class B 6,194,910.19 0.8 Deutsche Boerse AG 6,186,305.10 0.8 UPM-Kymmene Oyj 5,956,283.07 0.7 Deutsche Post AG 5,851,177.11 0.7 Enel SpA 5,808,234.13 0.7 AXA SA 5,790,969.55 0.7 Nintendo Co., Ltd. -

Smurfit Kappa Annual Report 2009

SMURFIT KAPPA GROUP PLC ANNUAL REPORT 2009 ANNUAL REPORT 2009 Raw materials The raw material for paper-based packaging comes from renewable sources and the end product is recycled many times making all forms of SKG’s paper-based packaging the most environmentally friendly available. SKG recovers almost 5 million tonnes of recycled paper each year in Europe where it is the European leader in recycling and 0.8 million tonnes in Latin America where it also holds a leading position. Almost all of this is sourced through our own recovery systems. Modern mills The Group produces well over 6 million tonnes of paper, primarily in the containerboard, solidboard and sackpaper grades, at its 38 mills across the world. The Group is the leading producer of containerboard in Europe and one of the largest in Latin America using wood and recovered paper to manufacture kraftliner and recycled paper grades respectively. Our containerboard production is integrated into our corrugated operations. Operating excellence The product range of our containerboard mills covers the complete spectrum of paper and board including features such as weight, colour and printability. On the packaging side, our extensive presence in 21 European and 9 Latin American countries allows us to offer customers a “one stop shop” for all their packaging needs and a differentiated quality of service. With a strong focus on innovative packaging solutions, our operations are supported by outstanding research and development facilities with a view to enhancing the customer offering. Design expertise/Innobook In SKG we have created “Innobook”, a library with over 3,000 proven design solutions, which is available to the more than 500 designers within our worldwide group and to both our sales and customer support people.