Peter X. Huang

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Entrepreneurs from Technology-Based Universities: Evidence from MIT David Hsu University of Pennsylvania

University of Pennsylvania ScholarlyCommons Management Papers Wharton Faculty Research 6-2007 Entrepreneurs From Technology-Based Universities: Evidence From MIT David Hsu University of Pennsylvania Follow this and additional works at: http://repository.upenn.edu/mgmt_papers Part of the Business Administration, Management, and Operations Commons, and the Entrepreneurial and Small Business Operations Commons Recommended Citation Hsu, D. (2007). Entrepreneurs From Technology-Based Universities: Evidence From MIT. Research Policy, 36 (5), 768-788. http://dx.doi.org/10.1016/j.respol.2007.03.001 This paper is posted at ScholarlyCommons. http://repository.upenn.edu/mgmt_papers/146 For more information, please contact [email protected]. Entrepreneurs From Technology-Based Universities: Evidence From MIT Abstract This paper analyzes major patterns and trends in entrepreneurship among technology-based university alumni since the 1930s by asking two related research questions: (1) Who enters entrepreneurship, and has this changed over time? (2) How does the rate of entrepreneurship vary with changes in the entrepreneurial business environment? We describe findings based on data from two linked datasets joining Massachusetts Institute of Technology (MIT) alumni and founder information. New company formation rates by MIT alumni have grown dramatically over seven decades, and the median age of first time entrepreneurs has gradually declined from about age 40 (1950s) to about age 30 (1990s). Women alumnae lag their male counterparts in the rate at which they become entrepreneurs, and alumni who are not U.S. citizens enter entrepreneurship at different (usually higher) rates relative to their American classmates. New venture foundings over time are correlated with measures of the changing external entrepreneurial and business environment, suggesting that future research in this domain may wish to more carefully examine such factors. -

Post Event Report

presents 9th Asian Investment Summit Building better portfolios 21-22 May 2014, Ritz-Carlton, Hong Kong Post Event Report 310 delegates representing 190 companies across 18 countries www.AsianInvestmentSummit.com Thank You to our sponsors & partners AIWEEK Marquee Sponsors Co-Sponsors Associate Sponsors Workshop Sponsor Supporting Organisations alternative assets. intelligent data. Tech Handset Provider Education Partner Analytics Partner ® Media Partners Offical Broadcast Partner 1 www.AsianInvestmentSummit.com Delegate Breakdown 310 delegates representing 190 companies across 18 countries Breakdown by Organisation Institutional Investors 46% Haymarket Financial Media delegate attendee data is Asset Managemer 19% independently verified by the BPA Consultant 8% Fund Distributor / Private Wealth Management 5% Media & Publishing 4% Commercial Bank 4% Index / Trading Platform Provider 3% Association 2% Other 9% Breakdown of Institutional Investors Insurance 31% Endowment / Foundation 27% Corporation 13% Pension Fund 13% Family Office 8% Breakdown by Country Sovereign Wealth Fund 6% PE Funds of Funds 1% Mulitlateral Finance Hong Kong 82% Institution 1% ASEAN 10% North Asia 5% Australia 1% Europe 1% North America 1% Breakdown by Job Function Investment 34% Finance / Treasury 20% Marketing and Investor Relations 19% Other 11% CEO / Managing Director 7% Fund Selection / Distribution 7% Strategist / Economist 2% 2 www.AsianInvestmentSummit.com Participating Companies Haymarket Financial Media delegate attendee data is independently verified by the BPA 310 institutonal investors, asset managers, corporates, bankers and advisors attended the Forum. Attending companies included: ACE Life Insurance CFA Institute Board of Governors ACMI China Automation Group Limited Ageas China BOCOM Insurance Co., Ltd. Ageas Hong Kong China Construction Bank Head Office Ageas Insurance Company (Asia) Limited China Life Insurance AIA Chinese YMCA of Hong Kong AIA Group CIC AIA International Limited CIC International (HK) AIA Pension and Trustee Co. -

Allianz Se Allianz Finance Ii B.V. Allianz

2nd Supplement pursuant to Art. 16(1) of Directive 2003/71/EC, as amended (the "Prospectus Directive") and Art. 13 (1) of the Luxembourg Act (the "Luxembourg Act") relating to prospectuses for securities (loi relative aux prospectus pour valeurs mobilières) dated 12 August 2016 (the "Supplement") to the Base Prospectus dated 2 May 2016, as supplemented by the 1st Supplement dated 24 May 2016 (the "Prospectus") with respect to ALLIANZ SE (incorporated as a European Company (Societas Europaea – SE) in Munich, Germany) ALLIANZ FINANCE II B.V. (incorporated with limited liability in Amsterdam, The Netherlands) ALLIANZ FINANCE III B.V. (incorporated with limited liability in Amsterdam, The Netherlands) € 25,000,000,000 Debt Issuance Programme guaranteed by ALLIANZ SE This Supplement has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") of the Grand Duchy of Luxembourg in its capacity as competent authority (the "Competent Authority") under the Luxembourg Act for the purposes of the Prospectus Directive. The Issuer may request the CSSF in its capacity as competent authority under the Luxemburg Act to provide competent authorities in host Member States within the European Economic Area with a certificate of approval attesting that the Supplement has been drawn up in accordance with the Luxembourg Act which implements the Prospectus Directive into Luxembourg law ("Notification"). Right to withdraw In accordance with Article 13 paragraph 2 of the Luxembourg Act, investors who have already agreed to purchase or subscribe for the securities before the Supplement is published have the right, exercisable within two working days after the publication of this Supplement, to withdraw their acceptances, provided that the new factor arose before the final closing of the offer to the public and the delivery of the securities. -

Entrepreneurs from Technology-Based Universities: Evidence from MIT David H

Research Policy 36 (2007) 768–788 Entrepreneurs from technology-based universities: Evidence from MIT David H. Hsu a,∗, Edward B. Roberts b, Charles E. Eesley b a Wharton School, University of Pennsylvania, 2000 Steinberg Hall-Dietrich Hall, Philadelphia, PA 19104, United States b MIT Sloan School of Management, 50 Memorial Drive, Cambridge, MA 02142, United States Received 13 March 2006; received in revised form 4 December 2006; accepted 6 March 2007 Available online 19 April 2007 Abstract This paper analyzes major patterns and trends in entrepreneurship among technology-based university alumni since the 1930s by asking two related research questions: (1) Who enters entrepreneurship, and has this changed over time? (2) How does the rate of entrepreneurship vary with changes in the entrepreneurial business environment? We describe findings based on data from two linked datasets joining Massachusetts Institute of Technology (MIT) alumni and founder information. New company formation rates by MIT alumni have grown dramatically over seven decades, and the median age of first time entrepreneurs has gradually declined from about age 40 (1950s) to about age 30 (1990s). Women alumnae lag their male counterparts in the rate at which they become entrepreneurs, and alumni who are not U.S. citizens enter entrepreneurship at different (usually higher) rates relative to their American classmates. New venture foundings over time are correlated with measures of the changing external entrepreneurial and business environment, suggesting that future research in this domain may wish to more carefully examine such factors. © 2007 Elsevier B.V. All rights reserved. Keywords: Entrepreneurship; University alumni 1. Introduction records from the Massachusetts Institute of Technol- ogy (MIT), thereby introducing several facts about the This paper analyzes major patterns and trends entrepreneurial activity of MIT alumni. -

Alibaba: Entrepreneurial Growth and Global Expansion in B2B/B2C Markets

JIntEntrep DOI 10.1007/s10843-017-0207-2 Alibaba: Entrepreneurial growth and global expansion in B2B/B2C markets Syed Tariq Anwar 1 # Springer Science+Business Media, LLC 2017 Abstract The purpose of this case-based research is to analyze and discuss Alibaba Group (hereafter Alibaba) and its entrepreneurial growth and global expansion in B2B/ B2C markets. The paper uses company and industry-specific data and surveys to analyze a fast growing Chinese B2B/B2C firm and its internationalization and expan- sion in global markets. Findings of the work reveal that in a short time, Alibaba has become a major entrepreneurial icon and global player and continues to grow world- wide because of its well-planned business initiatives and B2B/B2C-based business models. The paper also provides implications in the area of international entrepreneur- ship and its related areas. International entrepreneurs need to learn from Alibaba’sfast growing business model and dynamic growth because of its competitive platforms and Web-based strategies which helped the company to target small and medium-sized enterprises (SMEs) in global markets. Within the areas of international entrepreneurship and international business, the paper also provides discussion which deals with the changing e-commerce industry and its future growth and developments. El objetivo de esta investigación basada en casos de negocios es analizar y discutir el Grupo Alibaba (de aquí en adelante Alibaba) y su crecimiento empresarial y la expansión global en mercados de B2B/B2C. El ensayo utiliza estadísticas y encuestas específicas a la compañía e industria para analizar una empresa china B2B/B2C y su internalización y expansión en los mercados globales. -

Corporate Governance of Company Groups: International and Latin American Experience

Corporate Governance of Company Groups: International and Latin American Experience Preliminary version for comment. Hosted by : Please send written comments to [email protected] by 5 December, 2014 Latin American Roundtable Task Force on Corporate Governance of Company Groups 17 November, 2014 Hotel Hilton Bogotá, CARRERA 7 NO. 72-41, BOGOTA, 00000, COLOMBIA http://www.oecd.org/daf/ca/latinamericanroundtableoncorporategovernance.htm With funding support of: TABLE OF CONTENTS International and Latin American Overview ............................................................................. 3 1. Introduction............................................................................................................................ 3 2. Economic Rationale for Corporate Groups and the Role of Corporate Governance ............. 4 3. International Work on Corporate Governance of Groups ...................................................... 8 4. Economic Relevance of Company Groups in LatAm .......................................................... 12 5. What is an Economic Group in LatAm? .............................................................................. 12 6. Structure of the Regulatory and Supervisory Framework ................................................... 13 7. Protection of Minority Shareholder Rights .......................................................................... 14 8. Economic Groups and Conflicts of Interest ......................................................................... 15 9. Multinational -

Evaluation of Government-Sponsored R&D Consortia in Japan

Chapter 12 EVALUATION OF GOVERNMENT-SPONSORED R&D CONSORTIA IN JAPAN by Mariko Sakakibara 1 Anderson Graduate School of Management, University of California, Los Angeles Introduction Co-operative R&D has been widely celebrated as a means of promoting private R&D, and some see it as a major tool for enhancing industry competitiveness. Co-operative R&D is defined as an agreement among a group of firms to share the costs and results of an R&D project prior to the execution of that project. Co-operative R&D can be executed in many forms, including R&D contracts, R&D consortia and research joint ventures.2 In this analysis, these forms are collectively referred to as R&D consortia or co-operative R&D projects, interchangeably. Japan is regarded as a forerunner in the practice of co-operative R&D. The most celebrated example is the VLSI (Very Large Scale Integrated circuit) project, designed to help Japan catch up in semiconductor technology. The project, conducted between 1975 to 1985 with a budget of 130 billion yen (US$591 million) of which 22 per cent was financed by the government, developed state-of-the-art semiconductor manufacturing technology. All of the major Japanese semiconductor producers participated in this project, and Japanese semiconductor companies gained world leadership after the project. It is widely believed that this success story is only one of many. The perceived success of the VLSI project has motivated other countries to emulate “Japanese- style” collaboration. The 1984 US National Co-operative Research Act was enacted to relax antitrust regulations in order to allow the formation of research joint ventures. -

Risky Expertise in Chinese Financialisation Haigui Returnee Migrants in the Shanghai Financial Market

Risky Expertise in Chinese Financialisation Haigui Returnee Migrants in the Shanghai Financial Market. A thesis submitted in fulfillment of the requirements for the award for the degree Doctorate of Philosophy From Western Sydney University Giulia Dal Maso Institute for Culture and Society Western Sydney University 2016 Statement of Authentication The work presented in this thesis is, to the best of my knowledge and belief, original except as acknowledged in the text. I hereby declare that I have not submitted this material, either in full or in part, for a degree at this or any other institution. Sections of chapter 5 have been previsouly published in Dal Maso, Giulia. “The Financialisation Rush: Responding to Precarious Labor and Social Security by Investing in the Chinese Stock Market.” South Atlantic Quarterly 114, no. 1: 47-64. ............................................................................... (Signature) Acknowledgements I would like to thank my supervisors Professor Brett Neilson and Professor Ned Rossiter for their extraordinary intellectual support, encouragement and incredible patience. They have been invaluable interlocutors and the best supervisors I could hope for. My gratitude also goes to Professor Sandro Mezzadra for his intellectual generosity, guidance and for having encouraged me many times. It is thanks to him that my Chinese adventure started. Particular thanks go to Giorgio Casacchia. His support has been essential both for the time of my research fieldwork and for sustenance when writing. He has not -

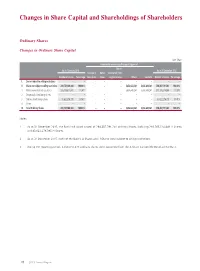

Changes in Share Capital and Shareholdings of Shareholders

Changes in Share Capital and Shareholdings of Shareholders Ordinary Shares Changes in Ordinary Share Capital Unit: Share Increase/decrease during the reporting period Shares As at 1 January 2015 As at 31 December 2015 Issuance of Bonus transferred from Number of shares Percentage new shares shares surplus reserve Others Sub-total Number of shares Percentage I. Shares subject to selling restrictions – – – – – – – – – II. Shares not subject to selling restrictions 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% 1. RMB-denominated ordinary shares 205,108,871,605 71.04% – – – 5,656,643,241 5,656,643,241 210,765,514,846 71.59% 2. Domestically listed foreign shares – – – – – – – – – 3. Overseas listed foreign shares 83,622,276,395 28.96% – – – – – 83,622,276,395 28.41% 4. Others – – – – – – – – – III. Total Ordinary Shares 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% Notes: 1 As at 31 December 2015, the Bank had issued a total of 294,387,791,241 ordinary shares, including 210,765,514,846 A Shares and 83,622,276,395 H Shares. 2 As at 31 December 2015, none of the Bank’s A Shares and H Shares were subject to selling restrictions. 3 During the reporting period, 5,656,643,241 ordinary shares were converted from the A-Share Convertible Bonds of the Bank. 79 2015 Annual Report Changes in Share Capital and Shareholdings of Shareholders Number of Ordinary Shareholders and Shareholdings Number of ordinary shareholders as at 31 December 2015: 963,786 (including 761,073 A-Share Holders and 202,713 H-Share Holders) Number of ordinary shareholders as at the end of the last month before the disclosure of this report: 992,136 (including 789,535 A-Share Holders and 202,601 H-Share Holders) Top ten ordinary shareholders as at 31 December 2015: Unit: Share Number of Changes shares held as Percentage Number of Number of during at the end of of total shares subject shares Type of the reporting the reporting ordinary to selling pledged ordinary No. -

Entrepreneurs from Technology-Based Universities: an Empirical First Look

PRELIMINARY Not for copying, distribution or quotation Entrepreneurs from Technology-Based Universities: An Empirical First Look by David H. Hsu*, Edward B. Roberts** and Charles E. Eesley*** Draft Date: September 2005 Abstract This paper provides an initial analysis of major patterns and trends in entrepreneurship among technology-based university alumni since the 1930s. We describe findings from two linked datasets joining MIT alumni with MIT founder information. The rate of forming new companies by MIT alumni has grown dramatically over seven decades. Women alumni have in more recent decades become entrepreneurs at a faster growth rate than men, but still constitute only 10% of new entrepreneurs. Alumni who are not U.S. citizens also are entering entrepreneurship at a faster pace than their American classmates, but still constitute only 15% of current entrants. The median age of first time entrepreneurs has gradually declined from about age 40 to about age 30. Our results also suggest that rather than examining stable individual traits, future research in this domain may wish to examine business and strategic environment factors. *Wharton School, University of Pennsylvania, 2000 Steinberg-Dietrich Hall, Philadelphia PA 19104. [email protected]; **MIT Sloan School of Management, 50 Memorial Drive, Cambridge MA 02142. [email protected]; *** MIT Sloan School of Management, 50 Memorial Drive, Cambridge MA 02142. [email protected] 1 PRELIMINARY 1. Introduction This paper provides an initial analysis of major patterns and trends in entrepreneurship among technology-based university alumni since the 1930s. The national innovative systems literature has stressed the role of universities in generating commercially important technical knowledge (Nelson, 1996). -

Recent Developments in the Public-Enterprise Sector of Korea

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Governance, Regulation, and Privatization in the Asia-Pacific Region, NBER East Asia Seminar on Economics, Volume 12 Volume Author/Editor: Takatoshi Ito and Anne O. Krueger, editors Volume Publisher: University of Chicago Press Volume ISBN: 0-226-38679-1 Volume URL: http://www.nber.org/books/ito_04-1 Conference Date: June 28-30, 2001 Publication Date: January 2004 Title: Recent Developments in the Public-Enterprise Sector of Korea Author: Il Chong Nam URL: http://www.nber.org/chapters/c10186 4 Recent Developments in the Public-Enterprise Sector of Korea Il Chong Nam 4.1 Introduction The government has always been the dominant figure in the corporate landscape of Korea. This is not surprising, considering that Korea has a relatively short history of capitalism and that the government played a de- cisive role in the fast industrialization process that began in the 1960s. An important aspect of the economic development strategy of the successive administrations was the creation of large firms in modern industries that realize economies of scale and scope. Many large commercial Korean firms were established by the chaebol system, which crucially depended on the government’s intervention in the financial market. Following the heavy and chemical industry drive of the mid-1970s, the automobile, shipbuild- ing, electronics, chemical, and oil refinery industries, as well as a host of others (including construction), were erected in this manner.1 The government’s involvement has been more direct in the remaining in- dustries that require large amounts of capital to start and maintain the business. -

Charles Zhang

In a little over 35 years China’s economy has been transformed Week in China from an inefficient backwater to the second largest in the world. If you want to understand how that happened, you need to understand the people who helped reshape the Chinese business landscape. china’s tycoons China’s Tycoons is a book about highly successful Chinese profiles of entrepreneurs. In 150 easy-to- digest profiles, we tell their stories: where they came from, how they started, the big break that earned them their first millions, and why they came to dominate their industries and make billions. These are tales of entrepreneurship, risk-taking and hard work that differ greatly from anything you’ll top business have read before. 150 leaders fourth Edition Week in China “THIS IS STILL THE ASIAN CENTURY AND CHINA IS STILL THE KEY PLAYER.” Peter Wong – Deputy Chairman and Chief Executive, Asia-Pacific, HSBC Does your bank really understand China Growth? With over 150 years of on-the-ground experience, HSBC has the depth of knowledge and expertise to help your business realise the opportunity. Tap into China’s potential at www.hsbc.com/rmb Issued by HSBC Holdings plc. Cyan 611469_6006571 HSBC 280.00 x 170.00 mm Magenta Yellow HSBC RMB Press Ads 280.00 x 170.00 mm Black xpath_unresolved Tom Fryer 16/06/2016 18:41 [email protected] ${Market} ${Revision Number} 0 Title Page.qxp_Layout 1 13/9/16 6:36 pm Page 1 china’s tycoons profiles of 150top business leaders fourth Edition Week in China 0 Welcome Note.FIN.qxp_Layout 1 13/9/16 3:10 pm Page 2 Week in China China’s Tycoons Foreword By Stuart Gulliver, Group Chief Executive, HSBC Holdings alking around the streets of Chengdu on a balmy evening in the mid-1980s, it quickly became apparent that the people of this city had an energy and drive Wthat jarred with the West’s perception of work and life in China.