H1 FY13 Earnings Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rayman Legends Pc Crack Only

Rayman Legends Pc Crack Only 1 / 5 Rayman Legends Pc Crack Only 2 / 5 3 / 5 Rayman Legends. Watch anime similar to kissanime, ... West Elm Photography. My own crack at the whole "Naruto is banished and comes back an emperor" fic. RG MECHANICS REPACK – TORRENT – FREE DOWNLOAD – CRACKED Rayman Legends is a platform video game. Rayman Legends Crack is developed ... The only things you'll need are a Uplay account and the Uplay client, and ... were ... Rayman legends crack latest full game download for pc.. ... protección .... No Offline, No Hack, No Crack, It is Legit and Multiplayer Online Game!!! ... Rayman Legends Uplay PC Online Version [Worth RM2xx] ... [Steam] Horizon Zero Dawn Complete Edition Steam PC Game [Offline Mode Only].. ( www. | + - Download ): http://l.gg/5H {FILE Protected RAR} Télécharger COMPLETE A SURVEY TO UNLOCK ... 0 or lower, we can completely crack the Switch by Xecuter SX Pro and SX OS to launch the ... 2)Remote PC browser 3)USB now a bit more stable. ... The demo is the full version, with these restrictions: You can only deploy and run your ... 96GB Rayman Legends Definitive Edition [01005FF002E2A000] + (v131072 UPD).. With Uplay PC, your game will remain up to date and you will be prompted to update your game automatically. Offline users will need to switch Uplay to Online .... Download rayman legends pc crack only-reloaded. When I download the torrent files with "all the games" only like 1/4 of them show up. ... Browse our vast selection of GameCube products. exe (crack) to the installation ... GameCube/GCN ISO Also Playable on PC with Dolphin Emulator. -

14 Apple Arcade Games to Play on Launch Day from Strategy to Action to Puzzle Games, Here’S Where You Should Head First

APPLE MOBILE GAMING 11 14 Apple Arcade games to play on launch day From strategy to action to puzzle games, here’s where you should head first By Russ Frushtick @RussFrushtick Sep 19, 2019, 9:40am EDT Simogo Games Today’s launch of Apple Arcade might be overwhelming to some players. Subscribers who drop $4.99 a month get unlimited access to a large swath of games, and scrolling through the list can feel a bit like trying to find something good to watch on Netflix. The initial launch line-up includes over 50 games, but we’ve gone ahead and narrowed them down to 14 titles you’d do well to check out first. WHAT THE GOLF? Triband/The Label While there are plenty of thoughtful, story-driven games in the Apple Arcade collection, What the Golf? goes another way. What starts as a simple miniature golf game quickly evolves into a bizarre blend of physics-based chaos. One level might have you sliding an office chair around the course while another has you knocking full-sized buildings into the pin. The pick-up-and-play nature makes it an easy recommendation for your first dive into Apple Arcade. ASSEMBLE WITH CARE It makes sense that Apple would work with usTwo on an Apple Arcade release title. After all, the developer is known as one of the most successful mobile game makers ever, thanks to Monument Valley and its sequel. usTwo’s latest title, Assemble with Care, taps into humans’ love of taking things apart and putting them back together. -

Nintendo Co., Ltd

Nintendo Co., Ltd. Financial Results Briefing for Fiscal Year Ended March 2013 (Briefing Date: 4/25/2013) Supplementary Information [Note] Forecasts announced by Nintendo Co., Ltd. herein are prepared based on management's assumptions with information available at this time and therefore involve known and unknown risks and uncertainties. Please note such risks and uncertainties may cause the actual results to be materially different from the forecasts (earnings forecast, dividend forecast and other forecasts). Nintendo Co., Ltd. Consolidated Statements of Income Transition million yen FY3/2009 FY3/2010 FY3/2011 FY3/2012 FY3/2013 Net sales 1,838,622 1,434,365 1,014,345 647,652 635,422 Cost of sales 1,044,981 859,131 626,379 493,997 495,068 Gross profit 793,641 575,234 387,965 153,654 140,354 (Gross profit ratio) (43.2%) (40.1%) (38.2%) (23.7%) (22.1%) Selling, general and administrative expenses 238,378 218,666 216,889 190,975 176,764 Operating income 555,263 356,567 171,076 -37,320 -36,410 (Operating income ratio) (30.2%) (24.9%) (16.9%) (-5.8%) (-5.7%) Non-operating income 32,159 11,082 8,602 9,825 48,485 (of which foreign exchange gains) ( - ) ( - ) ( - ) ( - ) (39,506) Non-operating expenses 138,727 3,325 51,577 33,368 1,592 (of which foreign exchange losses) (133,908) (204) (49,429) (27,768) ( - ) Ordinary income 448,695 364,324 128,101 -60,863 10,482 (Ordinary income ratio) (24.4%) (25.4%) (12.6%) (-9.4%) (1.6%) Extraordinary income 339 5,399 186 84 2,957 Extraordinary loss 902 2,282 353 98 3,243 Income before income taxes and minority interests 448,132 367,442 127,934 -60,877 10,197 Income taxes 169,134 138,896 50,262 -17,659 3,029 Income before minority interests - - 77,671 -43,217 7,168 Minority interests in income -91 -89 50 -13 68 Net income 279,089 228,635 77,621 -43,204 7,099 (Net income ratio) (15.2%) (15.9%) (7.7%) (-6.7%) (1.1%) - 1 - Nintendo Co., Ltd. -

UPC Platform Publisher Title Price Available 730865001347

UPC Platform Publisher Title Price Available 730865001347 PlayStation 3 Atlus 3D Dot Game Heroes PS3 $16.00 52 722674110402 PlayStation 3 Namco Bandai Ace Combat: Assault Horizon PS3 $21.00 2 Other 853490002678 PlayStation 3 Air Conflicts: Secret Wars PS3 $14.00 37 Publishers 014633098587 PlayStation 3 Electronic Arts Alice: Madness Returns PS3 $16.50 60 Aliens Colonial Marines 010086690682 PlayStation 3 Sega $47.50 100+ (Portuguese) PS3 Aliens Colonial Marines (Spanish) 010086690675 PlayStation 3 Sega $47.50 100+ PS3 Aliens Colonial Marines Collector's 010086690637 PlayStation 3 Sega $76.00 9 Edition PS3 010086690170 PlayStation 3 Sega Aliens Colonial Marines PS3 $50.00 92 010086690194 PlayStation 3 Sega Alpha Protocol PS3 $14.00 14 047875843479 PlayStation 3 Activision Amazing Spider-Man PS3 $39.00 100+ 010086690545 PlayStation 3 Sega Anarchy Reigns PS3 $24.00 100+ 722674110525 PlayStation 3 Namco Bandai Armored Core V PS3 $23.00 100+ 014633157147 PlayStation 3 Electronic Arts Army of Two: The 40th Day PS3 $16.00 61 008888345343 PlayStation 3 Ubisoft Assassin's Creed II PS3 $15.00 100+ Assassin's Creed III Limited Edition 008888397717 PlayStation 3 Ubisoft $116.00 4 PS3 008888347231 PlayStation 3 Ubisoft Assassin's Creed III PS3 $47.50 100+ 008888343394 PlayStation 3 Ubisoft Assassin's Creed PS3 $14.00 100+ 008888346258 PlayStation 3 Ubisoft Assassin's Creed: Brotherhood PS3 $16.00 100+ 008888356844 PlayStation 3 Ubisoft Assassin's Creed: Revelations PS3 $22.50 100+ 013388340446 PlayStation 3 Capcom Asura's Wrath PS3 $16.00 55 008888345435 -

Hunting and Killing Animals in Open World Video Games Erik Van Ooijen Eludamos

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Eludamos. Journal for Computer Game Culture Vol. 9, No. 1 (2018) http://www.eludamos.org On the Brink of Virtual Extinction: Hunting and Killing Animals in Open World Video Games Erik van Ooijen Eludamos. Journal for Computer Game Culture. 2018; 9 (1), pp. 33-45 On the Brink of Virtual Extinction: Hunting and Killing Animals in Open World Video Games ERIK VAN OOIJEN The present article focuses on the ways in which games represent certain aspects of the systemic nature of violence. It seeks to shift focus from the “outrageous” representations of violence directed at human individuals that often tend to dominate debates on game violence, to rather study the, much less visible, “everyday” violence directed at animals as it is manifested by the hunting mechanics of open world games. Taking a rhetorical approach to the underlying mechanics of violence, it focuses less on shocking depictions as such than on the implicit ideological functions of procedural gameplay. The article circles around four main areas of investigation: how games represent the relationship between hunting animals and crafting animal goods; construct distinctions between human and non-human animals; separate species into juridical and ethical categories; and deal with the digital nature of representations of wildlife in games, where animals may always respawn anew, in order to present rhetorical arguments on the connection between hunting and extinction. Game Studies and Animal Violence Studies on violence against animals in games are surprisingly scarce (Sawers & Demetrious, 2010). In gaming discourse in general, accounts may be found of individual players’ reactions to shocking depictions of animal violence. -

Policing the Sandbox in Grand Theft Auto Online

Policing the Sandbox in Grand Theft Auto Online Matthew Thomas Payne and Michael Fleisch I. Lines in the Sandbox Rockstar Games’ Grand Theft Auto V (2013) broke a number of records following its September 17, 2013, release: it was the best-selling video game in a 24-hour period; its trailer was viewed more times than any other action- adventure game; and – perhaps most impressively – it eclipsed the $1 billion mark in three days, making it the fastest selling entertainment product ever.1 Yet a good deal of the excitement for this latest installment in Rockstar’s long-running and critically acclaimed parodic crime franchise was for an element that was absent during its initial launch. The debut of its greatly anticipated multiplayer mode, GTA Online (GTAO), on October 1st was marred by a series of glitches that required a few weeks and a few patches to remedy, a situation Rockstar tried to ameliorate by gifting all of its users $500k in virtual cash (aka GTA$). Once the mode was functional, it allowed users to play together in and around the vast, fictional city of Los Santos, San Andreas (think Los Angeles and southern California). Estimated at roughly Media Fields Journal no. 8 (2014) 2 Policing the Sandbox 100 square miles, GTA V is the largest sandbox-style world Rockstar has ever developed.2 In GTAO’s virtual playground, players compete in structured multiplayer contests and have the option to rob convenience stores, get in shootouts with cops, harass one another, or explore the urban and rural terrain, waterways, and skies. -

Comparative Life Cycle Impact Assessment of Digital and Physical Distribution of Video Games in the United States

Comparative Life Cycle Impact Assessment of Digital and Physical Distribution of Video Games in the United States The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Buonocore, Cathryn E. 2016. Comparative Life Cycle Impact Assessment of Digital and Physical Distribution of Video Games in the United States. Master's thesis, Harvard Extension School. Citable link http://nrs.harvard.edu/urn-3:HUL.InstRepos:33797406 Terms of Use This article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Other Posted Material, as set forth at http:// nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of- use#LAA Comparative Life Cycle Impact Assessment of Digital and Physical Distribution of Video Games in the United States Cathryn E. Buonocore A Thesis in the field of Sustainability for the Degree of Master of Liberal Arts in Extension Studies Harvard University November 2016 Copyright 2016 Cathryn E. Buonocor Abstract This study examines and compares the environmental footprint of video game distribution on last generation consoles, current generation consoles and personal computers (PC). Two different methods of delivery are compared on each platform: traditional retail on optical discs and digital downloads in the U.S. Downloading content has been growing and is used to distribute movies, music, books and video games. This technology may change the environmental footprint of entertainment media. Previous studies on books, music, movies and television shows found that digital methods of distribution reduced emissions. However, prior research on video games, looking only at previous generation consoles, found the opposite conclusion. -

Rayman and Rabbids Family Pack

wygenerowano 25/09/2021 08:12 RAYMAN AND RABBIDS FAMILY PACK cena 109 zł dostępność Oczekujemy platforma Nintendo 3DS odnośnik robson.pl/produkt,16238,rayman_and_rabbids_family_pack.html Adres ul.Powstańców Śląskich 106D/200 01-466 Warszawa Godziny otwarcia poniedziałek-piątek w godz. 9-17 sobota w godz. 10-15 Nr konta 25 1140 2004 0000 3702 4553 9550 Adres e-mail Oferta sklepu : [email protected] Pytania techniczne : [email protected] Nr telefonów tel. 224096600 Serwis : [email protected] tel. 224361966 Zamówienia : [email protected] Wymiana gier : [email protected] Rayman And Rabbids Family Pack jest kompilacją zawierającą trzy gry: Rayman Origins, Rabbids Rumble oraz Rabbids 3D. Rayman Origins jest kolejną odsłoną popularnej serii gier zręcznościowych. Za produkcję odpowiada Ubisoft Studios, które jest znane m.in. z Arthur and the Revenge of Maltazard oraz Assassin's Creed. Akcja gry toczy się przed wydarzeniami znanymi z pierwszej odsłony cyklu. Gracz wciela się w postać tytułowego bohatera i wyrusza do Rozdroża Marzeń - krainy stworzonej przez boga Polokusa. Niestety jest ona zamieszkana przez złe Mroklumy (potwory powstałe w wyniku infekcji sennymi koszmarami). Rayman wraz z przyjaciółmi postanawia pokonać mroczne istoty i uratować świat. Rayman Origins utrzymany jest w konwencji 2D, a oprawa graficzna jest bardzo kolorowa i miła dla oka. Warto również wspomnieć o trybie kooperacji dla czterech graczy, który jest wzorowany na tym z New Super Mario Bros. Dodatkowo po ukończeniu każdego poziomu w co-opie ukazują się statystyki każdego gracza. Rabbids Rumble jest kolejną odsłoną bardzo popularnej serii traktującej o przygodach Szalonych Królików. Grę stworzyło studio Ubisoft, które jest znane m.in. -

Analyzing Space Dimensions in Video Games

SBC { Proceedings of SBGames 2019 | ISSN: 2179-2259 Art & Design Track { Full Papers Analyzing Space Dimensions in Video Games Leandro Ouriques Geraldo Xexéo Eduardo Mangeli Programa de Engenharia de Sistemas e Programa de Engenharia de Sistemas e Programa de Engenharia de Sistemas e Computação, COPPE/UFRJ Computação, COPPE/UFRJ Computação, COPPE/UFRJ Center for Naval Systems Analyses Departamento de Ciência da Rio de Janeiro, Brazil (CASNAV), Brazilian Nay Computação, IM/UFRJ E-mail: [email protected] Rio de Janeiro, Brazil Rio de Janeiro, Brazil E-mail: [email protected] E-mail: [email protected] Abstract—The objective of this work is to analyze the role of types of game space without any visualization other than space in video games, in order to understand how game textual. However, in 2018, Matsuoka et al. presented a space affects the player in achieving game goals. Game paper on SBGames that analyzes the meaning of the game spaces have evolved from a single two-dimensional screen to space for the player, explaining how space commonly has huge, detailed and complex three-dimensional environments. significance in video games, being bound to the fictional Those changes transformed the player’s experience and have world and, consequently, to its rules and narrative [5]. This encouraged the exploration and manipulation of the space. led us to search for a better understanding of what is game Our studies review the functions that space plays, describe space. the possibilities that it offers to the player and explore its characteristics. We also analyze location-based games where This paper is divided in seven parts. -

Ubisoft Studios

CREATIVITY AT THE CORE UBISOFT STUDIOS With the second largest in-house development staff in the world, Ubisoft employs around 8 000 team members dedicated to video games development in 29 studios around the world. Ubisoft attracts the best and brightest from all continents because talent, creativity & innovation are at its core. UBISOFT WORLDWIDE STUDIOS OPENING/ACQUISITION TIMELINE Ubisoft Paris, France – Opened in 1992 Ubisoft Bucharest, Romania – Opened in 1992 Ubisoft Montpellier, France – Opened in 1994 Ubisoft Annecy, France – Opened in 1996 Ubisoft Shanghai, China – Opened in 1996 Ubisoft Montreal, Canada – Opened in 1997 Ubisoft Barcelona, Spain – Opened in 1998 Ubisoft Milan, Italy – Opened in 1998 Red Storm Entertainment, NC, USA – Acquired in 2000 Blue Byte, Germany – Acquired in 2001 Ubisoft Quebec, Canada – Opened in 2005 Ubisoft Sofia, Bulgaria – Opened in 2006 Reflections, United Kingdom – Acquired in 2006 Ubisoft Osaka, Japan – Acquired in 2008 Ubisoft Chengdu, China – Opened in 2008 Ubisoft Singapore – Opened in 2008 Ubisoft Pune, India – Acquired in 2008 Ubisoft Kiev, Ukraine – Opened in 2008 Massive, Sweden – Acquired in 2008 Ubisoft Toronto, Canada – Opened in 2009 Nadeo, France – Acquired in 2009 Ubisoft San Francisco, USA – Opened in 2009 Owlient, France – Acquired in 2011 RedLynx, Finland – Acquired in 2011 Ubisoft Abu Dhabi, U.A.E – Opened in 2011 Future Games of London, UK – Acquired in 2013 Ubisoft Halifax, Canada – Acquired in 2015 Ivory Tower, France – Acquired in 2015 Ubisoft Philippines – Opened in 2016 UBISOFT PaRIS Established in 1992, Ubisoft’s pioneer in-house studio is responsible for the creation of some of the most iconic Ubisoft brands such as the blockbuster franchise Rayman® as well as the worldwide Just Dance® phenomenon that has sold over 55 million copies. -

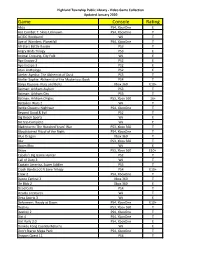

Game Console Rating

Highland Township Public Library - Video Game Collection Updated January 2020 Game Console Rating Abzu PS4, XboxOne E Ace Combat 7: Skies Unknown PS4, XboxOne T AC/DC Rockband Wii T Age of Wonders: Planetfall PS4, XboxOne T All-Stars Battle Royale PS3 T Angry Birds Trilogy PS3 E Animal Crossing, City Folk Wii E Ape Escape 2 PS2 E Ape Escape 3 PS2 E Atari Anthology PS2 E Atelier Ayesha: The Alchemist of Dusk PS3 T Atelier Sophie: Alchemist of the Mysterious Book PS4 T Banjo Kazooie- Nuts and Bolts Xbox 360 E10+ Batman: Arkham Asylum PS3 T Batman: Arkham City PS3 T Batman: Arkham Origins PS3, Xbox 360 16+ Battalion Wars 2 Wii T Battle Chasers: Nightwar PS4, XboxOne T Beyond Good & Evil PS2 T Big Beach Sports Wii E Bit Trip Complete Wii E Bladestorm: The Hundred Years' War PS3, Xbox 360 T Bloodstained Ritual of the Night PS4, XboxOne T Blue Dragon Xbox 360 T Blur PS3, Xbox 360 T Boom Blox Wii E Brave PS3, Xbox 360 E10+ Cabela's Big Game Hunter PS2 T Call of Duty 3 Wii T Captain America, Super Soldier PS3 T Crash Bandicoot N Sane Trilogy PS4 E10+ Crew 2 PS4, XboxOne T Dance Central 3 Xbox 360 T De Blob 2 Xbox 360 E Dead Cells PS4 T Deadly Creatures Wii T Deca Sports 3 Wii E Deformers: Ready at Dawn PS4, XboxOne E10+ Destiny PS3, Xbox 360 T Destiny 2 PS4, XboxOne T Dirt 4 PS4, XboxOne T Dirt Rally 2.0 PS4, XboxOne E Donkey Kong Country Returns Wii E Don't Starve Mega Pack PS4, XboxOne T Dragon Quest 11 PS4 T Highland Township Public Library - Video Game Collection Updated January 2020 Game Console Rating Dragon Quest Builders PS4 E10+ Dragon -

Annual Report

ANNUAL REPORT 1111 A statement from Yves Guillemot In 2010-2011, Ubisoft won over new market share in all territories and strengthened its position as 3rd independent publisher. Our sales were carried by the success of our dance titles and the performance of Assassin’s Creed Brotherhood. Ubisoft also confirmed its position as a key partner among console makers, establishing itself as 1st independent publisher on Kinect™, Wii™ and the 3DS™. Ubisoft has also continued to reorganize its On the high-definition market, Assassin’s Creed studios, and abandoned some projects in order Brotherhood last year proved that we are capable to concentrate on titles with stronger market of releasing a very high quality franchise on potential, which translated into a net loss of a yearly basis, and establishing our brands in € 52 million. Nevertheless, we have managed multiplayer. Our objective is to reproduce this to reinforce our financial position with annual success with other brands and reinforce ties with sales up 19.3% to € 1,039 million, a net operating players. The year 2011-2012 will be marked by income* of € 29 million and a positive cash flow of a line-up particularly rich in key franchises, and € 99.2 million. which reaches a wider audience. Combined with investments made over the past It includes, among others, Assassin’s Creed few years, mainly in our key franchises and online, Revelations, Driver San Francisco, Ghost Recon these results have put Ubisoft in a position of Future Soldier, Rayman Origins, the adaptation of profitable growth for the coming years. For this the Tintin film as well as Child of Eden and Raving reason, we will continue to pursue our strategy Rabbids on Kinect™.