Fred Goldstein

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2018 New Member Orientation November 26 – 27, 2018

2018 New Member Orientation November 26 – 27, 2018 Monday, November 26, 2018 *All events are in the State House unless noted* Throughout the day Slide Show: The Legislature Cafeteria Lounge 7:15 a.m. – 9:00 a.m. Registration, Payroll, Expenses, Benefits, Photographs, and Room: 10/Room: 11 iPad Distribution and Training 7:30 a.m. – 10:00 a.m. Breakfast [PLEASE register first] Cafeteria - sidebar Open Cafeteria Account (if desired) 9:15 a.m. – 9:25 a.m. Welcome and Introduction Room 11 Mark Snelling, President, Snelling Center for Government 9:25 a.m. – 10:10 a.m. The Legislative Process Senate Chamber, or New House and Senate Members go to their respective chambers House Chamber to discuss parliamentary procedures, reporting and debate of bills, the amendment process, recording and notice of proceedings in Calendars and Journals, and legislative decorum John Bloomer, Secretary of the Senate William MaGill, Clerk of the House 10:10 a.m. – 10:20 a.m. Transition to Room 11 on 1st Floor 10:20 a.m. – 10:50 a.m. Overview of the Office of Legislative Council Room 11 Luke Martland, Director and Chief Legislative Counsel 10:50 a.m. – 12:20 p.m. Drafting Bills, Committee Hearings, and the Role of Location to be determined Legislative Council Discussion of the drafting process, bill introduction, the legislative committee process, and the role of the Office VT LEG #319211 v.1A 2018 New Member Orientation Page 2 of 6 Monday, November 26, 2018 continued 12:20 p.m. – 12:30 p.m. Transition to State House Cafeteria on 2nd floor 12:30 p.m. -

HOUSE COMMITTEES 2019 - 2020 Legislative Session

HOUSE COMMITTEES 2019 - 2020 Legislative Session Agriculture & Forestry Education Health Care Rep. Carolyn W. Partridge, Chair Rep. Kathryn Webb, Chair Rep. William J. Lippert Jr., Chair Rep. Rodney Graham, Vice Chair Rep. Lawrence Cupoli, Vice Chair Rep. Anne B. Donahue, Vice Chair Rep. John L. Bartholomew, Ranking Mbr Rep. Peter Conlon, Ranking Member Rep. Lori Houghton, Ranking Member Rep. Thomas Bock Rep. Sarita Austin Rep. Annmarie Christensen Rep. Charen Fegard Rep. Lynn Batchelor Rep. Brian Cina Rep. Terry Norris Rep. Caleb Elder Rep. Mari Cordes Rep. John O'Brien Rep. Dylan Giambatista Rep. David Durfee Rep. Vicki Strong Rep. Kathleen James Rep. Benjamin Jickling Rep. Philip Jay Hooper Rep. Woodman Page Appropriations Rep. Christopher Mattos Rep. Lucy Rogers Rep. Catherine Toll, Chair Rep. Casey Toof Rep. Brian Smith Rep. Mary S. Hooper, Vice Chair Rep. Peter J. Fagan, Ranking Member Energy & Technology Human Services Rep. Charles Conquest Rep. Timothy Briglin, Chair Rep. Ann Pugh, Chair Rep. Martha Feltus Rep. Laura Sibilia, Vice Chair Rep. Sandy Haas, Vice Chair Rep. Robert Helm Rep. Robin Chesnut-Tangerman, Rep. Francis McFaun, Ranking Member Rep. Diane Lanpher Ranking Member Rep. Jessica Brumsted Rep. Linda K. Myers Rep. R. Scott Campbell Rep. James Gregoire Rep. Maida Townsend Rep. Seth Chase Rep. Logan Nicoll Rep. Matthew Trieber Rep. Mark Higley Rep. Daniel Noyes Rep. David Yacovone Rep. Avram Patt Rep. Kelly Pajala Rep. Heidi E. Scheuermann Rep. Marybeth Redmond Commerce & Rep. Michael Yantachka Rep. Carl Rosenquist Rep. Theresa Wood Economic Development General, Housing, & Military Affairs Rep. Michael Marcotte, Chair Judiciary Rep. Thomas Stevens, Chair Rep. Jean O'Sullivan, Vice Chair Rep. -

Meet Dean Corren Anti-Union 'Think Tank' Wrong About Vermont

Meet Dean Corren Dean Corren talks to board of directors recently. When your board of directors voted single payer health care.” ourselves,” he said in a recent interview to recommend Dean Corren for at Vermont-NEA headquarters. “If Corren, a Progressive who also has the lieutenant governor, the decision we are going to have a functioning backing of Democrats, wants to be a was easy. democracy, we need to restore the lieutenant governor who “will work to meaning of politics.” “He really gets it,” President Martha restore the meaning of politics.” By that, Allen said. “Dean is an unabashed he wants to transform “politics” from This is not Corren’s first stab at elected union supporter. He is a believer in angry, partisan wrangling to a platform office. He served four terms in the the importance of public education. where people of differing views House from 1993-2000; he also was And he, alone among all of the exchange ideas, debate, and agree on an aide to then-Congressman Bernie statewide candidates out there, is a course of action that serves only one Sanders. For more than a decade, dedicated to ensuring our members purpose: to better the lives of everyone. he’s been the chief technology officer are treated fairly in the transition to “Politics, at its core, is how we govern continued on p. 7 Vol. 81 No. 2 • Oct., 2013 www.vtnea.orgThe Official Publication of the Vermont-National EducationAssociation Anti-Union ‘Think Tank’ Wrong About Vermont Vermont-NEA Vermont-NEA Editor’s Note: Vermont-NEA President course let alone reality. -

Ballot Paper

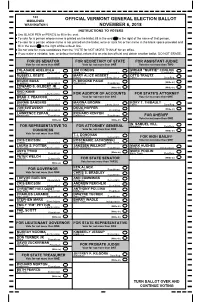

103 MIDDLESEX OFFICIAL VERMONT GENERAL ELECTION BALLOT WASHINGTON 5 NOVEMBER 6, 2018 INSTRUCTIONS TO VOTERS Use BLACK PEN or PENCIL to fill in the oval. To vote for a person whose name is printed on the ballot, fill in the oval to the right of the name of that person. To vote for a person whose name is not printed on the ballot, write or stick his or her name in the blank space provided and fill in the oval to the right of the write-in line. Do not vote for more candidates than the "VOTE for NOT MORE THAN #" for an office. If you make a mistake, tear, or deface the ballot, return it to an election official and obtain another ballot. DO NOT ERASE. FOR US SENATOR FOR SECRETARY OF STATE FOR ASSISTANT JUDGE Vote for not more than ONE Vote for not more than ONE Vote for not more than TWO FOLASADE ADELUOLA JIM CONDOS MIRIAM "MUFFIE" CONLON Shelburne Independent Montpelier Democratic Montpelier Democratic RUSSELL BESTE MARY ALICE HEBERT OTTO TRAUTZ Burlington Independent Putney Liberty Union Cabot Dem/Rep BRUCE BUSA H. BROOKE PAIGE Readsboro Independent Washington Republican (Write-in) EDWARD S. GILBERT JR Barre Town Independent (Write-in) (Write-in) REID KANE Hartford Liberty Union FOR AUDITOR OF ACCOUNTS FOR STATE'S ATTORNEY BRAD J. PEACOCK Vote for not more than ONE Vote for not more than ONE Shaftsbury Independent BERNIE SANDERS MARINA BROWN RORY T. THIBAULT Burlington Independent Charleston Liberty Union Cabot Dem/Rep JON SVITAVSKY DOUG HOFFER Bridport Independent Burlington Dem/Prog (Write-in) LAWRENCE ZUPAN RICHARD KENYON Manchester Republican Brattleboro Republican FOR SHERIFF Vote for not more than ONE (Write-in) (Write-in) W. -

2016 EM General Election Sample Ballot

103 OFFICIAL VERMONT GENERAL ELECTION BALLOT EAST MONTPELIER WASHINGTON 5 NOVEMBER 8, 2016 INSTRUCTIONS TO VOTERS Use BLACK PEN or PENCIL to fill in the oval. To vote for a person whose name is printed on the ballot, fill in the oval to the right of the name of that person. To vote for a person whose name is not printed on the ballot, write or stick his or her name in the blank space provided and fill in the oval to the right of the write-in line. Do not vote for more candidates than the "VOTE for NOT MORE THAN #" for an office. If you make a mistake, tear, or deface the ballot, return it to an election official and obtain another ballot. DO NOT ERASE. FOR US PRESIDENT AND VICE FOR STATE TREASURER FOR HIGH BAILIFF PRESIDENT Vote for not more than ONE Vote for not more than ONE Vote for not more than ONE MURRAY NGOIMA MARC POULIN Pomfret Liberty Union Barre Town Rep/Dem BETH PEARCE HILLARY CLINTON, New York Barre City Dem/Rep (Write-in) and TIM KAINE, Virginia DON SCHRAMM Democratic Burlington Progressive ROCKY DE LA FUENTE, Florida (Write-in) and MICHAEL A. STEINBERG, Florida Independent FOR SECRETARY OF STATE GARY JOHNSON, New Mexico Vote for not more than ONE and WILLIAM F. WELD, Massachusetts Libertarian JIM CONDOS Montpelier Dem/Rep GLORIA LARIVA, California MARY ALICE "MAL" HERBERT and EUGENE PURYEAR, Washington D.C. Putney Liberty Union Liberty Union (Write-in) JILL STEIN, Massachusetts and AJUMA BARAKA, Georgia Green FOR AUDITOR OF ACCOUNTS Vote for not more than ONE DONALD J. -

HOUSE COMMITTEES 2017 - 2018 Legislative Session

HOUSE COMMITTEES 2017 - 2018 Legislative Session Agriculture & Forestry Education Health Care Carolyn W. Partridge, Chair David Sharpe, Chair William J. Lippert Jr., Chair Richard Lawrence, Vice Chair Albert Pearce, Vice Chair Anne B. Donahue, Vice Chair John L. Bartholomew, Rkng Mbr Kathryn Webb, Ranking Member Timothy Briglin, Ranking Member Thomas Bock Scott Beck Annmarie Christensen Susan Buckholz Peter Conlon Brian Cina Rodney Graham Lawrence Cupoli Sarah Copeland-Hanzas Mark Higley Dylan Giambatista Betsy Dunn Jay Hooper Adam Greshin Douglas Gage Amy Sheldon Ben W. Joseph Michael Hebert Harvey Smith Emily Long Lori Houghton Linda Leehman, Committee Assist Alice Miller Ben Jickling Loring Starr, Committee Assistant Appropriations Energy & Technology Catherine Toll, Chair Stephen Carr, Chair Human Services Peter J. Fagan, Vice Chair Curt McCormack, Vice Chair Ann Pugh, Chair Kathleen C. Keenan, Rkng Mbr Corey Parent, Ranking Member Sandy Haas, Vice Chair Maureen Dakin Robin Chesnut-Tangerman Francis McFaun, Ranking Member Martha Feltus Robert Forguites Marianna Gamache Robert Helm Laura Sibilia Brian Keefe Mary S. Hooper Warren Van Wyck Michael Mrowicki Bernard Juskiewicz Michael Yantachka Daniel Noyes Diane Lanpher Faith Brown, Committee Assistant Oliver Olsen Matthew Trieber, Clerk Carl Rosenquist David Yacovone General, Housing & Military Affairs Joseph Troiano Theresa Utton-Jerman, Staff Assoc Helen Head, Chair Theresa Wood Maria Belliveau, Assoc Fiscal Officer Thomas Stevens, Vice Chair Julie Tucker, Committee Assistant Job Tate, Ranking Member Commerce & Economic Kevin "Coach" Christie Judiciary Development Rachael Fields Maxine Grad, Chair William Botzow II, Chair Diana Gonzalez Charles Conquest, Vice Chair Michael Marcotte, Vice Chair Mary E. Howard Thomas Burditt, Ranking Member Jean O'Sullivan, Ranking Member Heidi E. -

2007 – 2008 Scorecard

2007-2008 LEGISLATIVE BIENNIUM VERMONT environmental scorecard VERMONT LEAGUE OF CONSERVATION VOTERS KNOW THE SCORE he Vermont League of Conservation Voters is T a nonpartisan political organization working to turn your environmental values into state priorities. We seek to make environmental protection a top priority for elected officials, candidates, and voters. HOW THE VOTES WERE SELECTED his scorecard is based on the legislative priorities of the environmental and T conservation organizations that form the Vermont Environmental Collaborative as well as other environmental issues. Determining factors in the decision to list particular votes include whether the vote was substantive or procedural in nature, and which vote had the greatest effect on the outcome of the legislation. Please note the limitations of this report. Only roll call votes have been included, as voice votes are not recorded by name. A simple numeric score beside a legislator’s name cannot convey the depth of discussions about the issues, nor can it clearly indicate which legislators worked to protect the environment and which legislators worked to undermine environmental protections. This is particularly true when it comes to work done in the committee room. HOW THE VOTES WERE SCORED he scores were calculated by dividing the number of pro-environmental votes made T by the number of votes the legislator had the opportunity to cast. Absences were counted as a negative vote. Votes during which the Speaker of the House or the President Pro Tem of the Senate presided over their bodies were not counted either way. VLCV did not score legislators who served in 2007 but not 2008. -

Official Return of Votes Elections Division Office of the Secretary of State

OFFICIAL RETURN OF VOTES ELECTIONS DIVISION OFFICE OF THE SECRETARY OF STATE Town CALAIS Election PRIMARY ELECTION (08/11/2020) District WAS-6 1. Total Registered Voters on checklist for this polling place: 1,425 2. Total Number of Voters checked off on the entrance checklist: 672 (this includes absentee ballots) 3. Total number of absentee ballots returned: 588 (Include this count in Line 2) 4. Total number of ballots voted by the Accessible Voting System: 0 5. Total number of DEFECTIVE ballots (not counted but name checked off checklist): 8 (Enter the Total Defective ballots from the Defective Ballot Envelope. -- DO NOT include REPLACED ballots.) 6. TOTAL BALLOTS COUNTED: (Number of voters checked off checklist minus 664 defective ballots.) Total number of ballots counted for DEMOCRATIC 508 Total number of ballots counted for PROGRESSIVE 7 Total number of ballots counted for REPUBLICAN 149 7. Total number of PROVISIONAL ballots (to be sent to Secretary of State): 0 If line 6 (Total Votes Counted.) and the sum of the ballots counted for each party DO NOT agree, you must explain the discrepancies below and continue - Line 6 will be adjusted accordingly: Ballot bag seal #: 07769 þ I hereby certify, under the pains and penalties of perjury, that the information provided is true and accurate to the best of my knowledge, information, and belief.By checking this box, no signature is needed and you agree to the terms and conditions under Vermont law. BARBARA BUTLER JUDITH ROBERT ASSISTANT TOWN CLERK TOWN CLERK 08/12/2020 3120 PEKIN BROOK ROAD, -

Bernie Sanders* (I) Representative to Congress: Peter Welch* (D/WF)

VSEA Endorsements: Addison Senate District U.S. Senate: Bernie Sanders* (I) Representative to Congress: Peter Welch* (D/WF) Governor of Vermont: Peter Shumlin* (D/WF) Lieutenant Governor of Vermont: Cassandra Gekas (P/D) State Treasurer: Beth Pearce* (D/WF) Secretary of State: Jim Condos* (D/P/WF/R) Auditor of Accounts: Vincent Illuzzi (R/WF) Attorney General: Ed Stanak (P) For State Senate: Claire Ayer* (D) Christopher Bray (D) For State Representative: Addison‐1: Middlebury Addison‐Rutland: Orwell, Shoreham, o Betty Nuovo* (D) Whiting, Benson o Paul Ralston* (D) o Will Stevens* (I) Addison‐2: Cornwall, Goshen, Hancock, Orange‐Washington‐Addison: Leicester, Ripton, Salisbury Granville, Braintree, Brookfield, o Willem Jewett* (D) Randolph, Roxbury o Patsy French*(D) Addison‐3: Addison, Ferrisburgh, o Larry Townsend*(D) Panton, Vergennes, Waltham o Diane Lanpher*(D) Washington‐Chittenden: Bolton, Buels Gore, Huntington, Waterbury Addison‐4: Bristol, Lincoln, Monkton, o Rebecca Ellis*(D) Starksboro o Tom Stevens*(D) o Michael Fisher*(D) o Dave Sharpe*(D) Addison‐5: Bridport, New Haven, Weybridge o No Endorsement *Incumbent VSEA Endorsements: Bennington Senate District U.S. Senate: Bernie Sanders* (I) Representative to Congress: Peter Welch* (D/WF) Governor of Vermont: Peter Shumlin* (D/WF) Lieutenant Governor of Vermont: Cassandra Gekas (P/D) State Treasurer: Beth Pearce* (D/WF) Secretary of State: Jim Condos* (D/P/WF/R) Auditor of Accounts: Vincent Illuzzi (R/WF) Attorney General: Ed Stanak (P) For State Senate: Robert “Bob” Hartwell* -

Vermont Environmental Scorecard 2015-2016 Legislative Biennium Vermont Environmental Scorecard

Vermont Environmental Scorecard 2015-2016 Legislative Biennium Vermont Environmental Scorecard Dear Vermonter, We have prepared this Environmental Scorecard to let you know how your state legislators voted on top environmental priorities in the 2015-2016 legislative session. The legislative process can be complicated, and our objective with the Scorecard is to distill the results so you, as a voter, can see which lawmakers are representing your environmental values – and which are not. Each year, Vermont Conservation Voters publishes the Environmental Common Agenda of legislative priorities: a list of top-tier goals we develop in collaboration Vermont Conservation Voters with the state’s other leading environmental groups. The major priorities this (VCV) is the non-partisan biennium included: clean energy – particularly the establishment of a cutting- edge renewable energy standard, thoughtful deployment of clean energy across political action arm of Vermont’s the state, and creation of a Vermont Energy Independence Fund with resources environmental community. generated by putting a price on carbon pollution. Other top-tier priorities included cleaning up Lake Champlain and other waters across the state and better policies to Since 1982, our mission has been to maintain healthy forests. defend and strengthen the laws that Overall, the 2015-2016 legislative session was a success for Vermont’s safeguard our environment. We work environment. In 2015, Governor Peter Shumlin focused his inaugural address on clean water and clean energy, making clear that these were key administrative to elect environmentally responsible priorities and vital to the state’s economic strength. The legislature ultimately candidates. We then hold lawmakers enacted a significant water quality bill and legislation establishing an innovative accountable for the decisions renewable energy standard. -

From: Stephen Whitaker

-----Original Message----- From: Stephen Whitaker <[email protected]> Sent: Wednesday, February 06, 2019 3:28 AM To: Ann Cummings <[email protected]> Cc: Randy Brock <[email protected]>; Christopher Pearson <[email protected]>; Becca Balint <[email protected]>; Brian Campion <[email protected]>; Michael Sirotkin <[email protected]>; [email protected] Subject: What E911 Director Neal didn't tell you last Friday Senator Cummings and Finance Committee members The attached six page, (double spaced) excerpt of the transcript of the October 30 E911 Board meeting reveals not only a chronic management dysfunction but a life threatening flaw in our 911 system. My filing the complete transcript as a public comment in PUC Docket 8850 elicited an immediate response from the hearing officer (attached) due to there being a pending approval requested for a stipulated settlement which still fails to resolve this long known about problem. The E911 Board has not updated rules in more than 20 years yet has all the while has had rulemaking authority (and obligation under statute) such that the companies should have been required by rule to address the lack of redundant, diverse circuits between the host switches and the remotes. Addressing VOIP call blockages of 911 due to CATV amplifiers losing power and having inadequate battery or generator should also have been resolved by rulemaking. Similarly, the process for comprehensive and reliable reporting of outages in either the telecommunications or electric systems resulting in 911 call blockages has also not been made mandatory by rulemaking and the reporting is seriously deficient. -

VPIRG's 2013–2014 Legislative Scorecard

VPIRG’S 2013–2014 Legislative Scorecard VPIRG produces a scorecard of key votes at the conclusion of each legislative biennium. You can use this year’s scorecard to find out how your representatives in the Vermont House and Senate voted on VPIRG-backed legislation to promote clean energy, reduce exposure to toxins, make health care more accessible and affordable and protect our democracy. HOW TO READ THIS SCORECARD H.112—GMO Labeling PUBLIC INTEREST VOTE: YES More information about VPIRG’s work on Legislators were scored based on This bill, introduced and passed by the all these issues, including an archive of whether or not their vote was in past VPIRG scorecards, is available at the public interest. House on a 99 –42 vote in 2013, honors the public’s right to know by requiring ge - www.vpirg.org netically engineered foods in Vermont to = FOR the public interest position be labeled. It was then taken up in a ∆ = AGAINST the public interest slightly revised form by the Senate in S.82—More Money in Politics 2014 and passed on a strong 28 –2 vote. PUBLIC INTEREST VOTE: NO A=the legislator was ABSENT for the vote. This landmark law makes Vermont the In early 2014, legislators changed course N/O = the legislator was not in office at the first state in the nation to actually require on S.82 and decided to alter the legisla - time of the vote. labels on genetically engineered foods. tion significantly by allowing much larger P=Legislator did not vote because he/she was S.81—Banning Chlorinated Tris contributions to certain candidates and PRESIDING over the chamber for that vote PUBLIC INTEREST VOTE: YES political parties.