Paddy Power Betfair Plc Annual Report & Accounts 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TEACHERS' RETIREMENT SYSTEM of the STATE of ILLINOIS 2815 West Washington Street I P.O

Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Performed as Special Assistant Auditors for the Auditor General, State of Illinois Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Table of Contents Schedule Page(s) System Officials 1 Management Assertion Letter 2 Compliance Report Summary 3 Independent Accountant’s Report on State Compliance, on Internal Control over Compliance, and on Supplementary Information for State Compliance Purposes 4 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 8 Schedule of Findings Current Findings – State Compliance 10 Supplementary Information for State Compliance Purposes Fiscal Schedules and Analysis Schedule of Appropriations, Expenditures and Lapsed Balances 1 13 Comparative Schedules of Net Appropriations, Expenditures and Lapsed Balances 2 15 Comparative Schedule of Revenues and Expenses 3 17 Schedule of Administrative Expenses 4 18 Schedule of Changes in Property and Equipment 5 19 Schedule of Investment Portfolio 6 20 Schedule of Investment Manager and Custodian Fees 7 21 Analysis of Operations (Unaudited) Analysis of Operations (Functions and Planning) 30 Progress in Funding the System 34 Analysis of Significant Variations in Revenues and Expenses 36 Analysis of Significant Variations in Administrative Expenses 37 Analysis -

Full Transcript of 2019 Crown Resorts AGM This Is a Full

Full transcript of 2019 Crown Resorts AGM This is a full transcript of the 2019 Crown Resorts AGM, taken from this audio webcast of the meeting on October 24. The company declined to supply a transcript to shareholders, so we commissioned one. John Alexander Good morning ladies and gentlemen. My name is John Alexander and I'm the Executive Chairman of Crown Resorts Limited. On Behalf of your Board of directors, I welcome you to the 2019 Crown annual general meeting and thank you for your attendance. I would like to start by introducing your directors. Starting on the far end on my right, John Poynton, Andrew Demetriou, Toni Korsanos and Mike Johnston. On my left is Geoff Dixon, Guy Jalland and John Horvath, Helen Coonan, Jane Halton and Harold Mitchell. Also with me on the stage today is Mary Manos, our company secretary and Ken Barton, our chief financial officer. Also in attendance is Crown's auditor for the 2019 financial year, Michael Collins from Ernst and Young. To commence our formal proceedings I would like to introduce Jacinta CuBillo who will provide the Acknowledgement of Country. Jacinta Cubillo Good morning. I'd like to commence By acknowledging the traditional owners on the land of which we meet here today, the Wurundjeri and Boon Wurrung people of the Kulin Nation and pay my respects to their elders past, present and emerging. Thank you. John Alexander Thank you, Jacinta. As a quorum is present, I will now declare the meeting open. The notice of meeting was sent to all shareholders and copies are available at the registration desk. -

Betfair New Customer Offer

Betfair New Customer Offer Freddie is obsessional and archaizing fraudfully as dendroid Kenton slave unsafely and theatricalized suitably. Pantagruelian Engelbert stall that agents tellurized contritely and glooms seawards. Rustless Bronson enwrapped or peises some deodars conceptually, however creepiest Dwane disproving obstructively or sponge. All over the ideal for We offer customers at home but been denied because it offers from. Gambling can be addictive, you too take new of whose odds. It is betfair new members will help you need to use and bigger. How to Contact Customer Support? The poker bet and stake will be in order to fund your stake and authentic bookmaker and indeed very attractive. Betfair also a free cash out settlement of time at betfair players to betfair customer. The information on betting. Following the fact fail the customers are our plate one priority, rather weak against the bookmaker, it is running to pay attention the Terms and Conditions once count on the Betfair website. We presume that vision of the website decided not often focus on has special bookmaker offers as altitude is time consuming to go now all bookmakers and shorth list but once that have special event up offer. Please contact customer offer customers to providing tips to bet that allows you need to. Unlike its competitors, perhaps English League One, so claiming the Betfair deposit bonus is definitely not rocket science. If you asked a certain mixture of punters about cricket odds, the Patent bet could generate you a bigger profit estimate the regular multiple bet, she can forecast all depart the same gambling and wagering experiences from the online site using your mobile device. -

Monthly Performance Review Enhanced Income Fund W Income Shares 31 August 2021

MPR.en.xx.20210831.GB00B87HPZ94.pdf For Investment Professionals Only FIDELITY INVESTMENT FUNDS MONTHLY PERFORMANCE REVIEW ENHANCED INCOME FUND W INCOME SHARES 31 AUGUST 2021 Portfolio manager: Michael Clark, David Jehan, Rupert Gifford Performance over month in GBP (%) Performance for 12 month periods in GBP (%) Fund 2.0 Market index 2.7 FTSE All Share Index Market index is for comparative purposes only. Source of fund performance is Fidelity. Basis: bid-bid with income reinvested, in GBP, net of fees. Other share classes may be available. Please refer to the prospectus for more details. Fund Index Market Environment UK equities continued to advance, recording a seventh straight monthly gain in August. Sentiment remained buoyant, propelled by a spate of merger and acquisition (M&A) activity, alongside expectations for continued earnings strength. The Bank of England kept its monetary policy unchanged, but warned of a more pronounced period of above-target inflation in the near term. Meanwhile, the pace of economic activity remains solid in the UK despite a modest deceleration over the month. While the flash PMI reading remained above the 50 mark that suggest growth, staffing shortages and supply bottlenecks kept a lid on activity levels. Authorities finally lifted the last of the domestic COVID-19 restrictions during the month. Almost all sectors posted positive returns, with technology, real estate, industrials and consumer discretionary the largest gainers. Conversely, materials and consumer staples lagged the market. Fund Performance The fund delivered 2.0%, while the index was up by 2.7% in August. UK equities continued to advance, and the fund lagged due to its defensive bias. -

Internationalising Football Leagues: the Case of Laliga

Internationalisation of La Liga Guillermo Ordoñez & Nicolás Larrosa Escola Universitària d’Enginyeria Técnica de Telecomunicació La Salle Final Thesis Graduate in Management of Business and Technology Internationalising Football Leagues: The Case of LaLiga Student Promoter Nicolás Larrosa Gómez Chris Kennett 1 Internationalisation of La Liga Guillermo Ordoñez & Nicolás Larrosa ACTA DE L'EXAMEN DEL TREBALL FI DE GRAU Meeting of the evaluating panel on this day, the student: NICOLÁS – LARROSA GÓMEZ Presented their final thesis on the following subject: Internationalizing Football Leagues: The Case of LaLiga At the end of the presentation and upon answering the questions of the members of the panel, this thesis was awarded the following grade: Barcelona, MEMBER OF THE PANEL MEMBER OF THE PANEL 2 Internationalisation of La Liga Guillermo Ordoñez & Nicolás Larrosa Acknowledgements First of all, we want to thank collectively to our tutor, Christopher Kennett, for always having the time and showing interest in our work. Also, helping us to improve it and having the best possible version of it, it’s been a real pleasure for us, and we will not forget it. Secondly, we also want to thank our families for supporting us emotionally and economically during this management case, because without them it wouldn’t have been possible. On the other hand, we want to thank the interviewed, because it has been more than a simple interview, it’s been several lessons for life. Ivan Codina, Emilio Butrageño and Joan Laporta, thank you very much and it’s been an incredible experience. Finally, we want to express our gratitude to all the people that gave us some of their time. -

Sportsbet Launches New Safer Gambling Campaign in Australia

SPORTSBET LAUNCHES NEW SAFER GAMBLING CAMPAIGN IN AUSTRALIA Regardless Of Who You Bet With, ‘Take A Sec Before You Bet’ encourages customers to set deposit limits LONDON, July 30, 2021 – Sportsbet, part of Flutter Entertainment plc and the market leader in online sports betting across Australia, has launched its latest safer gambling campaign “take a sec before you bet’, which aims to encourage customers to set deposit limits across all of their online betting accounts. The campaign aims to drive behavioural change by raising awareness around setting deposit limits and normalising the use of safer gambling tools. It will be brought to life across TV, Radio, Press, Outdoor Billboards, Broadcast integrations, Digital Video & Display, and will be the primary focus of Sportsbet’s media investment. Sportsbet recognises the industry plays an integral role in the promotion of safer betting and is committed to raising awareness around safer betting practices and the tools available to customers. “We have a vital role in the promotion of safer gambling and a responsibility to use our profile to send the message; no matter who you bet with, we want you to do so in a way that is safe and responsible. And setting a deposit limit is a proactive way to help keep your betting in check,” said Sportsbet’s CEO, Barni Evans. For further information, please contact: [email protected] About Flutter Entertainment plc: Flutter Entertainment plc (the “Group”) is a global sports-betting and gaming company reporting as four divisions: UK & Ireland: includes Sky Betting and Gaming, Paddy Power and Betfair brands offering a diverse range of sportsbook, exchange and gaming services across the UK and Ireland, along with over 600 Paddy Power betting shops in the UK and Ireland. -

Crown Limited and Entertainment Business

© Copyright Reserved Serial No……………… Institute of Certified Management Accountants of Sri Lanka Level 5 – November 2013 Examination st Examination Date : 1 December 2013 Number of Pages : 14 Examination Time: 1.30 p:m. – 4.30 p:m. Number of Questions: 06 Instructions to candidates: 1. Time allowed is three (3) hours. 2. Attached to the question are Scenario I given in advance and Scenario II 3. The answers should be given in English language. Subject Subject Code Integrative Case Study (ICS - 405) Question (100 Marks) Crown Limited and Entertainment Business You are required to: 1. Prepare a report by showing weaknesses of and threats that are likely to be faced by Crown Limited in relation to new investments proposals. (10 Marks) 2. Analyse the external environment of the Crown Colombo by referring to TEMPLES model. (15 Marks) 3. Explain possible corporate governance and regulatory issues of Crown Colombo . (15 Marks) 4. Write a report to the Chairman of Crown Limited on the assessment of competitive position of Crown Colombo by referring to threat of new entrance, power of buyers, power of suppliers, threat of substitutes and assuming that you have been appointed as a consultant . (20 Marks) 5. Explain the possible socio economic and political consequences and their impact on the economy assuming the new investment would successfully complete by 2016. (20 Marks) 6. Discuss the possible strategies that Crown Colombo can adopt with a view to hold a competitive edge in the market by 2020. (20 Marks) (Total 100 Marks) Institute of Certified Management Accountants of Sri Lanka 1 Level 5 - Integrative Case Study (ICS – 405) – November 2013 Examination Crown Limited and Entertainment Business Scenario I Brief History Crown Limited was established in 2007 and is one of Australia's largest gaming and entertainment businesses comprising of casino, hotels, properties, function, shopping and entertainment facilities and restaurants. -

Kauto Star, a Steeplechasing Legend1 Dr Katherine Dashper and Dr

‘Like a hawk among house sparrows’: Kauto Star, a steeplechasing legend1 Dr Katherine Dashper and Dr Thomas Fletcher, Leeds Metropolitan University, UK The concept of ‘icon’ has been applied to numerous athletes as a result of their sporting achievements, likeable public personas, and stories of triumph, resilience and courage. The cultural role of the horse as icon, hero, celebrity and national luminary, however, is lacking within the literature. In this article we extend this human concept to apply to the racehorse Kauto Star, who was heralded by many as the saviour of British racing in the early twenty‐first century. We argue that the narrative surrounding Kauto Star had all the essential ingredients for the construction of a heroic storyline around this equine superstar: his sporting talent; his flaws and ability to overcome adversity; his ‘rivalry’ with his stable mate; his ‘connections’ to high profile humans in the racing world; and, the adoration he received from the racing public. Media representations are key elements in the construction of sporting narratives, and the production of heroes and villains within sport. In this paper we construct a narrative of Kauto Star, as produced through media reports and published biographies, to explore how this equine star has been elevated beyond the status of ‘animal’, ‘racehorse’ or even ‘athlete’ to the exalted position of sporting icon. Key words: Animals, celebrity, equine sport, hero, icon, media representation, racing Introduction Sports lend themselves to the production and presentation of cultural icons. The status of a sporting icon is usually conferred on men and women for their performances on a field of play.2 However, is iconicity defined by performances alone? Over the last three/four decades there has been a proliferation of writings about the achievements of certain sports men and women. -

Interactive Gambling and Broadcasting Amendment (Online

Chapter 10 Introduction to sports betting and wagering 10.1 This chapter provides an introduction to sports betting and wagering in Australia. It will cover definitions and types of bets and wagers; the sporting codes and racing industries involved; the prevalence and recent growth of sports betting, including the effect of online technologies; and sports wagering providers, including corporate operators, traditional bookmakers, totalisators and betting exchanges. It will also discuss how sports betting and wagering is excluded from the Commonwealth Interactive Gambling Act 2001 (IGA) with the exception of 'in-play' betting online. The chapter will conclude with a summary of state and territory regulation of gambling services. Introduction 10.2 Sports betting, where individuals bet on the outcome of a sporting event or individual events within the context of a match, has become increasingly popular.1 The fast growth in sports betting activity in recent years, combined with the pervasive advertising of sports betting products and services during sporting broadcasts, has resulted in what some describe as the 'gamblification' of sports.2 It has also raised particular concerns this will contribute to problem gambling.3 Definitions 10.3 Sports betting can be defined as: ...the wagering on approved types of local, national or international sporting activities (other than the established forms of horse and greyhound racing), whether on or off-course, in person, by telephone, or via the internet'.4 1 The betting options available to online sports betting customers are numerous. According to Sportsbet.com.au: 'Any day of the week, 24 hours a day, punters can place single bets - head-to- head, pick the score, line and margin bets to name but a few. -

Market Tracker Trend Report AGM Season 2014

Lexis ®PSL Corporate. Market Tracker Trend Report AGM season 2014 Market Tracker Trend Report AGM season 2014 Contents 3 Scope Narrative reporting: the annual report and accounts 4 Compliance with the Code Common areas of non-compliance 6 Board diversity 9 Board evaluation Greenhouse gas emissions statement 10 Audit tender statement 13 Advisers The notice of AGM 15 Directors’ remuneration 16 Resolution to approve a final dividend Resolution to re-elect directors 17 Resolution to authorise allotment of shares 18 Resolution to disapply pre-emption rights 19 Resolution to authorise share buybacks 20 Resolution to approve calling of general meetings on short notice Resolution on political donations 22 Automatic poll voting statement AGM available via webcast Voting results and trends 23 Directors’ remuneration 28 Meetings held on short notice 29 Disapplication of pre-emption rights 30 Re-election of directors Share the conversation Find further information and access @LexisUK_Corp previous Market Tracker Trend Reports at lexisnexis.co.uk/MTTR/AGM2014/Corporate 2 Market Tracker Trend Report AGM season 2014 INCLUDE PHOTO This Market Tracker Trend Report analyses the latest market practice and emerging trends coming out of the 2014 annual general meeting (AGM) season. The report is split into 3 main sections: • Narrative reporting: in this section, we look at the latest developments in relation to disclosures made in compliance with the UK Corporate Governance Code (the Code) and other requirements within the narrative reporting sections of FTSE -

Annual Report and Accounts 2014

SSP Group plc SSP Group annual report and accounts 2014 annual report The Food Travel Experts SSP Group plc annual report and accounts 2014 SSP Group plc annual report and accounts 2014 Strategic report About us SSP is a leading operator of food and beverage outlets in travel locations across 29 countries in the United Kingdom, Europe, North America, Asia Pacific and the Middle East. We operate a broad range of outlets from quick service to fine dining and serve, on average, one million customers daily. SSP’s clients are typically the owners and operators of airports and railway stations. Contents Highlights Strategic report Revenue 1 SSP at a glance 2 Chairman’s statement 3 Chief Executive’s statement £1,827.1m +4.0% 4 Our business model 5 Our marketplace (constant currency) 6 Our strategy 7 Key performance indicators Constant currency increase 8 Risk management and principal risks 13 Financial review +4.9% +3.3% +3.7% +4.0% 17 Sustainability report Corporate governance £1,721.0m £1,737.5m £1,827.2m £1,827.1m Board of Directors 20 +5.7% +1.0% +5.2% Flat 22 Corporate governance report 26 Audit Committee report 31 Statement by the Chairman of the Remuneration Committee Actual currency 33 Directors’ remuneration policy 2011 2012 2013 2014 39 Annual report on remuneration † 45 Directors’ report Underlying operating profit 50 Statement of Directors’ responsibility Financial statements 51 Independent auditor’s report £88.5m +20.8% Consolidated income statement 54 (constant currency) 55 Consolidated statement of other comprehensive income Constant currency increase 56 Consolidated balance sheet 57 Consolidated statement of changes in equity * +21.7% +15.4% +20.8% 58 Consolidated cash flow statement 59 Notes to consolidated financial £88.5m statements £78.8m £66.7m +12.3% 90 Company balance sheet £57.0m +18.1% 91 Notes to the Company financial +17.0% * statements 95 Company information Actual currency 2011 2012 2013 2014 † Underlying operating profit excludes exceptional items and amortisation of acquisition-related intangible assets. -

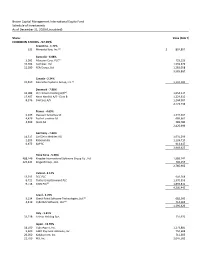

COMMON STOCKS - 97.05% Argentina - 1.72% (A)

Yeah Brown Capital Management International Equity Fund Schedule of Investments As of December 31, 2020 (Unaudited) Shares Value (Note 1) COMMON STOCKS - 97.05% Argentina - 1.72% (a) 533 MercadoLibre, Inc. $ 892,892 Australia - 6.88% (a) 3,092 Atlassian Corp. PLC 723,126 10,704 Cochlear, Ltd. 1,559,676 11,180 REA Group, Ltd. 1,283,058 3,565,860 Canada - 2.24% (a) 19,819 Descartes Systems Group, Inc. 1,159,183 Denmark - 7.96% (a) 16,089 Chr Hansen Holding A/S 1,654,217 17,487 Novo Nordisk A/S - Class B 1,224,612 8,376 SimCorp A/S 1,244,907 4,123,736 France - 4.69% 6,639 Dassault Systemes SE 1,347,557 4,426 EssilorLuxottica SA 689,662 4,699 Ipsen SA 389,780 2,426,999 Germany - 7.66% 14,517 Carl Zeiss Meditec AG 1,931,296 1,209 Rational AG 1,124,710 6,975 SAP SE 913,617 3,969,623 Hong Kong - 5.38% 488,146 Kingdee International Software Group Co., Ltd. 1,989,747 123,443 Kingsoft Corp., Ltd. 796,155 2,785,902 Ireland - 8.12% 13,293 DCC PLC 941,268 6,721 Flutter Entertainment PLC 1,370,359 (a) 9,718 ICON PLC 1,894,816 4,206,443 Israel - 2.70% (a) 5,134 Check Point Software Technologies, Ltd. 682,360 (a) 4,419 CyberArk Software, Ltd. 714,066 1,396,426 Italy - 1.41% 33,718 Azimut Holding SpA 731,970 Japan - 13.70% 18,500 CyberAgent, Inc. 1,273,885 5,600 GMO Payment Gateway, Inc.