Securities and Exchange Commission

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos. (02) 8 376-4039, (02) 8 376-4072, (02) 8 376-4044, (02) 8 332-2353, (02) 8 332-2341, (02) 8 376-5430 Locals 115, 116, 117 and look for Ms. Julie Ann G. Blanquisco or Ms. Marivic A. Dela Torre-Santos E-mail: [email protected] | [email protected] Website: http://llda.gov.ph List of APPROVED DISCHARGE PERMITS as of September 03, 2021 Establishment Address Permit No. Approve Date 11 FTC Enterprises, Inc. 236 P. Dela Cruz San Bartolome Quezon City MM DP-25b-2021-03532 August 18, 2021 189 Realty Corp. (CI Market) Qurino Highway Santa Monica, Novaliches Quezon City MM DP-25b-2021-03744 August 20, 2021 189 Realty Corporation - 2nd (CI Market/Commercial Complex) Quirino Highway, Sta. Monica Novaliches Quezon City MM DP-25b-2021-03743 August 20, 2021 21st Century Mouldings Corporation 18 F. Carlos St. cor. Howmart Road Apolonio Samson Quezon City MM DP-25b-2021-03541 August 23, 2021 24K Property Ventures, Inc. (20 Lansbergh Place Condominium) 170 T. Morato Ave. cor. Sct. Castor Sacred Heart Quezon City MM DP-25b-2021-02819 July 15, 2021 3J Foods Corp. Sta. Ana San Pablo City Laguna DP-16d-2021-03174 August 06, 2021 8 Gilmore Place Condominium 8 Gilmore Ave. cor. 1st St. Valencia New Manila Quezon City MM DP-25b-2021-03829 August 27, 2021 AC Technical Services, Inc. 5 RMT Ind`l. Complex Tunasan Muntinlupa City MM DP-23a-2021-01804 May 12, 2021 Ace Roller Manufacturing, Inc. -

Viper Total Information Solutions, Inc

m DBP Development Bank of the Philippines NOTICE OF AWARD January 31, 2018 VIPER TOTAT INFORMATION SOTUTIONS, INC. Suite 1003 Antel Global Corporate Center, Dona Julia Vargas Avenue, Ortigas Center, Pasig City, Philippines 1600 Telephone: 637-0768 Email address: ana.ramirez@vipe!'-solutions.com Attention MS. ANA VICTORIA E. RAMIREZ Business Development Group Subject : Ar€serve Backup Agent for Linux Maintenance and Support Gentlemen: We are pleased to inform you that the Development Bank of the Philippines hereby awards you the contract for the above-cited subject, details as follows: Toto I Contru ct ( i nc I usive Ptoduct Number Quantity Covered Period ol oll applicoble toxes) (in Php) March 12, 2018 to GMRBABWB2OW2OCG 1 7,900.00 March 11, 2019 To guarantee the faithful performance of obligations, you are required to post within ten (10) calendar days from receipt hereof, a performance security in any of the following forms and percentages: Minimum % of Form of Performance Security Contract Price per Minimum Amount I year Cash, cashier's/manage/s check issued by a Universal or Commercial Bank Bank draft/guarantee or irrevocable letter of credit Five percent 395.00 issued by a Universal or Commercial Bank; provided, (5%l P however, that it shall be confirmed or authenticated by a Universal or Commercial Bank, if issued by a foreign bank I I I Surety Bond callable upon demand issued by a lt l surety or insurance company together with Thirty percent certificate issued by lnsurance Commission certifying P 2,370.00 (30%) the surety or insurance company is authorized to I issue such surety bond HeadOfflce:Sen.CilJ.PuyatAv€nuecorn€rMakatiAvenue,MakatiCity,Philippines. -

NATIONAL CAPITAL REGION Child & Youth Welfare (Residential) ACCREDITED a HOME for the ANGELS CHILD Mrs

Directory of Social Welfare and Development Agencies (SWDAs) with VALID REGISTRATION, LICENSED TO OPERATE AND ACCREDITATION per AO 16 s. 2012 as of March, 2015 Name of Agency/ Contact Registration # License # Accred. # Programs and Services Service Clientele Area(s) of Address /Tel-Fax Nos. Person Delivery Operation Mode NATIONAL CAPITAL REGION Child & Youth Welfare (Residential) ACCREDITED A HOME FOR THE ANGELS CHILD Mrs. Ma. DSWD-NCR-RL-000086- DSWD-SB-A- adoption and foster care, homelife, Residentia 0-6 months old NCR CARING FOUNDATION, INC. Evelina I. 2011 000784-2012 social and health services l Care surrendered, 2306 Coral cor. Augusto Francisco Sts., Atienza November 21, 2011 to October 3, 2012 abandoned and San Andres Bukid, Manila Executive November 20, 2014 to October 2, foundling children Tel. #: 562-8085 Director 2015 Fax#: 562-8089 e-mail add:[email protected] ASILO DE SAN VICENTE DE PAUL Sr. Enriqueta DSWD-NCR RL-000032- DSWD-SB-A- temporary shelter, homelife Residentia residential care -5- NCR No. 1148 UN Avenue, Manila L. Legaste, 2010 0001035-2014 services, social services, l care and 10 years old (upon Tel. #: 523-3829/523-5264/522- DC December 25, 2013 to June 30, 2014 to psychological services, primary community-admission) 6898/522-1643 Administrator December 24, 2016 June 29, 2018 health care services, educational based neglected, Fax # 522-8696 (Residential services, supplemental feeding, surrendered, e-mail add: [email protected] Care) vocational technology program abandoned, (Level 2) (commercial cooking, food and physically abused, beverage, transient home) streetchildren DSWD-SB-A- emergency relief - vocational 000410-2010 technology progrm September 20, - youth 18 years 2010 to old above September 19, - transient home- 2013 financially hard up, (Community no relative in based) Manila BAHAY TULUYAN, INC. -

BUS Schedule, Stops And

BUS bus time schedule & line map Dbp Ave, Taguig City, Manila, Manila →Mmda BUS Navotos Bus Terminal, Circumferential Road 4, View In Website Mode Navotas City, Manila The BUS bus line (Dbp Ave, Taguig City, Manila, Manila →Mmda Navotos Bus Terminal, Circumferential Road 4, Navotas City, Manila) has 2 routes. For regular weekdays, their operation hours are: (1) Dbp Ave, Taguig City, Manila, Manila →Mmda Navotos Bus Terminal, Circumferential Road 4, Navotas City, Manila: 12:00 AM - 11:00 PM (2) Mmda Navotos Bus Terminal, Circumferential Road 4, Navotas City, Manila →Dbp Ave, Taguig City, Manila, Manila: 12:00 AM - 11:00 PM Use the Moovit App to ƒnd the closest BUS bus station near you and ƒnd out when is the next BUS bus arriving. Direction: Dbp Ave, Taguig City, Manila, BUS bus Time Schedule Manila →Mmda Navotos Bus Terminal, Dbp Ave, Taguig City, Manila, Manila →Mmda Circumferential Road 4, Navotas City, Manila Navotos Bus Terminal, Circumferential Road 4, 110 stops Navotas City, Manila Route Timetable: VIEW LINE SCHEDULE Sunday 12:00 AM - 10:00 PM Monday 12:00 AM - 11:00 PM Dbp Ave, Taguig City, Manila, Manila Tuesday 12:00 AM - 11:00 PM Dbp Ave, Taguig City, Manila, Manila East Service Road, Philippines Wednesday 12:00 AM - 11:00 PM Thursday 12:00 AM - 11:00 PM South Luzon Expressway, Taguig City, Manila C-5 Entrance ramp, Philippines Friday 12:00 AM - 11:00 PM South Luzon Expressway, Taguig City, Manila Saturday 12:00 AM - 10:00 PM South Luzon Expressway, Taguig City, Manila South Luzon Expressway, Taguig City, Manila Nichols Exit, -

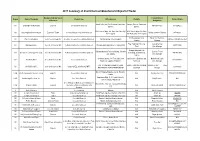

2017 Summary of Shell Charcoal Manufacturer/Exporter/Trader

2017 Summary of Shell Charcoal Manufacturer/Exporter/Trader Business Activity/ Nature Contact Person/ Region Name of Company Product Line Office Address Plantsite Contact Details of Business Designation Ramirez Ricemill, Sta. Catalina, Candelaria, Sariaya, Quezon, Candelaria, IVA Grannygreens Marketing Exporter Coconut Shell Charcoal Menalyn Prado 9566929252 Quezon Quezon 6120, Purok I Brgy. Sto. Nino San Pablo City, 6120, Purok I Brgy. Sto. Nino IVA Astute Agribusiness Ventures Exporter & Trader Coconut Meat,Coconut Shell Charcoal Rivelyn Cordero-Palabrica 335086240 4000 Laguna San Pablo City, 4000 Laguna 848 Masapang Victoria, Chung Yun Tien/ Gen. IVA Wua Yei Enterprises Coir Processor-Exporter Cocofiber, Cocopeat, Coconut Shell Charcoal 848 Masapang Victoria, Laguna 049-566-0269/049-566-0268 Laguna Manager Brgy. Taghangin Morong, Jacqueline Bien IVA Pjkmb Enterprise Coco Shell Charcoal Mfr. Activated Carbon/Coconut Shell Charcoal Sitio Bato Bato Brgy. Dolores Taytay, Rizal 9497135828 Rizal Gen. Manager Silangan Industrial Park Silangan Industrial Park Canlubang, Calamba Dr. Claro Torres IVA Bio-Chem Technology Phil. Corp. Coco Shell Charcoal Mfr. Activated Carbon/Coconut Shell Charcoal Canlubang, Calamba City, 049-549-0782 City, Laguna Gen. Manager Laguna Sia Arayat Street, Joel Town Subd. San San Antonio 1 Balanga, San Maria Monet Dayrit IVA Aim Famiy Farm Coco Shell Charcoal Mfr. Coconut Shell Charcoal 0918-391-4922 Pablo City, Laguna, Philippines Pablo City Gen. Manager LOT 16 ASEANA POWER STATION BRGY. AJOS CATANAUAN, WILMAN L. ISIP Gen. IVA CHARKAI CORP. Coco Shell Charcoal Mfr. COCO SHELL CHARCOAL MFR. 02-5797240 MACAPAGAL AVENUE PARAÑAQUE QUEZON Manager Rm. 235 Regina Bldg. Escolta St., Binondo, I-IVB Pacific Aquamaster Resource Corp. -

AFE-ADB News No 43.Indd

No. 43 | September 2013 The Newsletter of the Association of Former Employees of the Asian Development Bank Delhi Annual General Meeting People, Places and Passages Chapter News IN THIS ISSUE Our Cover No. 43 | September 2013 SEPTEMBER 2013 The Newsletter of the Association of Former Employees of the Asian Development Bank 3 AFE–ADB Updates 3 From the AFE President Delhi Annual General Meeting 3 Chapter Coordinators 4 What’s New at HQ?: Professor Yasutomo on ADB’s Beginnings People, Places and Passages Chapter News 6 Delhi 2013 6 Chapter Coordinators’ Meeting 9 AFE–ADB 27th Annual General Meeting 12 Cocktails 15 Participants Top right: ADB President Takehiko Nakao, 16 Around Delhi former ADB President (and new AFE member) Haruhiko Kuroda, and AFE Chair 19 Chapter News Bong-Suh Lee at the AFE Cocktail Left: “See Through” by Bill Staub 19 Indonesia Below: At the New Zealand Chapter gathering 20 New Zealand: Art Deco, Wine, and More 21 Washington DC 22 People, Places, and Passages AFE–ADB News 22 Connections: Bill Staub’s Art 25 Standing on Their Own (Jaipur) Feet Publisher: Hans-Juergen Springer 27 News Briefs 28 A Letter from the Governor Publications Committee: Jill Gale de Villa (head), 30 North to Anvaya Cove Gam de Armas, Wickie Mercado, Stephen 31 Fifty Years and Still Counting Banta, David Parker, Hans-Juergen Springer 32 Travel and Writing 33 A Walk in the Wilds Graphic Assistance: Jo Jacinto-Aquino 35 Friendship, Food, and Fun at CalloSpa Photographs: ADB Photobank, ADB Security Unit, 36 Humanitarian Ethel Raquel Cabiles, Adrian Davis, Daisy de Chavez, 37 AFE Finland Gathering Graham James Dwyer, Estrellita Gamboa, Ian 37 AFE–ADB Committees Gill, Midi Diel Kawashima, V.R. -

This Document Was Downloaded from Duplication Or Reproduction Is Allowed

This document was downloaded from www.psbank.com.ph. Duplication or reproduction is allowed. Please do not modify its content. Document Classification: PUBLIC COVER SHEET 15552 SEC Registration Number P H I L I P P I N E S AV I N G S B A N K (Company’s Full Name) P S B a n k C e n t e r , 7 7 7 P a s e o d e R o x a s c o r n e r S e d e ñ o S t r e e t , M a k a t i C i t y (Business Address: No. Street City/Town/Province) Leah M. Zamora 845-8888 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting – To be Announced) (Secondary License Type, If Applicable) Markets and Securities Regulation Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 1,455 Total No. of Stockholders Domestic Foreign As of March 31, 2020 To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. This document was downloaded from www.psbank.com.ph. Duplication or reproduction is allowed. Please do not modify its content. Document Classification: PUBLIC SEC Number 15552 FILE Number PHILIPPINE SAVINGS BANK (COMPANY’S NAME) PSBank Center 777 Paseo de Roxas cor. Sedeño St., Makati City (COMPANY’S ADDRESS) 8885-82-08 (TELEPHONE NUMBER) DECEMBER 31 (FISCAL YEAR ENDING MONTH & DAY) SEC FORM 17-A (FORM TYPE) December 31, 2019 (PERIOD ENDED DATE) Government Securities Eligible Dealer (SECONDARY LICENSE TYPE AND FILE NUMBER) This document was downloaded from www.psbank.com.ph. -

Standards Monitoring and Enforcement Division List Of

DEPARTMENT OF TOURISM OFFICE OF TOURISM STANDARDS AND REGULATION - STANDARDS MONITORING AND ENFORCEMENT DIVISION LIST OF OPERATIONAL HOTELS AS OF MARCH 26, 2020, 09:00 AM NATIONAL CAPITAL REGION COUNT NAME OF ESTABLISHMENT ADDRESS 1 Ascott Bonifacio Global City 5th ave. Corner 28th Street, BGC, Taguig 2 Ascott Makati Glorietta Ayala Center, San Lorenzo Village, Makati City 3 Cirque Serviced Residences Bagumbayan, Quezon City 4 Citadines Bay City Manila Diosdado Macapagal Blvd. cor. Coral Way, Pasay City 5 Citadines Millenium Ortigas 11 ORTIGAS AVE. ORTIGAS CENTER, PASIG CITY 6 Citadines Salcedo Makati 148 Valero St. Salcedo Village, Makati city Asean Avenue corner Roxas Boulevard, Entertainment City, 7 City of Dreams Manila Paranaque #61 Scout Tobias cor Scout Rallos sts., Brgy. Laging Handa, Quezon 8 Cocoon Boutique Hotel City 9 Connector Hostel 8459 Kalayaan Ave. cor. Don Pedro St., POblacion, Makati 10 Conrad Manila Seaside Boulevard cor. Coral Way MOA complex, Pasay City 11 Cross Roads Hostel Manila 76 Mariveles Hills, Mandaluyong City Corner Asian Development Bank, Ortigas Avenue, Ortigas Center, 12 Crowne Plaza Manila Galleria Quezon City 13 Discovery Primea 6749 Ayala Avenue, Makati City 14 Domestic Guest House Salem Complex Domestic Road, Pasay City 15 Dusit Thani Manila 1223 Epifanio de los Santos Ave, Makati City 16 Eastwood Richmonde Hotel 17 Orchard Road, Eastwood City, Quezon City 17 EDSA Shangri-La 1 Garden Way, Ortigas Center, Mandaluyong City 18 Go Hotels Mandaluyong Robinsons Cybergate Plaza, Pioneer St., Mandaluyong 19 Go Hotels Ortigas Robinsons Cyberspace Alpha, Garnet Road., San Antonio, Pasig City 20 Gran Prix Manila Hotel 1325 A Mabini St., Ermita, Manila 21 Herald Suites 2168 Chino Roces Ave. -

Where Is My New Servicing Branch Located and How Can I Contact The

Where is my HSBC Ortigas Branch currently located at GF/29F Discovery Suites, ADB Avenue, new servicing Ortigas Center, San Antonio, Pasig City will be relocated to the Lower Ground Level, branch located Shangri-La Plaza East Wing, EDSA corner Shaw Boulevard, Mandaluyong City on and how can I January 4, 2021. You may call HSBC Ortigas Branch phone numbers (+632) 8581- contact the 7903 or (+632) 8581-7435 for any questions. branch? HSBC Quezon City Branch will be permanently closed on December 29, 2020 and client accounts will be transferred to the new location of HSBC Ortigas Branch. You may call HSBC Quezon City Branch phone numbers (+632) 8581-7928 or (+632) 8581-7822 until December 29. 2020. Starting January 4, 2021, you may call HSBC Ortigas Branch through phone numbers mentioned above. HSBC Binondo Branch will be permanently closed on February 16, 2021 and accounts will be transferred to HSBC Makati Branch located at GF, Tower 1, The Enterprise Center, Ayala Avenue corner Paseo de Roxas, Makati City. You may call HSBC Binondo Branch phone numbers (+632) 8581-7249 or (+632) 8581-8198 until February 16, 2021. Starting February 17, 2021, you may call HSBC Makati Branch through phone numbers (+632) 8581-7787 or (+632) 8581-8097. How does this Your account will be automatically transferred into the branches specified above. affect us There will be no impact on how you transact your account which you can do in any of (customers)? our 5 HSBC branches: Makati, BGC, Ortigas, Cebu, and Davao. Do I need to do However, if you have a Safe Deposit Box in Ortigas Branch, Quezon City Branch or anything? Binondo Branch, please refer to the instructions on retrieval of your Safe Deposit Box (SDB) contents. -

No. Company Star

Fair Trade Enforcement Bureau-DTI Business Licensing and Accreditation Division LIST OF ACCREDITED SERVICE AND REPAIR SHOPS As of November 30, 2019 No. Star- Expiry Company Classific Address City Contact Person Tel. No. E-mail Category Date ation 1 (FMEI) Fernando Medical Enterprises 1460-1462 E. Rodriguez Sr. Avenue, Quezon City Maria Victoria F. Gutierrez - Managing (02)727 1521; marivicgutierrez@f Medical/Dental 31-Dec-19 Inc. Immculate Concepcion, Quezon City Director (02)727 1532 ernandomedical.co m 2 08 Auto Services 1 Star 4 B. Serrano cor. William Shaw Street, Caloocan City Edson B. Cachuela - Proprietor (02)330 6907 Automotive (Excluding 31-Dec-19 Caloocan City Aircon Servicing) 3 1 Stop Battery Shop, Inc. 1 Star 214 Gen. Luis St., Novaliches, Quezon Quezon City Herminio DC. Castillo - President and (02)9360 2262 419 onestopbattery201 Automotive (Excluding 31-Dec-19 City General Manager 2859 [email protected] Aircon Servicing) 4 1-29 Car Aircon Service Center 1 Star B1 L1 Sheryll Mirra Street, Multinational Parañaque City Ma. Luz M. Reyes - Proprietress (02)821 1202 macuzreyes129@ Automotive (Including 31-Dec-19 Village, Parañaque City gmail.com Aircon Servicing) 5 1st Corinthean's Appliance Services 1 Star 515-B Quintas Street, CAA BF Int'l. Las Piñas City Felvicenso L. Arguelles - Owner (02)463 0229 vinzarguelles@yah Ref and Airconditioning 31-Dec-19 Village, Las Piñas City oo.com (Type A) 6 2539 Cycle Parts Enterprises 1 Star 2539 M-Roxas Street, Sta. Ana, Manila Manila Robert C. Quides - Owner (02)954 4704 iluvurobert@gmail. Automotive 31-Dec-19 com (Motorcycle/Small Engine Servicing) 7 3BMA Refrigeration & Airconditioning 1 Star 2 Don Pepe St., Sto. -

MAXICARE PRIMA Outpatient Unbundled Product That Has No Age

MAXICARE PRIMA Outpatient unbundled product that has no age eligibility and application form requirement. The product offers unlimited outpatient consultation and laboratory procedures with additional emergency coverage of up to P20,000. Access will be through Maxicare’s Primary Care Center and MyHealth Clinics nationwide. Prima Gold VARIANTS Php 12, 999 SRP *Prices may be changed at any time without further notice Maximum Benefit Limit N/A Age Qualification 60 years old and above Benefit Description - Unlimited outpatient consultations with Maxicare Primary Care Center Physicians. - Pre- existing conditions are covered. - Coverage for outpatient laboratory and diagnostic procedure requested by Maxicare Primary Care Center physicians e.g. Laboratories (CBC, Urinalysis, Lipid Studies, Glucose, etc.) X-ray tests (Chest, Scoliotic, etc) or see last pages for the complete List of Laboratory & Diagnostic Procedures Additional Benefits -Up to P20,000 annual emergency room coverage for PRIMA GOLD, can be availed at any Maxicare affiliated hospital nationwide. -Avail of the following services for free once within one year in METRODENTAL CLINICS nationwide: o Mild Oral Prophylaxis (Cleaning) o Panoramic X-Ray (Full Mouth) o Dental Consult o Emergency relief of dental pain through medication o Cosmetic/Oral Rehab treatment planning o Dental nutrition and counselling o Dental Health Education o Preparation of dental certificates o Safekeeping of dental records as required by law and/or client 1 Enrollment Eligibility Maximum of One (1) card per member per year. Activation You can use the voucher or electronic card for consultation and laboratory within 24 hours from the registration period. For the emergency coverage of Prima Gold, activation is after 7 days from the date of registration. -

1623400766-2020-Sec17a.Pdf

COVER SHEET 2 0 5 7 3 SEC Registration Number M E T R O P O L I T A N B A N K & T R U S T C O M P A N Y (Company’s Full Name) M e t r o b a n k P l a z a , S e n . G i l P u y a t A v e n u e , U r d a n e t a V i l l a g e , M a k a t i C i t y , M e t r o M a n i l a (Business Address: No. Street City/Town/Province) RENATO K. DE BORJA, JR. 8898-8805 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A 0 4 2 8 Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) NONE (Secondary License Type, If Applicable) Corporation Finance Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 2,999 as of 12-31-2020 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. 2 SEC Number 20573 File Number______ METROPOLITAN BANK & TRUST COMPANY (Company’s Full Name) Metrobank Plaza, Sen. Gil Puyat Avenue, Urdaneta Village, Makati City, Metro Manila (Company’s Address) 8898-8805 (Telephone Number) December 31 (Fiscal year ending) FORM 17-A (ANNUAL REPORT) (Form Type) (Amendment Designation, if applicable) December 31, 2020 (Period Ended Date) None (Secondary License Type and File Number) 3 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1.