Official Journal L 40 of the European Union

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

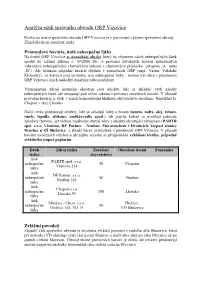

Analýza Rizik Správního Obvodu ORP Vizovice

Analýza rizik správního obvodu ORP Vizovice Riziko na území správního obvodu ORP Vizovice je v porovnání s jinými správními obvody Zlínského kraje poměrně nízké. Průmyslové havárie, únik nebezpečné látky Na území ORP Vizovice se nenachází objekt, který by objemem zásob nebezpečných látek spadal do režimu zákona č. 59/2006 Sb., o prevenci závažných havárií způsobených vybranými nebezpečnými chemickými látkami a chemickými přípravky (skupina „A“ nebo „B“). Ale účinkem případné havárie objektu v sousedících ORP (např. Vsetín, Valašské Klobouky), ve kterých jsou umístěny tyto nebezpečné látky, mohou být obce v působnosti ORP Vizovice jejich následky zasaženy nebo postiženy. Významnými zdroji možného ohrožení jsou objekty, kde se skladují větší zásoby nebezpečných látek, ale nespadají pod režim zákona o prevenci závažných havárií. V případě provozní havárie je však v jejich bezprostřední blízkosti obyvatelstvo ohroženo. Například fa. Cheport v obci Lhotsko Další rizika představují objekty, kde se skladují látky a hmoty benzin, nafta, olej, toluen, tmely, lepidla, silikony, změkčovadla apod.), při jejichž hoření se uvolňují jedovaté zplodiny (toxiny), jež mohou zasáhnout obytné zóny a objekty ohrožující výbuchem (PARTR spol. s.r.o. Všemina, DF Partner - Neubuz, Moraviachem v Hrobicích, čerpací stanice Benzina u ZŠ Slušovice a sklady barev rozmístěné v působnosti ORP Vizovice. V případě havárie uvedených objektů a dle jejího rozsahu se předpokládá vyhlášení třetího, případně zvláštního stupně poplachu. Druh Zdroj rizika Zasažené Ohrožené území Poznámka rizika obyvatelstvo únik PARTR spol. s.r.o. nebezpečné 50 Všemina Všemina 234 látky únik DF Partner, s.r.o. nebezpečné 50 Neubuz Neubuz 165 látky únik Cheport s.r.o nebezpečné 100 Lhotsko Lhotsko 93 látky únik Morávia - Chem, s.r.o. -

Commission Implementing Decision (EU) 2018/883

Status: Point in time view as at 31/10/2019. Changes to legislation: There are currently no known outstanding effects for the Commission Implementing Decision (EU) 2018/883. (See end of Document for details) Commission Implementing Decision (EU) 2018/883 of 18 June 2018 amending the Annex to Implementing Decision 2014/709/EU concerning animal health control measures relating to African swine fever in certain Member States (notified under document C(2018) 3942) (Text with EEA relevance) COMMISSION IMPLEMENTING DECISION (EU) 2018/883 of 18 June 2018 amending the Annex to Implementing Decision 2014/709/EU concerning animal health control measures relating to African swine fever in certain Member States (notified under document C(2018) 3942) (Text with EEA relevance) THE EUROPEAN COMMISSION, Having regard to the Treaty on the Functioning of the European Union, Having regard to Council Directive 89/662/EEC of 11 December 1989 concerning veterinary checks in intra-Community trade with a view to the completion of the internal market(1), and in particular Article 9(4) thereof, Having regard to Council Directive 90/425/EEC of 26 June 1990 concerning veterinary and zootechnical checks applicable in intra-Community trade in certain live animals and products with a view to the completion of the internal market(2), and in particular Article 10(4) thereof, Having regard to Council Directive 2002/99/EC of 16 December 2002 laying down the animal health rules governing the production, processing, distribution and introduction of products of animal origin for human consumption(3), and in particular Article 4(3) thereof, Whereas: (1) Commission Implementing Decision 2014/709/EU(4) lays down animal health control measures in relation to African swine fever in certain Member States, where there have been confirmed cases of that disease in domestic or feral pigs (the Member States concerned). -

Příloha Č. 2 - Seznam Zapojených Linek Do ID ZK

Příloha č. 2 - Seznam zapojených linek do ID ZK Linka Dopravce Název 1 771152 KRODOS BUS Bystřice p. Host. - Holešov - Fryšták - Zlín 2 771155 KRODOS BUS Holešov - Ludslavice - Lechotice - Otrokovice 3 771160 KRODOS BUS Kroměříž - Tlumačov - Otrokovice - Zlín 4 771161 KRODOS BUS Velké Těšany - Nová Dědina - Kvasice - Zlín 5 771201 KRODOS BUS Morkovice - Slížany - Střílky - Nemotice - Koryčany,Blišice 6 771211 KRODOS BUS Kroměříž - Rataje - Litenčice - Kunkovice 7 771231 KRODOS BUS Bystřice p. Host. - Holešov - Kroměříž 8 771240 KRODOS BUS Kroměříž - Chropyně - Záříčí 9 771241 KRODOS BUS Bystřice p. Host. - Chvalčov - Tesák - Troják 10 771242 KRODOS BUS Bystřice p.Host. - Hostýn 11 771243 KRODOS BUS Bystřice p. Host. - Všechovice - Rajnochovice 12 771244 KRODOS BUS Bystřice p. Host. - Rusava 13 771248 KRODOS BUS Holešov - Holešov,Žopy 14 771249 KRODOS BUS Holešov - Prusinovice - Bystřice p. Host. 15 771250 KRODOS BUS Holešov - Bořenovice 16 771251 KRODOS BUS Kroměříž - Hulín - Kostelec u Holešova,Karlovice 17 771252 KRODOS BUS Holešov - Kostelec u Holešova,Karlovice - Němčice 18 771255 KRODOS BUS Kroměříž - Hulín - Míškovice - Tlumačov - Kvasice 19 771261 KRODOS BUS Kroměříž - Zdounky - Zborovice - Morkovice-Slížany 20 771262 KRODOS BUS Kroměříž - Kostelany 21 771263 KRODOS BUS Kroměříž - Bařice - Velké Těšany - Lubná 22 771264 KRODOS BUS Kroměříž - Kvasice - Bělov - Karolín - Lubná 23 771271 KRODOS BUS Rusava - Holešov - Kroměříž 24 771901 KRODOS BUS Kroměříž - Střílky - Koryčany - Kyjov 25 771931 KRODOS BUS Kroměříž - Zlobice,Bojanovice - Kojetín - Prostějov 26 771933 KRODOS BUS Morkovice - Slížany - Dřínov - Věžky,Vlčí Doly 27 771934 KRODOS BUS Kroměříž - Věžky - Morkovice-Slížany - Pačlavice - Vyškov - Brno 28 771940 KRODOS BUS Kroměříž - Kyselovice - Chropyně - Přerov 29 771941 KRODOS BUS Bystřice p.Host. -

-

Celková Požadovaná

Celková požadovaná Příjmení žadatele Obec žadatele Obec realizace výše dotace Kč Abdul Vsetín Vsetín 74802 Adamec Uherský Brod Bojkovice 127500 Adamec Nezdenice Nezdenice 107500 Adámek Rožnov pod Radhoštěm Velká Lhota 127500 Adámek Rožnov pod Radhoštěm Rožnov pod Radhoštěm 127500 Adámek Jablůnka Jablůnka 107500 Adamík Ludslavice Ludslavice 90000 Adamík Lechotice Lechotice 107500 Adámková Vsetín Vsetín 102500 Adamová Zlín Hrobice 102500 Adamuška Brumov-Bylnice Brumov-Bylnice 97500 Ambruz Březolupy Březolupy 102500 Andrlík Záhorovice Záhorovice 102500 Andrys Dolní Bečva Dolní Bečva 127500 Antošová Slavičín Hostětín 120000 Arnesen Janušová Nezdenice Nezdenice 73350 Bábek Střížovice Střížovice 127500 Babíčková Provodov Prostřední Bečva 102500 Babovec Janová Janová 102500 Baček Újezd u Valašských Klobouk Újezd 87500 Baďurová Zádveřice - Raková Zádveřice-Raková 127500 Bachan Uherský Ostroh Uherský Ostroh 127500 Bachanová Uherský Ostroh Uherský Ostroh 127500 Bajza Zlín Zlín 127500 Balaštíková Tupesy Tupesy 102500 Balcar Karolinka Karolinka 102500 Balvan Valašské Meziříčí Valašské Meziříčí 127500 Bambuch Francova Lhota Francova Lhota 90000 Bambuch Kelč Kelč 127500 Bambušek Horní Bečva Horní Bečva 127500 Barcuch Slavičín Slavičín 102500 Baroň Mikulůvka Mikulůvka 107500 Barot Zlín Zlín 102500 Bártek Ratiboř Ratiboř 107500 Bartko Uherský Brod Lopeník 127500 Bartková Nivnice Nivnice 127500 Bártková Slavkov pod Hostýnem Valašské Meziříčí 102500 Bartoníková Otrokovice Otrokovice 127500 Bartošek Kudlovice Kudlovice 102500 Bartošík Slavičín Slavičín -

Situaţie Privind Efectivele De Animale Din Judeţul Maramureş 1

JUDEŢUL MARAMUREŞ PLAN DE ANALIZĂ ŞI ACOPERIRE A RISCURILOR 2016 Anexa nr. 31 SITUAŢIE PRIVIND EFECTIVELE DE ANIMALE DIN JUDEŢUL MARAMUREŞ 1. FERME NR. LOCALITATEA DENUMIRE UNITATE Nr. SPECIA / CATEGORIA EFECTIV DATE DE CONTACT PROPRIETAR / CRT. AUTORIZAŢIE LA RESPONSABIL / DATA 31.12.2014 NUMELE ŞI PRENUMELE NR. TEL. 1 ARDUSAT CAN STAR GS 202 / 25.09.2013 BOVINE LAPTE 20 GHITA NADIA 0262-265012 2 -,,- SELECT FERM 185 / 16.04.2013 BOVINE ÎNGRĂŞAT 67 COŢ ALEXANDRU DĂNUŢ 0262-265012 3 -,,- SELECT FERM 74 / 03.11.2010 PORCINE ÎNGRĂŞAT 2750 COŢ ALEXANDRU DĂNUŢ 0744-617452 4 -,,- CANAGRO GS 218 / 26.06.2014 PORCINE ÎNGRĂŞAT 790 GHITA STELIAN 0722-678777 5 ARDUZEL GLOBAL MARA TR 206 / 11.12.2013 PORCINE ÎNGRĂŞAT 1597 CHERECHEŞ CRISTIAN CĂLIN 0262-223338 6 -,,- -,,- 205 / 05.12.2013 PUI CARNE CHERECHEŞ CRISTIAN CĂLIN 0262-223338 7 BAIA MARE NAŞU 167 / 14.09.2012 BOVINE ÎNGRĂŞAT 19 BRETAN VASILE 0744-265256 8 -,,- COMBIMAR 25 / 30.06.2010 GĂINI OUĂTOARE (G.O.C.) 27742 MOLDOVAN TEODOR 0262-222801 9 -,,- -,,- 24 / 30.06.2010 PUI CARNE MOLDOVAN TEODOR 0262-222801 10 BĂIŢA LANEY 7 / 11.06.2010 GĂINI OUĂTOARE (G.O.C.) 7.525 VEZENTAN VASILE 0746-160801 11 BĂIUŢ BĂIUŢ SERV 92 / 21.12.2010 OVINE ŞI CAPRINE 60 VAUM CAZIMIR 0749-268917 12 BĂSEŞTI AGROFERM DEAC 213 / 14.05.2014 PORCINE ÎNGRĂŞAT 2.407 VOIE DÎNUŢ 0744-372398 13 -,,- FER MARAYUL 197 / 22.08.2013 PORCINE ÎNGRĂŞAT 2294 SZOKE NAGY ATTILA 0742-322104 14 -,,- NARLUC 217 / 17.06.2014 PORCINE ÎNGRĂŞAT 0 MONI ZOLTAN 0769-049329 15 -,,- PREDILECT 8 / 14.06.2010 PORCINE ÎNGRĂŞAT 2.029 REMEŞ STELIANA 0745-572964 16 -,,- RAMISA IMPEX 203 / 17.10.2013 GĂINI OUĂTOARE (G.O.C.) 39.710 SZASZ SANDOR IŞTVAN 0745-972748 17 BOIU MARE POP G. -

Mm-Lista-Gradinitelor-Maramures.Pdf

TABEL CUPRINZÂND GRĂDINIŢELE DIN JUDEŢUL MARAMUREŞ- AN ŞCOLAR 2012-2013- grupe cu grupe cu grupe cu predare grupe predare în limba predare în limba Nr. Nr. în limba maghiară antepreşcolari ucraineană germană grupe Preşcolari (copii între 2-3 Nr. preşcol inscrisi ani) crt unitatea cu personalitate juridică Denumire grădiniţă Adresă Telefon ari 2012-2013 nr. nr. nr. nr. nr. nr. nr. nr. total total grupe copii grupe copii grupe copii grupe copii Gradinita cu Program Baia Mare, GRADINITA CU PROGRAM Prelungit "Ion Creanga", PRELUNGIT ION CREANGA, BAIA Piata 1 Iunie, 1 MARE Baia Mare nr.1 0262-211261 6 130 BAIA MARE PIATA 1 IUNIE NR. 1 Baia [email protected] Gradinita cu Program 0262211263 0262211261 / prescolar Prelungit "Mihai Mare,Crisan,nr 2 Eminescu", Baia Mare .13 0262 -211056 5 115 1 20 Gradinita cu Program Baia Mare, str. 0262 279125 GRADINITA CU PROGRAM Normal Nr. 4, Baia Mare Paltinisului, 3 NORMAL NR.4, BAIA MARE 65/B 6 109 BAIA MARE STR. PALTINISULUI NR. 65B [email protected] Grădiniţa Caritas, Baia 0262279125 0262279125 / prescolar Mare Baia Mare 4 str.Macului 2 41 Gradinita cu Program GRADINITA CU PROGRAM Prelungit "Step by Step", PRELUNGIT STEP BY STEP, BAIA MARE Baia Mare BAIA MARE STR. DR. VICTOR Baia Mare, str. BABES NR. 2 [email protected] Victor Babes, 5 0262422021 0262422021 / prescolar nr. 2 0262-422021 7 171 1 17 SCOALA GIMNAZIALA PETRE Gradinita cu Program DULFU, BAIA MARE BAIA MARE STR. CETATII NR. 4 Prelungit Nr. 8, Baia [email protected] 0262213690 Mare 0262213690 / prescolar/primar / Baia Mare, str. 6 gimnaziu Horea, nr. -

Official Journal L228

Official Journal L 228 of the European Union ★ ★ ★ ★ ★ ★ ★ ★ ★ ★ ★ ★ Volume 62 English edition Legislation 4 September 2019 Contents II Non-legislative acts REGULATIONS ★ Commission Implementing Regulation (EU) 2019/1383 of 8 July 2019 amending and correcting Regulation (EU) No 1321/2014 as regards safety management systems in continuing airworthiness management organisations and alleviations for general aviation aircraft concerning maintenance and continuing airworthiness management (1) .................................. 1 ★ Commission Implementing Regulation (EU) 2019/1384 of 24 July 2019 amending Regulations (EU) No 965/2012 and (EU) No 1321/2014 as regards the use of aircraft listed on an air operator certificate for non-commercial operations and specialised operations, the establishment of operational requirements for the conduct of maintenance check flights, the establishment of rules on non-commercial operations with reduced cabin crew on board and introducing editorial updates concerning air operations requirements (1) ................................ 106 DECISIONS ★ Commission Implementing Decision (EU) 2019/1385 of 3 September 2019 amending the Annex to Implementing Decision 2014/709/EU concerning animal health control measures relating to African swine fever in certain Member States (notified under document C(2019) 6432) (1) 141 (1) Text with EEA relevance. Acts whose titles are printed in light type are those relating to day-to-day management of agricultural matters, and are generally valid for a limited period. EN The titles -

Official Journal L129

Official Journal L 129 of the European Union ★ ★ ★ ★ ★ ★ ★ ★ ★ ★ ★ ★ Volume 62 English edition Legislation 17 May 2019 Contents II Non-legislative acts REGULATIONS ★ Commission Implementing Regulation (EU) 2019/791 of 16 May 2019 amending for the 302nd time Council Regulation (EC) No 881/2002 imposing certain specific restrictive measures directed against certain persons and entities associated with the ISIL (Da'esh) and Al-Qaida organisations ..................................................................................................... 1 DECISIONS ★ Council Decision (EU) 2019/792 of 13 May 2019 entrusting to the European Commission — the Office for the Administration and Payment of Individual Entitlements (PMO) — the exercise of certain powers conferred on the appointing authority and the authority empowered to conclude contracts of employment ............................................................... 3 ★ Commission Implementing Decision (EU) 2019/793 of 16 May 2019 amending the Annex to Implementing Decision 2014/709/EU concerning animal health control measures relating to African swine fever in certain Member States (notified under document C(2019) 3797) (1) ............... 5 RECOMMENDATIONS ★ Commission Recommendation (EU) 2019/794 of 15 May 2019 on a coordinated control plan with a view to establishing the prevalence of certain substances migrating from materials and articles intended to come into contact with food (notified under document C(2019) 3519) (1) .......... 37 (1) Text with EEA relevance. (Continued overleaf) -

Tarif ID Zlínského Kraje

TARIF INTEGROVANÉ DOPRAVY ZLÍNSKÉHO KRAJE (ID ZK) Platnost od 01. 01. 2021 Dodatek č. 1 Tarifu ID ZK platný od 01. 09. 2021 Úplné znění, včetně všech uvedených dodatků TARIF ID ZK 2021 Obsah TARIF INTEGROVANÉ DOPRAVY ZLÍNSKÉHO KRAJE ................................................................................ 1 I. Preambule ............................................................................................................................. 3 II. Úvodní ustanovení ................................................................................................................ 3 III. Základní pojmy ...................................................................................................................... 3 IV. Druhy jízdného ...................................................................................................................... 5 V. Tarifní pravidla ...................................................................................................................... 7 VI. Jízdní doklady ........................................................................................................................ 8 1. Jednotlivé kilometrické jízdné ................................................................................................. 8 2. Dlouhodobé časové kilometrické jízdné (pouze v železniční dopravě) ................................... 9 3. Další jízdní doklady ................................................................................................................ 10 VII. Dovozné ............................................................................................................................. -

Počet Obyvatel V Obcích České Republiky K 1. 1. 2020 Population of Municipalities of the Czech Republic, 1 January 2020

Počet obyvatel v obcích České republiky k 1. 1. 2020 Population of municipalities of the Czech Republic, 1 January 2020 Kód Code Počet obyvatel Population Průměrný věk Average age Název obce okresu obce celkem muži ženy celkem muži ženy Name of municipality LAU 1 LAU 2 Total Males Females Total Males Females CZ0100 554782 Praha 1324277 647286 676991 41,9 40,5 43,3 Okres Benešov CZ0201 529303 Benešov 16758 8024 8734 42,9 41,2 44,5 CZ0201 532568 Bernartice 234 112 122 44,6 47,7 41,8 CZ0201 530743 Bílkovice 218 108 110 43,5 43,7 43,3 CZ0201 532380 Blažejovice 111 54 57 48,4 45,5 51,2 CZ0201 532096 Borovnice 86 41 45 43,9 40,9 46,6 CZ0201 532924 Bukovany 773 387 386 40,4 40,9 39,9 CZ0201 529451 Bystřice 4483 2235 2248 41,5 40,3 42,7 CZ0201 532690 Ctiboř 150 79 71 36,4 36,4 36,5 CZ0201 529478 Čakov 125 66 59 40,5 39,0 42,2 CZ0201 529486 Čechtice 1393 675 718 43,3 41,8 44,7 CZ0201 529516 Čerčany 2917 1453 1464 41,4 40,8 42,1 CZ0201 529532 Červený Újezd 349 173 176 41,1 40,5 41,7 CZ0201 529541 Český Šternberk 166 80 86 43,6 44,1 43,1 CZ0201 529567 Čtyřkoly 721 348 373 40,6 40,1 41,1 CZ0201 532746 Děkanovice 63 32 31 43,8 43,5 44,0 CZ0201 529621 Divišov 1758 881 877 40,5 38,9 42,2 CZ0201 529648 Dolní Kralovice 881 440 441 44,8 43,3 46,3 CZ0201 532151 Drahňovice 103 55 48 37,0 32,3 42,4 CZ0201 532843 Dunice 63 35 28 42,9 39,2 47,6 CZ0201 529702 Heřmaničky 728 368 360 43,0 42,9 43,1 CZ0201 532932 Hradiště 23 15 8 53,4 49,2 61,4 CZ0201 529737 Hulice 298 144 154 44,1 44,7 43,6 CZ0201 529745 Hvězdonice 334 170 164 42,1 41,5 42,7 CZ0201 532886 Chářovice -

Fine-Scale Distribution of Geese in Relation to Key Landscape Elements in Coastal Dobrudzha, Bulgaria

Fine-scale distribution of geese in relation to key landscape elements in coastal Dobrudzha, Bulgaria Preliminary report Anne Harrison & Dr Geoff Hilton May 2014 Wildfowl & Wetlands Trust Slimbridge Gloucestershire GL2 7BT UK T 01453 891900 F 01453 890827 E [email protected] Registered charity in England & Wales, number 1030884, and Scotland, number SC039410 This publication should be cited as: Harrison, AL, & GM Hilton. 2014. Fine-scale distribution of geese in relation to key landscape elements in coastal Dobrudzha, Bulgaria. Preliminary report, WWT Slimbridge, 28 pp. Email [email protected] This study was funded by the LIFE financial instrument of the European Community under the ‘Safe Ground for Red-breasts’ project LIFE09/NAT/BG/000230. 2 Table of Contents Summary ..................................................................................................................................... 4 Introduction .................................................................................................................................. 5 Aims ............................................................................................................................................. 6 Study area ................................................................................................................................... 6 Materials and methods ............................................................................................................... 7 Dropping density as response variable ................................................................................