RESPA Frequently Asked Questions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

YOUR RIGHTS AS a HOMEBUYER OR SELLER Your Rights As a Homebuyer Or Seller

Wisconsin REALTORS® Association YOUR RIGHTS AS A HOMEBUYER OR SELLER Your Rights as a Homebuyer or Seller Congrats on your decision to pursue homeownership! Buying or selling a home is an important life event that requires many important decisions. This booklet explains the services you may expect from a licensed real estate agent and the duties these professionals owe to you under the law. Wisconsin law provides strong protections for all real estate consumers. For more real estate information designed for you, the consumer, visit the WRA’s Downloadable Consumer Brochure page online at www.wra.org/dcb. What’s a real estate agent? that the buyer has the insurance binder and a certified check for A real estate agent is a professional licensed by the state of payment. Wisconsin to help you buy or sell your home. The agent’s job Not all real estate licensees provide the same services, nor do is to bring buyers and sellers together and help them reach an they charge the same fees. To ensure that you are getting the agreement. An agent also provides other services. best value for your money, ask the real estate agents in your community what services they provide, what they charge, and what A real estate agent may assist both parties in negotiating the additional services are recommended or are necessary to complete purchase contract and in filling out certain legal contract forms. the transaction. It is always recommended that you consider the Forms such as the offer to purchase and counter-offer are typically services of an experienced real estate attorney as early in the used during a real estate transaction. -

The Real Estate Marketplace Glossary: How to Talk the Talk

Federal Trade Commission ftc.gov The Real Estate Marketplace Glossary: How to Talk the Talk Buying a home can be exciting. It also can be somewhat daunting, even if you’ve done it before. You will deal with mortgage options, credit reports, loan applications, contracts, points, appraisals, change orders, inspections, warranties, walk-throughs, settlement sheets, escrow accounts, recording fees, insurance, taxes...the list goes on. No doubt you will hear and see words and terms you’ve never heard before. Just what do they all mean? The Federal Trade Commission, the agency that promotes competition and protects consumers, has prepared this glossary to help you better understand the terms commonly used in the real estate and mortgage marketplace. A Annual Percentage Rate (APR): The cost of Appraisal: A professional analysis used a loan or other financing as an annual rate. to estimate the value of the property. This The APR includes the interest rate, points, includes examples of sales of similar prop- broker fees and certain other credit charges erties. a borrower is required to pay. Appraiser: A professional who conducts an Annuity: An amount paid yearly or at other analysis of the property, including examples regular intervals, often at a guaranteed of sales of similar properties in order to de- minimum amount. Also, a type of insurance velop an estimate of the value of the prop- policy in which the policy holder makes erty. The analysis is called an “appraisal.” payments for a fixed period or until a stated age, and then receives annuity payments Appreciation: An increase in the market from the insurance company. -

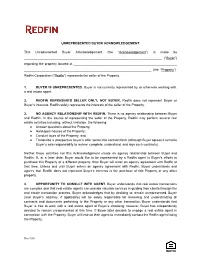

Unrepresented Buyer Acknowledgement

UNREPRESENTED BUYER ACKNOWLEDGEMENT This Unrepresented Buyer Acknowledgement (the “Acknowledgement”) is made by ____________________________________________________________________________ (“Buyer”) regarding the property located at _________________________________________________________ ______________________________________________________________________ (the “Property”). Redfin Corporation (“Redfin”) represents the seller of the Property. 1. BUYER IS UNREPRESENTED. Buyer is not currently represented by, or otherwise working with, a real estate agent. 2. REDFIN REPRESENTS SELLER ONLY, NOT BUYER. Redfin does not represent Buyer or Buyer’s interests. Redfin solely represents the interests of the seller of the Property. 3. NO AGENCY RELATIONSHIP WITH REDFIN. There is no agency relationship between Buyer and Redfin. In the course of representing the seller of the Property, Redfin may perform several real estate activities including, without limitation, the following: ● Answer questions about the Property; ● Hold open houses of the Property; ● Conduct tours of the Property; and ● Transcribe a prospective buyer’s offer terms into contract form (although Buyer agrees it remains Buyer’s sole responsibility to review, complete, understand, and sign such contracts). Neither those activities nor this Acknowledgement create an agency relationship between Buyer and Redfin. If, at a later date, Buyer would like to be represented by a Redfin agent in Buyer’s efforts to purchase this Property or a different property, then Buyer will enter an agency agreement with Redfin at that time. Unless and until Buyer enters an agency agreement with Redfin, Buyer understands and agrees that Redfin does not represent Buyer’s interests in the purchase of this Property or any other property. 4. OPPORTUNITY TO CONSULT WITH AGENT. Buyer understands that real estate transactions are complex and that real estate agents can provide valuable services in guiding their clients through the real estate transaction process. -

OPINION 2020-02 Issued February 7, 2020 Withdraws Adv

OPINION 2020-02 Issued February 7, 2020 Withdraws Adv. Op. 1988-30 Preparation of Deed Upon Direction of Real Estate Agent SYLLABUS: A lawyer should not draft a deed at the direction of his or her client’s real estate agent that is different than the deed required by an executed contract, without the client’s consent, if the new deed will affect the ultimate resolution of the matter or the substantive rights of the client. When interacting with an unrepresented party in a real estate transaction, a lawyer must identify himself or herself as the lawyer for either the buyer or seller, refrain from giving the unrepresented party any legal advice, and may only advise the unrepresented party to secure independent legal counsel. This nonbinding advisory opinion is issued by the Ohio Board of Professional Conduct in response to a prospective or hypothetical question regarding the application of ethics rules applicable to Ohio judges and lawyers. The Ohio Board of Professional Conduct is solely responsible for the content of this advisory opinion, and the advice contained in this opinion does not reflect and should not be construed as reflecting the opinion of the Supreme Court of Ohio. Questions regarding this advisory opinion should be directed to the staff of the Ohio Board of Professional Conduct. 65 SOUTH FRONT STREET, 5TH FLOOR, COLUMBUS, OH 43215-3431 Telephone: 614.387.9370 Fax: 614.387.9379 www.bpc.ohio.gov HON. JOHN W. WISE RICHARD A. DOVE CHAIR DIRECTOR PATRICIA A. WISE D. ALLAN ASBURY VICE- CHAIR SENIOR COUNSEL KRISTI R. MCANAUL COUNSEL OPINION 2020-02 Issued February 7, 2020 Withdraws Adv. -

The Ultimate Guide to Becoming a Real Estate Agent

PLANNING FOR YOUR NEW CAREER: The Ultimate Guide to Becoming a Real Estate Agent A REAL ESTATE EBOOK FROM WELCOME TO YOUR GuideGuide toto BecomingBecoming aa RealReal EstateEstate AgentAgent We know that there’s an overwhelming amount of information out there when it comes to becoming a real estate agent. You may wonder what exactly the job entails, what kinds of salary you can expect to make, or even how you get clients. To help answer your most-pressing questions, we took the guesswork out of it and collected the best and most current information you need to get started. It’s time to follow your dreams! | PAGE 2 IS REAL ESTATE FOR YOU? A career in real estate means a lot things for a lot of people, but here are a few key points that make a career in real estate ideal for you: 1. FLEXIBLE SCHEDULE 2. ENTREPRENEURIAL OPPORTUNITY 3. THE ABILITY TO HELP OTHERS 4. A FUN PROFESSION 5. LOW BARRIER TO ENTRY | PAGE 3 IS NOW THE TIME? YES! The real estate market has historically had its ups and downs, but there’s never been a better time to get started with a career in real estate. Ask yourself these questions to determine if real estate is right for you. HAVE YOU BEEN EAGER IS THE Market Right? FOR A New Career? DO SOME RESEARCH ONLINE AND AT A LOCAL REAL ESTATE AGENCY TO SEE ARE YOU READY TO DO YOU KNOW HOW TO Determine Your Future? Get Your License? DO SOME RESEARCH ONLINE AND AT A LOCAL REAL ESTATE AGENCY TO SEE WHAT’S HAPPENING IN YOUR AREA. -

Mid-Kansas Multiple Listing Service, Inc

Rules and Regulations Of the Mid-Kansas Multiple Listing Service, Inc. Adopted July 2015; Amended April 2016; Amended April 2017; Amended June 2018; Amended Sept 2018; Amended April 2019 SECTION 1 - LISTING PROCEDURES Section 1.0 Listing Procedures Listings of real or personal property of the following types, which are listed subject to a real estate broker’s license, and are located within the service area of the Mid-Kansas Multiple Listing Service, Inc., and are taken by Participants on “Exclusive Right-to-Sell Agreements” or “Exclusive Agency Agreements” shall be entered into the Multiple Listing Service within 2 business days of the listing date or after all necessary signatures of seller(s) have been obtained: a. single family homes for sale or exchange b. vacant lots and acreage for sale or exchange c. two-family, three-family, and four-family residential buildings for sale or exchange d. commercial property e. mobile homes Note 1: The Multiple Listing Service shall not require a Participant to submit listings on a form other than the form the Participant individually chooses to utilize provided the listing is of a type accepted by the Service, although a “Property Profile Sheet” may be required as approved by the Mid-Kansas Multiple Listing Service. However, the Multiple Listing Service, through its legal counsel: a. may reserve the right to refuse to accept a listing form which fails to adequately protect the interests of the public and the Participants b. assure that no listing form filed with the Multiple Listing Service establishes, directly or indirectly, any contractual relationship between the Multiple Listing Service and the client (buyer or seller) The Multiple Listing Service shall accept exclusive right-to-sell listing contracts and exclusive agency listing contracts, and may accept other forms of agreement which make it possible for the listing broker to offer compensation to the other Participants of the Multiple Listing Service acting as subagents, buyer agents, transaction brokers or all. -

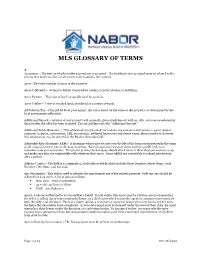

Mls Glossary of Terms

MLS GLOSSARY OF TERMS A Acceptance - The time at which an offer to purchase is accepted. The fact that it was accepted must be relayed to the person that made an offer for all parties to be bound to the contract. Acres - The total number of acres of the property. Acres Cultivated – (of land or fields) Prepared for raising crops by plowing or fertilizing. Acres Pasture – This type of land is typically used by animals. Acres Timber – Trees or wooded land considered as a source of wood. Ad Valorem Tax – Charged by local government, this tax is based on the value of the property, as determined by the local government authorities. Additional Deposit – A buyer of real property will generally give a small deposit with an offer, and a more substantial deposit after the offer has been accepted. The second deposit is the "additional deposit." Additional Public Remarks – "The additional remarks shall not include any contact information i.e. agent, broker, company, bonuses, commission, URL information, affiliated businesses and owner name, phone numbers, however this information may be entered in the Realtor Remarks field". Adjustable Rate Mortgage (ARM) - A mortgage whose interest rate over the life of the loan is not necessarily the same as the original interest rate at the loan inception. Rate changes may go up or down and are usually tied to an economic indicator and a time. The person getting the mortgage should check to see if these fluctuations have a cap, and make sure they are comfortable with whatever that cap is. Some ARMS are convertible to a fixed interest rate after a period. -

A Real Estate Agent Reasons to Become a Real Estate Agent

The BLUEPRINT to Becoming A Real Estate Agent Reasons to Become A Real Estate Agent 1 Make your own schedule and work on your own time. 5 Know that real estate is here to stay! The market will always be there. The economy ebbs and flows, but at the end 2 Unlimited earning potential There are no earnings caps of the day, there will always be customers in need of your in the real estate industry! services and support to buy and sell homes. 3 Start up quickly The process of becoming a real estate 6 Be social and active in your community! Meet agent is less time-consuming than starting many other new people, grow your client base. As a person who careers. loves meeting new people, you’ll develop trust and build relationships with clients who want to give you their future 4 Be Your Own Boss. If you work best independently business. Whether it’s referring friends and family to you, or outside of a team environment, the field is open for you to returning years later with a new opportunity, your friendly and be your own boss. If you thrive on collaboration and working supportive attitude will serve to keep your business booming. closely with others, you can join a firm or establish your own! The average income for a real estate agent is $58,710 according to the Bureau of Labor Statistics. HONDROS College • The Blueprint To Becoming A Real Estate Agent 2 Find Your Fit QUALITIES of A Real Estate Professional Strong work ethic Empathic Charismatic Adapt to Healthy sense Tech savvy changing markets of curiosity Strong Positive attitude Willingness to learn communication skills HONDROS College • The Blueprint To Becoming A Real Estate Agent 3 Other Opportunities in the Real Estate Industry You might think of an agent when real estate comes to mind, but there are more options beyond becoming a salesperson. -

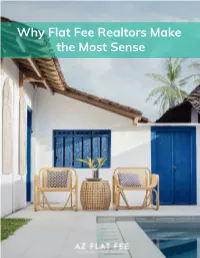

Why Flat Fee Realtors Make the Most Sense TABLES of CONTENTS

Why Flat Fee Realtors Make the Most Sense TABLES OF CONTENTS 02 What Is a Flat Fee in Real Estate? 03 Are Flat Fee Realtors Good? 6 Things a Full Service Flat Fee Estate Broker Can 04 Do for You 05 Flat Fee vs Commission Real Estate The Major Distinguishing Factor Between Flat Fee 06 vs Commission 07 Can You Avoid Paying Realtor Fees? 08 Frequently Asked Questions About Flat Fee Services Working with flat-fee realtors makes the What Is a Flat selling process easier. For instance, one of the biggest reasons people work with flat Fee in Real fee real estate brokers is that they’re able to negotiate offers on your behalf, saving Estate? you thousands of dollars, which you can spend on other things like a down A flat fee is a flat rate charged by real payment. estate agents for listing and selling your property, among other services. It refers to a fixed charge a seller pays an agent Advantages of Hiring Flat instead of the percentage-based Fee Listing Realtor commission. 1. Get more profits from your A traditional agent usually receives a fee- property’s sale based commission that’s usually 2. Save money on commissions calculated at a fixed percentage of the 3. Experienced realtors handle the sale property’s sale price. A flat fee agent of your property works differently as they charge a fixed 4. Enjoy a stress-free sales process rate regardless of the final sale price. 02 Are Flat Fee Realtors Good? Yes, flat-fee realtors are good because they’re less expensive to work with than full-rate realtors. -

Redfin Launches Career Accelerator Program to Bring New, Diverse Talent Into the Real Estate Industry

Redfin Launches Career Accelerator Program to Bring New, Diverse Talent into the Real Estate Industry July 8, 2021 Redfin Helps New Agents Get Established by Offering a Salary, Benefits, $1,500 Signing Bonus, Training and Mentorship Opportunities SEATTLE, July 8, 2021 /PRNewswire/ -- (NASDAQ: RDFN) — Redfin www.redfin.com( ), the technology-powered real estate brokerage, today announced it has launched a career accelerator program to hire and train 50 new real estate agents in the Seattle and Washington, D.C. metro areas. This program is designed for people from outside the real estate industry to successfully transition into a full-time, real estate career. Unlike most agents who work as independent contractors, earning commissions from home sales, Redfin agents are employees who earn a base salary and bonuses for every transaction. Redfin also provides comprehensive benefits, including health insurance and paid leave. In 2020, Redfin agents earned a median income of $112,200. That is more than double the median gross income of $43,330 earned by a typical Realtor in 2020, according to research from the National Association of Realtors (NAR). Redfin agents earn an average of $63,000 in their first year at the company. Realtors with two years of experience or less earned a median gross income of just $8,500 in 2020, according to NAR. "Typically, you need to spend money to make money in real estate and new agents often rack up debt on dues, fees, marketing and technology costs before they sell a house or earn a penny. The career accelerator program gives new agents everything they need to thrive in their first year: a salary and benefits, training, team support, introductions to customers, and a $1,500 signing bonus to make the transition easier," said Kathryn Rion, senior director of real estate operations. -

Guide for Buyers and Sellers Disclaimer

Real estate A guide for buyers and sellers Disclaimer Because this publication avoids the use of legal language, information about the law may have been expressed in general statements. This guide should not be relied upon as a substitute for the Estate Agents Act 1980, the Sale of Land Act 1962 or professional legal advice. © Copyright State of Victoria 2010 No part may be reproduced by any process except in accordance with the provisions of the Copyright Act 1968. For advice on how to reproduce any material from this publication contact Consumer Affairs Victoria. Published by Consumer Affairs Victoria Department of Justice 121 Exhibition Street Melbourne Victoria 3000 Authorised by the Victorian Government 121 Exhibition Street Melbourne Victoria 3000 Printed by Print Dynamics 25 Lionel Road Mt Waverley 3149 ISBN: 0-9750813-7-3 Additional copies This guide is available from Consumer Affairs Victoria, www.consumer.vic.gov.au or 1300 73 70 30. To order more than five copies fax a request to (03) 8684 6333 or write to: Consumer Affairs Victoria GPO Box 123 Melbourne Victoria 3001. Introduction i Introduction This guide provides an overview of the basic steps involved in a residential real estate transaction, including laws that regulate the conduct of estate agents and the buying and selling of real estate in Victoria. These steps have been presented in the order in which you would normally experience them in the buying or selling process. Wherever possible, information is presented for both buyers and sellers. Information specific to one or the other is clearly identified in the form of a buyer’s or seller’s tip. -

REE-103 Real Estate Principles and Practices I

SAMPLE Portfolio Assessment for REE-103 Real Estate Principles and Practices I Note from the Office of Portfolio Assessment For a number of years Thomas Edison State University awarded credit for holders of the current, active NJ Real Estate Sales license, noted below: TESU Course Equivalent Course # Effective Dates Real Estate Broker 3 REE-105 5/1/2000 - 5/31/2015 Real Estate Salesperson License REE-101 5/1/2000 - 5/31/2015 Real Estate Referral Agent 3 REE-101 5/1/2000 - 5/31/2015 During that 15-year period students submitted notarized copies of their NJ, PA or NY credential to earn credit for the above listed courses. Information about these and other “Academic Program Reviews” can be found on the website at: http://www.tesu.edu/academics/cal/apr.cfm For those with other training or credentials, there remains the option for earning credit through portfolio assessment for any other Real Estate course-related subjects. This portfolio is directed toward earning credit for REE-103 Real Estate Principles and Practices I. Real Estate Principles/Practices I (REE-103) 3.00 s.h. Course Description The student will be able to demonstrate knowledge of the complex nature of land ownership, methods of holding title and types of estates as well as a detailed understanding of the option, binder, contract, deed, mortgage and a variety of other instruments. The student should also be able to demonstrate knowledge of real property taxes and assessments, title search, title insurance and closing statements. Learning Outcomes Through the Portfolio Assessment process, students will demonstrate that they can appropriately address the following outcomes: • Compute land perimeters and area (acreage).