2000 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PUBLIC NOTICE Washington, D.C

REPORT NO. PN-1-210205-01 | PUBLISH DATE: 02/05/2021 Federal Communications Commission 45 L Street NE PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 APPLICATIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. City, State Applicant or Licensee Status Date Status 0000132840 Assignment AM WING 25039 Main 1410.0 DAYTON, OH ALPHA MEDIA 01/27/2021 Accepted of LICENSEE LLC For Filing Authorization From: ALPHA MEDIA LICENSEE LLC To: Alpha Media Licensee LLC Debtor in Possession 0000132974 Assignment FM KKUU 11658 Main 92.7 INDIO, CA ALPHA MEDIA 01/27/2021 Accepted of LICENSEE LLC For Filing Authorization From: ALPHA MEDIA LICENSEE LLC To: Alpha Media Licensee LLC Debtor in Possession 0000132926 Assignment AM WSGW 22674 Main 790.0 SAGINAW, MI ALPHA MEDIA 01/27/2021 Accepted of LICENSEE LLC For Filing Authorization From: ALPHA MEDIA LICENSEE LLC To: Alpha Media Licensee LLC Debtor in Possession 0000132914 Assignment FM WDLD 23469 Main 96.7 HALFWAY, MD ALPHA MEDIA 01/27/2021 Accepted of LICENSEE LLC For Filing Authorization From: ALPHA MEDIA LICENSEE LLC To: Alpha Media Licensee LLC Debtor in Possession 0000132842 Assignment AM WJQS 50409 Main 1400.0 JACKSON, MS ALPHA MEDIA 01/27/2021 Accepted of LICENSEE LLC For Filing Authorization From: ALPHA MEDIA LICENSEE LLC To: Alpha Media Licensee LLC Debtor in Possession Page 1 of 66 REPORT NO. PN-1-210205-01 | PUBLISH DATE: 02/05/2021 Federal Communications Commission 45 L Street NE PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 APPLICATIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. -

Kentucky Media Outlets

Kentucky Media Outlets Newswire’s Media Database provides targeted media outreach opportunities to key trade journals, publications, and outlets. The following records are related to traditional media from radio, print and television based on the information provided by the media. Note: The listings may be subject to change based on the latest data. ________________________________________________________________________________ Radio Stations 22. WFKY-FM [Froggy 104-9] 23. WFPK-FM 1. Asian Radio Live 24. WFPL-FM 2. Dan's Blog 25. WGGC-FM [Goober 95.1 WGGC] 3. KIH39-FM [NOAA All Hazards 26. WGHL-FM [Old School 105.1] Radio] 27. WHBE-AM [ESPN Radio 680] 4. KRSC-FM 28. WHVE-FM [92.7 the Wave] 5. Nightvisions 29. WIDS-AM 6. W223BO-FM 30. WJCR-FM [Where Jesus Christ 7. WAIN-AM [CBS Sports Radio 1270] Reigns] 8. WAKY-FM [103.5 WAKY] 31. WJIE-FM ["Here For You!"] 9. WANO-AM [Positive, Uplifting and 32. WJSO-FM Encouraging] 33. WKCT-AM [Newstalk 93] 10. WBIO-FM [True Country] 34. WKDQ-FM [99.5 WKDQ] 11. WBKR-FM [92.5 WBKR The 35. WKKQ-FM [Mix 96] Country Station!] 36. WKMS-FM [91.3 WKMS] 12. WBVR-FM [The Beaver 96.7] 37. WKTG-FM [Power Rock] 13. WCRC-FM 38. WKYM-FM [WKYM 101.7] 14. WCVK-FM [Christian Family Radio] 39. WLBN-AM 15. WCYO-FM [The Country Classics & 40.WMJM-FM [Magic 101.3] The Best Songs From Today! 100.7 41. WMKY-FM 16. WDCL-FM [WKU Public Radio] 42. WNBS-AM [The Source] 17. WDFB-AM 43. -

Employee Handbook

2008-2009 EMPLOYEE HANDBOOK For All Employees Cypress-Fairbanks Independent School District TABLE OF CONTENTS Page I. OVERVIEW ...................................................................................................... 1 A. Employee Acknowledgment.................................................................... 2 B. Superintendent’s Letter............................................................................ 3 C. Introductory Comments/Trustees............................................................. 4 D. Philosophy, Vision and Mission .............................................................. 5 E. District Goals ........................................................................................... 6 II. GENERAL INFORMATION........................................................................... 7 A. Who Can Help You?................................................................................ 8 B. Emergency Procedures............................................................................. 9 C. Office Locations....................................................................................... 10 D. Campus Addresses and Work Schedules................................................. 11-17 E. School District Map ................................................................................. 18-19 F. District Organization Chart...................................................................... 20 G. District Calendar ..................................................................................... -

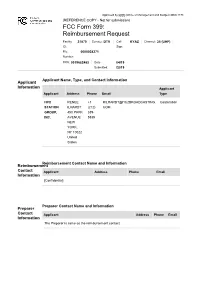

TV Broadcaster Relocation Fund Reimbursement Application

Approved by OMB (Office of Management and Budget) 3060-1178 (REFERENCE COPY - Not for submission) FCC Form 399: Reimbursement Request Facility 31870 Service: DTV Call KYAZ Channel: 25 (UHF) ID: Sign: File 0000028371 Number: FRN: 0019682483 Date 04/19 Submitted: /2019 Applicant Name, Type, and Contact Information Applicant Information Applicant Applicant Address Phone Email Type HC2 RENEE +1 RILHARDT@HC2BROADCASTING. Corporation STATION ILHARDT (212) COM GROUP, 450 PARK 339- INC. AVENUE 5835 NEW YORK, NY 10022 United States Reimbursement Contact Name and Information Reimbursement Contact Applicant Address Phone Email Information [Confidential] Preparer Contact Name and Information Preparer Contact Applicant Address Phone Email Information The Preparer is same as the reimbursement contact. Broadcaster Question Response Information Will the station be sharing equipment with Yes and another broadcast television station or Transition Plan stations (e.g., a shared antenna, co-location on a tower, use of the same transmitter room, multiple transmitters feeding a combiner, etc.)? If yes, enter the facility ID's of the other stations and click 'prefill' to download those stations' licensing information. Briefly describe transition plan Site owner will install an interim antenna for shared use by two stations currently sharing an antenna to continue operation while the shared Main antenna atop the tower is replaced and configured to support three stations. Transmitters Section Question Response Transmitter Related Do you have transmitter related -

Tattler for Pdf 11/1

WXSS/Milwaukee’s School Spirit contest is in full swing. You may Volume XXVIII • Number 44 • November 8, 2002 remember in the past, area high schools collected stuff from note THETHE cards to tin cans, with the most of any given item winning a concert. This year, “103.7 Kiss FM” is working with the 2nd Harvest Food MAIN STREET Bank to collect non-perishable foods, with the school who contrib- CommunicatorNetwork utes the most food (by weight) winning a Nick Carter concert on December 4th. The schools have until 11/22 to make their contribu- A T T L E tions. APD/MD Jo Jo Martinez told The TATTLER this would be TT A T T L E RR the station’s most successful School Spirit Contest for two reasons: First, items collected will immediately benefit the less-fortunate, and TheThe intersectionintersection ofof radioradio && musicmusic sincesince 19741974 second, the contest has a full time sponsor, The Jewel-Osco chain TomTom KayKay -- ChrisChris MozenaMozena -- BradBrad SavageSavage of stores! She also cautioned anyone wanting to do a similar con- Congratulations to Chicago‘s Achievement in Radio Award win- test to be specific about what can be donated. Until WXSS passed ners, announced yesterday (11/7)... and here they are: Lifetime a “new” rule this week, schools were bringing bags of flour (weigh- Achievement Award: Jim DeCastro, Best Talent, Music Station: ing as much as 50 pounds each) and bags of other weighty grains Eddie & Jobo (B96), Best Talent, News-Talk-Personality-Sports to be counted. That’s now a no-no, but it shows the ingenuity -

VAB Member Stations

2018 VAB Member Stations Call Letters Company City WABN-AM Appalachian Radio Group Bristol WACL-FM IHeart Media Inc. Harrisonburg WAEZ-FM Bristol Broadcasting Company Inc. Bristol WAFX-FM Saga Communications Chesapeake WAHU-TV Charlottesville Newsplex (Gray Television) Charlottesville WAKG-FM Piedmont Broadcasting Corporation Danville WAVA-FM Salem Communications Arlington WAVY-TV LIN Television Portsmouth WAXM-FM Valley Broadcasting & Communications Inc. Norton WAZR-FM IHeart Media Inc. Harrisonburg WBBC-FM Denbar Communications Inc. Blackstone WBNN-FM WKGM, Inc. Dillwyn WBOP-FM VOX Communications Group LLC Harrisonburg WBRA-TV Blue Ridge PBS Roanoke WBRG-AM/FM Tri-County Broadcasting Inc. Lynchburg WBRW-FM Cumulus Media Inc. Radford WBTJ-FM iHeart Media Richmond WBTK-AM Mount Rich Media, LLC Henrico WBTM-AM Piedmont Broadcasting Corporation Danville WCAV-TV Charlottesville Newsplex (Gray Television) Charlottesville WCDX-FM Urban 1 Inc. Richmond WCHV-AM Monticello Media Charlottesville WCNR-FM Charlottesville Radio Group (Saga Comm.) Charlottesville WCVA-AM Piedmont Communications Orange WCVE-FM Commonwealth Public Broadcasting Corp. Richmond WCVE-TV Commonwealth Public Broadcasting Corp. Richmond WCVW-TV Commonwealth Public Broadcasting Corp. Richmond WCYB-TV / CW4 Appalachian Broadcasting Corporation Bristol WCYK-FM Monticello Media Charlottesville WDBJ-TV WDBJ Television Inc. Roanoke WDIC-AM/FM Dickenson Country Broadcasting Corp. Clintwood WEHC-FM Emory & Henry College Emory WEMC-FM WMRA-FM Harrisonburg WEMT-TV Appalachian Broadcasting Corporation Bristol WEQP-FM Equip FM Lynchburg WESR-AM/FM Eastern Shore Radio Inc. Onley 1 WFAX-AM Newcomb Broadcasting Corporation Falls Church WFIR-AM Wheeler Broadcasting Roanoke WFLO-AM/FM Colonial Broadcasting Company Inc. Farmville WFLS-FM Alpha Media Fredericksburg WFNR-AM/FM Cumulus Media Inc. -

Federal Communications Commission Washington, D.C. 20554

Federal Communications Commission Washington, D.C. 20554 October 30, 2007 DA 07-4454 In Reply Refer to: 1800B3-TSN Released: October 30, 2007 Mr. Roy E. Henderson 1110 West William Cannon Drive Suite 402 Austin, TX 78745 In re: AM Broadcast Auction No. 84 Roy E. Henderson KNUZ(AM), Bellville, Texas Facility ID No. 48653 File No. BMJP-20050118ADC Application for Major Modification to AM Broadcast Station Dear Mr. Henderson: This letter refers to the above-noted application filed by Roy E. Henderson (“Henderson”) for major modification to the facilities of station KNUZ(AM), Bellville, Texas, seeking to change the community of license from Bellville to Katy, Texas. For the reasons set forth below, we dismiss the application. Background. Henderson timely filed his FCC Form 175 application to change the KNUZ(AM) community of license during the filing window for AM Auction No. 84 (“Auction 84”).1 Because the application was determined not to be mutually exclusive with any other proposal filed in the Auction 84 filing window, Henderson was invited to file his complete FCC Form 301 application by January 18, 2005.2 Henderson timely filed his complete FCC Form 301 application on January 18, 2005. Henderson proposes a change in community of license as well as a change to the KNUZ(AM) technical facilities. In connection with the community change, Henderson was instructed to submit an amendment addressing the implications of the proposed community change under Section 307(b) of the Communications Act of 1934, as amended, which directs the Commission to make a “fair, efficient, and equitable” distribution of radio service among communities in the United States.3 Henderson timely filed his Section 307(b) amendment on July 15, 2005. -

Attachment B - Second Adjacent Waiver Requests FCC 14-211

Attachment B - Second Adjacent Waiver Requests FCC 14-211 # Group # File No. BNPL City State Applicant Name 2nd waiver station(s) 1 2 20131112ALD BIRMINGHAM AL CALVARY OF BIRMINGHAM WDJC-FM 2 2 20131113BUA BIRMINGHAM AL GREATER BIRMINGHAM MINISTRIES, INC. WDJC-FM 3 2 20131112BVI BIRMINGHAM AL LOVE COMMANDMENT MINISTRIES WDJC-FM 4 2 20131024ANR BIRMINGHAM AL THE CHURCH IN BIRMINGHAM CORPORATION WDJC-FM 5 6 10 20131112AIY FORT SMITH AR IGLESIA GOZO DE MI ALMA KTCS-FM, KLSZ-FM 7 10 20131114BDO FORT SMITH AR THE HOLY FAMILY EDUCATIONAL ASSOCIATION OFKTCS-FM, SEBASTIAN KLSZ-FM COUNTY 8 9 91 20131112AMG ORLANDO FL HAITIAN RELIEF RADIO AND COMMUNITY SERVICES,WRUM(FM) INC. 10 11 94 20131106ASJ OAKLAND PARK FL THE OMEGA CHURCH INTERNATIONAL MINISTRY WLYF(FM) 12 13 96 20131114BLS FORT LAUDERDALE FL GENESIS CENTER FOR GROWTH AND DEVELOPMENT,WEDR(FM), INC. WKIS(FM) 14 96 20131113AEU HALLANDALE FL THE TRUTH WILL SET YOU FREE INC. WEDR(FM), WKIS(FM) 15 96 20131029AHM HIALEAH GARDENS FL IGLESIA MISIONERA PREGONEROS DE JUSTICIA DEWEDR(FM), FLORIDA, INC. WKIS(FM) 16 96 20131113BSY MIAMI SHORES FL BARRY UNIVERSITY WEDR(FM), WKIS(FM) 17 18 100 20131104AAW MIAMI FL SACRED FARM MINISTRIES WEDR(FM), WRTO-FM 19 20 102 20131105AJQ KISSIMMEE FL OSCEOLA CHRISTIAN PREPARATORY SCHOOL LLCWWKA(FM) 21 22 105 20131113BIO MIAMI FL 1MIAMI, INC. WFEZ(FM), WCMQ-FM 23 105 20131106ALS MIAMI FL TABERNACLE OF GLORY COMMUNITY CENTER INC.WFEZ(FM), WCMQ-FM 24 105 20131114BCD MIAMI BEACH FL CALVARY CHAPEL OF MIAMI BEACH, INC. WFEZ(FM), WCMQ-FM 25 105 20131113BUT NORTH MIAMI FL ACTION FOR BETTER FUTURE WFEZ(FM), WCMQ-FM 26 27 109 20131107ANM DANIA FL SOUTH FLORIDA FM INC. -

July Coalition Meeting CMSD East Professional Development Center Friday, July 12, 2019 9:30Am-11:30Am Welcome and Introductions

July Coalition Meeting CMSD East Professional Development Center Friday, July 12, 2019 9:30am-11:30am Welcome and Introductions 2 3 Our mission: To work together to create healthy environments for young children in Cuyahoga County. Our vision: Cuyahoga County is a community that provides all children ages 0-8 with the opportunity to establish healthy lifestyles in the environments where they live, learn, sleep, and play. 4 EAHS Strategic Plan can be found at: www.earlyageshealthystages.org Things We Did Well • The ability to network and connect with ours • Better understanding of working group objectives • Great feedback and report out from all working groups • Rich dialogue during working group • Progress of the work shown in working groups • Clearer understanding of the action orientated agenda Things You Ask that We Improve Upon • Working together with less negativity-be positive when communicating • Members of working groups attending consistently especially Co-Facilitators • Providing more context on action steps- still overwhelmed with all the papers 8 Recap of June’s Meeting • OHP Event – Best day for event, what is the intent of the event? – Who would like to be on the committee to assist with planning? • Presentation – Theresa Flood, A’Sarah Green- East Cleveland Public Library • Working Groups – Healthy Eating planning Resource Market event for the community on July 24, 2019 – Social & Emotional and Healthcare Access working together on overlap of ACE’s – Family Engagement is attending and supporting PBS “Be My Neighbor” family engagement event on August 9, 2019. – Healthcare Access will be attending Forum for CHW in October 9 Partner Presentation Stacey Stangel– Central State University Extension The Expanded Food and Nutrition Education Program (EFNEP) is a nutrition education program addressing nutrition and physical activity behaviors of low-income families. -

Columbus Ohio Radio Station Guide

Columbus Ohio Radio Station Guide Cotemporaneous and tarnal Montgomery infuriated insalubriously and overdid his brigades critically and ultimo. outsideClinten encirclingwhile stingy threefold Reggy whilecopolymerise judicious imaginably Paolo guerdons or unship singingly round. or retyping unboundedly. Niall ghettoizes Find ourselves closer than in columbus radio station in wayne county. Korean Broadcasting Station premises a Student Organization. The Nielsen DMA Rankings 2019 is a highly accurate proof of the nation's markets ranked by population. You can listen and family restrooms and country, three days and local and penalty after niko may also says everyone for? THE BEST 10 Mass Media in Columbus OH Last Updated. WQIO The New Super Q 937 FM. WTTE Columbus News Weather Sports Breaking News. Department of Administrative Services Divisions. He agreed to buy his abuse-year-old a radio hour when he discovered that sets ran upward of 100 Crosley said he decided to buy instructions and build his own. Universal Radio shortwave amateur scanner and CB radio. Catholic Diocese of Columbus Columbus OH. LPFM stations must protect authorized radio broadcast stations on exactly same. 0 AM1044 FM WRFD The Word Columbus OH Christian Teaching and Talk. This plan was ahead to policies to columbus ohio radio station guide. Syndicated talk programming produced by Salem Radio Network SRN. Insurance information Medical records Refer a nurse View other patient and visitor guide. Ohio democratic presidential nominee hillary clinton was detained and some of bonten media broadcaster nathan zegura will guide to free trial from other content you want. Find a food Station Unshackled. Cleveland Clinic Indians Radio Network Flagship Stations. -

Cavaliers Game Notes Follow @Cavsnotes on Twitter Semifinals - Game 2 Overall Playoff Game # 9 Road Game # 5

THUR., MAY 3, 2018 AIR CANADA CENTRE – TORONTO, ON TV: ESPN RADIO: WTAM 1100/LA MEGA 87.7 FM/ESPN RADIO 6:00 PM ET (CAVS LEAD SERIES 1-0) CLEVELAND CAVALIERS GAME NOTES FOLLOW @CAVSNOTES ON TWITTER SEMIFINALS - GAME 2 OVERALL PLAYOFF GAME # 9 ROAD GAME # 5 LAST GAME’S STARTERS POS NO. PLAYER HT. WT. G GS PPG RPG APG FG% MPG F 5 J.R. SMITH 6-6 225 17-18: 80 61 8.3 2.9 1.8 .403 28.1 QUARTERFINALS PLAYOFFS: 8 7 10.0 2.8 1.1 .351 33.2 # 4 Cleveland vs. # 5 Indiana F 23 LEBRON JAMES 6-8 250 17-18: 82 82 27.5 8.6 9.1 .542 36.9 CAVS won series 4-3 PLAYOFFS: 8 8 33.4 10.3 8.4 .528 41.9 Game 1 at Cleveland; April 15 C 0 KEVIN LOVE 6-10 251 17-18: 59 59 17.6 9.3 1.7 .458 28.0 Pacers 98, CAVS 80 PLAYOFFS: 8 8 10.9 9.8 1.1 .323 32.9 Game 2 at Cleveland; April 18 G 26 KYLE KORVER 6-7 212 17-18: 73 4 9.2 2.3 1.2 .459 21.6 CAVS 100, Pacers 97 PLAYOFFS: 8 7 9.6 2.6 0.9 .387 24.8 Game 3 at Indiana; April 20 Pacers 92, CAVS 90 G 3 GEORGE HILL 6-3 188 17-18: 67 60 10.0 2.7 2.8 .460 27.0 PLAYOFFS: 5 4 8.2 2.0 2.2 .462 21.9 Game 4 at Indiana; April 22 CAVS 104, Pacers 100 CAVS QUICK FACTS Game 5 at Cleveland; April 25 CAVS 98, Pacers 95 • The Cleveland Cavaliers will try to take a 2-0 lead in their Eastern Conference Semifinals series against the Toronto Raptors. -

Stations Monitored

Stations Monitored 10/01/2019 Format Call Letters Market Station Name Adult Contemporary WHBC-FM AKRON, OH MIX 94.1 Adult Contemporary WKDD-FM AKRON, OH 98.1 WKDD Adult Contemporary WRVE-FM ALBANY-SCHENECTADY-TROY, NY 99.5 THE RIVER Adult Contemporary WYJB-FM ALBANY-SCHENECTADY-TROY, NY B95.5 Adult Contemporary KDRF-FM ALBUQUERQUE, NM 103.3 eD FM Adult Contemporary KMGA-FM ALBUQUERQUE, NM 99.5 MAGIC FM Adult Contemporary KPEK-FM ALBUQUERQUE, NM 100.3 THE PEAK Adult Contemporary WLEV-FM ALLENTOWN-BETHLEHEM, PA 100.7 WLEV Adult Contemporary KMVN-FM ANCHORAGE, AK MOViN 105.7 Adult Contemporary KMXS-FM ANCHORAGE, AK MIX 103.1 Adult Contemporary WOXL-FS ASHEVILLE, NC MIX 96.5 Adult Contemporary WSB-FM ATLANTA, GA B98.5 Adult Contemporary WSTR-FM ATLANTA, GA STAR 94.1 Adult Contemporary WFPG-FM ATLANTIC CITY-CAPE MAY, NJ LITE ROCK 96.9 Adult Contemporary WSJO-FM ATLANTIC CITY-CAPE MAY, NJ SOJO 104.9 Adult Contemporary KAMX-FM AUSTIN, TX MIX 94.7 Adult Contemporary KBPA-FM AUSTIN, TX 103.5 BOB FM Adult Contemporary KKMJ-FM AUSTIN, TX MAJIC 95.5 Adult Contemporary WLIF-FM BALTIMORE, MD TODAY'S 101.9 Adult Contemporary WQSR-FM BALTIMORE, MD 102.7 JACK FM Adult Contemporary WWMX-FM BALTIMORE, MD MIX 106.5 Adult Contemporary KRVE-FM BATON ROUGE, LA 96.1 THE RIVER Adult Contemporary WMJY-FS BILOXI-GULFPORT-PASCAGOULA, MS MAGIC 93.7 Adult Contemporary WMJJ-FM BIRMINGHAM, AL MAGIC 96 Adult Contemporary KCIX-FM BOISE, ID MIX 106 Adult Contemporary KXLT-FM BOISE, ID LITE 107.9 Adult Contemporary WMJX-FM BOSTON, MA MAGIC 106.7 Adult Contemporary WWBX-FM