UBL Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

JSY Mother Beneficiary of District Poonch for the Year 2019-20 Name of the Name of Name of the Complete Contact Date of Amount S.No

JSY Mother Beneficiary of District Poonch for the year 2019-20 Name of the Name of Name of the Complete Contact Date of Amount S.No. Husband's Name Institution where Through DBT the Block Beneficiary Address Number Delivery Paid (Rs.) delivery 1 Poonch Nazma Bi Safeer Ahmed Poonch 9622193647 DH Poonch 06.01.2019 ₹ 1,000.00 RSSDH/P/11 2 Poonch Rukhsana Mushtaq Ahmed Poonch 9086853585 DH Poonch 09.03.2019 ₹ 1,000.00 RSSDH/P/11 3 Poonch Meenakshi Rakesh Kumar Poonch 9622299018 DH Poonch 20.03.2019 ₹ 1,000.00 RSSDH/P/11 4 Poonch Rimpy Kumari Sandeep Poonch 9797571072 DH Poonch 12.03.2019 ₹ 1,000.00 RSSDH/P/11 5 Poonch Anjana Pappu Poonch 9797554896 DH Poonch 20.02.2019 ₹ 1,000.00 RSSDH/P/11 6 Poonch Naseeb Fatimah Layqait Ali Poonch 8492930511 DH Poonch 23.09.2018 ₹ 1,000.00 RSSDH/P/11 7 Poonch Nahida Kosser Maroof H Shah Poonch 9596748089 DH Poonch 02.02.2019 ₹ 1,000.00 RSSDH/P/11 8 Poonch Shamshed Begum Mohd Sadiq Poonch 9797314510 DH Poonch 13.03.2019 ₹ 1,000.00 RSSDH/P/11 9 Poonch Santosh Rani Vishal Sharma Poonch 8492928468 DH Poonch 03.04.2019 ₹ 1,000.00 RSSDH/P/11 10 Poonch Khalida Bee Mohd Shoket Poonch 9070654248 DH Poonch 07.04.2019 ₹ 1,000.00 RSSDH/P/11 11 Poonch Farzana Koser Mohd Tariq Poonch 9086202935 DH Poonch 16.03.2019 ₹ 1,000.00 RSSDH/P/11 12 Poonch Heena Kosser Maroof Ahmed Poonch 9596747960 DH Poonch 24.12.2019 ₹ 1,000.00 RSSDH/P/11 13 Poonch Farzana Akhter Aqeel Hussain Poonch 8492012939 DH Poonch 13.04.2019 ₹ 1,000.00 RSSDH/P/25 14 Poonch Meetu Rishi Bharat Bushan Poonch 7051848693 DH Poonch 10.06.2019 ₹ 1,000.00 RSSDH/P/25 -

1-Star Badge Winners 2019

1 - STAR BADGE WINNERS 12th IKSC - 2019 SR. NO. ROLL NO. STUDENT NAME FATHER NAME CLASS 1 19-021-11012-1-002-S MUHAMMAD SUBHAN MUHAMMAD UMAIR 1 2 19-021-11012-1-003-S ABDUL HADI TAHSEEN AHMED 1 3 19-021-11012-1-004-S MANHA SAFWAN SAFWAN AHMED 1 4 19-021-11012-1-012-S NIZAM UDDIN MUHAMMAD HASSAN 1 5 19-021-11020-1-011-S UMAIMA KHAN HIDAYAT ULLAH 1 6 19-021-11077-1-002-S MUHAMMAD HASEEM MUHAMMAD FAISAL 1 7 19-021-11096-1-009-S MANHA IMRAN MUHAMMAD IMRAN ZAFAR 1 8 19-021-11096-1-010-S NABIHA AAMIR AAMIR IQBAL 1 9 19-021-11096-1-011-S BAREERAH FAROOQ FAROOQ 1 10 19-021-11195-1-005-S ALI OSSAT NAQVI ASIF RAZA NAQVI 1 11 19-021-11260-1-002-S TALAL AHMED ALVI FARHAN AHMED ALVI 1 12 19-021-11260-1-006-S AREESHA AZIZ KARIM PADANI 1 13 19-021-11260-1-008-S ZAINAB JUNAID JUNAID SHAMS 1 14 19-021-11260-1-009-S LAISHA SOOMRO SHOAIB IMTIAZ SOOMRO 1 15 19-021-11260-1-017-S AYAAN ABID ABID MAJEED BHATTI 1 16 19-021-11276-1-007-S FAHAD SHEIKH NOUREEN BANO 1 17 19-021-11297-1-003-S SAKINA FAHIM FAHIM IFTEKHAR 1 18 19-021-11305-1-002-S USMAN AZEEM AZEEM KHAN 1 19 19-021-11305-1-004-S ALI HASSAN AHMED HASSAN 1 20 19-021-11305-1-005-S ABDUL HADI TAHIR MUHAMMAD TAHIR 1 21 19-021-11305-1-008-S MUHAMMAD SAAD HANIF GHULAM NASEER 1 22 19-021-11443-1-007-S MUHAMMAD HASAN HASAN MEHMOOD RIZVI 1 23 19-021-11443-1-009-S MUHAMMAD WAHAJ ATTA HUSSAIN JAFRI 1 24 19-021-11443-1-015-S MARYAM BATOOL SYED FAZAL ABBAS 1 25 19-021-11443-1-018-S SYED MUHAMMAD ANJAB JAFRI SYED QAMBER ABBAS JAFRI 1 26 19-021-11443-1-028-S SYED HUSSAIN ABBAS RIZVI SYED HAIDER ABBAS 1 27 19-021-11455-1-009-S SYED KHIZER HUSSAIN ADEEL AHMED HUSSAIN 1 *Criteria: 30% or above but less than 50% score achieved in the respective class 1 - STAR BADGE WINNERS 12th IKSC - 2019 SR. -

FACULTY : COLLEGE : 1 of Page SINDH E-CENTRALIZED

SINDH E-CENTRALIZED COLLEGE ADMISSION POLICY 2017 PLACEMENT IN XI ON MERIT UNDER SECCAP-2017 PRINT DATE : 04/09/2017 FACULTY : Pre-Engineering - Female Page 1 of 9 COLLEGE : 201 ABDULLAH GOVT. COLLEGE FOR WOMEN KARACHI ADMISSION START AT = 751 ADMISSION CLOSED AT = 591 # ROLL - YEAR Name Marks 1 483160 - 2017 TOOBA SHAKIL D/O SHAKIL AKHTAR 751 2 483179 - 2017 NADIA SALEEM D/O MUHAMMAD SALEEM 742 3 470543 - 2017 AQSA SHERAZ D/O MUHAMMAD KHALID SHEROZ 739 4 483178 - 2017 MISBAH D/O ABDUL RAOOF 737 5 481587 - 2017 AYESHA D/O MUHAMMAD IQBAL 724 6 483165 - 2017 FAZEELA QADIR D/O ABDUL QADIR 722 7 484420 - 2017 SAMINA D/O SHAMIM AKHTER 714 8 433353 - 2017 DANIA AHMED D/O SALAHUDDIN AHMED QURAISHI 713 9 439093 - 2017 FABIHA IKHLAQ D/O MUHAMMAD IKHLAQ 709 10 444873 - 2017 FABIHA NADIR D/O NADIR MUHAMMAD QURESHI 708 11 484046 - 2017 AYESHA FAROOQ D/O MUHAMMAD FAROOQ 708 12 432060 - 2017 KHADIJA D/O FAKHRUDDIN 708 13 433941 - 2017 MARIA MEHMOOD D/O MEHMOOD ASHRAF 706 14 446166 - 2017 BIBI IQRA D/O SHAKEEL AHMED 705 15 485623 - 2017 MUBASHRA SABIR D/O SABIR AHMED 705 16 478101 - 2017 NAYAB SHAH D/O SYED WAQAR HUSSAIN SHAH 704 17 484023 - 2017 MISBAH ANSARI D/O IKHLAQ AHMED 704 18 429700 - 2017 HAREEM BINT E ZIA D/O AHMED ZIA UDDIN 703 19 430944 - 2017 NIMRA KHANUM D/O MUHAMMAD SHARIF ULLAH KHAN 703 20 478099 - 2017 IRSA D/O GHULAM RASOOL 702 21 479586 - 2017 DUA ZAHRA JAFRI D/O AZHAR ABBAS JAFRI 702 22 484249 - 2017 MARIA NOUREEN D/O SHAFI ALAM 702 23 477809 - 2017 MARIYAM D/O MUHAMMAD ISHAQ 701 24 482955 - 2017 LAIBA ISLAM RANA D/O SHOUKAT ISLAM -

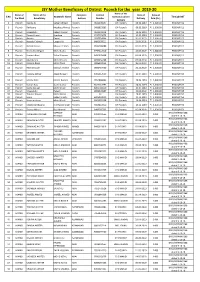

PAKISTAN SERVICES LIMITED LIST of SHAREHOLDERS/BENEFICIAL OWNERS S

PAKISTAN SERVICES LIMITED LIST OF SHAREHOLDERS/BENEFICIAL OWNERS s. No. Folio No. Name of Shareholder Father Name Address Nationality Occupation CNIC NO. Category No. of Shares 1 14 SECRETARY, P.I.A P.I.A. CORPORATION PIA BUILDING KARACHI AIRPORT KARACHI PAKISTANI OTHER OTHERS 172,913 2 15 PRESIDENT OF PAKISTAN PRESIDENTS SECRETARIAT RAWALPINDI PAKISTANI OTHER OTHERS 336,535 3 16 MAHMUD A. HAROON HAROON HOUSE DR. ZIAUDDIN AHMAD ROAD KARACHI-2 PAKISTANI OTHER INDIVIDUALS 40 4 17 SAID A. HAROON HAROON HOUSE DR. ZIAUDDIN AHMAD ROAD KARACHI-2 PAKISTANI OTHER INDIVIDUALS 27 5 23 S.A. SHAKOOR PASHA S/O AL-HAJ S. KARIM BAKSH A-502, BLOCK-3 GULSHAN-E-IQBAL KARACHI PAKISTANI OTHER INDIVIDUALS 67 6 24 ZAFAR MOHAMMAD KHAN 55, MUSLIMABAD M.A. JINNAH ROAD KARACHI-5 PAKISTANI OTHER INDIVIDUALS 67 7 26 HAJIANI HAWA BAI W/O HAJI HASHIM 1119/3, HUSSAINABAD FEDERAL B AREA KARACHI-38 PAKISTANI OTHER INDIVIDUALS 2 8 29 KHAWAJA ABDUL RASHEED S/O MR. ABDUL HAMID C/O CONTINENTAL CYCLE AND MOTOR COMPANY 425, DR. ZIAUDDIN AHMED ROAD, KARACHI. PAKISTANI OTHER INDIVIDUALS 272 9 34 AVARI BYRAMJI DINSHAW S/O MR.BYRAMJI BEACH LUXURY HOTEL NEW QUEENS ROAD KARACHI PAKISTANI OTHER INDIVIDUALS 3,751 10 36 SAFDAR IQBAL PURI S/O MR. M. SHARIF PURI 59-C-2 GULBERG III LAHORE PAKISTANI OTHER INDIVIDUALS 3,716 11 40 NUZHAT JAMILA QAYUM W/O MR. M.A. QAYYUM 229-2A, BLOCK-2 (AL-FATIMA) P.E.C.H. SOCIETY KARACHI-75400 PAKISTANI OTHER INDIVIDUALS 597 12 49 U.B.L. (SYED SIBTE RAZA NAQVI) A/C SYED SIBTE RAZA NAQVI JUBILEE INSURANCE HOUSE I.I. -

RESULT of ENTRANCE TEST for ADMISSION to PRIVATE and PUBLIC SECTOR MEDICAL and DENTAL COLLEGES 2011 ID No

RESULT OF ENTRANCE TEST FOR ADMISSION TO PRIVATE AND PUBLIC SECTOR MEDICAL AND DENTAL COLLEGES 2011 ID No. NAME FATHER NAME MARKS 00001 KARESHMA WALI SHER WALI 116 00002 KASHIF ULLAH HAKEEM KHAN 194 00003 MUHAMMAD NAEEM MUHAMMED ILYAS 88 00004 TAZA GUL JANAN KHAN 394 00005 SHEEMA IQBAL MUHAMMAD IQBAL 30 00006 AMIR JAMAL NOOR JAMAL 73 00007 GOHAR JAMAL NOOR JAMAL 35 00008 RAHEEL ZAMAN SHAH ZAMAN 437 00009 SAMRINA KHAN PROF. DR. AMIR KHAN 189 00010 SIKANDAR IQBAL MUHAMMAD TAHIR 320 00011 MEHRUNISA KHAN KHALIL AURANGZEB KHAN KHALIL 395 00012 KARIM ULLAH SARFARAZ KHAN 244 00013 SUMAYYA SADIQ HAJI SADIQ SHAH 221 00014 SYED SEBGHAT ULLAH SAHIBZADA 123 00015 NAZISH YOUSAF YOUSAF ALI 120 00016 NAILA IJAZ IJAZ HUSSAIN 273 00017 NADIA ZAIB JEHAN ZAIB KHAN 75 00018 MAHREEN GOHAR GOHAR DIN 115 00019 ANAM ULLAH MUZAMMIL KHAN 419 00020 MARIA NIZAM NIZAM UD DIN 360 00021 MUJHAMMAD BASIT MUSHTAQ HUSSAIN 378 00022 UZMA MUSHRAZULLAH 89 00023 IJAZ ULLAH BAKHT SULTAN 27 00024 HAMID KHAN MUHAMMAD AFZAL 367 00025 ANEES KHAN MUHAMMAD KHAN 187 00026 ASIF KAMAL ABDUL MAJEEB 436 00027 ASIF ULLAH FAIZ ULLAH 70 00028 UMAR HAYAT BAKHTAWAR SHAH 429 00029 SHEHZADI UMBREEN EID BADSHAH 232 00030 BILAL AHMAD YAR MUHAMMAD 79 00031 SAMEERA TAJ BAHADAR 202 00032 AMJAD HAMEED ABDUL HAMEED KHAN 20 00033 ZEESHAN KAMIL KHAN 232 00034 NAJMUL ALAM SHAH DAD KHAN 228 00035 ALMAS RANI NABI REHMAT 314 00036 IQRA NAWAZ MUHAMMAD NAWAZ 344 00037 MUHAMMAD ASAD ALI SHAUKAT ALI 218 00038 AYESHA ZAIB JEHANZAIB 424 00039 IZHAR UL HAQ GUL SALAM KHAN 104 00040 MIDRARULLAH KHAN MOHAMMAD ALI -

List of Category -I Members Registered in Membership Drive-Ii

LIST OF CATEGORY -I MEMBERS REGISTERED IN MEMBERSHIP DRIVE-II MEMBERSHIP CGN QUOTA CATEGORY NAME DOB BPS CNIC DESIGNATION PARENT OFFICE DATE MR. DAUD AHMAD OIL AND GAS DEVELOPMENT COMPANY 36772 AUTONOMOUS I 25-May-15 BUTT 01-Apr-56 20 3520279770503 MANAGER LIMITD MR. MUHAMMAD 38295 AUTONOMOUS I 26-Feb-16 SAGHIR 01-Apr-56 20 6110156993503 MANAGER SOP OIL AND GAS DEVELOPMENT CO LTD MR. MALIK 30647 AUTONOMOUS I 22-Jan-16 MUHAMMAD RAEES 01-Apr-57 20 3740518930267 DEPUTY CHIEF MANAGER DESTO DY CHEIF ENGINEER CO- PAKISTAN ATOMIC ENERGY 7543 AUTONOMOUS I 17-Apr-15 MR. SHAUKAT ALI 01-Apr-57 20 6110119081647 ORDINATOR COMMISSION 37349 AUTONOMOUS I 29-Jan-16 MR. ZAFAR IQBAL 01-Apr-58 20 3520222355873 ADD DIREC GENERAL WAPDA MR. MUHAMMA JAVED PAKISTAN BORDCASTING CORPORATION 88713 AUTONOMOUS I 14-Apr-17 KHAN JADOON 01-Apr-59 20 611011917875 CONTRALLER NCAC ISLAMABAD MR. SAIF UR REHMAN 3032 AUTONOMOUS I 07-Jul-15 KHAN 01-Apr-59 20 6110170172167 DIRECTOR GENRAL OVERS PAKISTAN FOUNDATION MR. MUHAMMAD 83637 AUTONOMOUS I 13-May-16 MASOOD UL HASAN 01-Apr-59 20 6110163877113 CHIEF SCIENTIST PROFESSOR PAKISTAN ATOMIC ENERGY COMMISION 60681 AUTONOMOUS I 08-Jun-15 MR. LIAQAT ALI DOLLA 01-Apr-59 20 3520225951143 ADDITIONAL REGISTRAR SECURITY EXCHENGE COMMISSION MR. MUHAMMAD CHIEF ENGINEER / PAKISTAN ATOMIC ENERGY 41706 AUTONOMOUS I 01-Feb-16 LATIF 01-Apr-59 21 6110120193443 DERECTOR TRAINING COMMISSION MR. MUHAMMAD 43584 AUTONOMOUS I 16-Jun-15 JAVED 01-Apr-59 20 3820112585605 DEPUTY CHIEF ENGINEER PAEC WASO MR. SAGHIR UL 36453 AUTONOMOUS I 23-May-15 HASSAN KHAN 01-Apr-59 21 3520227479165 SENOR GENERAL MANAGER M/O PETROLEUM ISLAMABAD MR. -

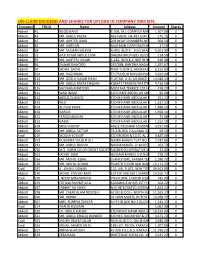

Un-Claim Dividend and Shares for Upload in Company Web Site

UN-CLAIM DIVIDEND AND SHARES FOR UPLOAD IN COMPANY WEB SITE. Company FOLIO Name Address Amount Shares Abbott 41 BILQIS BANO C-306, M.L.COMPLEX MIRZA KHALEEJ1,507.00 BEG ROAD,0 PARSI COLONY KARACHI Abbott 43 MR. ABDUL RAZAK RUFI VIEW, JM-497,FLAT NO-103175.75 JIGGAR MOORADABADI0 ROAD NEAR ALLAMA IQBAL LIBRARY KARACHI-74800 Abbott 47 MR. AKHTER JAMIL 203 INSAF CHAMBERS NEAR PICTURE600.50 HOUSE0 M.A.JINNAH ROAD KARACHI Abbott 62 MR. HAROON RAHEMAN CORPORATION 26 COCHINWALA27.50 0 MARKET KARACHI Abbott 68 MR. SALMAN SALEEM A-450, BLOCK - 3 GULSHAN-E-IQBAL6,503.00 KARACHI.0 Abbott 72 HAJI TAYUB ABDUL LATIF DHEDHI BROTHERS 20/21 GORDHANDAS714.50 MARKET0 KARACHI Abbott 95 MR. AKHTER HUSAIN C-182, BLOCK-C NORTH NAZIMABAD616.00 KARACHI0 Abbott 96 ZAINAB DAWOOD 267/268, BANTWA NAGAR LIAQUATABAD1,397.67 KARACHI-190 267/268, BANTWA NAGAR LIAQUATABAD KARACHI-19 Abbott 97 MOHD. SADIQ FIRST FLOOR 2, MADINA MANZIL6,155.83 RAMTLA ROAD0 ARAMBAG KARACHI Abbott 104 MR. RIAZUDDIN 7/173 DELHI MUSLIM HOUSING4,262.00 SOCIETY SHAHEED-E-MILLAT0 OFF SIRAJUDULLAH ROAD KARACHI. Abbott 126 MR. AZIZUL HASAN KHAN FLAT NO. A-31 ALLIANCE PARADISE14,040.44 APARTMENT0 PHASE-I, II-C/1 NAGAN CHORANGI, NORTH KARACHI KARACHI. Abbott 131 MR. ABDUL RAZAK HASSAN KISMAT TRADERS THATTAI COMPOUND4,716.50 KARACHI-74000.0 Abbott 135 SAYVARA KHATOON MUSTAFA TERRECE 1ST FLOOR BEHIND778.27 TOOSO0 SNACK BAR BAHADURABAD KARACHI. Abbott 141 WASI IMAM C/O HANIF ABDULLAH MOTIWALA95.00 MUSTUFA0 TERRECE IST FLOOR BEHIND UBL BAHUDARABAD BRANCH BAHEDURABAD KARACHI Abbott 142 ABDUL QUDDOS C/O M HANIF ABDULLAH MOTIWALA252.22 MUSTUFA0 TERRECE 1ST FLOOR BEHIND UBL BAHEDURABAD BRANCH BAHDURABAD KARACHI. -

Women-Empowerment a Bibliography

Women’s Studies Resources; 5 Women-Empowerment A Bibliography Complied by Meena Usmani & Akhlaq Ahmed March 2015 CENTRE FOR WOMEN’S DEVELOPMENT STUDIES 25, Bhai Vir Singh Marg (Gole Market) New Delhi-110 001 Ph. 91-11-32226930, 322266931 E-mail: [email protected] Website: www.cwds.ac.in/library/library.htm 1 PREFACE The “Women’s Studies Resources Series” is an attempt to highlight the various aspect of our specialized library collection relating to women and development studies. The documents available in the library are in the forms of books and monographs, reports, reprints, conferences Papers/ proceedings, journals/ newsletters and newspaper clippings. The present bibliography on "Women-Empowerment ” especially focuses on women’s political, social or economic aspects. It covers the documents which have empowerment in the title. To highlight these aspects, terms have been categorically given in the Subject Keywords Index. The bibliography covers the documents upto 2014 and contains a total of 1541 entries. It is divided into two parts. The first part contains 800 entries from books, analytics (chapters from the edited books), reports and institutional papers while second part contains over 741 entries from periodicals and newspapers articles. The list of periodicals both Indian and foreign is given as Appendix I. The entries are arranged alphabetically under personal author, corporate body and title as the case may be. For easy and quick retrieval three indexes viz. Author Index containing personal and institutional names, Subject Keywords Index and Geographical Area Index have been provided at the end. We would like to acknowledge the support of our colleagues at Library. -

Study of Sexually Transmitted Infections Among Urban Men in Pakistan: Identifying the Bridging Population

Population Council Knowledge Commons Reproductive Health Social and Behavioral Science Research (SBSR) 2008 Study of sexually transmitted infections among urban men in Pakistan: Identifying the bridging population Ali M. Mir Laura Reichenbach Population Council Abdul Wajid Population Council Mumraiz Khan Population Council Follow this and additional works at: https://knowledgecommons.popcouncil.org/departments_sbsr-rh Part of the Demography, Population, and Ecology Commons, Family, Life Course, and Society Commons, Gender and Sexuality Commons, International Public Health Commons, Maternal and Child Health Commons, Medicine and Health Commons, and the Women's Health Commons How does access to this work benefit ou?y Let us know! Recommended Citation Mir, Ali M., Laura Reichenbach, Abdul Wajid, and Mumraiz Khan. 2008. "Study of sexually transmitted infections among urban men in Pakistan: Identifying the bridging population." Islamabad: Population Council. This Report is brought to you for free and open access by the Population Council. Study of Sexually Transmitted Infections Among Urban Men in Pakistan: Identifying the Bridging Population Ali M. Mir Laura Reichenbach Abdul Wajid Mumraiz Khan Commissioned by Conducted by National AIDS Control Programme Ministry of Health - Government of Pakistan Sponsored by The Population Council, an international, nonprofit, nongovernmental organization established in 1952, seeks to improve the well being and reproductive health of current and future generations around the world and to help achieve a -

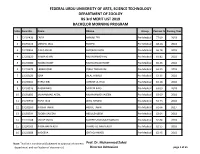

FEDERAL URDU UNIVERSITY of ARTS, SCIENCE TECHNOLOGY DEPARTMENT of ZOOLOY BS 3Rd MERIT LIST 2019 BACHELOR MORNING PROGRAM

FEDERAL URDU UNIVERSITY OF ARTS, SCIENCE TECHNOLOGY DEPARTMENT OF ZOOLOY BS 3rd MERIT LIST 2019 BACHELOR MORNING PROGRAM S.No. Form No. Name FName Group Percent % Passing Year 1 13192436 FAIZA ANWAR ZEB Pre-Medical 77.09 2018 2 23191142 MIRCHU MAL ROOPO Pre-Medical 68.18 2018 3 13190853 AISHA KHAN MAQBALI KHAN Pre-Medical 66.18 2018 4 13192820 NIMRA KHAN MUHAMMAD FIAZ Pre-Medical 65.82 2018 5 13193080 TOOBA HANIF MUHAMMAD HANIF Pre-Medical 65.36 2018 6 13193679 LARAB IQBAL IQBAL TABASSUM Pre-Medical 63.55 2018 7 13192626 IQRA JALAL AHMED Pre-Medical 63.36 2018 8 23190651 HAFSA BIBI ANWAR UL HAQ Pre-Medical 63.18 2018 9 23193516 AHSAN BAIG SALEEM BAIG Pre-Medical 63.00 2018 10 13191895 MUHAMMAD AFZAL MUHAMMAD YASEEN Pre-Medical 63.00 2018 11 13190550 RAFIA NAZ WASI AHMED Pre-Medical 62.73 2018 12 23192200 ARISHA TAHIR ABDUL TAHIR Pre-Medical 62.64 2017 13 13192334 TOOBA SALEEM ABDULSALEEM Pre-Medical 62.64 2018 14 23191948 SADAF SADIQ MAHER SADIQ MUHAMMAD Pre-Medical 62.64 2018 15 23190563 ARIBA ARFIN ALVI SHAMS-UL-ARFIN ALVI Pre-Medical 62.55 2018 16 13192688 NADEEYA ISHTAQ AHMED Pre-Medical 62.45 2018 Note: This list is conditional (Subjected to approval of concern Prof. Dr. Muhammad Zahid department and verification of documents). Director Admission page 1 of 55 FEDERAL URDU UNIVERSITY OF ARTS, SCIENCE TECHNOLOGY DEPARTMENT OF ZOOLOY BS 3rd MERIT LIST 2019 BACHELOR MORNING PROGRAM S.No. Form No. Name FName Group Percent % Passing Year 17 13191846 ONEEBA AKRAM MUHAMMAD AKRAM Pre-Medical 62.36 2018 18 23193363 SYEDA ALIZA NAQVI SYED ZAHANAT -

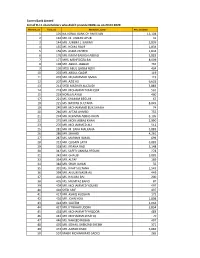

Soneri Bank Limted List of D-11 Shareholders Who Didn't Provide

Soneri Bank Limted List of D-11 shareholders who didn't provide IBANs as on 20.04.2020 Warrant_no Folio_no Memeber_name Net_dividend 1 101NATIONAL BANK OF PAKISTAN 13,104 2 140MR. M. USMAN AYUB 31 3 144MR. JUMMA J. KARIMI 3,839 4 155MS. HOMA RAUF 1,834 5 156MS. ASMA ZAHEER 1,834 6 176MR. IMAM BAKHSH ABBASI 3,883 7 177MRS. MEHFOOZA BAI 8,009 8 198MR. ABDUL JABBAR 765 9 199SYED ABUL QASIM RIZVI 404 10 202MR. ABDUL QADIR 119 11 203MR. MUHAMMAD ISMAIL 119 12 207MR. AZIZ ALI 6,628 13 214SYED MAZHAR ALI ZAIDI 3,883 14 218MR. MOHAMMED RAFIQUE 565 15 219NOREEN AYUB 480 17 221MS. SHAMIM BEGUM 67 18 225MS. NAYYAR SULTANA 8,049 19 240MR. MOHAMMAD BUX SHAIKH 74 20 246MR. AFTAB AHMED 755 21 274MR. REHMAN ABBAS KHAN 3,105 22 275MR. MOIN ABBAS KHAN 2,990 23 276MR. MOHAMMED ALI 512 25 281MR. M. ZAKA MALKANA 3,883 26 286MR. SHAHID 4,261 27 287MS. MARIAM ISMAIL 699 28 313MR. QUSAIN LATIF 3,883 29 328MS. IRFANA RAZI 5,148 30 342MS. SAEED UNNISA BEGUM 278 31 343MR. GHALIB 3,883 33 354MR. ALTAF 169 34 384MR. SHAH JAHAN 56 35 391MS. IFFAT SULTANA 1,543 36 399MR. ANJUM NASIR ALI 449 37 401MS. HALIMA BAI 200 38 405MS. MUMTAZ BANO 87 39 409MR. MOHAMMED YOUNIS 497 40 410SYED ARIF 497 41 417MR. ASHIQ HUSSAIN 172 42 420MR. JOHN HOU 1,808 43 424MR. SALEEM 1,064 44 427MR. IFTIKHAR UDDIN 3,854 45 438MR. MOHAMMED YAQOOB 483 46 443MR. -

PMAS-Arid Agriculture University Rawalpindi

Pir Mehr Ali Shah ARID AGRICULTURE UNIVERSITY RAWALPINDI OFFICE OF THE SENIOR TUTOR Tutorial Group : A - 1 Name of Tutor : Dr. Abid Riaz Assistant Professor, Plant Pathology Reg. No. Name Faculty Semester Ateeq Ur Rehman FAE 1st 13-arid-790 Sajeel Saleem FAE AAMINAH TARIQ FC&FS 1st 13-ARID-262 AAMIR SOHAIL FC&FS 11-ARID-349 Abdul Haleem FC&FS ABDUL HAMEED FC&FS 1st 13-ARID-263 ABDUL HANAN FC&FS ABDUL HASEEB KHAN FC&FS 1st ABDUL MAJI FC&FS 1st ABD-UL-QADIR FC&FS 1st 12-ARID-207 FIZA BATOOL FC&FS 12-ARID-211 HAFSA ANWAR FC&FS 11-ARID-250 Hira Mahfooz FC&FS 12-ARID-249 MUHAMMAD HASNAT AQIB FC&FS 11-ARID-288 Muhammad Rizwan FC&FS 11-ARID-307 Sadia Batool FC&FS Abdullah Mujahid FFRM 1st 13-ARID-2434 MUHAMMAD FARRUKH IQBAL FFRM 10-ARID-836 Aamir Nawab FVAS 11-ARID-106 Farooq Ahsan FVAS 12-arid-590 Ibrar Faisal FVAS 12-arid-612 Muhammad Shahid FVAS 12-ARID-2492 NAIMA RAZZAQI FVAS Zeeshan Ejaz FVAS 1st 13-ARID-3195 ABBAS ALI Sciences 11-ARID-1019 Ayesha Mazhar Sciences (Microbiology) HALEEMA NOUREEN Sciences 1st (Biochemistry) HALEEMA TARIQ Sciences 1st 12-ARID-2512 RABIA ASHRAF Sciences (Economics) SIDRA KHAN Sciences 1st 12-ARID-2515 YOUSRA AFZAL Sciences 13-ARID-645 AAMIR FAIZ UIIT BSCS AASHIR RAZA UIIT 1st BSCS ABDUL MAJID UIIT 1st 13-ARID-651 ABDUR RAFEY UIIT 10-ARID-174 Adeel Ahmed UIIT BSIT ADEEL IFTIKHAR UIIT 1st BSIT ADEEL REGINALD UIIT 1st 13-ARID-661 ANUM BATOOL UIIT 12-ARID-1801 ATTAUR REHMAN UIIT 08-ARID-417 Atta-Ur-Rehman UIIT 09-ARID-503 Awais Tanveer UIIT 12-ARID-2094 BILAWAL BASHIR UIIT 12-ARID-1817 HAMMAD HASSAN UIIT 11-ARID-771 Imran Ali UIIT 10-arid-204 M.