Infrastructure Investments Fund

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sonnedix Scholars

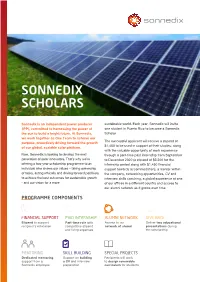

SONNEDIX SCHOLARS Sonnedix is an independent power producer sustainable world. Each year, Sonnedix will invite (IPP), committed to harnessing the power of one student in Puerto Rico to become a Sonnedix the sun to build a bright future. At Sonnedix, Scholar. we work together as One Team to achieve our The successful applicant will receive a stipend of purpose, proactively driving forward the growth $1,450 to be used in support of their studies, along of our global, scalable solar platform. with the valuable opportunity of work experience Now, Sonnedix is looking to develop the next through a part-time paid internship from September generation of solar innovators. That’s why we’re to December 2020 (a stipend of $3,500 for the offering a two-year scholarship programme to an internship period along with $1,450 financial individual who shares our values – taking ownership support towards accommodation), a mentor within of tasks, acting ethically and driving forward positively the company, networking opportunities, CV and to achieve the best outcomes for sustainable growth interview skills coaching, a global experience at one - and our vision for a more of our offices in a different country and access to our alumni network as it grows over time. PROGRAMME COMPONENTS FINANCIAL SUPPORT PAID INTERNSHIP ALUMNI NETWORK GIVE BACK Stipend to support Part-time role with Access to our Deliver two educational recipient's education competitive stipend network of alumni presentations during and living expenses the scholarship MENTORING SKILL BUILDING SPECIAL PROJECTS Dedicated mentoring Support on building Recipients will work support from a a CV and interview to design renewable Sonnedix employee preparation curriculum for students HOW TO APPLY Sonnedix Scholars are the solar innovators of the future; when they see problems, they are driven to find solutions. -

Top 70 European Solar Pv Portfolios Provided by Solarplaza International Bv

TOP 70 EUROPEAN SOLAR PV PORTFOLIOS PROVIDED BY SOLARPLAZA INTERNATIONAL BV Aquila Capital‘s track record in photovoltaics 477 4th 22 MWp total capacity place out of 70 European transactions Solar PV Portfolios since 2009 Size 2015 Size 2014 Name (MWp) (MWp) Role HQ 1 Lightsource Renewable Energy 942.7 608.4 Developer/Owner UK 2 Enerparc AG 749.0 700.0 IPP, Investor Germany 3 EDF Energies Nouvelles 575.6 656.5 Utility France 4 Aquila Capital 477.7 355.5 Investor Germany 5 Foresight Group 404.5 206.0 Investor, Fund, Asset Manager UK 6 Capital Stage AG 391.7 339.5 IPP, Investor Germany 7 KGAL 373.0 335.4 IPP, Investor Germany 8 RTR Energy 318.0 318.0 IPP Italy 9 Bluefield Solar Income Fund Ltd 262.5 158.0 Investor UK 10 Wattner 232.8 230.3 Owner/Developer Germany 11 Renewable Energy Capital Partners 232.4 232.4 Asset Manager Germany 12 Enel Green Power 221.0 221.0 Utility Italy 13 NextEnergy Solar Fund 217.0 NEW Investor UK 14 Silver Ridge Power 212.3 212.3 Utility USA 15 Glennmont Partners 186.0 168.0 Investor UK 16 Low Carbon 177.3 198.9 Investor UK 17 Primrose Solar 173.7 126.2 Investor UK 18 T-Solar Group Global Operating Assets 168.0 167.7 IPP Spain 19 Fotowatio (FSL) 147.0 147.0 Owner Spain 20 Allianz Renewable Energy Fund 135.7 NEW Investor Germany 21 SUSI Partners AG 126.5 116.2 Investor Switzerland 22 Infrared Capital Partners 126.2 119.0 Investor UK 23 CEZ Group 125.1 NEW Utility Czech Republic 24 The Renewables Infrastructure Group (TRIG) 119.0 62.5 Investor Guernsey 25 Hazel Capital LLP 111.0 80.0 Investor/Developer UK 26 Quadran 107.0 82.0 IPP France 27 Voigt & Collegen 102.2 71.4 Investor Germany 28 Solarig Group 101.8 31.7 IPP Spain 29 Akuo Energy 98.7 119.3 IPP France 30 Diamond Generating Europe 95.0 94.0 IPP UK 31 Quercus Asset Selection 94.7 NEW Investor Luxembourg 32 Origis Energy 82.6 77.2 Owner Belgium 33 Sonnedix 77.6 73.4 IPP France 34 Antin Solar Investments 77.0 77.0 Investor France 35 DIF 75.2 171.1 Investor Netherlands Source: The „Top 70 overview of European solar PV portfolios“ is provided by Solarplaza International BV („Solarplaza“). -

The Global Solar Independent Power Producer (Ipp) Market Who We Are Leader 01 05 in Esg

THE GLOBAL SOLAR INDEPENDENT POWER PRODUCER (IPP) MARKET WHO WE ARE LEADER 01 05 IN ESG SONNEDIX WHAT WE DO 02 06 HISTORY CONTENT A GROWING GLOBAL OUR TEAM 03 PLATFORM 07 ENVIRONMENTAL, SOCIAL AND OUR OFFICES 04 GOVERNANCE (ESG) 08 WHO WE ARE We are a leading global solar Independent Power Producer (IPP) with a proven track record in delivering high-performance, cost-competitive solar photovoltaic plants to the market. The Sonnedix Group is majority owned by institutional investors advised by J.P. Morgan Asset Management. A Shared Purpose: to harness the power of the sun to build a bright future. Solar energy’s potential to transform daily life drives and inspires us to build solar plants that endure, using the most current technologies available and working with partners that share our commitment to producing a continuous, reliable and efficient supply of clean energy from the sun. A Social Citizen, playing an active role in 0the Energy Transition. We are constantly evaluating multiple regulatory regimes at different phases of integration in the rapidly-expanding global solar market to uncover new opportunities to revolutionise the energy industry. A diverse and inclusive workplace. At Sonnedix, everyone knows and feels they belong. We listen to one another, educate ourselves and those around us, and implementing changes to become a THE FUTURE IS SOLAR AND truly diverse and inclusive organization. WE’RE DOING EVERYTHING IN OUR POWER TO GET THERE SOONER 1 Sonnedix Oita 38MW, Japan WHAT WE DO Sonnedix concentrates its value add in the development, construction, production and sale of PV electricity. -

Directors' Report and Additional Disclosures

Directors’ report and additional disclosures The Directors present their report on the affairs Powers of the Directors Share capital of the Group, together with the audited The Directors are responsible for the As at 31 March 2019, the Company’s issued financial statements and the report of the management of the business of the Company share capital was 1,213,878,659 ordinary auditor for the year ended 31 March 2019. and may exercise all powers of the Company shares of 5 pence, each credited as fully paid. Information required to be disclosed in the subject to applicable legislation and regulation The Company holds 157,229 ordinary shares Directors’ report may be found below and in and the Company’s Articles. in treasury, and the issued share capital of the the following sections of the Annual Report Directors’ indemnities Company which carries voting rights of one and Accounts, in accordance with the and liability insurance vote per share comprises 1,213,721,430 Companies Act 2006 (the ‘2006 Act’) and FirstGroup maintains liability insurance for its ordinary shares. Listing Rule 9.8.4R of the Financial Conduct Directors and Officers. The Company has also Further details of the Company’s issued share Authority (the ‘FCA’): granted indemnities to each of the Directors capital are shown in note 27 to the Company’s Information Section Page as well as the General Counsel & Company financial statements. Secretary, the Director of Finance, the Group Sustainability Corporate 59 Financial Controller, the Group Treasury & Tax The Company’s shares are listed on the governance Governance Director, the Chief Information Officer, the London Stock Exchange. -

Matching Gifts Program

Hundreds of companies have matched gifts to French American and International. WILL YOURS? Make Your Contributions Go Further! This is just a partial list of companies who will match your philanthropic contributions (and sometimes volunteer hours!) to our school. We encourage you to check with your company’s personnel department to find out the specifics of their matching gifts program. If you have questions or need assistance, please contact Monica Hernandez, Advancement Services Associate, at 415-558-2015. Aluminum Co. of America Arbella Mutual Insurance Co. Barnett Associates, Inc. A AMAX, Inc. Archer Daniels Midland Barnett Banks, Inc. Abbott Laboratories Fnd. AMBAC Ares Advanced Technology Barrett Technology/Barrett Abcor, Inc. Amcast Industrial Corp. Argonaut Group, Inc. Design, Inc. Abstract Models, Inc. Amerada Hess Corp. Argus Research Laboratories Barry Wright Corp. Access Energy Corp. American Brands, Inc. Aristech Chemical Corp. The Barton-Gillet Co. ACF Industries, Inc. American Cyanamid Co. Arkwright Mutual Ins. Co. BASF Corp. A-Copy Inc. American Electric Power Co. Armco., Inc. BATUS Inc. Acorn Structures Inc American Express Co. Armstrong World Industries Baupost Group, Inc. Acuson Corp. American Express Financial Armtek Corp. Bay Networks, Inc. A-D Electronics, Inc. Advisors Arrow Electronics, Inc. Bayer Corporation Adams, Harkness & Hill, Inc. American General Corp. Art Technology Group Beatrice Companies, Inc. ADC Foundation American International Group Arthur Andersen & Co., SC Bechtel Power Corp. Add, Inc. American Medical International Arthur J. Gallagher Foundation Becor Western, Inc. Addison-Wesley Publishing Co. American National Bank Ashland Oil, Inc. Becton Dickinson and Co. Adobe Systems Inc. American National Can Co. Aspect Telecommunications Beech Aircraft Corp. -

The Global Solar Independent Power Producer (Ipp) Market Who We Are Leader 01 05 in Esg

THE GLOBAL SOLAR INDEPENDENT POWER PRODUCER (IPP) MARKET WHO WE ARE LEADER 01 05 IN ESG SONNEDIX WHAT WE DO 02 06 HISTORY CONTENT A GROWING GLOBAL OUR TEAM 03 PLATFORM 07 ENVIRONMENTAL, SOCIAL AND OUR OFFICES 04 GOVERNANCE (ESG) 08 WHO WE ARE We are a leading global solar Independent Power Producer (IPP) with a proven track record in delivering high-performance, cost-competitive solar photovoltaic plants to the market. The Sonnedix Group is majority owned by institutional investors advised by J.P. Morgan Asset Management. A Shared Purpose: to harness the power of the sun to build a bright future. Solar energy’s potential to transform daily life drives and inspires us to build solar plants that endure, using the most current technologies available and working with partners that share our commitment to producing a continuous, reliable and efficient supply of clean energy from the sun. A Social Citizen, playing an active role in 0the Energy Transition. We are constantly evaluating multiple regulatory regimes at different phases of integration in the rapidly-expanding global solar market to uncover new opportunities to revolutionise the energy industry. A diverse and inclusive workplace. At Sonnedix, everyone knows and feels they belong. We listen to one another, educate ourselves and those around us, and implementing changes to become a THE FUTURE IS SOLAR AND truly diverse and inclusive organization. WE’RE DOING EVERYTHING IN OUR POWER TO GET THERE SOONER 1 Sonnedix Oita 38MW, Japan WHAT WE DO Sonnedix concentrates its value add in the development, construction, production and sale of PV electricity. -

2 FEBRUARY 2017 Grange City Hotel, London, UK

31 JANUARY - 2 FEBRUARY 2017 Grange City Hotel, London, UK POST-EVENT REPORT 2017 Delegate profiles | Testimonials | Feedback finance.solarenergyevents.com #SFIEurope 1 Perfect opportunities to network, made all the desired contacts Delegate Profiles Nicolas Vierge, Dong Energy Breakdown by country 139% United Kingdom 21% Germany 16% Spain 7% Italy 6% Ireland Job Titles: 5% Turkey 5% Denmark 4% France 4% Egypt 4% Netherlands 4% United States 3% Switzerland 3% Greece 2% China 2% India 2% Hong Kong 2% Portugal 2% Israel This conference always 1% Jordan draws a crowd and has 1% Belgium become a must for my 1% Saudi Arabia calendar to catch up with 1% Norway key people and trends for 1% Austria the year ahead 1% New Zealand Louise Wilson, 1% Czech Republic Abundance Investment 3 Delegate Profiles Company Activity 38.2% Finance 14.3% Developer 14.3% 8.4% O&M 8.4% 8% Manufacturer 8% 4.6% Consultancy 4.6% Good networking opportunity Energy Management 4.6% 4.6% Mark Weller, Eneco UK Ltd 3.8% EPC 3.8% 3.8% Other 3.8% Yet again a great event getting together all the major players 3.4% Legal 3.4% in the industry and proper honest discussion as to how Utilities 3.4% 3.4% solar can survive and adapt in the ever changing environment 2.9% PR/Media/Partnerships 2.9% and also giving a high level 2.5% Independent Power Producer 2.5% overview of overseas markets and the advent of storage 2.1% Large Energy User 2.1% Stuart Cleak, Foot Anstey 4 A great meeting place to understand what is going on in the solar space in Europe for asset owners, investors, financiers and service providers. -

Jinkosolar Supplies METKA-EGN with 57.65 MW of PV Modules for Puerto Rico's Largest PV Plant

JinkoSolar Supplies METKA-EGN with 57.65 MW of PV Modules for Puerto Rico's Largest PV Plant April 1, 2016 SHANGHAI, April 1, 2016 /PRNewswire/ -- JinkoSolar Holding Co., Ltd. ("JinkoSolar" or the "Company") (NYSE: JKS), a global leader in the solar PV industry, today announced that it will supply METKA-EGN USA LLC ("METKA-EGN ") with 57.65 MW of PV solar modules for the largest solar PV plant in Puerto Rico. JinkoSolar will deliver the 57.65 MW of PV solar modules for the project located in the municipality of Isabela, Puerto Rico. The Owner of the project is Oriana LLC, a subsidiary of Sonnedix USA Limited, and a member of the Sonnedix group of companies. JinkoSolar has collaborated with METKA-EGN on several different projects in various markets across the globe. "METKA-EGN is one of our most important European EPC clients and we are very happy to expand our partnership into other growth regions of the world. Global strategic partnerships like this one with METKA-EGN, one of the leading EPC players in the world, forms a cornerstone of JinkoSolar's global success story", said Mr. Frank Niendorf, General Manager JinkoSolar Europe. "METKA-EGN is pleased to collaborate with JinkoSolar on the completion of the largest solar PV project in Puerto Rico. We look forward to cooperating with JinkoSolar's professional and dedicated team again on future projects," commented Mr. Nikos Papapetrou, CEO of METKA-EGN. About JinkoSolar Holding Co., Ltd. JinkoSolar (NYSE: JKS) is a global leader in the solar industry. JinkoSolar distributes its solar products and sells its solutions and services to a diversified international utility, commercial and residential customer base in China, the United States, Japan, Germany, the United Kingdom, Chile, South Africa, India, Mexico, Brazil, the United Arab Emirates, Italy, Spain, France, Belgium, and other countries and regions. -

List of Participating Merchants Mastercard Automatic Billing Updater

List of Participating Merchants MasterCard Automatic Billing Updater 3801 Agoura Fitness 1835-180 MAIN STREET SUIT 247 Sports 5378 FAMILY FITNESS FREE 1870 AF Gilroy 2570 AF MAPLEWOOD SIMARD LIMITED 1881 AF Morgan Hill 2576 FITNESS PREMIER Mant (BISL) AUTO & GEN REC 190-Sovereign Society 2596 Fitness Premier Beec 794 FAMILY FITNESS N M 1931 AF Little Canada 2597 FITNESS PREMIER BOUR 5623 AF Purcellville 1935 POWERHOUSE FITNESS 2621 AF INDIANAPOLIS 1 BLOC LLC 195-Boom & Bust 2635 FAST FITNESS BOOTCAM 1&1 INTERNET INC 197-Strategic Investment 2697 Family Fitness Holla 1&1 Internet limited 1981 AF Stillwater 2700 Phoenix Performance 100K Portfolio 2 Buck TV 2706 AF POOLER GEORGIA 1106 NSFit Chico 2 Buck TV Internet 2707 AF WHITEMARSH ISLAND 121 LIMITED 2 Min Miracle 2709 AF 50 BERWICK BLVD 123 MONEY LIMITED 2009 Family Fitness Spart 2711 FAST FIT BOOTCAMP ED 123HJEMMESIDE APS 2010 Family Fitness Plain 2834 FITNESS PREMIER LOWE 125-Bonner & Partners Fam 2-10 HBW WARRANTY OF CALI 2864 ECLIPSE FITNESS 1288 SlimSpa Diet 2-10 HOLDCO, INC. 2865 Family Fitness Stand 141 The Open Gym 2-10 HOME BUYERS WARRRANT 2CHECKOUT.COM 142B kit merchant 21ST CENTURY INS&FINANCE 300-Oxford Club 147 AF Mendota 2348 AF Alexandria 3012 AF NICHOLASVILLE 1486 Push 2 Crossfit 2369 Olympus 365 3026 Family Fitness Alpin 1496 CKO KICKBOXING 2382 Sequence Fitness PCB 303-Wall Street Daily 1535 KFIT BOOTCAMP 2389730 ONTARIO INC 3045 AF GALLATIN 1539 Family Fitness Norto 2390 Family Fitness Apple 304-Money Map Press 1540 Family Fitness Plain 24 Assistance CAN/US 3171 AF -

Comprehensive Economic Development Strategy (Ceds) 1

COMPREHENSIVE ECONOMIC DEVELOPMENT STRATEGY (CEDS) 1. COMPETITIVE ASSESSMENT 2. TARGET BUSINESS REVIEW 3. STRATEGIC PLAN 4. IMPLEMENTATION PLAN INDIANAPOLIS REGION, INDIANA September 2015 TABLE OF CONTENTS Project Overview ................................................................................................................................................................................................... 1 Steering Committee ............................................................................................................................................................................................. 2 1. Competitive Assessment .......................................................................................................................................................... 4 The Indianapolis Identity: Dilemma and Dichotomy .................................................................................................................... 6 Growth within the Indianapolis Region: a Reemerging Core.................................................................................................... 8 Workforce Sustainability: Attracting and Retaining Talent ...................................................................................................... 13 Workforce Sustainability: Developing “Homegrown” Talent .................................................................................................. 19 Education & Incomes: Consequences of Slow Improvement ................................................................................................ -

Jinkosolar Powers the Miami Science Barge

JinkoSolar Powers the Miami Science Barge August 4, 2016 SHANGHAI, Aug. 4, 2016 /PRNewswire/ -- JinkoSolar Holding Co., Ltd. ("JinkoSolar" or the "Company") (NYSE: JKS), a global leader in the solar PV industry, today announced that it has donated 16.9 kilowatts (kW) of PV modules for the construction of the Miami Science Barge ("Barge"), a floating marine lab and environmental education center in Miami, Florida. The Miami Science Barge, a 3,600 square foot barge docked in the Museum Park in Biscayne Bay, was designed to focus on STEM (Science, Technology, Engineering, and Mathematics) education and sustainability initiatives. It features three interconnecting zones which will educate visitors on a number of topics including living ecosystems, marine experiments, and renewable energy. JinkoSolar's high-efficiency modules will be powering the Barge, allowing it to function completely off the grid. Aboard the Barge there will be around 75 kWh of storage, enough for a total of 3 days' worth of stored energy. There will be a cost savings of over $1,000 per year, which will be used towards ensuring that the Barge's programs can be provided free to those with limited financial means. Sonnedix USA Services Limited, a member of the Sonnedix Group of Companies (collectively, "Sonnedix"), donated the solar inverters, provided engineering support, and coordinated the donation of energy storage equipment from Pittsburgh, PA based Aquion Energy. Andreas Mustad, Director and CEO of the Sonnedix Group of companies, said: "Spurring an interest in Miami's youth regarding how easily a self-sustaining platform can be implemented on even a limited footprint such as the science barge leaving ample room for the activities aboard is something we are extremely proud to be a part of and one of several corporate social responsibility initiatives we are committed to supporting globally." "The Miami Science Barge embodies sustainability and solar panels are a critical part of our identity. -

Modern Slavery Statement 2019

Modern Slavery Statement 2019 This statement is published by Sonnedix Power Holdings Limited, on behalf of its subsidiary Sonnedix UK Services Limited, pursuant to section 54 of the UK Modern Slavery Act. It sets out the steps taken by Sonnedix Power Holdings Limited and its subsidiaries (collectively “Sonnedix”) during the financial year 2019 to prevent and eradicate forced labour and human trafficking in Sonnedix’s global operations and supply chains. Our Business Sonnedix is an established Independent Power Producer (IPP) with a proven track record of successfully designing, financing, building and monitoring high-performance, cost-competitive solar plants around the world. At the close of 2019, the Sonnedix corporate structure included multiple entities in and approximately 250 employees across Chile, the United States of America, Puerto Rico, France, Spain, Italy, South Africa and the United Kingdom. Sonnedix had a controlled capacity of 1,856 MW of which 958 MW were operational/mechanically complete, 428 MW were under construction, and a further 470 MW were under documentation. The majority of Sonnedix employees are office or project based, as a result the key risk area for modern slavery is within the procurement and supply chain activities undertaken through a limited number of global partners and suppliers. Our Policies Integrating responsible, forward-thinking corporate policies into our daily business practices is key to us achieving our goal of smartly transforming the sun’s power into clean energy. It’s what allows Sonnedix to behave sustainably, ethically and accountably as we develop, finance, build and operate solar plants around the world. It’s also what ensures that Sonnedix have a positive impact on our people and the environments and communities within which we work.