Population, Housing, Economy and Spatial

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Address of Estate Offices Under Hong Kong Housing Authority and Hong Kong Housing Authority Customer Service Centre

香港房屋委員會轄下屋邨辦事處及香港房屋委員會客務中心地址 Address of Estate Offices under Hong Kong Housing Authority and Hong Kong Housing Authority Customer Service Centre 辦事處名稱 Name of Office 地址 Address 香港房屋委員會客務 Hong Kong Housing 九龍橫頭磡南道3號 3 Wang Tau Hom South Road, 中心 Authority Customer Kowloon Service Centre 鴨脷洲邨辦事處 Ap Lei Chau Estate 香港鴨脷洲邨利滿樓(高座)地下24- No. 24-31, G/F, Lei Moon House Office 31號 (High Block), Ap Lei Chau Estate, Hong Kong 蝴蝶邨辦事處 Butterfly Estate Office 屯門蝴蝶邨蝶聚樓地下 G/F, Tip Chui House, Butterfly Estate, Tuen Mun 柴灣邨物業服務辦事 Chai Wan Estate Property 柴灣柴灣邨灣畔樓地下 G/F, Wan Poon House, Chai Wan 處 Services Management Estate, Chai Wan Office 澤安邨辦事處 Chak On Estate Office 深水埗澤安邨華澤樓地下17A-24號 Unit 17A-24, G/F, Wah Chak House, Chak On Estate, Sham Shui Po 長青邨物業服務辦事 Cheung Ching Estate 青衣長青邨青槐樓地下20-29號 Unit 20-29, G/F, Ching Wai House, 處 Property Services Cheung Ching Estate, Tsing Yi Management Office 長亨邨物業服務辦事 Cheung Hang Estate 青衣長亨邨亨麗樓地下1-8號 Unit 1-8, G/F, Hang Lai House, 處 Property Services Chueng Hang Estate, Tsing Yi Management Office 長康邨辦事處 Cheung Hong Estate 青衣長康邨康平樓地下 G/F, Hong Ping House, Cheung Hong Office Estate, Tsing Yi 長貴邨物業服務辦事 Cheung Kwai Estate 長洲長貴邨長旺樓101-102號 Unit 101-102, Cheung Wong House, 處 Property Services Cheung Kwai Estate, Cheung Chau Management Office 祥龍圍邨物業服務辦 Cheung Lung Wai Estate 上水祥龍圍邨景祥樓地下 G/F, King Cheung House, Cheung 事處 Property Services Lung Wai Estate, Sheung Shui Management Office 長沙灣邨物業服務辦 Cheung Sha Wan Estate 深水埗長沙灣邨長泰樓一樓 1/F, Cheung Tai House, Cheung Sha 事處 Property Services Wan Estate, Sham Shui Po Management Office -

S-K14S-21 TPB Paper 10409

TPB Paper No. 10409 For Consideration by the Town Planning Board on 23.3.2018 DRAFT KWUN TONG (SOUTH) OUTLINE ZONING PLAN NO. S/K14S/21 INFORMATION NOTE AND HEARING ARRANGEMENT FOR CONSIDERATION OF REPRESENTATIONS AND COMMENTS 1. Introduction 1.1 On 3.11.2017, the draft Kwun Tong (South) Outline Zoning Plan No. S/K14S/21 (the Plan) was exhibited for public inspection under section 5 of the Town Planning Ordinance (the Ordinance). The amendments mainly involve rezoning of a site at Ting On Street, Ngau Tau Kok (the Site) from “Government, Institution or Community” to “Residential (Group A)3” and stipulation of building height restriction (Item A), as well as amendments to the Notes of the Plan. The amendment is to facilitate a proposed public housing development at the Site by the Hong Kong Housing Society (HKHS), which will serve as a decanting site for redevelopment of the adjacent Kwun Tong Garden Estate Phase II (Garden Estate II). The Schedule of Amendments setting out the amendments incorporated into the Plan is at Annex I and the location of the amendment item is shown on Plan P-1. 1.2 During the two-month exhibition period, a total of 104 representations were received. On 26.1.2018, the representations were published for three weeks for public comments. Upon expiry of the public inspection period on 20.2.2018, five comments were received. The list of representers and commenters and the summaries of representations and comments are shown in Annexes II, III, IV and V respectively for Members’ reference. The location of the representation site is the same as Item A as shown on Plan P-1. -

Address of Estate Offices Under Hong Kong Housing Authority and Hong

香港房屋委員會轄下屋邨辦事處及香港房屋委員會客務中心地址 Address of Estate Offices under Hong Kong Housing Authority and Hong Kong Housing Authority Customer Service Centre 辦事處名稱 地址 Name of Office Address Hong Kong Housing Authority 香港房屋委員會客務中心 九龍橫頭磡南道3號 3 Wang Tau Hom South Road, Kowloon Customer Service Centre No. 24-31, G/F, Lei Moon House (High Block), 鴨脷洲邨辦事處 Ap Lei Chau Estate Office 香港鴨脷洲邨利滿樓(高座)地下24-31號 Ap Lei Chau Estate, Hong Kong 蝴蝶邨辦事處 Butterfly Estate Office 屯門蝴蝶邨蝶聚樓地下 G/F, Tip Chui House, Butterfly Estate, Tuen Mun Chai Wan Estate Property Services 柴灣邨物業服務辦事處 柴灣柴灣邨灣畔樓地下 G/F, Wan Poon House, Chai Wan Estate, Chai Wan Management Office Unit 17A-24, G/F, Wah Chak House, Chak On Estate, 澤安邨辦事處 Chak On Estate Office 深水埗澤安邨華澤樓地下17A-24號 Sham Shui Po Cheung Ching Estate Property Services Unit 20-29, G/F, Ching Wai House, Cheung Ching 長青邨物業服務辦事處 青衣長青邨青槐樓地下20-29號 Management Office Estate, Tsing Yi Cheung Hang Estate Property Services Unit 1-8, G/F, Hang Lai House, Chueng Hang Estate, 長亨邨物業服務辦事處 青衣長亨邨亨麗樓地下1-8號 Management Office Tsing Yi 長康邨辦事處 Cheung Hong Estate Office 青衣長康邨康平樓地下 G/F, Hong Ping House, Cheung Hong Estate, Tsing Yi Cheung Kwai Estate Property Services Unit 101-102, Cheung Wong House, Cheung Kwai 長貴邨物業服務辦事處 長洲長貴邨長旺樓101-102號 Management Office Estate, Cheung Chau Cheung Lung Wai Estate Property G/F, King Cheung House, Cheung Lung Wai Estate, 祥龍圍邨物業服務辦事處 上水祥龍圍邨景祥樓地下 Services Management Office Sheung Shui Cheung Sha Wan Estate Property 1/F, Cheung Tai House, Cheung Sha Wan Estate, Sham 長沙灣邨物業服務辦事處 深水埗長沙灣邨長泰樓一樓 Services Management Office Shui Po Cheung -

G.N. 1889 Housing Authority It Is Hereby Notified That Contracts and Tenancy Agreements of the Following Contracts and Premises

G.N. 1889 Housing Authority It is hereby notified that contracts and tenancy agreements of the following contracts and premises have been executed by the Authority during the month of February 2014:— DEVELOPMENT AND CONSTRUCTION DIVISION Name of Contract Successful Tenderer Tendered Amount ($) Purchase of Unserviceable Plastic Refuse Hop Shing Plastic Material 495,000.00 Containers from the Hong Kong Housing Authority (Tender Ref. HAQ20130800) Provision of Specialist Cleaning and Minor International Architectural 166,800.00 Maintenance Services for Models Displayed in Model Co. the Hong Kong Housing Authority Exhibition Centre (Tender Ref. HAQ20130919) Provision of Counselling Services on Stress Hong Kong Family 200,000.00 Management Welfare Society (Tender Ref. HAQ20130842) Supply, Delivery, Maintenance and Other ELM Computer 2,977,200.00 Related Services of Additional Software Technologies Ltd. Licences for System Monitoring for the Hong Kong Housing Authority (Tender Ref. HAQ20130788) ESTATE MANAGEMENT DIVISION Name of Contract Successful Tenderer Tendered Amount ($) Lift Modernization for Mei Shan House ThyssenKrupp Elevator 11,323,728.00 (Block 42), Mei Hung House (Block 43) and (HK) Ltd. Mei Choi House (Block 44) in Shek Kip Mei Estate (Contract No. 20139135) District Term Contract for the Maintenance, Unistress Building 369,302,000.00 Improvement and Vacant Flat Refurbishment Construction Ltd. for Property Managed by the Property Service Administration Unit/Tuen Mun and Yuen Long (1) 2014/2017 (Contract No. 20139370) Operation and Maintenance of Automated Associated Engineers, Ltd. 4,500,000.00 Refuse Collection System for Tin Heng Estate (Contract No. 20139410) Extension of Cleansing Service Contract for Ying Wah Cleaning Service 1,026,432.00 Model Housing Estate Ltd. -

Public Housing in the Global Cities: Hong Kong and Singapore at the Crossroads

Preprints (www.preprints.org) | NOT PEER-REVIEWED | Posted: 11 January 2021 doi:10.20944/preprints202101.0201.v1 Public Housing in the Global Cities: Hong Kong and Singapore at the Crossroads Anutosh Das a, b a Post-Graduate Scholar, Department of Urban Planning and Design, The University of Hong Kong (HKU), Hong Kong; E-mail: [email protected] b Faculty Member, Department of Urban & Regional Planning, Rajshahi University of Engineering & Technology (RUET), Bangladesh; E-mail: [email protected] Abstract Affordable Housing, the basic human necessity has now become a critical problem in global cities with direct impacts on people's well-being. While a well-functioning housing market may augment the economic efficiency and productivity of a city, it may trigger housing affordability issues leading crucial economic and political crises side by side if not handled properly. In global cities e.g. Singapore and Hong Kong where affordable housing for all has become one of the greatest concerns of the Government, this issue can be tackled capably by the provision of public housing. In Singapore, nearly 90% of the total population lives in public housing including public rental and subsidized ownership, whereas the figure tally only about 45% in Hong Kong. Hence this study is an effort to scrutinizing the key drivers of success in affordable public housing through following a qualitative case study based research methodological approach to present successful experience and insight from different socio-economic and geo- political context. As a major intervention, this research has clinched that, housing affordability should be backed up by demand-side policies aiming to help occupants and proprietors to grow financial capacity e.g. -

List of Abbreviations

LIST OF ABBREVIATIONS AAHK Airport Authority Hong Kong AAIA Air Accident Investigation Authority AFCD Agriculture, Fisheries and Conservation Department AMS Auxiliary Medical Service ASC Aviation Security Committee ASD Architectural Services Department BD Buildings Department CAD Civil Aviation Department CAS Civil Aid Service CCCs Command and Control Centres CEDD Civil Engineering and Development Department CEO Chief Executive’s Office / Civil Engineering Office CESC Chief Executive Security Committee CEU Casualty Enquiry Unit CIC Combined Information Centre CS Chief Secretary for Administration DECC District Emergency Co-ordination Centre DEVB Development Bureau DH Department of Health DO District Officer DSD Drainage Services Department EDB Education Bureau EMSC Emergency Monitoring and Support Centre EMSD Electrical and Mechanical Services Department EPD Environmental Protection Department EROOHK Emergency Response Operations Outside the HKSAR ESU Emergency Support Unit ETCC Emergency Transport Coordination Centre FCC Food Control Committee FCP Forward Control Point FEHD Food and Environmental Hygiene Department FSCC Fire Services Communication Centre FSD Fire Services Department GEO Geotechnical Engineering Office GFS Government Flying Service GL Government Laboratory GLD Government Logistics Department HA Hospital Authority HAD Home Affairs Department HD Housing Department HyD Highways Department HKO Hong Kong Observatory HKPF Hong Kong Police Force HKSAR Hong Kong Special Administrative Region HQCCC Police Headquarters Command -

Hansard (English)

LEGISLATIVE COUNCIL ─ 26 January 2011 5291 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 26 January 2011 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE JASPER TSANG YOK-SING, G.B.S., J.P. THE HONOURABLE ALBERT HO CHUN-YAN IR DR THE HONOURABLE RAYMOND HO CHUNG-TAI, S.B.S., S.B.ST.J., J.P. THE HONOURABLE LEE CHEUK-YAN DR THE HONOURABLE DAVID LI KWOK-PO, G.B.M., G.B.S., J.P. THE HONOURABLE FRED LI WAH-MING, S.B.S., J.P. DR THE HONOURABLE MARGARET NG THE HONOURABLE JAMES TO KUN-SUN THE HONOURABLE CHEUNG MAN-KWONG THE HONOURABLE CHAN KAM-LAM, S.B.S., J.P. THE HONOURABLE MRS SOPHIE LEUNG LAU YAU-FUN, G.B.S., J.P. THE HONOURABLE LEUNG YIU-CHUNG DR THE HONOURABLE PHILIP WONG YU-HONG, G.B.S. 5292 LEGISLATIVE COUNCIL ─ 26 January 2011 THE HONOURABLE WONG YUNG-KAN, S.B.S., J.P. THE HONOURABLE LAU KONG-WAH, J.P. THE HONOURABLE LAU WONG-FAT, G.B.M., G.B.S., J.P. THE HONOURABLE MIRIAM LAU KIN-YEE, G.B.S., J.P. THE HONOURABLE EMILY LAU WAI-HING, J.P. THE HONOURABLE ANDREW CHENG KAR-FOO THE HONOURABLE TIMOTHY FOK TSUN-TING, G.B.S., J.P. THE HONOURABLE TAM YIU-CHUNG, G.B.S., J.P. THE HONOURABLE ABRAHAM SHEK LAI-HIM, S.B.S., J.P. THE HONOURABLE LI FUNG-YING, S.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, S.B.S., J.P. THE HONOURABLE FREDERICK FUNG KIN-KEE, S.B.S., J.P. -

OFFICIAL RECORD of PROCEEDINGS Wednesday, 17

LEGISLATIVE COUNCIL ─ 17 November 2010 2033 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 17 November 2010 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE JASPER TSANG YOK-SING, G.B.S., J.P. THE HONOURABLE ALBERT HO CHUN-YAN IR DR THE HONOURABLE RAYMOND HO CHUNG-TAI, S.B.S., S.B.ST.J., J.P. THE HONOURABLE LEE CHEUK-YAN DR THE HONOURABLE DAVID LI KWOK-PO, G.B.M., G.B.S., J.P. THE HONOURABLE FRED LI WAH-MING, S.B.S., J.P. DR THE HONOURABLE MARGARET NG THE HONOURABLE JAMES TO KUN-SUN THE HONOURABLE CHEUNG MAN-KWONG THE HONOURABLE CHAN KAM-LAM, S.B.S., J.P. THE HONOURABLE MRS SOPHIE LEUNG LAU YAU-FUN, G.B.S., J.P. THE HONOURABLE LEUNG YIU-CHUNG DR THE HONOURABLE PHILIP WONG YU-HONG, G.B.S. 2034 LEGISLATIVE COUNCIL ─ 17 November 2010 THE HONOURABLE LAU KONG-WAH, J.P. THE HONOURABLE LAU WONG-FAT, G.B.M., G.B.S., J.P. THE HONOURABLE MIRIAM LAU KIN-YEE, G.B.S., J.P. THE HONOURABLE EMILY LAU WAI-HING, J.P. THE HONOURABLE ANDREW CHENG KAR-FOO THE HONOURABLE TIMOTHY FOK TSUN-TING, G.B.S., J.P. THE HONOURABLE TAM YIU-CHUNG, G.B.S., J.P. THE HONOURABLE ABRAHAM SHEK LAI-HIM, S.B.S., J.P. THE HONOURABLE LI FUNG-YING, S.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, S.B.S., J.P. THE HONOURABLE FREDERICK FUNG KIN-KEE, S.B.S., J.P. THE HONOURABLE AUDREY EU YUET-MEE, S.C., J.P. -

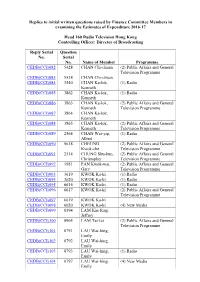

Replies to Initial Written Questions Raised by Finance Committee Members in Examining the Estimates of Expenditure 2016-17 Head

Replies to initial written questions raised by Finance Committee Members in examining the Estimates of Expenditure 2016-17 Head 160 Radio Television Hong Kong Controlling Officer: Director of Broadcasting Reply Serial Question No. Serial No. Name of Member Programme CEDB(CCI)082 5428 CHAN Chi-chuen (2) Public Affairs and General Television Programme CEDB(CCI)083 5518 CHAN Chi-chuen CEDB(CCI)084 3540 CHAN Ka-lok, (1) Radio Kenneth CEDB(CCI)085 3862 CHAN Ka-lok, (1) Radio Kenneth CEDB(CCI)086 3863 CHAN Ka-lok, (2) Public Affairs and General Kenneth Television Programme CEDB(CCI)087 3864 CHAN Ka-lok, Kenneth CEDB(CCI)088 3865 CHAN Ka-lok, (2) Public Affairs and General Kenneth Television Programme CEDB(CCI)089 2564 CHAN Wai-yip, (1) Radio Albert CEDB(CCI)090 5618 CHEUNG (2) Public Affairs and General Kwok-che Television Programme CEDB(CCI)091 2514 CHUNG Shu-kun, (2) Public Affairs and General Christopher Television Programme CEDB(CCI)092 1981 FAN Kwok-wai, (2) Public Affairs and General Gary Television Programme CEDB(CCI)093 3619 KWOK Ka-ki (1) Radio CEDB(CCI)094 3620 KWOK Ka-ki (1) Radio CEDB(CCI)095 6616 KWOK Ka-ki (1) Radio CEDB(CCI)096 6617 KWOK Ka-ki (2) Public Affairs and General Television Programme CEDB(CCI)097 6619 KWOK Ka-ki CEDB(CCI)098 6620 KWOK Ka-ki (4) New Media CEDB(CCI)099 0394 LAM Kin-fung, Jeffrey CEDB(CCI)100 0964 LAM Tai-fai (2) Public Affairs and General Television Programme CEDB(CCI)101 0791 LAU Wai-hing, Emily CEDB(CCI)102 0792 LAU Wai-hing, Emily CEDB(CCI)103 0793 LAU Wai-hing, (1) Radio Emily CEDB(CCI)104 0797 LAU Wai-hing, (4) New Media Emily Reply Serial Question No. -

CUHK Startup Scheme for Social Impact 3

annual report Recurrent Funding for Knowledge Transfer 2015 - 2016 submitted to: University Grants Committee Table of Contents 1. Execuve Summary 2. A New CUHK Startup Scheme for Social Impact 3. Fostering Entrepreneurship 3.1. Pre-incubation Centre (Pi Centre) 3.2. Technology Startup Support Scheme for Universities (TSSSU) 3.3. Extending Outside Practice (OP) Policy to Non-Professoriate Research Staff 4. Facilitang Technology Transfer 4.1. Reaching Out to Investors and Development Partners 4.2. Building Relationships with Organizations Locally and Abroad 4.3. IP Licensing and Competition 4.4. Revision of IP Policy 5. Capacity Building and Connuous Improvement 5.1. Capacity Building 5.2. Continuous Improvement 6. Impact Case Studies Case Study 1: Method for Preparing Titanium Dioxide (TiO2) with Higher Photocatalytic and Antibacterial Activities Case Study 2: Novel Therapeutics Against Rare Neurodegenerative Diseases Case Study 3: Nourishing a Life of Dignity: Healthy Individuals, Resilient Families and Sustainable Communities Case Study 4: Enhancing Public Awareness of Sarcopenia 7. Looking Ahead Annex 1 Impact Case Studies Annex 2 Financial Report on the Use of UGC KT Fund Annex 3 Updates on Table 4.1 of Inial Statement Annex 4 Updates on Table 4.2 of Inial Statement Annex 5 Number of Patents Filed in 2015/16 with Breakdown Annex 6 Number of Patents Granted in 2015/16 with Breakdown Annex 7 Number of Licenses Granted in 2015/16 with Breakdown Annex 8 Contracts Reviewed and/or Executed through ORKTS 2015/16 Annex 9 Knowledge Transfer Project Fund: Project List and Details Annex 10 Sustainable Knowledge Transfer Fund: Project Details Annex 11 Technology and Business Development Fund: Project List and Details Annex 12 Number of Spin-off Companies with Breakdown 2015/16 Annex 13 Knowledge Transfer Seminar Series Annex 14 Network Building: Acvies Conducted or Parcipated by ORKTS 2015/16 1. -

香港特別行政區政府 the Government of the Hong Kong Special Administrative Region

LC Paper No. CB(1)533/18-19(01) 香港特別行政區政府 The Government of the Hong Kong Special Administrative Region 運輸及房屋局 Transport and Housing Bureau 香港九龍何文田佛光街 33 號 33 Fat Kwong Street, Ho Man Tin, Kowloon, Hong Kong 本局檔號 Our Ref. HD(CEPWP)12/5/31 電話 Tel No. 2129 3701 來函檔號 Your Ref. 圖文傳真 Fax No. 3691 9899 30 January 2019 Clerk to Legislative Council Panel on Housing Legislative Council Secretariat Legislative Council Complex 1 Legislative Council Road, Central Hong Kong (Attn : Mr Derek LO) Dear Mr LO, Panel on Housing Subcommittee to Follow Up the Issues Related to the Wang Chau Development Project Email on 11 January 2019 Thank you for your email on 11 January 2019, attaching a letter dated 18 December 2018 from the Chairman of LegCo Subcommittee to Follow Up the Issues Related to the Wang Chau Development Project under Panel on Housing, requesting the Government to provide information on the issues listed below - (i) pet keeping arrangement at public housing for affected residents; (ii) adoption of animals which are affected by Government development projects; (iii) “Trap, Neuter and Release” (TNR) trial programme; (iv) animal welfare policy; (v) number of animals, which are affected by Wang Chau Development Project, can be received by animal welfare organisations (AWOs) in future; and (vi) draft sample of application form of “Transitional Rental Housing for Non-means Tested Domestic Occupants in Squatters Affected by Government’s Development Clearance Exercises”. 2. After consolidation of information gathered from relevant bureau/departments, we provide a reply to the related issues as follows - Pet Keeping Arrangement at Public Housing for Affected Residents 3. -

The Ombudsman, Hong Kong, Annual Report 2019/20

The Ombudsman, Hong Kong Annual Report 2019/20 Annual Report of The Ombudsman, Hong Kong 2019/20 Hong Kong The Ombudsman, Annual Report of • 32nd Issue POSITIVE COMPLAINT CULTURE FOR BETTER ADMINISTRATION Key Figures of the Year Complaints Complaints received 19,767 completed 19,838 93% 5% by email/fax by post 17,031 2,418 Closed after Concluded by assessment inquiry 2% 1% in person by phone 240 149 Concluded by full Resolved by investigation mediation 99.4% 93.5% 99.3% (target: 99.0%) (target: 80.0%) (target: 99.0%) Complaints closed within Complaints concluded Complaints concluded 15 working days after within 3 months within 6 months initial assessment due to jurisdictional restrictions Cases related 10 to access to Direct Investigations information completed completed 84 Recommendations given 177 Enquiries received 8,581 VISION To ensure that Hong Kong is served by a fair and efficient public administration which is committed to accountability, openness and quality of service MISSION Through independent, objective and impartial investigation, to redress grievances and address issues arising from maladministration in the public sector and bring about improvement in the quality and standard of and promote fairness in public administration VALUES • Maintaining impartiality and objectivity in our investigations • Making ourselves accessible and accountable to the public and organisations under our jurisdiction • According the public and organisations courtesy and respect • Upholding professionalism in the performance of our functions CONTENTS