1Q15 Earnings Call Presentation April 22, 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Marina Bay Sands

3Q19 Earnings Call Presentation October 23, 2019 Forward Looking Statements This presentation contains forward-looking statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve a number of risks, uncertainties or other factors beyond the company’s control, which may cause material differences in actual results, performance or other expectations. These factors include, but are not limited to, general economic conditions, competition, new development, construction and ventures, substantial leverage and debt service, fluctuations in currency exchange rates and interest rates, government regulation, tax law changes and the impact of U.S. tax reform, legalization of gaming, natural or man- made disasters, terrorist acts or war, outbreaks of infectious diseases, insurance, gaming promoters, risks relating to our gaming licenses and subconcession, infrastructure in Macao, our subsidiaries’ ability to make distribution payments to us, and other factors detailed in the reports filed by Las Vegas Sands with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date thereof. Las Vegas Sands assumes no obligation to update such information. Within this presentation, the company may make reference to certain non-GAAP financial measures including “adjusted net income,” “adjusted earnings per diluted share,” and “consolidated adjusted property EBITDA,” which have directly comparable financial measures presented in accordance with accounting principles generally accepted in the United States of America ("GAAP"), along with “adjusted property EBITDA margin,” “hold-normalized adjusted property EBITDA,” “hold-normalized adjusted property EBITDA margin,” “hold-normalized adjusted net income,” and “hold-normalized adjusted earnings per diluted share,” as well as presenting these or other items on a constant currency basis. -

UP SET for VENETIAN MACAO OPEN Macao, Octob

PRESS RELEASE STAR-STUDDED LINE-UP SET FOR VENETIAN MACAO OPEN Macao, October 9: The Venetian Macao Open is poised to welcome a stellar line-up of stars from the Asian Tour, with seven Order of Merit champions and no fewer than 45 Tour champions primed to challenge defending champion Anirban Lahiri for his title next week. In addition to the presence of four-time Major winner Ernie Els, seven players from the current top-10 of the Merit list and seven other former champions of the Venetian Macao Open, including two-time winner Zhang Lian-wei of China, will tee up at the challenging Macau Golf and Country Club from October 15-18. Reigning Asian Tour number one David Lipsky will also return to Asian soil for the first time since April and will be banking on a recent tied third finish in Italy to spur him towards a third Asian Tour title. Lahiri, currently top of the Merit list, is expected to fight hard to retain his crown especially when he will arrive in Macao on the back of a maiden appearance at the on-going Presidents Cup in Korea where he is the first Indian to feature in the biennial team competition. “The Venetian Macao Open is certainly one of the best tournaments we play all year. It’s very intimate and it’s just great fun to be right in the heart of Macao,” said the 28-year-old Lahiri, who is ranked 39th in the world. Other stars in the top-10 of the current Merit rankings heading to Macao include second- ranked Andrew Dodt of Australia, 2013 Venetian Macau Open champion Scott Hend of Australia, Malaysia’s Danny Chia, S.S.P. -

2020 Annual Report

Stock Code: 1928 and Note Stock Codes: 5140, 5141, 5142, 5725, 5727, 5733, 40246, 40247, 40584, 40585 www.sandschina.com From Luxury Duty Free Shopping, Exciting Entertainment and Fabulous Dining to World-Class Hotel Suites and MICE, Come and Discover Everything at Sands China. SANDS CHINA LTD. CONTENTS 1. OVERVIEW 4 1.1 Financial Results Summary 4 1.2 Highlights of 2020 5 1.3 Directors and Senior Management 11 2. BUSINESS REVIEW 18 2.1 Chairman’s Statement 18 2.2 Business Overview and Outlook 20 2.3 Our Properties 26 2.4 Management Discussion and Analysis 33 2.5 Priority Risk Factors 47 2.6 Stakeholder Information 59 3. CORPORATE GOVERNANCE 66 REPORT 3.1 Introduction 66 3.2 Corporate Governance Code Compliance 66 3.3 Board Governance Structure 67 3.4 The Board 68 3.5 Audit Committee 74 3.6 Remuneration Committee 76 3.7 Nomination Committee 78 3.8 Capex Committee 81 3.9 Risk Management and Internal Control 82 3.10 Shareholders 87 3.11 Compliance Disclosures and Other Matters 90 3.12 Directors’ Report 92 4. FINANCIAL STATEMENTS 113 4.1 Independent Auditor’s Report 113 4.2 Financial Statements 117 4.3 Notes to the Consolidated Financial Statements 123 4.4 Financial Summary 193 5. CORPORATE INFORMATION 194 6. CONTACT US 195 7. GLOSSARY 196 In case of any inconsistency between the English version and the Chinese version of this Annual Report, the English version shall prevail. SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS 2 ANNUAL REPORT 2020 SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS our Luxurious Hotel Rooms and Suites await you. -

Press Release

Press Release Celebrities Shine at The Venetian Macao for Asia Rainbow TV Awards Integrated resort brings another star-studded awards show to Macao (Macao, June 26, 2014) – The first Asian television awards show presented by mainland China, the Asia Rainbow TV Awards, were held in Macao for the first time Thursday night, hosted at The Venetian Theatre. With SONIQ as the exclusive title sponsor, and The Venetian® Macao as special sponsor, the Asia Rainbow TV Awards – known as Asia's version of Hollywood's Emmy Awards – is the first awards show for the television industry to be held at The Venetian Macao. Celebrities arriving on the red carpet for the awards show included actors Lee Li-Chun, Hawick Lau and Jerry Lee, and actresses Tongshu Yang, Dandan Song and Guitian Sun. Crowds of screaming fans clamoured to get a view of the famous faces as the glamorous luminaries captured everyone’s attention with their star power. With nearly 400 nominees hailing from 14 countries, 80 awards were given across 27 categories, including awards for Best Actor/Actress, Best Scriptwriter, and Best Actor/Actress Comedy. “Sands China brings the best of the best to Macao, so it is with great pleasure that we are hosting Asia Rainbow TV Awards, an outlet for recognising Asia’s top television talent,” said Olaf Gueldner, Senior Vice President and Chief Marketing Officer of Sands China Ltd. “Our properties are the place to be for seeing the brightest stars, as our multi-tiered entertainment strategy continues to cement Macao’s position as one of the region’s top entertainment destinations for superstars events and to promote the city as a world centre of tourism and leisure.” The awards show was broadcast via 23 television stations to audiences across mainland China, reaching an estimated audience of half a billion viewers. -

Inauguration of 2008 MIECF

Press Release No 4 23 th April 2008 Inauguration of 2008 MIECF The “2008 Macau International Environmental Co-operation Forum and Exhibition” (2008 MIECF) was inaugurated this morning (April 23) at The Cotai Strip Convention and Exhibition Centre of the Venetian Macao Resort Hotel. The event is hosted by the Government of the Macao Special Administrative Region, co-organized by Provincial and Regional Governments of the Pan-Pearl River Delta Region, and supported by the Ministry of Environmental Protection of the People's Republic of China. Mr. Edmund Ho, Chief Executive of Macau SAR, gave a speech in the opening ceremony, pointing out that water and energy are matters of concern for both the international community and the Macau citizenry. He stressed that Macau’s water and energy security hinges on the support of the Central Government, and that the SAR is dedicated to solving problems regarding salinity, energy conservation, and environmental protection awareness-raising, in order to attain sustainable development. The officiating guests accompanying the Chief Executive in the opening ceremony include Mr. Li Benjun, Deputy Director General of the Liaison Office of the Central People’s Government in the Macao SAR, Mr. Wan Yongxiang, Commissioner of the Ministry of Foreign Affairs of the People’s Republic of China in the Macao SAR, Mr. Hu Siyi, Vice Minister of Ministry of Water Resources of the PRC, Mr. Xu Qinghua, Representative of the Minister of Ministry of Environmental Protection of the PRC, Mr. Su Zengtian, Vice Governor of the People’s Government of Fujian Province, Mr. Hong Lihe, Vice Governor of the People’s Government of Jiangxi Province, Mr. -

The Venetian Macao Reserves the Right to Release the Suites for Resale Without Prior Notice

Terms and Conditions General 1. All rates are in MOP/HKD and subject to 5% Government Tax and 10% Service Charge. 2. All reservations, unless guaranteed by deposit or credit card, will be held until Macao local time 18:00 of proposed arrival date only. The Venetian Macao reserves the right to release the suites for resale without prior notice. 3. All cancellations or amendments must be made 24 hours before arrival. A charge equivalent to the total package price plus service charge and government tax will be imposed for No Show. 4. Any extension of stay, after initial booking is confirmed, will be subject to availability and will be at Hotel’s Best Available Rate. 5. All package inclusions are on a per stay basis. 6. Unused package benefits cannot be reimbursed or redeemed for cash either in full or in part. 7. Cost for an additional guest (12 years old or below) is MOP/HKD150 per person per night inclusive of: One- way Macao to Hong Kong Cotai Water Jet Cotai Class ferry ticket / Gondolier Ride / entry for Qube or Qube 2 (1st night), breakfast/lunch (1st night), breakfast/lunch/dinner (2nd night) AND Breakfast/Lunch/Afternoon tea (3-night). 8. Cost for an additional guest (13 years old or above) is MOP/HKD350 per person per night inclusive of: One- way Macao to Hong Kong Cotai Water Jet Cotai Class ferry ticket / Gondolier Ride / entry for Qube or Qube 2 (1st night), breakfast/lunch (1-night), breakfast/lunch/dinner (2nd night) AND breakfast/Lunch/Afternoon tea (3rd night). -

Downloadable Content Supported by Multiple RNG (Random Num- Ber Generation) Levels and System Configurations

Aug 2007 • MOP 30 Macau Bottlenecks The Walls Have Eyes Crown Revisited Out of Australia Facilities to draw a new breed of visitor Changing Macau’s Profile Aug 2007 Changing Macau’s Profile Page 6 ~ Changing Macau’s Visitor Profile 4 Page 12 ~ Macau Development Bottlenecks 12 Page 19 ~ The Walls Have Eyes 18 Page 26 ~ Vendor Profile - Videobet 22 Page 28 ~ Destination Singapore 26 Page 32 ~ Crown Revisited 30 Page 34 ~ Riding Asia’s Slot Wave 32 Page 36 ~ Out of Australia 34 Page 40 ~ Regional Briefs 36 Page 42 ~ International Briefs 40 Page 4442 ~ Online Briefs Page 4644 ~ Going Global 45 2 3 4 Editorial Changing Macau’s Profile Sands Macao may have become the biggest table-gaming casino city. When Sands Macao opened, it had a slot to table ratio of 1.46, but in the world, and generates more gaming revenue than many coun- Venetian’s ratio at opening will be 5.06. High returns from putting in tries—last month, Inside Asian Gaming visited the Philippines (report more tables had previously discouraged investment in slot machines to appear in next issue), and while the various casinos were hives of in Macau, but the tide is clearly turning as both table and slot capacity activity, the entire country’s gaming revenue was less than half the show explosive growth, but wins per slot have remained steady while revenue of Sands Macao. wins per table have declined. The properties opening to date in Macau have concentrated pri- The capacity increase has boosted overall casino revenue, which marily on gambling. -

4Q14 Earnings Call Presentation January 28, 2015

The Venetian Macao Sands Cotai Central, Macao Marina Bay Sands, Singapore The Parisian, Macao 4Q14 Earnings Call Presentation January 28, 2015 Sands Macao Four Seasons Macao Sands Bethlehem The Venetian Las Vegas The Palazzo Las Vegas Forward Looking Statements This presentation contains forward-looking statements that are made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Forward- looking statements involve a number of risks, uncertainties or other factors beyond the company’s control, which may cause material differences in actual results, performance or other expectations. These factors include, but are not limited to, general economic conditions, competition, new ventures, substantial leverage and debt service, government regulation, legalization of gaming, interest rates, future terrorist acts, influenza, insurance, gaming promoters, risks relating to our gaming licenses, certificate and subconcession, infrastructure in Macao and other factors detailed in the reports filed by Las Vegas Sands Corp. with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date thereof. Las Vegas Sands Corp. assumes no obligation to update such information. 2 The Investment Case for Las Vegas Sands The global leader in Integrated Resort development and operation, delivering strong and diversified cash flow and earnings as well as growing recurring dividends Best positioned operator to deliver growth -

The Parisian Macao Official Website in the Form of Confirmation Numbers

Terms and Conditions • Flexible Rate, Any 7 and 14 Day Advance Purchase, Bed and Breakfast, Ferry Package, Parisian Macao Package, Monkey King Package and Macao Summer Celebration Bookings made on parisianmacao.com or a Venetian Cotai Limited authorized online travel partner (Booking.com and Rakuten) from 00:00 September 13th, 2017 to 23:59 September 20th, 2017, the guest will automatically enter a chance to win one free night stay. • A total of 10 qualified reservations will be randomly selected on a daily basis from September 14th, 2017 to September 21st, 2017. • First night of the qualified winning bookings made on parisianmacao.com will be complimentary. Any advance payment made for the first night will be credited back to winner’s account. • Any qualified winning bookings made on Venetian Cotai Limited’s authorized online travel partners (Booking.com and Rakuten) will receive a future one night complimentary stay (room only) in the same paid room type on the original reservation. Future complimentary stay will be subject to availability at the time of booking. Email address must be collected at the time of check in for future complimentary stay booking. In the event email address provided by winner is invalid or no reply from winner within 7 days of first contact, complimentary room will be voided. Additional Terms and Conditions of future complimentary stay may apply. • All participants must be aged over 18. • Winners will be announced on the Parisian Macao official website in the form of confirmation numbers. • In the event of a winning reservation is a no show or cancelled, it will result in disqualification, the correspondent prize will be forfeited and no additional winner will be selected. -

2Q18 Earnings Call Presentation July 25, 2018

The Venetian Macao Sands Cotai Central, Macao Marina Bay Sands, Singapore The Parisian Macao 2Q18 Earnings Call Presentation July 25, 2018 Sands Macao Four Seasons Macao Sands Bethlehem The Venetian Las Vegas The Palazzo, Las Vegas Forward Looking Statements This presentation contains forward‐looking statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Forward‐looking statements involve a number of risks, uncertainties or other factors beyond the company’s control, which may cause material differences in actual results, performance or other expectations. These factors include, but are not limited to, general economic conditions, competition, new development, construction and ventures, substantial leverage and debt service, fluctuations in currency exchange rates and interest rates, government regulation, tax law changes and the impact of U.S. tax reform, legalization of gaming, natural or man‐made disasters, terrorist acts or war, outbreaks of infectious diseases, insurance, gaming promoters, risks relating to our gaming licenses, certificate and subconcession, infrastructure in Macao, our subsidiaries’ ability to make distribution payments to us, and other factors detailed in the reports filed by Las Vegas Sands with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward‐looking statements, which speak only as of the date thereof. Las Vegas Sands assumes no obligation to update such information. Within this presentation, the -

The God of Fortune Smiling Down on Shoppes This Chinese New Year

Press Release Get Ready to Shop Like Never Before at the Sands Mega Brand Sale Over 150 international brands will come together in Cotai Expo Hall C to offer discounts of up to 80%, starts Nov. 26 for four days only (Macao, Nov. 16, 2015) – For just four days only the Sands Mega Brand Sale will offer fashion conscious shoppers the chance to update their wardrobe at greatly reduced prices from over 150 international designer brands, with many items priced up to 80 per cent off the normal retail price. This incredible sale will take place in Cotai Expo Hall C in The Venetian® Macao from Nov. 26-29. This limited-time sale is not to be missed by fashion lovers! Brands participating in the sale range from high street retailers to the biggest designer names available today, including Armani Collezione, Armani Exchange, Branco, Calvin Klein, Fossil, Honma Golf, Jimmy Choo, JOAN&DAVID, Just Cavalli, Love Moschino, Michael Kors, MOISELLE, Optica, Rene Caovilla, Roberto Cavalli, Steve Madden, Triumph, Trussardi, TUMI, Versace Jeans, Vivienne Westwood and Weekend by Max Mara. Those looking to add to their shoe collection will also be able to get fantastic discounts from famous brands such as Florsheim, Hush Puppies, iiJin, Jipi Japa, Joy & Peace, Millies, Mirabell, Navyboot and STACCATO. The Sands Mega Brand Sale will take place from Nov. 26-27 from noon – 10 p.m. and from Nov. 28-29 from 10 a.m. – 8 p.m. The Sands Mega Brand Sale offers unprecedented discounts from well-known brands and with so many outlets to choose from customers are guaranteed to find something to take home. -

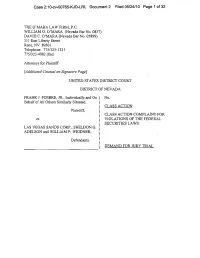

Case 2:10-Cv-00765-KJD-LRL Document 2 Filed 05/24/10 Page 1 of 32

Case 2:10-cv-00765-KJD-LRL Document 2 Filed 05/24/10 Page 1 of 32 THE O'MARA LAW FIRM, P.C. WILLIAM 0. O'MARA (Nevada Bar No, 0837) DAVID C. O'MARA (Nevada Bar No. 05899) 311 East Liberty Street Reno, NV 89501 Telephone: 775/323-1321 775/323-4082 (fax) Attorneys for Plaintiff [Additional Counsel on Signature Page] UNITED STATES DISTRICT COURT DISTRICT OF NEVADA FRANK I. FOSBRE, JR., Individually and On ) No. Behalf of All Others Similarly Situated, ) ) CLASS ACTION Plaintiff, ) ) CLASS ACTION COMPLAINT FOR VS. ) VIOLATIONS OF THE FEDERAL ) SECURITIES LAWS LAS VEGAS SANDS CORP., SHELDON G. ADELSON and WILLIAM P. WEIDNER, ) ) . Defendants. ) ) ) DEMAND FOR JURY TRIAL Case 2:10-cv-00765-KJD-LRL Document 2 Filed 05/24/10 Page 2 of 32 Plaintiff alleges the following based upon the investigation of his counsel, which included a review of United States Securities and Exchange Commission ("SEC") filings made by Las Vegas Sands Corp. ("Las Vegas Sands" or the "Company"), as well as regulatory filings and reports, securities analysts' reports and advisories about the Company, press releases and other public statements issued by the Company, and media reports about the Company, and believes that substantial additional evidentiary support will exist for the allegations set forth herein after a reasonable opportunity for discovery. NATURE OF THE ACTION 1. This federal securities class action is brought on behalf of purchasers of the common stock of Las Vegas Sands between August 1, 2007 and November 6, 2008, inclusive (the "Class Period"), seeking to pursue remedies under the Securities Exchange Act of 1934 (the "Exchange Act").