Chapter 7 INFRASTRUCTURE DEVELOPMENT

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Administrative Atlas , Punjab

CENSUS OF INDIA 2001 PUNJAB ADMINISTRATIVE ATLAS f~.·~'\"'~ " ~ ..... ~ ~ - +, ~... 1/, 0\ \ ~ PE OPLE ORIENTED DIRECTORATE OF CENSUS OPERATIONS, PUNJAB , The maps included in this publication are based upon SUNey of India map with the permission of the SUNeyor General of India. The territorial waters of India extend into the sea to a distance of twelve nautical miles measured from the appropriate base line. The interstate boundaries between Arunachal Pradesh, Assam and Meghalaya shown in this publication are as interpreted from the North-Eastern Areas (Reorganisation) Act, 1971 but have yet to be verified. The state boundaries between Uttaranchal & Uttar Pradesh, Bihar & Jharkhand and Chhattisgarh & Madhya Pradesh have not been verified by government concerned. © Government of India, Copyright 2006. Data Product Number 03-010-2001 - Cen-Atlas (ii) FOREWORD "Few people realize, much less appreciate, that apart from Survey of India and Geological Survey, the Census of India has been perhaps the largest single producer of maps of the Indian sub-continent" - this is an observation made by Dr. Ashok Mitra, an illustrious Census Commissioner of India in 1961. The statement sums up the contribution of Census Organisation which has been working in the field of mapping in the country. The Census Commissionarate of India has been working in the field of cartography and mapping since 1872. A major shift was witnessed during Census 1961 when the office had got a permanent footing. For the first time, the census maps were published in the form of 'Census Atlases' in the decade 1961-71. Alongwith the national volume, atlases of states and union territories were also published. -

Village & Townwise Primary Census Abstract, Kapurthala, Part X-A & B, Series-17, Punjab

CENSUS 1971 PARTS X-A & B VILLAGE & TOWN SERIES 17 DIRECTORY PUNJAB VILLAGE & TOWNWISE PRIMARY CENSUS ABSTRACT DISTRICT CENSUS KAPURTHALA HANDBOOK DISTRICT P. L. SONDHI H. S. KWATRA OF THE INDIAN ADMINISTRATIVE SERVICE OF THE PUNJAB CIVil, SERVICE Ex-Officio Director of Census Opemtions Deputy Director of Census Opemtions PUNJAB PUNJAB Motif-- GURDWARA BER SAHIB, SULTANPUR LODHI Gurdwara Be?" Sahib is a renowned place of pilgrimage of the Sikhs. It is situated at Sultanpur Lodhi, 16 miles South of Kapurthala, around a constellation of other Gurdwaras (Sikh Temples) associated with the early life of Guru Nanak Dev. It is n:a,.med after the 'Ber', tree under which Guru Nanak Dev used to meditate. Legend has it that sterile women beget child7'en after takinq leaves of this tree. The old Gu'rdwara was re-constructed by the joint effo'rts of Maharaja Jagatjit Singh of Kapurthala, Maharaja Yadvindra Singh of Patiala and Bhai Arjan Singh of Bagrian. A big fair is held at this Gurdwara on Guru Nanak Dev's birthday. Motif by : J. S. Gill. 15 '40' PUNJAB DISTRICT KAPURTHALA s· KILOIUTRES S o 5 10 15 20 4 8 12 MILES 4 o· 3 " Q TO JUL LlJNDllR <' ~O "'''<, U ""a". I. \.. u .) . 31 DISTRICT 80UNOARV..... POST' TtLEGftAPH OFfiCE "................. P'T TAHSIL BOUNDARY.. _TALlil PRIMARV HEALTH DISTRICT HEADQUARTERS .. CENTRE S IMATERNITY • CHIlD T"HSIL HEADQUARTERS. WELfARE CENTRES ............... - ... $ NATIONAL HIGHWAY .. liECONDARY SCHOOL./COl.LEGE .............•..• , OTHER METAI.LED ROAII.. 45 BROAD GAUGE RAILWAYS WITH STATIOfll. ... RS 4 RIVER .. - CANAL .. UklAII AREA •.. RUT HOUSE .... VILLAQES HAVING POPULATION 5000+ URBAN POPULATION " 50.000 PERSONS 10.000 •.. -

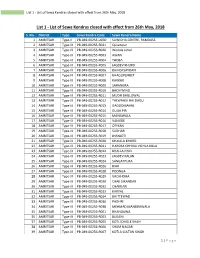

List 1 - List of Sewa Kendras Closed with Effect from 26Th May, 2018

List 1 - List of Sewa Kendras closed with effect from 26th May, 2018 List 1 - List of Sewa Kendras closed with effect from 26th May, 2018 S. No. District Type Sewa Kendra Code Sewa Kendra Name 1 AMRITSAR Type-II PB-049-00255-U030 SUWIDHA CENTRE, RAMDASS 2 AMRITSAR Type-III PB-049-00255-R031 Quiampur 3 AMRITSAR Type-III PB-049-00256-R020 Wadala Johal 4 AMRITSAR Type-III PB-049-00255-R003 AWAN 5 AMRITSAR Type-III PB-049-00255-R004 THOBA 6 AMRITSAR Type-III PB-049-00255-R005 JAGDEV KHURD 7 AMRITSAR Type-III PB-049-00255-R006 BHINDI SAYDAN 8 AMRITSAR Type-III PB-049-00255-R007 BHAGUPURBET 9 AMRITSAR Type-III PB-049-00255-R008 KAKKAR 10 AMRITSAR Type-III PB-049-00255-R009 SARANGRA 11 AMRITSAR Type-III PB-049-00255-R010 BACHIWIND 12 AMRITSAR Type-III PB-049-00255-R011 MUDH BHILLOWAL 13 AMRITSAR Type-III PB-049-00255-R012 TALWANDI RAI DADU 14 AMRITSAR Type-III PB-049-00255-R013 GAGGOMAHAL 15 AMRITSAR Type-III PB-049-00255-R014 GUJJA PIR 16 AMRITSAR Type-III PB-049-00255-R015 MANAWALA 17 AMRITSAR Type-III PB-049-00255-R016 VANIEKE 18 AMRITSAR Type-III PB-049-00255-R017 OTHIAN 19 AMRITSAR Type-III PB-049-00255-R018 SUDHAR 20 AMRITSAR Type-III PB-049-00255-R019 JHANJOTI 21 AMRITSAR Type-III PB-049-00255-R020 KHAIALA KHURD 22 AMRITSAR Type-III PB-049-00255-R021 HARSHA CHHINA VICHLA KILLA 23 AMRITSAR Type-III PB-049-00255-R022 BHALLA PIND 24 AMRITSAR Type-III PB-049-00255-R023 JAGDEV KALAN 25 AMRITSAR Type-III PB-049-00255-R024 SANGATPURA 26 AMRITSAR Type-III PB-049-00255-R026 RIAR 27 AMRITSAR Type-III PB-049-00255-R028 POONGA 28 AMRITSAR Type-III -

World Bank Document

Procurement Plan for Punjab RWSS (P150520) I. General 1. Bank’s approval Date of the procurement Plan 2012 Public Disclosure Authorized 2. Date of General Procurement Notice: [October 01, 2014 ] 3. Period covered by this procurement plan: January 2017 onwards II. Goods and Works and non-consulting services. 1. Prior Review Threshold: Procurement Decisions subject to Prior Review by the Bank as stated in Appendix 1 to the Guidelines for Procurement: 2. Procurement Method Prior Review Threshold US$ 1. ICB and LIB (Goods) Above US$ 500,000 2. NCB (Goods) Above US$ 100,000 3. ICB (Works) Above US$ 40 million Public Disclosure Authorized 4. NCB (Works) Above US$ 10 million 5. (Non-Consultant Services) Below US$ 100,000 2. Prequalification for Bidders _Not applicable_ 3. Proposed Procedures for CDD Components (as per paragraph. 3.17 of the Guidelines: NA 4. Reference to (if any) Project Operational/Procurement Manual: Project Implementation Manual for World Bank Loan Project P150520 Public Disclosure Authorized 5. Any Other Special Procurement Arrangements: In addition, the justification for all contracts to be issued on the basis of LIB, single-source or direct contracting (except for contracts less than US$50,000 in value) will be subject to prior review. Justification for all contracts to be issued on the basis of LIB, single-source or direct contracting (except for contracts less than US$50,000 in value) will be subject to prior review. III. Selection of Consultants 1. Prior Review Threshold: Selection decisions subject to Prior Review by Bank as stated in Appendix 1 to the Guidelines Selection and Employment of Consultants: Public Disclosure Authorized Selection Method Prior Review Threshold 1. -

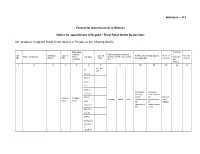

Annexure – H 2 Format for Advertisement in Website Notice For

Annexure – H 2 Format for Advertisement in Website Notice for appointment of Regular / Rural Retail Outlet Dealerships IOC proposes to appoint Retail Outlet dealers in Punjab, as per following details: Estimated Fixed Fee monthly Minimum Dimension (in / Sl. Revenue Type of Type of Finance to be arranged by Mode of Security Name of location Sales Category M.)/Area of the site (in Sq. Minimum No District RO Site* the applicant Selection Deposit Potential M.). * Bid # amount 1 2 3 4 5 6 7 8 9a 9b 10 11 12 CC / DC / SC CFS SC CC-1 SC CC-2 SC PH ST ST CC-1 Estimated Estimated ST CC-2 working fund required capital for Draw of Regular / MS+HSD ST PH Frontage Depth Area requirement development Lots / Rural in Kls OBC for of Bidding OBC CC-1 operation of infrastructure RO at RO OBC CC-2 OBC PH OPEN OPEN CC-1 OPEN CC- 2 OPEN PH FROM KM STONE 11 TO KM STONE 20 ON NH-54 (OLD NH-15) LEFT HAND Draw of 1 PATHANKOT Regular 150 SC CFS 35 45 1575 0 0 0 3 SIDE (WHILE GOING lots FROM PATHANKOT TO AMRITSAR) FROM KM STONE 340 TO KM STONE 347 ON NH 44 (OLD NH 1A) RIGHT HAND Draw of 2 PATHANKOT Regular 160 SC CFS 35 45 1575 0 0 0 3 SIDE (WHILE GOING lots FROM MADHOPUR TO JALANDHAR) VILLAGE- BABRI ON NH Draw of 3 GURDASPUR Regular 150 SC CFS 35 45 1575 0 0 0 3 54 lots FROM KM STONE 365 TO KM STONE 370 ON NH 44 (OLD NH 1A) LEFT HAND Draw of 4 PATHANKOT Regular 150 SC CFS 35 45 1575 0 0 0 3 SIDE (WHILE GOING lots FROM PATHANKOT TO JALANDHAR) AMRITSAR CITY (WML) Draw of 5 ON TARN TARAN ROAD AMRITSAR Regular 160 SC CFS 15.24 18.29 278.74 0 0 0 3 lots LHS FROM KM -

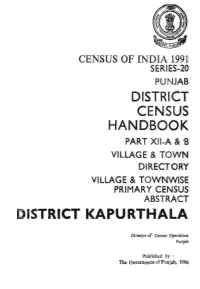

Village & Townwise Primary Census Abstract, Kapurthala, Part XII-A & B

CENSUS OF INDIA 1991 SERIES-20 PUNJAB DISTRICT CENSUS HAND·BOOK PA'RT XII-A & lB VILLAGE & T.OWN DrRECTORY VILLAGE & TOWNWISE .PRIMAR Y CENSUS ABSTRACT DISTRICT KAPURTHALA DIrector of Census Operations Punjab Published by : The Government of Punjab, 1996 PUNJAB DISTRICT KAPURTHALA ~m5 o 5 10 I5 20 Km q.. ~ \. '" q.. ,.. + A.., (J \. q. '" "" () " A.., .. l ;:;p. (" ~• ; ~ \ "z 0 s '{ .. BOUNDARY, DISTRICT _.-..- C.O. BLOCKS TAHSIL A NAOALA " C.D. BLOCK .' .. ........ .. , .. ...... " .. 1"" "e B I(APURTHALA H€ADOUARTERS: DlSTRlCTj TAHSIL .. ... .. .. @; @ C SUL TANPUR LOOM' NATIONAL HIGHWAY .......... .... .•. •. .. _...;,;N""'H.;..'_ o PHAGWARA IMPORTANT METALLED ROAD .. ........ .. " .... e' _-=__ RA!lWAY LINE WITH STATION, BROAD GAUGE: eo •• ' _~ RIVER AND STREAM .. .. .. .. .' .. .. ~ VILLAGE HAVING 5000 AND A90JE POPULATION WITH NAME ... ...... .. ...... .. .. .. .. .. .... Oh«wan• All Ixlondaries 0,. up«lted ullo I~ D«:embor, 1989. URBAN AREA WITH POP\JLATION SIZE CLASS II S IV •• POST AND TELEGRAPH OFFICE .. .. .. .. .. .. .. .. .. PTO DEGREE COLl.EG£ AND TECt-tlICAL INSTITUTION.. .. I!!!l m REST HOUSE RH DISTRICT H£ADQUARTERS IS AlSO TAHSL HEADQUARTERS 80sed upon Survey 01 IIIdkl map .llh the permission 01 the Sur~eyor 0._11 .f 1MiI. © GovlI'nmIIII of In4Ia Cop,,~t. 897. CENSUS OF INDlA-199i A-CENTRAL GOVERNMENT PUBLICATIONS ··Tho publications relating to Punjab bear Series No. 20 and will bo published as follows :- part I·A Administration Report- Enumeration (for official use only). Pa.rt l-B Admi nistration Report-Ta bulatio n (for official use only), "- Part II·A General Population Tables 1 and and r Combined Volume. Pan lI·B Primary Census Abstract J Part III General Economic Tables. -

World Bank Document

Procurement Plan for Punjab RWSS (P150520) I. General 1. Bank’s approval Date of the procurement Plan 2012 Public Disclosure Authorized 2. Date of General Procurement Notice: [October 01, 2014 ] 3. Period covered by this procurement plan: January 2017 onwards II. Goods and Works and non-consulting services. 1. Prior Review Threshold: Procurement Decisions subject to Prior Review by the Bank as stated in Appendix 1 to the Guidelines for Procurement: 2. Procurement Method Prior Review Threshold US$ 1. ICB and LIB (Goods) Above US$ 500,000 2. NCB (Goods) Above US$ 100,000 3. ICB (Works) Above US$ 40 million Public Disclosure Authorized 4. NCB (Works) Above US$ 10 million 5. (Non-Consultant Services) Below US$ 100,000 2. Prequalification for Bidders _Not applicable_ 3. Proposed Procedures for CDD Components (as per paragraph. 3.17 of the Guidelines: NA 4. Reference to (if any) Project Operational/Procurement Manual: Project Implementation Manual for World Bank Loan Project P150520 Public Disclosure Authorized 5. Any Other Special Procurement Arrangements: In addition, the justification for all contracts to be issued on the basis of LIB, single-source or direct contracting (except for contracts less than US$50,000 in value) will be subject to prior review. Justification for all contracts to be issued on the basis of LIB, single-source or direct contracting (except for contracts less than US$50,000 in value) will be subject to prior review. III. Selection of Consultants 1. Prior Review Threshold: Selection decisions subject to Prior Review by Bank as stated in Appendix 1 to the Guidelines Selection and Employment of Consultants: Public Disclosure Authorized Selection Method Prior Review Threshold 1. -

For the Quarter Ending 31-03-2012. Monitoring of Approved Proposals (Under Forest Conservation Act,1980)

FOR THE QUARTER ENDING 31-03-2012. MONITORING OF APPROVED PROPOSALS (UNDER FOREST CONSERVATION ACT,1980) Sr. No. GOI Name of the project Category Circle Division GOVT OF INDIA APPROVAL Forest area STIPULATIONS Financial IMPLEMENTATION OF STIPULATION Amount spent Code DATE diverted ORDER NO Compensatory Afforestation amount to be Funds made Area afforestated. up to the R E M A R K S On Forest Land On Non- deposited by available On Forest Land On Non of reporting forest User Agency. by the User forest quarter Area Plants land Agency Area Plants land ha ha ha {Rs,} (Rs.) 12 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 15Setting up of BSF Check Post Amritsar Check Post Bist Amritsar 8-15/FRI Const. 08-Sep-86 1.71000 1.7100 18000 18000 1.7100 18,000 Compensatory A Division afforestation has been done on kamalpur in Ajnala range 21Alignment of 132 KV D/C line Electricity Line Shiwalik Ropar 8-233/83-FC 29-Nov-83 2.25000 5.0000 57245 57245 5.0000 57,245 Plantation done with A Govt funds but this amount deposited in Revenue head. 33Const. Of Head Regulator for Ropar Thermal Thermal Plant Shiwalik Ropar 8-111/84-FRY 30-Apr-84 1.00000 2.0000 57800 57800 2.0000 57,800 Plantation done with A Plant departmenatl funds and funds (Rs. 2000) asked from user agency. 44220 KV Ganguwal-Patiala Tr Line in Ropar Electricity Line Shiwalik Ropar 8-1/3/84 08-Jan-85 0.08000 2.0000 2313 2313 2.0000 2,313 Balance amount will A be spent on maintenance 56Diversion of 9.6 ha P.F. -

Village & Townwise Primary Census Abstract, Kapurthala, Part XIII-A & B

CENSUS 1981 PART XIII-A & B VILLAGE & TOWN DIRECTORY SERIES 17 PUNJAB VILLAGE & TOWNWISE PRIMARY CENSUS ABSTRACT KAPURTHALA DISTRICT DISTRICT CENSUS HAND BOOK D. N. DHIR OF THE INDIAN ADMINISTRATIVE SERVICE Director Of Census Operations PUNJAB PUNJAB DISTRICT KAPURTHALA 10 15 20 KILOMETRES '\;:; z » >< o \ o » ::0 IJRBAN CENTRE WITH POPlJlATION / SIZE CLASS CLASS POPULATION BOUNDARY DISTRICT" . _._._._ TAHSIL -@'-@' H EAOO\JARTERS DISTRICT. TAHSIL . " I 100.000 AND ABOVE NATIONAL HIGHWAY . NHI IMPORTANT METALLED ROAO . ~O . OOO 99.999 II RAILWAY LINE. BROAO GAUGE " •e WITH STATION .... -_ e m 20.000 49.999 RIVER AND STREAM "~ G:;; POST AND TELEGRAPH OFFICE . " PTO lll' 10.000 19.999 DEGREE COllEGE AND [iJ 11' 5.000 9.999 TECHNICAL INSTITUTION .. • • REST HOIJSE RH •• 'l1I BELOW 5.000 DISTIlICT H.a . IS AlSO TAHSIL H.a. CENSUS.oF IONIA-19M1 A--C:::;ENTRAL GOVERNMENT PUBLICA TlONS Part I A Administration Report Enumeration (printed) Part I B Administration Report Tabulation Part II A General Population Tables (Printed) Part II B Primary Census Abstract Part III General Economic Tables Part IV Sbcial and Cultural Tables Part v Migration Tables Patt VI Fertility Tables Part VIi Tabies on Houses and Disabled Population Part VIiI Household Tables Part IX Special Tables on Scheduled Castes and Scheduled Tribes Part X A T own Directory Part X B Survey Report on Selected Towns Part XC Survey Report on Selected Villages Part XI Ethnographic Notes and Special Studies on Scheduled Castes and Scheduled Tribes B-STATE GOVERNMENT PUBLICATIONS Part XIII District Census Handbook for each district Part XIII A Village and Town Directory Part XIII B Village and Town-wise Primary Census Abstract (ii) CONTENTS Pages 1. -

Sultanpur Lodhi Sr

Villages and Category District Kapurthala Block Sultanpur Lodhi Sr. No. Name of village/Gram Panchayat Kandi BET SC 1 Ahli Kalan Yes 2 Alla Ditta 3 Allah Dad Chak Yes 4 Amarjitpur 5 Amanipur Yes 6 Alluwal 7 Amritpur Yes 8 Ahmedpur Yes 9 Ahli Khurd Yes 10 Bhago Budha Yes 11 Baoopur Jadid Yes 12 Bhago Arian 13 Burewal Yes Yes 14 Bhaini Hassa Khan Yes 15 Baja Yes Yes 16 Basti Rangilpur 17 Bhaur 18 Basti Amar Kot 19 Bidhipur Yes 20 Basti Jangla 21 Boolpur 22 Bhagatpur 23 Bussowal 24 Basti Meerpur 25 Bharoana Yes 26 Chananwindi Yes 27 Chauladha Yes 28 Chuharpur 29 Chak Kotla 30 Dandupur 31 Dandwindi 32 Dariawal 33 Daula Yes 34 Dalla Yes 35 Deepewal Yes 36 Dera Saidan Yes 37 Doda Wazir Yes Block-Villages-Kapurthala Sultanpur Lodhi 1 Villages and Category Sr. No. Name of village/Gram Panchayat Kandi BET SC 38 Farid Sairai Yes 39 Fattowal 40 Fauji Colony Randhirpur 41 Fattuwal 42 Fauji Colony Mahablipur 43 Gazipur 44 Gill 45 Haibitpur Yes 46 Hussainpur Dulowal Yes Yes 47 Hyderabad Bet Yes 48 Hajipur Yes Yes 49 Hussainpur Bulle Yes 50 Hazara Yes 51 Jainpur 52 Jeorgepur 53 Jabbo Sudhar 54 Jabbowal 55 Jhal Lahiwala 56 Jhanduwal Kamboan 57 Kalru Yes 58 Kabirpur Yes 59 Kamalpur Yes 60 Karamjitpur 61 Khokar Jadid Kadim 62 Kutbewal Yes 63 Khurd 64 Latianwala 65 Lodhiwal 66 Ladwal 67 Lakh Warah Yes Yes 68 Mahijitpur Yes 69 Miani Bahadur Yes 70 Mirzapur Yes 71 Mahablipur 72 Mewa Singh Wala 73 Mangopur 74 Masit Yes 75 Muket Ramwala 76 Mokhe Block-Villages-Kapurthala Sultanpur Lodhi 2 Villages and Category Sr. -

World Bank Document

Procurement Plan for Punjab RWSS (P150520) I. General 1. Bank’s approval Date of the procurement Plan 2012 Public Disclosure Authorized 2. Date of General Procurement Notice: [October 01, 2014 ] 3. Period covered by this procurement plan: January 2017 onwards II. Goods and Works and non-consulting services. 1. Prior Review Threshold: Procurement Decisions subject to Prior Review by the Bank as stated in Appendix 1 to the Guidelines for Procurement: 2. Procurement Method Prior Review Threshold US$ 1. ICB and LIB (Goods) Above US$ 500,000 2. NCB (Goods) Above US$ 100,000 3. ICB (Works) Above US$ 40 million Public Disclosure Authorized 4. NCB (Works) Above US$ 10 million 5. (Non-Consultant Services) Below US$ 100,000 2. Prequalification for Bidders _Not applicable_ 3. Proposed Procedures for CDD Components (as per paragraph. 3.17 of the Guidelines: NA 4. Reference to (if any) Project Operational/Procurement Manual: Project Implementation Manual for World Bank Loan Project P150520 Public Disclosure Authorized 5. Any Other Special Procurement Arrangements: In addition, the justification for all contracts to be issued on the basis of LIB, single-source or direct contracting (except for contracts less than US$50,000 in value) will be subject to prior review. Justification for all contracts to be issued on the basis of LIB, single-source or direct contracting (except for contracts less than US$50,000 in value) will be subject to prior review. III. Selection of Consultants 1. Prior Review Threshold: Selection decisions subject to Prior Review by Bank as stated in Appendix 1 to the Guidelines Selection and Employment of Consultants: Public Disclosure Authorized Selection Method Prior Review Threshold 1. -

ITEM 1.11B- NEW LINK ROADS 2006-07 1 Amritsar 330 330 333.81

ITEM 1.11B- NEW LINK ROADS 2006-07 As on 26-6-2006 Proposal recd from DCs SN District KM Length Approval by MB (KM) Cost in Rs. Lac Completed Remarks as on 26/6/06 1 Amritsar 330 330 333.81 3948.93 2 Bathinda 110 110 112.17 1383.52 3 Faridkot 52 52 53.38 575.89 4 Fatehgarh Sahib 92 92 92.04 1010.21 5 Ferozepur 226 226 228.61 2751.99 6 Gurdaspur 368 368 372.78 5458.62 Lists of Garhdiwal, Mahilpur & 7 Hoshiarpur 272 166 166.97 1903.62 Tanda not received 8 Jalandhar 218 218 217.57 2348.57 Works being taken up 9 Kapurthala 142 142 143.16 1646.46 in hand. Loan is being 10 Ludhiana 232 232 232.74 2685.98 raised. 11 Mansa 82 82 83.46 982.28 12 Moga 86 86 86.44 912.63 13 Muktsar 84 84 85.66 1029.92 14 Nawanshaher 104 104 96.03 997.40 15 Patiala 230 230 230.67 2612.73 16 Ropar 136 136 139.00 1712.51 17 SAS Nagar 28 28 28.15 350.98 Lists of Dhuri & Sangrur not 18 Sangrur 222 168 168.91 1877.93 received Total 3014 2854 2871.55 34190.17 Annexures23-05-2006 Annex 1.11B- New Links 2006-07 1 ITEM 1.11 A- CONSTRUCTION OF NEW LINK ROADS 2005-06 As on 26-6-2006 Proposals recd Under Jurisdiction of PMB Under Jurisdiction of PWD Comlpetion Status Approval by Cost in Rs. SN District KM Length from DCs as Remarks MB (KM) Lac TS Length Completed %age TS Length Completed %age Total %age on 26.06.06 in KM length (KM) completion in KM length (KM) completion Length completion 1 Amritsar 162 162 166.59 1544.54 111.00 53.13 47.86% 71.57 7.70 10.76% 60.83 33.32% 2 Bathinda 55 55 56.47 576.20 1.50 0.00 0.00% 54.97 14.29 26.00% 14.29 25.31% 3 Faridkot 26 26 27.48 275.90