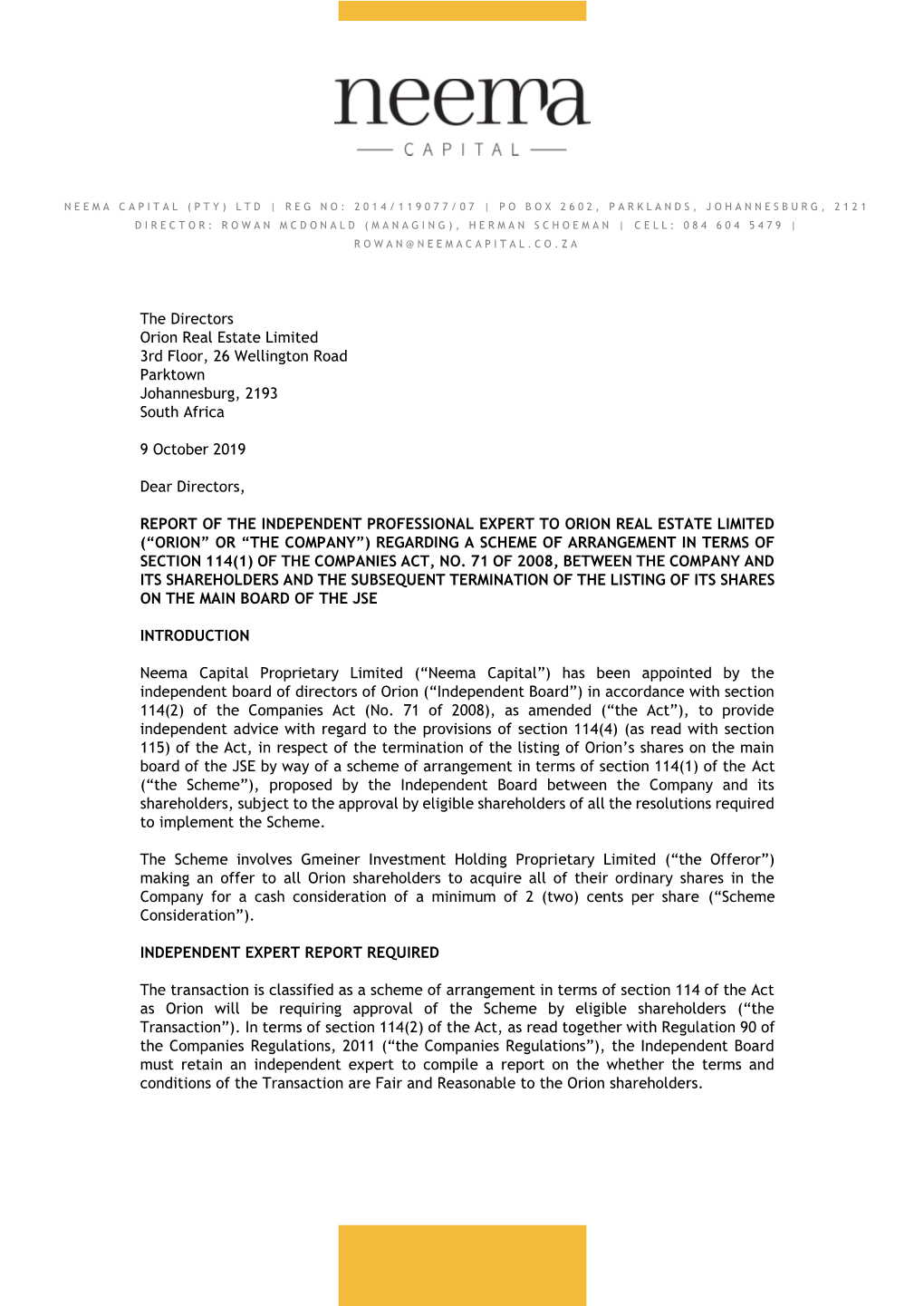

Fair Reasonable Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Map Showing Proposed Feeder Zone Of

n Nooitgedacht Bloubosrand e Fourways Kya Sand SP p D p o MapA sHhowing Proposed Feeder Zone of : RAND PARK HIGo H SCJHohOanOneLsb 7ur0g0151241 lie Magaliessig tk u s B i North g e Hoogland l L W e W a y s Norscot i e ll r Cosmo City ia s Noordhang Jukskei m N a n i N a r Park u Douglasdale i d a c é o M North l Rietfontein AH Sonnedal AH Riding AH Bryanston District Name: JN Circuit No: 4 North Riding G ro Cluster No: 2 sv Bellairs Park en Jackal or Address: Creek Golf Northworld AH d 1 J n a a Estate Olivedale c l ASSGAAI AVE a r n r o Northgate a e t n b s RANDPARK RIDGE EXT1 Zandspruit SP da n m a u y Rietfontein AH r RANDPARK RIDGE Sharonlea C s B n y Vandia i a H a o Sundowner Hunters K Grove m M e e Zonnehoewe AH Hill A. h s Roodekrans Ext c t Legend u e H. SP o Beverley a AH F d Country s. e Gardens er r Life Ruimsig Noord et P School P Bryanbrink Park Sundowner Northworld Sonneglans Tres Jolie AH Laser Park t Kensington B Proposed Feeder r ord E Alsef AH a xf t Ruimsig w O o Zone Ruimsig AH .S Strijdompark n Lyme Park .R Ambot AH C Bond Bromhof H New Brighton a Other roads n s Boskruin Eagle Canyon s Schoeman S Han t Hill Ferndale Kimbult AH r ij Major roads Poortview t d Hurlingham e ut o Willowbrook ho m AH W r d Bordeaux e Harveston AH st Malanshof r e Y e r d o Willowild Subplaces uge R Kr Randpark ep w ul n ub Pa lic r a s e a Ridge Ruiterhof h i R V c t a Amorosa Aanwins AH i ic b N r Honeydew s ie k i i Glenadrienne SP1 e r r d e Ridge h President d i Jo Moret n Craighall Locality in Gauteng Province C hn Vors Fontainebleau D ter Ridge e H J Wilro Wilgeheuwel a J n Radiokop . -

Legal Notices Wetlike Kennisgewings

Vol. 550 Pretoria, 21 April 2011 No. 34217 LEGAL NOTICES WETLIKE KENNISGEWINGS SALES IN EXECUTION AND OTHER PUBLIC SALES GEREGTELIKE EN ANDER QPENBARE VERKOPE 2 NO.34217 GOVERNMENT GAZETTE, 21 APRIL 2011 IMPORTANT NOTICE The Government Printing Works will not be held responsible for faxed documents not received due to errors on the fax machine or faxes received which are unclear or incomplete. Please be advised that an "OK" slip, received from a fax machine, will not be accepted as proof that documents were received by the GPW for printing. If documents are faxed to the GPW it will be the sender's respon sibility to phone and confirm that the documents were received in good order. Furthermore the Government Printing Works will also not be held responsible for cancellations and amendments which have not been done on original documents received from clients. TABLE OF CONTENTS LEGAL NOTICES Page SALES IN EXECUTION AND OTHER PUBLIC SALES ....... .... ............. ........... 9 Sales in execution: Provinces: Gauteng....... ................. .......... ....................... ................. 9 Eastern Cape ...... .................. ............................. ............. 27 Free State....................... .......................... ...................... 30 KwaZulu-Natal ................................................................ 31 Limpopo .......................................................................... 43 Mpumalanga ........ ..................... ............................. ......... 44 Northern Cape................................................ -

35885 23-11 Legalap1 Layout 1

Government Gazette Staatskoerant REPUBLIC OF SOUTH AFRICA REPUBLIEK VAN SUID-AFRIKA Vol. 569 Pretoria, 23 November 2012 No. 35885 PART 1 OF 2 LEGAL NOTICES A WETLIKE KENNISGEWINGS N.B. The Government Printing Works will not be held responsible for the quality of “Hard Copies” or “Electronic Files” submitted for publication purposes AIDS HELPLINE: 0800-0123-22 Prevention is the cure 201513—A 35885—1 2 No. 35885 GOVERNMENT GAZETTE, 23 NOVEMBER 2012 IMPORTANT NOTICE The Government Printing Works will not be held responsible for faxed documents not received due to errors on the fax machine or faxes received which are unclear or incomplete. Please be advised that an “OK” slip, received from a fax machine, will not be accepted as proof that documents were received by the GPW for printing. If documents are faxed to the GPW it will be the sender’s respon- sibility to phone and confirm that the documents were received in good order. Furthermore the Government Printing Works will also not be held responsible for cancellations and amendments which have not been done on original documents received from clients. TABLE OF CONTENTS LEGAL NOTICES Page BUSINESS NOTICES.............................................................................................................................................. 11 Gauteng..................................................................................................................................................... 11 Eastern Cape............................................................................................................................................ -

Learning Curve 8% Offer Campuses

Learning Curve 8% Cash Back offer for student licence purchases made using Virgin Money Spot - Available for the following campuses: Name Address AAA School of Advertising 1st Floor, Bond Street Centre, Cnr Bram Fischer Drive & Bond Street, Kensington B, Randburg, 2194 BHC School of Design 72 Salt River Road, Woodstock, Cape Town, 7925 Boston City Campus & Business College 247 Louis Botha Avenue, Orchards, Orange Grove, Johannesburg 2192 Boston Media House 137, 11th Street,Parkmore, Johannesburg 2196 Cape Town College of Fashion Design 7 Delaney Road, Plumstead, Cape Town, 7801 Cape Town Creative Academy The Old Biscuit Mill, 375 Albert Road, Woodstock, Cape Town, 7915 Capricorn TVET College Die Meer Street,Polokwane 0699 Centurion Akademie - Rustenberg 39 Heystek Street, Rustenburg Centurion Academy 1023 Bank Avenue Centurion City Varsity Cape Town Coastal KZN FET College 1 Jameson Crescent, Congella, 4013, Durban Concept Interactive COMMUNITYWest Block, Tannery ARTS CENTRE, Park, 23 LEONARD Belmont AUALA Road, Rondebosch,STREET, WINDHOEK, Cape Town, NAMIBIA 7700 College of The Arts (Reseller: PC Centre) CTU Training Solutions Unit 26, Garsfontein Office Park, 645 Jacqueline Drive, Pretoria, 1788 Design Academy of Fashion 208 Albert Road, Woodstock, Cape Town, 7925 East London Management Institute 231 Oxford Street, East London, 5201 Elizabeth Galloway Fashions Techno Road, 26 Techno Avenue, Stellenbosch, 7600 Faculty Training Institute CT Faculty Training Institute Joburg Fedisa 81 Church Street, Cape Town, 8001 Friends of Design Business -

Region B Contact & Information Directory

REGION B CONTACT & INFORMATION DIRECTORY UPDATED JANUARY 2016 REGION B CONTACT & INFORMATION DIRECTORY: JANUARY 2016 INDEX NAME PAGE Emergency Numbers …………………………………………………………………… 1 Head Office Staff A – Z …………………………………………………………………… 1 – 6 Ward Councillors …………………………………………………………….…….. 6 -7 Ward Governance Administrators …………………………………………………………………… 8 PR Councillors …………………………………………………………………… 8 Group Citizen Relationship & Urban Management (CRUM): Head Office …………………………… 8 - 9 Regional Directors A – G …………………………………………………………... 9 - 10 Citizen Relationship & Urban Management Management Support …………………………………………………… 10 Area Based Management …………………………………………………… 11 Citizen Relationship Management …………………………………………………... 11 Integrated Service Delivery …………………………………………………... 12 Planning, Profiling & Data Management …..……………………………………… 12 Health Community Health Clinics …………………………………………………… 13 – 14 Environmental Health …………………………………………………… 15 – 18 Housing …………………………………………………………………… 19 Libraries …………………………………………………………………… 20-21 Social Development TDC (Transformation & Development Centre) ………………………………………… 22 Techno Centre …………………………………………………………………… 23 Sport and Recreation Recreation …………………………………………………………………… 23 Recreation Centres …………………………………………………………………… 24 NAME PAGE Sport …………………………………………………………………… 25 Sports Clubs & Stadiums …………………………………………………………………… 25 – 26 Aquatics …………………………………………………………………… 26 Swimming Pools …………………………………………………………………… 26 – 27 Group Finance Revenue Shared Services Centre ………………………………………………….. 27 Development Planning Building Control -

R0160/19 Re-Advert Description of Print and Supply of Sect

City of Johannesburg Supply Chain Management Unit SUPPLIER NAME: _______________________________________________ REQUEST FOR QUOTATION FOR GOODS AND SERVICES FOR THE CITY OF JOHANNESBURG Procurement Less than R 200 000 (Including Vat) (For publication on the City of Johannesburg Notice Board/s & Website) The City of Johannesburg requests your quotation on the goods and/or services listed hereunder and/or on the available RFQ forms. Please furnish all information as requested and return your quotation on the date stipulated. Late and incomplete submissions will invalidate the quotation submitted. ADVERTISEMENT DATE 13 FEBRUARY 2019 DEPARTMENT JMPD RFQ NUMBER: R0160/19 RE-ADVERT DESCRIPTION OF PRINT AND SUPPLY OF SECT. 56 BY-LAW BOOKS FOR JMPD GOODS/SERVICES The COJ Website – www.joburg.org.za/quotations RFQ SPECIFICATION FORMS/ DOCUMENTS ARE OR OBTAINABLE FROM: FROM INFORMATION DESK 15TH FLOOR METRO CENTRE 158 Civic Boulevard street BRAAMFONTEIN COMPULSORY PLEASE NOTE THAT NOT SUBMITTING THE COMPULSORY REQUIREMENTS DOCUMENTS MAY LEAD TO DISQUALIFICATION. ADDITIONAL COMPULSORY SAMPLES WILL BE REQUESTED FROM SHORTLISTED REQUIREMENTS SUPPLIERS COMPULSORY BRIEFING 15 FEBRUARY 2019 DATE: 13H00 PM TIME: BOARDROOM: FINES ADMINISTRATION, VENUE: B-BLOCK , ROOM 22 , C/o VILLAGE RD. & ELOFF EXT.JMPD QUOTATION BOX, GROUND FLOOR, METRO CENTRE SUBMISSION OF QUOTES: 158 Civic Boulevard street, Braamfontein TIME: 10h30 CLOSING DATE 20 FEBRUARY 2019 ENQUIRIES: ELIZE FORTUNE:011 490 - 1618 Quotations above R30 000 will be evaluated on the basis of the 80:20 point system as stipulated in the Preferential Procurement Policy Framework Act (Act number 5 of 2000) & the City’s Supply Chain Management Policies and Procedures. CHECKLIST RFQ NO: R0160/19 RE-ADVERT PLEASE USE THE CHECKLIST TO CONFIRM THAT ALL COMPULSORY DOCUMENTS HAVE BEEN ATTACHED TO YOUR QUOTATION. -

Legal Notices Wetlike Kennisgewings

. October Vol. 652 Pretoria, 18 Oktober 2019 No. 42771 LEGAL NOTICES WETLIKE KENNISGEWINGS SALES IN EXECUTION AND OTHER PUBLIC SALES GEREGTELIKE EN ANDER QPENBARE VERKOPE 2 No. 42771 GOVERNMENT GAZETTE, 18 OCTOBER 2019 STAATSKOERANT, 18 OKTOBER 2019 No. 42771 3 CONTENTS / INHOUD LEGAL NOTICES / WETLIKE KENNISGEWINGS SALES IN EXECUTION AND OTHER PUBLIC SALES GEREGTELIKE EN ANDER OPENBARE VERKOPE Sales in execution • Geregtelike verkope ....................................................................................................... 12 Gauteng ...................................................................................................................................... 12 Eastern Cape / Oos-Kaap ................................................................................................................ 55 Free State / Vrystaat ....................................................................................................................... 57 KwaZulu-Natal .............................................................................................................................. 63 Limpopo ...................................................................................................................................... 80 Mpumalanga ................................................................................................................................ 82 North West / Noordwes ................................................................................................................... 86 Northern -

SAARF OHMS 2006 Database Layout

SAARF OUTDOOR MEASUREMENT SURVEY PRIVATE & CONFIDENTIAL Outdoor Database Layout South Africa (GAUTENG & KWAZULU-NATAL) August 2007 FILES FOR COMPUTER BUREAUX Prepared for: - South African Advertising Research Foundation (SAARF) Prepared by: - Nielsen Media Research and Nielsen Outdoor Copyright Reserved Confidential 1 The following document describes the content of the database files supplied to the computer bureaux. The database includes four input files necessary for the Outdoor Reach and Frequency algorithms: 1. Outdoor site locations file (2 – 3PPExtracts_Sites) 2. Respondent file (2 – 3PPExtracts_Respondents) 3. Board Exposures file (2 – Boards Exposure file) 4. Smoothed Board Impressions file (2 – Smoothed Board Impressions File) The data files are provided in a tab separated format, where all files are Window zipped. 1) Outdoor Site Locations File Format: The file contains the following data fields with the associated data types and formats: Data Field Max Data type Data definitions Extra Comments length (where necessary) Media Owner 20 character For SA only 3 owners: Clear Channel, Outdoor Network, Primedia Nielsen Outdoor 6 integer Up to a 6-digit unique identifier for Panel ID each panel Site type 20 character 14 types. (refer to last page for types) Site Size 10 character 30 size types (refer to last pages for sizes) Illumination hours 2 integer 12 (no external illumination) 24 (sun or artificially lit at all times) Direction facing 2 Character N, S, E, W, NE, NW, SE, SW Province 25 character 2 Provinces – Gauteng , Kwazulu- -

Chapter 1 BOMMASTANDI of ALEXANDRA TOWNSHIP

Chapter 1 BOMMASTANDI OF ALEXANDRA TOWNSHIP 1.1. Background In 1912 the following billboard written in Sotho, Zulu and English appeared in Alexandra Township advertising freehold properties. First, this advert points to the obvious; Africans were already engaging in private property at the turn of the 20th century. This township was subdivided into 2,500 stands which were sold to individuals. Title deeds were given to the individuals once payment was concluded. Second, it indicates that Africans were acquiring private property away from a „traditional village‟ where access to property is said to be communal. A closer look at the acquisition processes of such properties unsettles the notion of private property as individual. It becomes increasingly clear in the study that in spite of the naming of an individual in the titled deed it was not uncommon for family resources to be pooled during acquisition of the said property and hence a shared ownership among members of extended families would be understood. The following conversations attest to some of these experiences. Mme Mihloti explains how her parents and her siblings purchased their properties. 1 Ko 15th o ka re ke nako e abuti a bereka le mosu ausi, ke bona ba neng ba thusa mokgalabe. ......... Bona ke itse ba berekile ba thusa, ba ntshitse chelete ausi le abuti, ena Lucas. …….1 (It seemes like when my brother and sister were working, they are the ones who helped the old man with purchasing the property at 15th Avenue. I do know that they contributed some money helping our father in acquiring the properties…… Another example is drawn from mme Hunadi‟s family. -

Legend South View ! M Stop

± Halfway House Maroeladal Witkoppen Witkoppen Extensions Craigavon Bloubosrand Matika Paulshof Magaliessig Kleve Hill Sunninghill Megawatt Park Park Rivonia Petervale Gardens Woodmead Woodmead Ext Woodmead East Bryanston Rivonia Northgate The Woodlands Sharonlea W i l l i a m N Morningside i c o l D Manor r Sonneglans i v Strydom e Park Kelvin m Sundowner l M a e i o l v a l c i l i i i r b Bryanston N W D Morningside o n g West Ext 1 Wendywood w Kensington B Lyme W e D e Morning Side s L C Honeydew r t e Park i o o v A n r u e e v k g n Extentions Eastgate M e u ds A oodlan e W A A n n V a v v v e n v e l l u i a Avenue i e i e A u b e v l e h Eagle e n a n d D t t n e k n o A r u y a u r e e r n n u i u T e e e a o v e o u v g e i o o r e t f n i e Y n r R w r A i u S Canyon h e o u e u t a P t n r i a d v S n s e e p n an MB 9 - 7 a a H l A e r Hil v r o o an Hi S l P l K A v em H ! B ho a et R i Sc ns Stre S MB 7 - 20 tr t t R Sc A eet h F e s oe v e Sandown Marlboro m ! e r e a A K e ! t MB 8 - 14 n r MB 8 - 13 n MB 7 - 19 v e n S W M e r u ! e n k ! n i i e e n o r u 1 u rd e a 1 Strathavon e Harley a g r n th ch e g v 6 M e S Randburg r u a th tr Gra O n a St v ee ysto ! Street ve W re A t n ! A et MB 8 - 18 Driv MB 8 - 12! S e G B p S E ! MB 7 - 18 a r r a n s u a d G MB 7 - 17 r s Road St to t r F J d a rew n MB 8 - 17 a i And e y e a t St D s o e m ri S r t is R M ews ve o l n n T Andr 5 ! h MB 2 - 19 D n E r A t t r d o a r f ! h r i a b S S a n u v R v R a o a e e a o a i tr i ! Ruiterhof e m n n Wilgeheuwel b R e i n e e -

City of Johannesburg Ward Councillors by Region, Suburbs and Political Party

CITY OF JOHANNESBURG WARD COUNCILLORS BY REGION, SUBURBS AND POLITICAL PARTY No. Councillor Name/Surname & Par Region: Ward Ward Suburbs: Ward Administrator: Cotact Details: ty: No: 1. Cllr. Msingathi Mazibukwana ANC G 1 Streford 5,6,7,8 and 9 Phase 1, Bongani Dlamini 078 248 0981 2 and 3 082 553 7672 011 850 1008 011 850 1097 [email protected] 2. Cllr. Dimakatso Jeanette Ramafikeng ANC G 2 Lakeside 1,2,3 and 5 Mzwanele Dloboyi 074 574 4774 Orange Farm Ext.1 part of 011 850 1071 011 850 116 083 406 9643 3. Cllr. Lucky Mbuso ANC G 3 Orange Farm Proper Ext 4, 6 Bongani Dlamini 082 550 4965 and 7 082 553 7672 011 850 1073 011 850 1097 4. Cllr. Simon Mlekeleli Motha ANC G 4 Orange Farm Ext 2,8 & 9 Mzwanele Dloboyi 082 550 4965 Drieziek 1 011 850 1071 011 850 1073 Drieziek Part 4 083 406 9643 [email protected] 5. Cllr. Penny Martha Mphole ANC G 5 Dreziek 1,2,3,5 and 6 Mzwanele Dloboyi 082 834 5352 Poortjie 011 850 1071 011 850 1068 Streford Ext 7 part 083 406 9643 [email protected] Stretford Ext 8 part Kapok Drieziek Proper 6. Shirley Nepfumbada ANC G 6 Kanama park (weilers farm) Bongani Dlamini 076 553 9543 Finetown block 1,2,3 and 5 082 553 7672 010 230 0068 Thulamntwana 011 850 1097 Mountain view 7. Danny Netnow DA G 7 Ennerdale 1,3,6,10,11,12,13 Mzwanele Dloboyi 011 211-0670 and 14 011 850 1071 078 665 5186 Mid – Ennerdale 083 406 9643 [email protected] Finetown Block 4 and 5 (part) Finetown East ( part) Finetown North Meriting 8. -

35762 12-10 Legalbp1 Layout 1

Government Gazette Staatskoerant REPUBLIC OF SOUTH AFRICA REPUBLIEK VAN SUID-AFRIKA October Vol. 568 Pretoria, 12 2012 Oktober No. 35762 PART 1 OF 2 LEGAL NOTICES B WETLIKE KENNISGEWINGS SALES IN EXECUTION AND OTHER PUBLIC SALES GEREGTELIKE EN ANDER OPENBARE VERKOPE N.B. The Government Printing Works will not be held responsible for the quality of “Hard Copies” or “Electronic Files” submitted for publication purposes AIDS HELPLINEHELPLINE: 08000800-0123-22 123 22 Prevention Prevention is is the the cure cure 200025—A 35762—1 2 No. 35762 GOVERNMENT GAZETTE, 12 OCTOBER 2012 IMPORTANT NOTICE The Government Printing Works will not be held responsible for faxed documents not received due to errors on the fax machine or faxes received which are unclear or incomplete. Please be advised that an “OK” slip, received from a fax machine, will not be accepted as proof that documents were received by the GPW for printing. If documents are faxed to the GPW it will be the sender’s respon- sibility to phone and confirm that the documents were received in good order. Furthermore the Government Printing Works will also not be held responsible for cancellations and amendments which have not been done on original documents received from clients. TABLE OF CONTENTS LEGAL NOTICES Page SALES IN EXECUTION AND OTHER PUBLIC SALES ................................... 9 Sales in execution: Provinces: Gauteng .......................................................................... 9 Eastern Cape.................................................................. 130