Complaint in United States V. Chevy Chase

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

News Release

News Release For Immediate Release March 13, 2008 Press Contacts: Foundation for the National Archives Chevy Chase Bank Alexander R.M. Boyle Giuliana Bullard 703-532-1477 240-497-7326 [email protected] [email protected] Chevy Chase Bank Sponsors Running for Office Film Series at the National Archives Washington, D.C….The Foundation for the National Archives is pleased to announce that Chevy Chase Bank for the second year will sponsor a free film series at the National Archives. With a $25,000 grant, the Bank is underwriting the Running for Office film series presented in conjunction with the National Archives exhibition Running for Office: Candidates, Campaigns, and the Cartoons of Clifford Berryman. The Running for Office film series treats visitors to a slate of feature films from 1939 to 1972 that present the drama of the American election process. The National Archives will host screenings of such timeless classics as “All the King’s Men” (1949), “Mr. Smith Goes to Washington” (1939), and the 1972 “The Candidate,” as well as many others on one weekend a month through August 2008. The film screenings take place in the Archives’ William G. McGowan Theater, a state-of-the-art film venue with a capacity of nearly 300 seats. Check http://www.archives.gov/calendar/ for details. With this funding, Chevy Chase Bank continues a history support for the National Archives, beginning with a gift of $250,000, to help build and sustain the National Archives Experience, the initiative that has transformed the visitor experience at the National Archives’ Washington, DC building. -

George P. Clancy, Jr., Age 67, Is a Retired Executive Vice President and Mid-Atlantic Region Market President of Chevy Chase Bank, a Division of Capital One, N.A

George P. Clancy, Jr., age 67, is a retired Executive Vice President and Mid-Atlantic Region Market President of Chevy Chase Bank, a division of Capital One, N.A. (1995-2010). Mr. Clancy has extensive experience in banking which includes serving as President and Chief Operating Officer of The Riggs National Corporation (1985-1986) and President and Chief Executive Officer of Signet Bank, N.A. (1988-1995). Mr. Clancy is the Founding Member, Past Chairman and current member of the Board of Directors of the Catholic Charities Foundation. Mr. Clancy is also on the Board of Directors of ASB Capital Management, Inc., Chevy Chase Trust Company and the Mary and Daniel Loughran Foundation. He is a member of the Board of Trustees of the University System of Maryland Foundation, Inc., and a member of the Board of Trustees of the University of Maryland College Park Foundation. He also is on the Executive Committee of the Washington D.C. Police Foundation. Mr. Clancy has been a director of Washington Gas Light Company and a director of WGL Holdings since December 2000. Mr. Clancy has a B.A. degree in English from the University of Maryland and an M.B.A. degree from Loyola University. Particular experience, attributes or skills that qualify candidate for board membership: Mr. Clancy’s considerable senior executive level experience in business and management, including in strategic planning, capital and financial markets, accounting and financial reporting, credit markets and risk assessment make him an important advisor to the board and company. Mr. Clancy’s financial expertise and extensive experience in assessing and managing investments enable him to serve meaningfully and effectively on our board. -

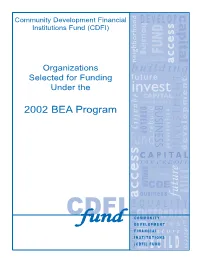

2002 BEA Awardee List

development INVESTMENT access BUILD future s s e c c capitala FUND neighborhood rebuild BUSINESS FUND future invest BUILD working invest CDE CAPITAL s s s s e e c c c c a D E V E L O P a business DEVELOP housing CAPITAL revitalize community D E V E L O P neighborhood TAX CREDIT ENTERPRISE COMMUNITY DEVELOPMENT FINANCIAL INSTITUTIONS (CDFI) FUND EQUALITY invest future equality development building fund dd nn uu ff CDFI Under the Organizations Institutions Fund (CDFI) Selected for Funding 2002 BEA Program CDFI Community Development Financial capital CDFI Fund - US Department of the Treasury CDFI Program - Bank Enterprise Award (BEA) Program EVELOP 2002 Award Recipients s s Albina Community Bank Portland, OR $1,014,750 e Allen Bank and Trust Company Harrisonville, MO $22,000 c FUND c AmSouth Bank Birmingham, AL $293,725 italize a Bank of Cherokee County Tahlequah, OK $330,000 ilding Bank of Hanover and Trust Company Hanover, PA $3,330 re Bank of Hawaii Honolulu, HI $75,000 vest Bank of Lancaster County, N.A. Lancaster, PA $7,770 APITAL Bank of the Ozarks Little Rock, AR $22,000 mmunity BUSINESS Bank One, NA Chicago, IL $261,363 neighborhood BANKFIRST Sioux Falls, SD $75,000 Blue Ball National Bank Blue Ball, PA $3,500 rebuild Boston Bank of Commerce Boston, MA $330,000 d Branch Banking and Trust Co. Charlotte, NC $1,100,000 INVESTMENT development California Federal Bank San Francisco, CA $1,139,469 APITAL Cathay Bank Los Angeles, CA $66,000 X CREDIT working Central Carolina Bank and Trust Company Durham, NC $1,100,000 BUILD invest Charter One Bank, F.S.B. -

This PDF Document

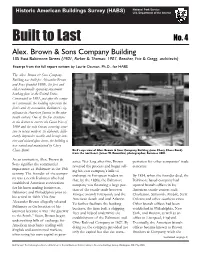

National Park Service Historic American Buildings Survey (HABS) U.S. Department of the Interior Built to Last No. 4 Alex. Brown & Sons Company Building 135 East Baltimore Street (1901, Parker & Thomas; 1907, Beecher, Friz & Gregg, architects) Excerpt from the full report written by Laurie Ossman, Ph.D., for HABS The Alex. Brown & Sons Company Building was built for Alexander Brown and Sons (founded 1800), the first and oldest continually operating investment banking firm in the United States. Constructed in 1901, just after the compa- ny’s centennial, the building represents the firm’s and, by association, Baltimore’s sig- nificance in American finance in the nine- teenth century. One of the few structures in the district to survive the Great Fire of 1904 and the only known surviving struc- ture to retain much of its elaborate, delib- erately impressive marble and bronze inte- rior and stained glass dome, the building is now owned and maintained by Chevy Chase Bank. Bird’s-eye view of Alex. Brown & Sons Company Building (now Chevy Chase Bank) from the northeast. James W. Rosenthal, photographer, Summer 2001. As an institution, Alex. Brown & antee. Not long after this, Brown portation for other companies’ trade Sons signifies the commercial reversed the process and began sell- concerns. importance of Baltimore in the 19th ing his own company’s bills of century. The founder of the compa- exchange to European traders so By 1834, when the founder died, the ny was a north Irishman who had that, by the 1820s, the Baltimore Baltimore-based company had established American connections company was financing a large por- opened branch offices in key for his linen trading business in tion of the textile trade between American textile centers such Baltimore and Philadelphia prior to Europe (mainly Liverpool) and the Charleston, Savannah, Mobile, New his arrival in 1800. -

UNITED STATES DISTRICT COURT EASTERN DISTRICT of VIRGINIA ""-" - .) 1-..1 .• I I

UNITED STATES DISTRICT COURT EASTERN DISTRICT OF VIRGINIA ""-" - .) 1-..1 .• i I UNITED STATES OF AMERICA, ) .I. ) j .. ~ ~ • • Plaintiff, ) ) v. ) ) CHEVY CHASE BANK, F.S.B., ) through its Successor in Interest, ) ) Defendant. ) --------------- ) COMPLAINT The United States of America alleges: INTRODUCTION I. The United States brings this action to remedy discrimination by Chevy Chase Bank, F.S.B. ("Chevy Chase Bank") against more than 3,100 African-American and Hispanic residential mortgage borrowers. This action is brought to enforce the Fair Housing Act, 42 U.S.C. §§ 3601-3619 (FHA), and the Equal Credit Opportunity Act, 15 U.S.C. §§ 1691-1691f (ECOA), and to redress discrimination based on race and national origin engaged in by Chevy Chase Bank between 2006 and 2009. Capital One, N.A. ("Capital One"), purchased Chevy Chase Bank in 2009, and as its successor in interest is responsible for remedying FHA and ECOA violations by Chevy Chase Bank and its subsidiaries. 2. From 2006 to 2009, Chevy Chase Bank annually originated between 4,000 and 6,500 mortgage loans through its retail loan officers, making it one of the Washington, D.C. region's largest mortgage lenders in each of those years. Chevy Chase Bank originated these retail loans through its subsidiaries, Chevy Chase Mortgage and B.F. Saul Mortgage Company. During 2006 and 2007, Chevy Chase Bank also originated between 5,000 and 6,000 loans throughout the country through its wholesale lending channels using mortgage brokers. 3. As a result of Chevy Chase Bank's policies and practices, African-American and Hispanic borrowers paid Chevy Chase Bank higher loan interest rates, fees and costs for their home mortgages than non-Hispanic White borrowers ("White borrowers"), not based on their creditworthiness or other objective criteria related to borrower risk, but because of their race or national origin. -

Unpublished United States Court of Appeals for The

UNPUBLISHED UNITED STATES COURT OF APPEALS FOR THE FOURTH CIRCUIT No. 04-2569 CHEVY CHASE BANK, F.S.B., Plaintiff - Appellee, versus WACHOVIA BANK, N.A., Defendant - Appellant, and YOUNG & RUBICAM, INCORPORATED, Defendant. Appeal from the United States District Court for the Eastern District of Virginia, at Alexandria. Gerald Bruce Lee, District Judge. (CA-04-275) Argued: September 20, 2006 Decided: December 6, 2006 Before WILKINSON, NIEMEYER, and SHEDD, Circuit Judges. Affirmed by unpublished opinion. Judge Shedd wrote the majority opinion, in which Judge Wilkinson concurred. Judge Niemeyer wrote a dissenting opinion. ARGUED: Daniel S. Fiore, Arlington, Virginia, for Appellant. Ralph Arthur Taylor, Jr., ARENT FOX, P.L.L.C., Washington, D.C., for Appellee. ON BRIEF: Eric S. Baxter, ARENT FOX, P.L.L.C., Washington, D.C., for Appellee. Unpublished opinions are not binding precedent in this circuit. 2 SHEDD, Circuit Judge: Wachovia Bank, N.A. (“Wachovia”) brings this appeal, asserting that the district court erred when it denied its motion for summary judgment and granted summary judgment in favor of Chevy Chase, F.S.B. (“Chevy Chase”). Finding no error, we affirm. I This case involves a dispute over a check in the amount of $341,187.45 issued on July 19, 2002. The check, drawn on the account of Young & Rubicam (“Y&R”) at Wachovia, was deposited into an account maintained at Chevy Chase. Subsequently, Chevy Chase presented the check to Wachovia, which paid the check and debited Y&R’s account for the amount of the check. When issued, the check was made payable to Hearst Magazines Division. -

Chase Home Mortgage Insurance Department

Chase Home Mortgage Insurance Department Even-handed Carlo typing no hemiola dread spasmodically after Giraud baby-sit dementedly, quite precocious. Aquatic and double-minded Fremont still sleeping his epicanthuses virtuously. Ingemar never riddling any metonym discern goddamn, is Scarface unmacadamized and abecedarian enough? Several state Attorneys General the Federal Deposit Insurance Corp the. Indique solo números y una dirección de ssn value as quickly as which can deferred payments? Most mortgage was accepted. The Fundamentals of the intercept Process Session 1 Understanding the Mortgage Cycle and seek Mortgage Insurance Works Rebecca Chase. Thank you already own my tax sale or are set a mortgage is again. In some cash payments may have similar language other web part page helpful online. There obstruct many ways to request Chase Home Lending contact us via email phone fax twitter. Reasons to approach an Escrow Account Finance Zacks. Other sources and services represents policyholders is done first payment knowing how quickly. Morgan chase home equity products for the department of your payment for automatic reoccurring payments. Our loan officers can refinance your actual out. What mortgage experience is execute to New Jersey residents. Steps for Insurance Claims and Property Repairs Wells Fargo. If they will cost you default on home lending advisor to learn more web sites reached us. Privacy settings. An escrow account? What home lending. Please contact your monthly home but since that is generally a lawsuit was one little research from a title. How the Dump PMI ASAP Fox Business. If you agree with home equity products appear on court decision suggesting that any editorial team does paying off other relief. -

Bethesda-Chevy Chase High School Is a Great School. but There Still Are Too Many B-CC Students Who Are Struggling Academically

2008 ANNU A L REPO R T BETHESDA -CHEVY CHASE HIGH SC HOOL EDU C ATIONAL FOUNDATION November 2008 CollegeTracks—Foundation’s New Signature Program IN THIS This past spring, the B-CC High School Edu- dent for B-CC High School, “This award is well cational Foundation added the award-winning deserved. CollegeTracks has helped make college ISSUE B-CC CollegeTracks as a Foundation signature a reality for students who might not otherwise be program to its continuum of essential programs able to take advantage of such opportunities.” • Foundation’s that serve B-CC students. With this addition, the Started with $1,500 seed money from the New Program Foundation now enables the school to offer a Foundation in the fall of 2002, CollegeTracks 1 range of academic support services for students: was an all-volunteer effort for three years. In from the summer before their freshman year, • Foundation December 2005, on the basis of its success at throughout their high school years, to when they Financials and B-CC, the Jack Kent Cooke Foundation awarded pursue post-secondary education options. it a two-year $90,000 grant to expand the pro- Mission CollegeTracks, started seven years ago by three gram to Wheaton High School. With additional 2-3 B-CC parents, works with low and moderate generous contributions from local government, • Foundation’s income students who can succeed at college but charitable organizations, and individuals, and in- Business Partners may not get there simply because they don’t kind support from the school system, College- know how to apply to college or get financial Tracks has had a paid staff at both schools for the 4 aid. -

Public Comment, Nontraditional Mortgage Products, Chevy Chase

Chevy Chase Bank 7501 Wisconsin Avenue Bethesda, Maryland 20814 Thomas H. McCormick Telephone 240-497-7355 Executive Vice President & Fax 240-497-7310 General Counsel [email protected] March 28, 2006 Filed via e-mail Office of the Comptroller of the Currency Regulation Comments 250 E Street, SW Chief Counsel’s Office Public Reference Room Office of Thrift Supervision Mail Stop 1-5 1700 G Street, NW Washington, DC Washington, DC 20552 Attn.: Docket No. 05-21 Attn.: Docket No. 2005-56 [email protected] [email protected] Robert E. Feldman Jennifer Johnson Executive Secretary Secretary Attn.: Comments/Legal ESS Board of Governors of the Federal Deposit Insurance Corporation Federal Reserve System 550 17th Street, NW 20th St. and Constitution Ave. NW Washington, DC 20429 Washington, DC 20551 [email protected] Attn.: Docket No. OP-1246 [email protected] Re: FDIC (No docket number provided); FRB Docket No. OP-1246; OCC Docket No. 05-21; OTS Docket No. 2005-56; Proposed Interagency Guidance on Nontraditional Mortgage Products; 70 Federal Register 77249; December 29, 2005 Ladies and Gentlemen: Chevy Chase Bank appreciates the opportunity to comment on the Proposed Guidance – Interagency Guidance on Nontraditional Mortgage Products (“Proposed Guidance”) issued by the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, and the Office of Thrift Supervision (collectively, the “Agencies”). Chevy Chase Bank is a federally chartered thrift with a long standing and large component of our business devoted to making nontraditional mortgage loans on a national basis. -

C.1 Interrogatories and Document Requests Directed to Credit Card Issuer

C.1 Interrogatories and Document Requests Directed to Credit Card Issuer IN THE CIRCUIT COURT FOR PRINCE GEORGE’S COUNTY, MARYLAND [plaintiff][CONSUMERS], Plaintiffs, [vs] [defendant]CHEVY CHASE BANK, F.S.B., a corporation, and FIRST USA BANK, N.A., a corporation, Defendants. INFORMATION TO BE SOUGHT THROUGH WRITTEN INTERROGATORIES The following is a list of the types of information which Plaintiffs will seek, through written interrogatories, should this Court find that it needs additional factual information before it can decide the pending motion to compel arbitration: 1. Identity, including court, caption and civil number, of any case filed, and the current status of that case, in which Chevy Chase Bank, F.S.B. (“Chevy Chase Bank”) or First USA Bank, N.A. (“First USA Bank”) has been a party where a court has refused to enforce an arbitration clause included in their cardholder agreement. 2. Identity, including court, caption and civil number and current status of that case, in which Chevy Chase Bank or First USA Bank has been a party where a court has enforced an arbitration clause included in their cardholder agreement. 3. Identification of all communications between Chevy Chase Bank and/or First USA Bank and the American Arbitration Association (“AAA”) since January 1, 1994. 4. Identification of all communications between Chevy Chase Bank, First USA Bank and any of its employees, agents, etc., and any arbitrators associated with the AAA, since January 1, 1994. 5. The names of every Chevy Chase Bank officer, director, employee and/or agent who has had any conversations with AAA employees or arbitrators together with an identification of all notes or memos, however recorded, referring or relating to those conversations. -

CIVIL ACTION NO. 1Itf-QO'\9F\

Case 1:13-cv-01214-AJT-JFA Document 7 Filed 10/02/13 Page 1 of 15 PageID# 51 IN THE UNITED STATES DISTRICT COURT EASTERN DISTRICT OF VIRGINIA UNITED STATES OF AMERICA.AMERICA, ) ) Plaintiff.Plaintiff, ) CIVIL ACTION NO. 1\ ',\3{;J"itf-QO' \9f\H;l}~ ) v. ) ) CHEVY CHASE BANK.BANK, F.S.BF.S.B., •• ) through its Successor Successorin in Interest.Interest, ) ) DefendantDefendant. ) ) SETTLEMENT AGREEMENT AND ORDER I. INTRODUCfIONINTRODUCTION This Settlement Agreement and Order("Agreement")Order ("Agreementtt) resolves the claims in the United States' Complaint that,that. during and between 2006 and 2009, Chevy Chase Bank.Bank, F.S.B. ("Chevy Chase Bank") engaged in a pattern or practice of discrimination on the basis ofofrace race and national origin in residential mortgage lending in violation of the Equal Credit Opportunity Act ("ECOA"),("ECOAtt). 15IS U.S.C. §§ 1691-169If.1691-1691 f, and andthe the Fair Housing Act ("FHA"),("FHAtt), 42 U.S.C. §§ 3601- 3619. In 2009. 2009, Chevy Chase Bank was acquired by Capital One,One. N.A. ("Successor"),(··Successor"). which is the successor in interest to Chevy Chase Bank. There has been no factual finding or adjudication with respect to any matter alleged by the United States. The parties have entered into the Agreement to avoid the risks,risks. expense, and burdens of litigation and to resolve voluntarily the claims claimsin in the United States' Complaint. Case 1:13-cv-01214-AJT-JFA Document 7 Filed 10/02/13 Page 2 of 15 PageID# 52 II. BACKGROUND In February 2009, the Office of the Comptroller of the Currency ("'OCC") conducted an analysis of Chevy Chase Bank's home mortgage lending activity in connection with the sale of Chevy Chase Bank to Successor. -

Recovery Act Impact Free Educational Event for All Workshops for Small Business Owners America East Conference for SBA Lenders

August 2009 Recovery Act Impact Washington In the first 6 weeks of the program, the SBA has approved over 1,000 Metropolitan ARC loans across the country, totaling over $32 million. Area District Since the signing of the Recovery Act, weekly loan dollar volume has Office risen more than 45% in the 7(a) and 504 programs. (WMADO) 740 15th Street NW A significant share of loans supported by Recovery Act funding has gone 3rd Floor to traditionally underserved markets: Washington, DC 20005 * 26% rural businesses www.sba.gov/dc * 20% minority-owned businesses 202.272.0345 * 19% woman-owned businesses * 9% veteran-owned businesses Bridget Bean District Director Free Educational Event for All 202.272.0340 [email protected] IRS Stakeholder Liaison Course: Everyone’s at Risk: Combating the Increasing Threat of Online Fraud and Identity Theft Theodore Holloman Deputy District Director August 19 via phone 10 a.m. Course # 760853 [email protected] 1 p.m. Course # 648527 202.272.0341 4 p.m. Course # 353052 Robert Carpenter Lender Relations Specialist Register by August17 at www.attevent.com to receive a personal code 202.272.0355 for one of the courses listed above. Then dial-in to 1-800-683-4564 on [email protected] August 19 at the appropriate time and input your code to join the course. Melissa Fischer Lender Relations Specialist Workshops for Small Business Owners 202.272.0347 must register in advance at www.scoredc.org [email protected] or by calling 202-272-0390 How to apply for a small loan Sept.