An Initial Public Stock Offering (IPO) Referred to Simply As an "Offering" Or

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Using Brokerage Commissions to Secure IPO Allocations1

Working Paper No. 4/2010 Using Brokerage Commissions to November 2010 Secure IPO Allocations Sturla Lyngnes Fjesme, Roni Michaely and Øyvind Norli © Sturla Lyngnes Fjesme, Roni Michaely and Øyvind Norli 2011. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission, provided that full credit, including © notice, is given to the source. This paper can be downloaded without charge from the CCGR website http://www.bi.no/ccgr 1 Using Brokerage Commissions to Secure IPO Allocations1 . Sturla Lyngnes Fjesme2 The Norwegian School of Management (BI) . Roni Michaely Cornell University and the Interdisciplinary Center . Øyvind Norli The Norwegian School of Management (BI) November 11, 2011 JEL classification: G24; G28 Keywords: IPO allocations; Equity issue; Commission; Rent seeking 1 We are grateful to Jay Ritter, Øyvind Bøhren, François Derrien, seminar participants at the Norwegian School of Management for valuable suggestions, “The Center for Corporate Governance Research (CCGR)”at the Norwegian School of Management for financial support, the Oslo Stock Exchange VPS for providing the data and the investment banks and companies that helped us locate the listing prospectuses. All errors are our own. 2 The Norwegian School of Management (BI), Nydalsveien 37, 0484 Oslo, Norway. E-mail address: [email protected] Telephone: 607-793-6911. 2 Abstract Using data, at the investor level, on the allocations of shares in initial public offerings (IPOs), we document a strong positive relationship between the amount of stock-trading commission and the number of shares an investor receives in a subsequent IPO. We find no evidence to support the idea that investment banks allocate shares to investors that are perceived to be long-term investors. -

Business Valuation Courses

The specialist in highly technical, market-driven bankingmergers and corporate & acquisitions finance trainingtraining BusinessMergers & ValuationAcquisitions Courses Courses web: redliffetraining.co.uk email: [email protected] phone: +44 (0)20 7387 4484 Advanced Negotiation Issues in M&A Date: BrochureLocation: London Content Standard Price: £*** + VAT Membership Price: £*** + VAT BOOK NOW PUBLIC COURSES Course Overview • Advanced Equity Valuation • Advanced Negotiation Issues in Financial Covenants • Advanced Negotiation Issues in M&A • Advanced Private Equity & Leverage Buy-Outs: A 5 Day Masterclass • Advanced Private Equity & LBOs Training • Advanced Takeover Code - Current Strategies & Tactics • Bank Valuation • Corporate Finance Masterclass • Corporate Finance Transactions • Equity & Debt Capital Markets • Effective Business Writing for Corporate Finance • European Term Loan “B” • How to Buy A Business • How to Sell A Business • Introduction to The Takeover Code • Joint Ventures - Key Negotiating and Structuring Issues Coursewith Content Sample Documents • Leveraged Loans in Private Equity and Corporate Transactions • Negotiating Heads of Terms (LOI/MOU) & Related Issues To book this course or find out more, please click the “Book” button Advanced Negotiation Issues in M&A Date: BrochureLocation: London Content Standard Price: £*** + VAT Membership Price: £*** + VAT BOOK NOW PUBLIC COURSES Course Overview • Tax Issues in M&A • The M&A Course • Modelling for M&A Course • Private Equity & MBO • The SPA Course - Commercial -

Initial Public Offerings

November 2017 Initial Public Offerings An Issuer’s Guide (US Edition) Contents INTRODUCTION 1 What Are the Potential Benefits of Conducting an IPO? 1 What Are the Potential Costs and Other Potential Downsides of Conducting an IPO? 1 Is Your Company Ready for an IPO? 2 GETTING READY 3 Are Changes Needed in the Company’s Capital Structure or Relationships with Its Key Stockholders or Other Related Parties? 3 What Is the Right Corporate Governance Structure for the Company Post-IPO? 5 Are the Company’s Existing Financial Statements Suitable? 6 Are the Company’s Pre-IPO Equity Awards Problematic? 6 How Should Investor Relations Be Handled? 7 Which Securities Exchange to List On? 8 OFFER STRUCTURE 9 Offer Size 9 Primary vs. Secondary Shares 9 Allocation—Institutional vs. Retail 9 KEY DOCUMENTS 11 Registration Statement 11 Form 8-A – Exchange Act Registration Statement 19 Underwriting Agreement 20 Lock-Up Agreements 21 Legal Opinions and Negative Assurance Letters 22 Comfort Letters 22 Engagement Letter with the Underwriters 23 KEY PARTIES 24 Issuer 24 Selling Stockholders 24 Management of the Issuer 24 Auditors 24 Underwriters 24 Legal Advisers 25 Other Parties 25 i Initial Public Offerings THE IPO PROCESS 26 Organizational or “Kick-Off” Meeting 26 The Due Diligence Review 26 Drafting Responsibility and Drafting Sessions 27 Filing with the SEC, FINRA, a Securities Exchange and the State Securities Commissions 27 SEC Review 29 Book-Building and Roadshow 30 Price Determination 30 Allocation and Settlement or Closing 31 Publicity Considerations -

Data Integrity in Financial Modeling

Data Integrity in Financial Modeling By Eric Kolchinsky, NAIC Director, Structured Securities fundamental assumptions of statistics and how they can Group limit the usefulness of financial models. Next, we review the differences between the mortgage loan information used to Introduction analyze pre-crisis RMBS and the loans’ true characteristics. With the benefit of hindsight, we can see 2009 was the be- Lastly, we discuss how the SSG and the Valuation of Securi- ginning of a slow recovery from the nadir of the recent global ties (E) Task Force are working to ensure the appropriate financial crisis. However, as the mortgage-induced crisis con- use of financial models for structured securities purchased tinued, the NAIC took a brave and a radical step—no longer by insurance companies. were ratings to be used to set the capital for residential mort- gage-backed securities (RMBS). RMBS, along with collateral- “Garbage in, Garbage out” ized debt obligations (CDOs), were at the epicenter of the crisis and had leveled financial giants such as Bear Stearns, “Pray, Mr. Babbage, if you put into the machine wrong Lehman Brothers, Fannie Mae, Freddie Mac and AIG. figures, will the right answers come out?” —Question posed to Charles Babbage, the creator of The NAIC decided to directly engage analytical vendors who the first mechanical computer. would work under the direct supervision of the Securities Valuation Office (SVO). PIMCO was chosen as the vendor for It is a common failure of human nature to find purpose in RMBS and, the following year, BlackRock Solutions was cho- complexity, and financial models are not immune. -

Investment Banking

NIRMA UNIVERSITY Institute of Management Master of Business Administration (Full Time) Programme/ Integrated Bachelor of Business Administration-Master of Business Administration Programme/ Master of Business Administration (Family Business & Entrepreneurship) Programme L T PW C 3 - - 3 Course Code MFT5SEEF17 MBM5SEEF17 MFB5SEEF18 Course Title Investment Banking Course Learning Outcomes (CLO): At the end of the course, students will be able to: 1. Interpret the managing aspects and regulations affecting of Investment Banks. 2. Develop appropriate instruments keeping in view the terms of issue of security. 3. Assess the valuation aspect and issue of various kind securities. 4. Plan the restructuring including capital restructuring of a company. Syllabus Teaching Hours Unit I: Overview of Investment Banking 04 • Basic Concepts and Definitions • Role of Investment Banking as Financial Intermediaries • Business of Investment Banking • American and Indian Investment Banks Unit II: Domestic Issue Management 06 • Dynamics of primary market • Listing requirements and procedure • Raising funds through IPO • Methods of bringing out an IPO, and IPO Pricing • Due diligence process Unit III: Restructuring, Underwriting and Ancillary Services 09 • Structured products and risk management advisory • Financial Restructuring Services • Corporate Debt Restructuring (CDR) • Underwriting Services, Business Model of Underwriting, Underwriting Commissions, Devolvement and Green Shoe Option • Issuing ADR, GDR and IDRs • Arranging for Buyback and Delisting of Shares Unit IV: Investment Banking and Business Valuation 07 • Various valuation models applied in estimating value of the firm and value of equity • Merits and Limitations of each models/methods of valuation • Valuing Private Equity and Venture Finance Unit V: Issues facing Investment Banks 04 • Designing new financial instruments • Adoption of Blockchain in Investment Banks • Data Security • Other Issues Suggested Readings: 1. -

Sr. Financial Analyst/Underwriter Portfolio Management & Project

Job Opening November 10, 2014 JOB TITLE: Sr. Financial Analyst/Underwriter LOCATION: NYC DEPARTMENT: Portfolio Management & Project Finance BASIC FUNCTION: Conduct financial and credit analysis of commercial/real estate developments and operating companies to determine amount of State support required and to structure loans, grants, disposition of State assets and other subsidies accordingly. WORK PERFORMED: Review and analyze financial statements to determine the creditworthiness of all commercial loan originations. Obtain financial projections and create cash flow models for operating companies and real estate developments. Perform site visits and conduct interviews with counter parties. Perform risk assessment of credit and collateral ensuring loan stability and sound credit quality. Draft loan reports and present to the board for approval. Research, develop and implement programs that promote economic development. Create financial products which help fill funding gaps and the market. Develop revenue generating ideas such as loans, credit enhancements, etc. Provide high-level financial analysis assistance to various other departments, including real estate, venture capital and loans & grants, in addition to other governmental agencies. Critically analyze large-scale development projects throughout New York State and help structure potential loans, grants and other state subsides. Perform sensitivity analyses and initiate financial feasibility studies on complex business development proposals. Conduct site visits to borrowers and grantees for continued engagement and research. Cultivate relations with small/mid-size, regional banks, CDFIs, local development agencies and industry organizations and form partnerships to help businesses in New York State to grow and prosper. Attend various conferences and seminars to establish new contacts and discover new opportunities. EDUCATION & REQUIREMENTS: Education Level required: MBA in Finance or Real Estate desirable. -

Condensed Consolidated Financial Statements (Unaudited)

Condensed Consolidated Financial Statements (unaudited) For the three and nine months ended September 30, 2015 and 2014 (Expressed in Canadian Dollars) SECURE ENERGY SERVICES INC. Condensed Consolidated Statements of Financial Position ($000's) (unaudited) Note s September 30, 2015 December 31, 2014 Assets Current assets Cash 2,670 4,882 Accounts receivable and accrued receivables 146,973 228,642 Current tax asset 11,650 - Prepaid expenses and deposits 6,601 8,396 Inv entories 3 63,825 70,199 231,719 312,119 Assets under construction 104,677 210,139 Property, plant and equipment 4 895,984 735,196 Intangible assets 74,668 124,102 Goodw ill 91,847 111,650 Other assets 1,543 2,911 Total Assets 1,400,438 1,496,117 Liabilities Current liabilities Accounts payable and accrued liabilities 97,402 193,121 Asset retirement obligations 7 1,697 1,800 Current tax liability - 5,886 Finance lease liabilities 10,011 10,458 109,110 211,265 Long-term borrow ings 6 256,593 397,385 Asset retirement obligations 7 77,145 70,639 Finance lease liabilities 8,156 12,060 Deferred income tax liability 35,968 42,473 Total Liabilities 486,972 733,822 Shareholders' Equity Issued capital 8 847,769 631,229 Share-based compensation reserve 33,959 25,227 Foreign currency translation reserve 37,240 14,629 (Deficit) retained earnings (5,502) 91,210 Total Shareholders' Equity 913,466 762,295 Total Liabilities and Shareholders' Equity 1,400,438 1,496,117 The accompanying notes are an integral part of these condensed consolidated financial statements 1 SECURE ENERGY SERVICES INC. -

Fundamentals of Corporate Valuation

Fundamentals of Corporate Valuation Debt free cash free company valuations: what are they? Imagine a typical company which has some amount of net debt (where net debt equals debt less cash that could be applied to refinancing that debt). Imagine too that those net liabilities could magically be removed, perhaps by a magnificent benefactor or a fairy godmother – someone who could work a wonder over the company and take away its net debt. Without those net liabilities, magically the company’s value would increase. That’s the debt free cash free valuation: the value of the company imagining it had no net debt. Shares/ equity valuation vs. debt free cash free How does debt free cash free valuation compare to shares or equity value? Let’s imagine a company that has shares/ equity with a valuation of 70 million. You can see that 70 million on the right hand side of the chart below. Let’s imagine that same company had debt less cash (= net debt) of 30 million. The debt free cash free valuation would be 100 million. That’s the value on the left hand side. Equity valuation vs. DFCF 1 Equity valuations are usually higher than DFCF values For a company that has net debt (that is, where debt is greater than cash) the debt free cash free value is higher than the shares/ equity valuation for the business. You can see that in the chart above: the 100 million on the left is higher than the 70 million on the right. Working from left to right, if the owner of a company had received a debt free cash free offer of 100 million, and if net debt was 30 million, the owner would expect to receive 70 million for the shares/ equity in the business. -

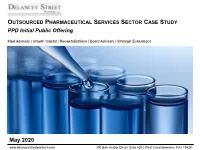

PPD Initial Public Offering

OUTSOURCED PHARMACEUTICAL SERVICES SECTOR CASE STUDY PPD Initial Public Offering M&A Advisory | Growth Capital | Recapitalizations | Board Advisory | Strategic Evaluations May 2020 www.delanceystreetpartners.com 300 Barr Harbor Drive | Suite 420 | West Conshohocken | PA | 19428 PPD INITIAL PUBLIC OFFERING Transaction Overview PPD (NASDAQ: PPD) Stock Price Performance $34.00 On February 5, 2020, Pharmaceutical Product $33.00 2/11/20 Closing Price: $32.87 Development (PPD) announced it raised $1.86 billion in its $32.00 initial public offering (IPO) $31.00 The company announced it priced 60 million primary shares of its common stock at the top end of its targeted range or $27.00 per share $30.00 2/6/20 Opening Price: $30.99 ‒ The underwriters simultaneously exercised the greenshoe option, $29.00 offering an additional 9 million primary shares of PPD’s common stock $28.00 at the IPO price, resulting in total IPO shares and gross proceeds of 69 million and $1.86 billion, respectively $27.00 3/6/20 Closing Price: $28.60 ‒ Implied Enterprise Value of $13.1 billion $26.00 ‒ Implied Enterprise Value / LTM Adjusted EBITDA multiple of 16.9x $25.00 PPD used the net proceeds from the offering to redeem a portion of its 5-Mar 1-Mar 2-Mar 3-Mar 4-Mar 6-Mar 7-Feb 8-Feb 9-Feb senior notes that were due to retire in 2022 and will use any remaining 6-Feb 11-Feb 10-Feb 12-Feb 13-Feb 14-Feb 15-Feb 16-Feb 17-Feb 18-Feb 19-Feb 20-Feb 21-Feb 22-Feb 23-Feb 24-Feb 25-Feb 26-Feb 27-Feb 28-Feb 29-Feb proceeds for general corporate purposes On February 6th, shares -

Project Finance

Project finance From Wikipedia, the free encyclopedia Jump to: navigation, search Project finance is the long term financing of infrastructure and industrial projects based upon the projected cash flows of the project rather than the balance sheets of the project sponsors. Usually, a project financing structure involves a number of equity investors, known as sponsors, as well as a syndicate of banks that provide loans to the operation. The loans are most commonly non-recourse loans, which are secured by the project assets and paid entirely from project cash flow, rather than from the general assets or creditworthiness of the project sponsors, a decision in part supported by financial modeling.[1] The financing is typically secured by all of the project assets, including the revenue-producing contracts. Project lenders are given a lien on all of these assets, and are able to assume control of a project if the project company has difficulties complying with the loan terms. Generally, a special purpose entity is created for each project, thereby shielding other assets owned by a project sponsor from the detrimental effects of a project failure. As a special purpose entity, the project company has no assets other than the project. Capital contribution commitments by the owners of the project company are sometimes necessary to ensure that the project is financially sound. Project finance is often more complicated than alternative financing methods. Traditionally, project financing has been most commonly used in the mining, transportation, telecommunication and public utility industries. More recently, particularly in Europe, project financing principles have been applied to public infrastructure under public± private partnerships (PPP) or, in the UK, Private Finance Initiative (PFI) transactions. -

Project Finance Course Outline

PROJECT FINANCE COURSE OUTLINE Term: Spring 2009 (1st half-semester) Instructor: Adjunct Prof. Donald B. Reid Time: Office: KMEC 9-95, 212-759-5655 Classroom: Email: [email protected] Admin aide: Contact: [email protected] Background Project finance is used on a global basis to finance over $300 billion of capital- intensive projects annually in industries such as power, transportation, energy, chemicals, and mining. This increasingly critical, financial technique relies on non- recourse, risk-mitigated cash flows of a specific project, not the balance sheet or corporate guarantee of a sponsor, to support the funding, using a broad-based set of inter-disciplinary skills Not all projects can support project financing. Project finance is a specialized financial tool necessitating an in-depth understanding of markets, technology, sponsors, offtakers, contracts, operators, and financial structuring. It is important to understand the key elements that support a project financing and how an investor or lender can get comfortable with making a loan or investment. Several industries will be used to demonstrate project-financing principles, with emphasis on one of the most important, power. Objective of the Course The purpose of the course is to understand what project finance is, its necessary elements, why it is used, how it is used, its advantages and its disadvantages. At the end of the course, students should be able to identify projects that meet the essential criteria for a project financing and know how to create the structure for a basic project financing. The course will study the necessary elements critical to project financing to include product markets, technology, sponsors, operators, offtakers, environment, consultants, taxes and financial sources. -

Swiss Biotech Report 2015

Swiss Biotech Report 2015 Impressum Steering committee Domenico Alexakis, Swiss Biotech Association, Zürich Seraina Benz, SIX Swiss Exchange AG, Zürich Oreste Ghisalba, CTI, Bern Jan Lucht, scienceindustries, Zürich Liv Minder, Switzerland Global Enterprise, Zürich Heinz Müller, Swiss Federal Institute of Intellectual Property, Bern Swiss National Science Foundation, Bern Andrea von Bartenwerffer, SIX Swiss Exchange AG, Zürich Jürg Zürcher, Ernst & Young AG, Basel Further partners Daniel Gygax, biotechnet, Muttenz Concept, layout and design sherif ademi | kommunikationsdesign, Schlieren Scan the QR code to download the Swiss Biotech Report 2015. www.swissbiotechreport.ch Publicly traded Swiss biotech companies 3500 in CHF million 3061 2918 2012 3000 2843 2013 2014 2500 2064 1955 Source: Annual Reports, 2000 1852 website information and EY 1500 1000 728 691 678 525 500 374 233 0 –500 Revenues R&D expenses Profits/losses Liquidity Privately held Swiss biotech companies 2500 in CHF million 2012 2000 2013 1799 1826 1824 2014 1500 Source: EY 1000 848 725 673 650 606 602 500 –68 –63 –98 0 Revenues R&D expenses Profits/losses Liquidity –500 Cover Picture: Picture courtesy of Jürg Zürcher © View from Schynige Platte on “Ussri Sägissa” and “Winteregg”. 31 Table of contents Editorial 4 International relationships – Made in Switzerland 5 International cooperation a prerequisite to research 7 Switzerland 2i – innovation and internationalism 8 Short outline of CTI’s national and international activities 9 Patent literature reflects international focus of Swiss biotech 11 Global network and local production drive success 13 Switzerland: strategic business location for life sciences 14 Gearing up for growth: Molecular Partners powers Swiss biotechs’ rise 15 Year in review 19 Swiss biotech at a glance 28 Facts & figures 29 3 Editorial Switzerland’s success has been built on a combination of inter- nationalism and ‘Swissness’.