Case M.9316 - PEAB / YIT's PAVING and MINERAL AGGREGATES BUSINESS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

YIT Management System GRIP / HP&AH&TT 2019

YIT management system GRIP / HP&AH&TT 2019 YIT Company-Wide Management System for Project Business JOHANNA AROLA , DEVELOPMENT MANAGER, YIT SUOMI OY 2019 Creating better living environments We develop and build apartments and living services, business premises and entire areas. We are also specialised in demanding infrastructure construction and paving. Together with our customers, we create more functional, more attractive and more sustainable cities and environments. MERENKULKIJANRANTA, HELSINKI, FINLAND The history of YIT 1910–2019 1960 2018 1920 1930 1940 1950 1970 1980 1990 2000 2010 1910 1912 2019 1970 2013 LEMMINKÄINEN SALE OF NORDIC YIT GROWS YIT UNDERGOES A 1990 AND YIT MERGE PAVING AND 1920 to become the DEMERGER 1960 THE MODERN PROJECTS AROUND Stronger and MINERAL FINNISH BUSINESSMEN largest construction to form two separate YIT IS FORMED THE WORLD more AGGREGATES ESTABLISH YLEINEN 1950 company and IN THE 2000s, companies. YIT continues by Perusyhtymä, By 1994, the Group stable together BUSINESS 1910 INSINÖÖRITOIMISTO THE COMPANY construction YIT EXPANDS its construction operations, Yleinen 1980 operates in 11 Announced in LEMMINKÄINEN to continue the EXPANDS ITS exporter in Finland. operations to building while its building services 1930 Insinööritoimisto, HOUSING countries. Foreign July, estimated to IS ESTABLISHED operations. The CONSTRUCTION services in the Nordic are transferred to a newly Asfaltti Osakeyhtiö DEVELOPMENTS IN Pellonraivaus Oy CONSTRUCTION BEGINS business accounts take place company grows to OPERATIONS 1975 countries and Central formed publicly listed Lemminkäinen is PAVING and Insinööritoimisto Operations are more than half of January 1, 2020 become Finland’s and starts to export STRONG GROWTH Europe. Housing and company, Caverion. -

Labour Market Areas Final Technical Report of the Finnish Project September 2017

Eurostat – Labour Market Areas – Final Technical report – Finland 1(37) Labour Market Areas Final Technical report of the Finnish project September 2017 Data collection for sub-national statistics (Labour Market Areas) Grant Agreement No. 08141.2015.001-2015.499 Yrjö Palttila, Statistics Finland, 22 September 2017 Postal address: 3rd floor, FI-00022 Statistics Finland E-mail: [email protected] Yrjö Palttila, Statistics Finland, 22 September 2017 Eurostat – Labour Market Areas – Final Technical report – Finland 2(37) Contents: 1. Overview 1.1 Objective of the work 1.2 Finland’s national travel-to-work areas 1.3 Tasks of the project 2. Results of the Finnish project 2.1 Improving IT tools to facilitate the implementation of the method (Task 2) 2.2 The finished SAS IML module (Task 2) 2.3 Define Finland’s LMAs based on the EU method (Task 4) 3. Assessing the feasibility of implementation of the EU method 3.1 Feasibility of implementation of the EU method (Task 3) 3.2 Assessing the feasibility of the adaptation of the current method of Finland’s national travel-to-work areas to the proposed method (Task 3) 4. The use and the future of the LMAs Appendix 1. Visualization of the test results (November 2016) Appendix 2. The lists of the LAU2s (test 12) (November 2016) Appendix 3. The finished SAS IML module LMAwSAS.1409 (September 2017) 1. Overview 1.1 Objective of the work In the background of the action was the need for comparable functional areas in EU-wide territorial policy analyses. The NUTS cross-national regions cover the whole EU territory, but they are usually regional administrative areas, which are the re- sult of historical circumstances. -

The Dispersal and Acclimatization of the Muskrat, Ondatra Zibethicus (L.), in Finland

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Wildlife Damage Management, Internet Center Other Publications in Wildlife Management for 1960 The dispersal and acclimatization of the muskrat, Ondatra zibethicus (L.), in Finland Atso Artimo Suomen Riistanhoito-Saatio (Finnish Game Foundation) Follow this and additional works at: https://digitalcommons.unl.edu/icwdmother Part of the Environmental Sciences Commons Artimo, Atso, "The dispersal and acclimatization of the muskrat, Ondatra zibethicus (L.), in Finland" (1960). Other Publications in Wildlife Management. 65. https://digitalcommons.unl.edu/icwdmother/65 This Article is brought to you for free and open access by the Wildlife Damage Management, Internet Center for at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in Other Publications in Wildlife Management by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. R I 1ST A TIE T L .~1 U ( K A I S U J A ,>""'liSt I " e'e 'I >~ ~··21' \. • ; I .. '. .' . .,~., . <)/ ." , ., Thedi$perscdQnd.a~C:li"'dti~otlin. of ,the , , :n~skret, Ond~trq ~ib.t~i~',{(.h in. Firtland , 8y: ATSO ARTIMO . RllSTATIETEELLISljX JULKAISUJA PAPERS ON GAME RESEARCH 21 The dispersal and acclimatization of the muskrat, Ondatra zibethicus (l.), in Finland By ATSO ARTIMO Helsinki 1960 SUOMEN FIN LANDS R I 1ST A N HOI T O-S A A T I b ] AK TV ARDSSTI FTELSE Riistantutkimuslaitos Viltforskningsinstitutet Helsinki, Unionink. 45 B Helsingfors, Unionsg. 45 B FINNISH GAME FOUNDATION Game Research Institute Helsinki, Unionink. 45 B Helsinki 1960 . K. F. Puromichen Kirjapaino O.-Y. The dispersal and acclimatization of the muskrat, Ondatra zibethicus (L.), in Finland By Atso Artimo CONTENTS I. -

Peab Community Builder Peab Builds Effective Processes for Group Reporting with Unit4 Consolidation

Unit4 Consolidation case study Peab Community builder Peab builds effective processes for group reporting with Unit4 Consolidation. In keeping with its focus on quality, efficiency and governance, this Nordic-wide construction group chose Unit4 Consolidation to gain a clearer picture of its financial performance and simplify consolidated financial reporting. Overview The situation Background Peab is a construction group with operations across Peab is a Nordic construction group with operations Sweden, Norway and Finland, whose vision is to across Sweden, Norway and Finland. be the natural partner for community building in the Nordic region. • Approximately 13,000 employees. • Headquartered in Förslöv, Sweden. • 300 subsidiaries. • Listed on NASDAQ OMX Stockholm. • A turnover in 2013 of around SEK 43 billion. The Group has over 300 subsidiaries, 130 strategically • Four key business areas: Civil Engineering, located offices throughout the region and about Construction, Property Development and Industry. 13,000 employees; it achieved a turnover in 2013 of SEK 43 billion. Peab’s guiding principle is total Key requirements quality in all phases of the construction process. The Peab needed an easy-to-use, flexible and powerful company has reached its current position through system for group reporting, with a focus on legal innovation, with leading-edge climate-smart solutions consolidation. that are sustainable throughout their lifecycle. Solution Following 50 years of growth, Peab has in recent Peab chose Unit4 Consolidation to simplify and years taken important steps to become “the Nordic streamline its reporting procedures. Community Builder”. Since January 2012, the Group’s business has been organized around 300 subsidiaries Customer benefits in four Nordic business areas: Civil Engineering, • Easy to use. -

Roadshow Presentation November 2018 Contents

Roadshow presentation November 2018 Contents 1 Merger and integration 2 YIT in a nutshell 3 YIT’s strategy 2019-2021 4 Performance in Q3 5 Segment reviews 6 Financial position and key ratios 7 Outlook and guidance 8 Appendices SÄHKÖTTÄJÄNPUISTO PARL 2 Roadshow presentation, November 2018 HELSINKI, FINLAND 1 Merger and intergration 3 Roadshow presentation, November 2018 The merger of YIT and Lemminkäinen, February 1st 2018 Revenue: EUR 1,909 million Adjusted EBIT: EUR 122.3 million 2018 - MERGER Personnel: 5,427 YIT is the largest Finnish and significant SINCE YIT creates more attractive North European construction company. We Target to and sustainable urban develop and build apartments, business 1912 environments by building premises and entire areas. become housing, business premises, infrastructure and entire We are also specialised in demanding together the areas. infrastructure construction and paving. Together with our customers our leading urban Revenue: EUR 1,847 million 10,000 professionals are creating more Adjusted EBIT: EUR 46.6 million functional, more attractive and more developer in Personnel: 4,632 sustainable cities and environments. Northern SINCE An expert in complex infrastructure construction We work in 11 countries: Finland, Russia, 1910 ana building construction in Scandinavia, the Baltic States, the Czech Europe northern Europe and one of Republic, Slovakia and Poland. the largest paving companies in our market area. * Revenue, adjusted EBIT and personnel at the end of period in 2017. YIT’s figures according to POC -

Annual Report 2014 Contents

Annual Report 2014 Contents Highlighting green certification Group overview Throughout this Annual Report the relevant logos are used to indicate 2014 in brief 2 when projects are, or are in the process of being, certified to a green Comments by the President and CEO 4 certification scheme. Green certification provides voluntary third-party Mission, goals and strategy 6 validation of the environmental design and/or performance of build- Financial targets 8 ings and infrastructure. Skanska has expertise around a number of the Business model 10 schemes most relevant to its home markets. Today over 600 Skanska Risk management 12 employees are accredited by external agencies for their expertise in this area – expertise which is used to execute projects for clients and Sustainable development 16 for Skanska’s own development units. –Environmental agenda 17 –Social agenda 23 Employees 32 Share data 36 Business streams 40 Construction 42 Leadership in Energy BRE Environmental Civil Engineering – Nordics 46 and Environmental Assessment Method, Environmental Quality – Other European countries 50 Design, LEED BREEAM Assessment and Award Scheme, CEEQUAL – North America 54 Residential Development 58 – Nordics 62 – Central Europe 64 Commercial Property Development 66 Strong year for Skanska in London – Nordics 70 – Central Europe 72 – North America 74 Infrastructure Development 76 – Project portfolio 79 30 St Mary Axe Heron Tower (The Gherkin) Financial information Bevis Marks Dashwood Report of the Directors 85 House Corporate governance report 93 Consolidated income statement 103 Consolidated statement of comprehensive income 104 Consolidated statement of financial position 105 Consolidated statement of changes in equity 107 Consolidated cash flow statement 108 Parent Company income statement 110 London is a major construction market for Skanska, and in 2014 the company had Parent Company balance sheet 111 10 office projects in progress covering an overall area of 237,000 sq m with a total Parent Company statement of changes in equity 112 contract value of GBP 684 M. -

Annual and Sustainability Report 2018

Annual and Sustainability Report 2018 We build for a better society. B Skanska Annual and Sustainability Report 2018 Operations Skanska’s operations consist of Construction and Project Development, including Residential Development, Commercial Property Development and, until 2018, Infrastructure Development. Business units within these streams collaborate in various ways, creating operational and financial synergies that generate increased value. Residential Commercial Property Infrastructure Construction Development Development Development 1 Constructs and renovates build- Develops new residential projects, Develops customer-focused office Secures and manages the value ings, infrastructure and homes, including single and multi-family buildings, shopping centers and of Skanska’s existing public- along with facilities manage- housing, built by the Construction logistics properties built by the private partnership (PPP) assets. ment and other related services. business stream. Construction business stream. 1 As of January 1, 2019, Infrastructure Development is no longer a business stream and is reported in Central on a separate line. Well diversified, Percentage of total revenue in 2018 with a leading market position Skanska’s diversification across various business streams with operations in eleven countries and several market segments strengthens the Group’s 40% SwedenSweden competitive standing and ensures FinlandFinland Norway a balanced and diversified risk profile. USA 38% Denmark United Kingdom Poland Czech Republic SlovakiaSlovakia Hungary 22% Romania Green revenue in 2018 Green market value in 2018 Green financing in 2018 Percentage of total Construction revenue Percentage of Commercial Property Percentage of total central debt 3 that is that is Green and Deep green, as defined Development market value from Green Green, according to the Skanska Green by the Skanska Color Palette™ 2. -

Peab's Annual and Sustainability Report 2016

Annual and Sustainability Report 2016 A LOCALLY ENGAGED COMMUNITY BUILDER Content 2016 in summary 1 Comments from the CEO 2–3 External circumstances and the market 4–5 Goals and strategies 6–9 Market summary – Peab’s business areas 10–11 Peab’s take on sus- P21 Our take on sustainable operations 12–35 tainable operations Attitude The Employees 16–21 changing The Business 22–25 Five initiatives that reflect our work with workshops sustainability in the focus areas The Climate and Environment 26–31 Employees, The Business, Climate and Environment and Social Engagement. Social Engagement 32–35 Board of Directors' report 36–56 The Group 36–39 Business area Construction 40–41 Business area Civil Engineering 42–43 Business area Industry 44–45 P24 P28 Business area Project Development 46–49 Everything Peab’s ECO- Risks and risk management 50–52 in order Asfalt – a better Other information and appropriation of profit 53–56 choice for the Financial reports and notes 57–109 environment Auditor's report 110–113 Corporate governance 114–117 Board of Directors 118 Executive management and auditor 119 The Peab share 120–121 Five-year overview 122 Alternative performance measures P31 P33 and definitions 123 Forward-looking The Peab School About the sustainability report 124 neighborhood with trains young Global Compact principles 124 a strong environ- immigrants mental profile Active memberships 125 GRI Index 126–127 Annual General Meeting 128 Shareholder information 128 Formal annual and Group financial reports which have been audited by company accountants, pages 36–109. Peab AB is a public company, Company ID 556061-4330. -

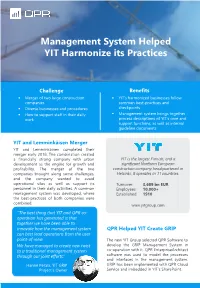

Management System Helped YIT Harmonize Its Practices

Management System Helped YIT Harmonize its Practices Challenge Benefits . Merger of two large construction . YIT’s harmonized businesses follow companies common best-practices and . Diverse businesses and procedures checkpoints . How to support staff in their daily . Management system brings together work process descriptions of YIT’s core and support functions, as well as internal guideline documents YIT and Lemminkäisen Merger YIT and Lemminkäinen completed their merger early 2018. The combination created a financially strong company with urban YIT is the largest Finnish, and a development as the engine for growth and significant Northern European profitability. The merger of the two construction company headquartered in companies brought along some challenges, Helsinki. It operates in 11 countries. and the company wanted to avoid operational silos as well as support its Turnover: 3,689 bn EUR personnel in their daily activities. A common Employees: 10,000+ management system was developed, where Established: 1910 the best-practices of both companies were combined. www.yitgroup.com “The best thing that YIT and QPR co- operation has generated is that together we have been able to innovate how the management system QPR Helped YIT Create GRIP can best lead operations from the user point-of-view. The new YIT Group selected QPR Software to We have managed to create new twist develop the GRIP Management System in to a traditional management system co-operation with it. QPR EnterpriseArchitect through our joint efforts.” software was used to model the processes and interfaces in the management system. Hanne Perälä, YIT GRIP GRIP has been implemented with QPR Cloud Project’s Owner Service and imbedded in YIT’s SharePoint. -

Annual Report 2001 (Pdf)

NCC 2001 REPORT ANNUAL CONTENTS/TURN FLAP responsibility focus simplicity NCC AB, SE-170 80 Solna, Sweden. Tel +46 8 585 510 00. Fax +46 8 85 77 75. www.ncc.se NCC Annual Report 2001 CONTENTS THIS IS NCC TOMORROW’S ENVIRONMENTS FOR WHERE TO FIND NCC WORKING, LIVING AND COMMUNICATIONS ASPHALT, AGGREGATES, MACHINERY RENTAL 1 Responsibility,focus,simplicity SALES NCC is one of the leading construction and property-developing companies in the Nordic region. NCC AB NCC Construction NCC Construction se Norway Sweden PAVING, CONCRETE, 1997–2001, SEK BN -170 80 Solna Altima AB 2 Highlights of 2001 The Group had annual sales of SEK 46 billion in 2001, with 28,000 employees. Street address: Vallgatan 3 NCC Norge A/S se-170 80 Solna ROAD SERVICES, p.b Tagenevägen 25 3 Review by the president 50 Tel: +46 8 585 510 00 93 Sentrum Tel: +46 8 585 510 00 TRAFFIC SAFETY se- 46.1 n 425 37 Hisings Kärra NCC constructs roads and civil engineering facilities, telecommunications infrastructure, hous- Fax: +46 8 85 77 75 -0101 Oslo Fax: +46 8 624 05 19 NCC Roads 6 Strategic orientation and financial objectives 40.8 Tel: +46 31 57 67 00 40 E-mail: [email protected] Tel: +47 22 98 68 00 E-mail: [email protected] Tuborg Havnevej 15 10 The NCC share 37.5 ing, offices and other buildings. It also produces building materials and is one of the largest sup- Fax: +46 31 57 67 50 34.2 www.ncc.se Fax: +47 22 98 69 23 www.ncc.se dk 32.1 -2900 Hellerup www.altima.se pliers of aggregates, asphalt and ready-mixed concrete in the Nordic region. -

Naturally Near By

LLoppioppi NNaturallyaturally nnearear bbyy www.loppi.fi Loppi is a lively, growing rural municipality in the Tavastia Proper region. Our central location, active business community, beauti- ful natural surroundings and excellent community services make Loppi a great place for living, leisure and work. Around 8300 people live in Loppi. The municipality has three main population centres: the town of Loppi (Kirkonkylä), Launonen and Läyliäinen. There are also a number of smaller villages. With its beautiful countryside and many lakes and ponds, Loppi munici- pality is also a popular place for outdoor leisure activities. Loppi has thousands of summer cottages, and the area’s population nearly doubles in the summertime. We have a wide variety of cultural events all year round. There are concerts and exhibitions organised throughout the year by the community as well as non-profi t organisations. Thousands of people fl ock to enjoy the summer theatre performances put on by the Loppi Theatre in its summer home in the village of Sajaniemi. We look forward to welcoming you to Loppi to visit, to live and to enjoy! Karoliina Viitanen Municipal Manager NNaturallyaturally nnearear bbyy Close to nature Welcome to Loppi Loppi combines the best aspects of peaceful natural surround- Loppi is especially famous for its potatoes. In addition to tradi- ings, convenient living and closeness to larger cities. tional family farms, the municipality has some 400 businesses. The municipality of Loppi enjoys a prime location in the Tavastia The town of Loppi Kirkonkylä is lively, with its shops and schools, Lake Highlands in Southern Tavastia province. We have some of but there are numerous other villages in the municipality, each the loveliest landscapes in Finland, yet Loppi is located in the with its own active village life. -

Ncc A-Del ENG Slutkorr 2 98-04-01 10.33 Sidan 1 Summary

/ncc A-del ENG slutkorr 2 98-04-01 10.33 Sidan 1 Summary Summary Pro forma consolidated income after net financial KEY FIGURES IN BRIEF items, excluding merger costs, amounted to SEK 1997 1996 Income after net financial items 74 m. (273). Including merger costs, a loss of SEK excluding merger costs, SEK m.1 74 273 375 m. was reported after net financial items. Equity/assets ratio 33% 30% Net income after full tax and excluding merger Earnings/loss per share excluding merger costs, SEK 2.60 2.00 costs amounted to SEK 276 m. (159) which Dividend per share, SEK 1.50 2 1.50 corresponds to SEK 2.60 (2.00) per share. 1) Pro forma, see page 62. Including merger costs, a net loss of SEK 173 m. 2) Board of Directors’ proposal to Annual General Meeting was reported, which corresponds to a loss of SEK 1.60 per share. A dividend of SEK 1.50 (1.50) per share is proposed. BO AX:SON JOHNSON Bo Ax:son Johnson died on May 9, 1997, Total orders received by construction operations at an age of 79. Bo Ax:son Johnson was rose 9 percent to SEK 29.8 billion (27.3). On a active in the Nordstjernan Group for 52 years, the last 18 of which as Chairman of pro forma basis, orders received by NCC’s Nordstjernan. Swedish construction operations declined by During these years, Bo Ax:son Johnson 9 percent during the year to SEK 18.3 billion became intimately associated with Sweden’s industrial history and the (20.0).