Statistical Testing of Technical Trading Rule Profitability

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Copyrighted Material

INDEX Page numbers followed by n indicate note numbers. A Arnott, Robert, 391 Ascending triangle pattern, 140–141 AB model. See Abreu-Brunnermeier model Asks (offers), 8 Abreu-Brunnermeier (AB) model, 481–482 Aspray, Thomas, 223 Absolute breadth index, 327–328 ATM. See Automated teller machine Absolute difference, 327–328 ATR. See Average trading range; Average Accelerated trend lines, 65–66 true range Acceleration factor, 88, 89 At-the-money, 418 Accumulation, 213 Average range, 79–80 ACD method, 186 Average trading range (ATR), 113 Achelis, Steven B., 214n1 Average true range (ATR), 79–80 Active month, 401 Ayers-Hughes double negative divergence AD. See Chaikin Accumulation Distribution analysis, 11 Adaptive markets hypothesis, 12, 503 Ayres, Leonard P. (Colonel), 319–320 implications of, 504 ADRs. See American depository receipts ADSs. See American depository shares B 631 Advance, 316 Bachelier, Louis, 493 Advance-decline methods Bailout, 159 advance-decline line moving average, 322 Baltic Dry Index (BDI), 386 one-day change in, 322 Bands, 118–121 ratio, 328–329 trading strategies and, 120–121, 216, 559 that no longer are profitable, 322 Bandwidth indicator, 121 to its 32-week simple moving average, Bar chart patterns, 125–157. See also Patterns 322–324 behavioral finance and pattern recognition, ADX. See Directional Movement Index 129–130 Alexander, Sidney, 494 classic, 134–149, 156 Alexander’s filter technique, 494–495 computers and pattern recognition, 130–131 American Association of Individual Investors learning objective statements, 125 (AAII), 520–525 long-term, 155–156 American depository receipts (ADRs), 317 market structure and pattern American FinanceCOPYRIGHTED Association, 479, 493 MATERIALrecognition, 131 Amplitude, 348 overview, 125–126 Analysis pattern description, 126–128 description of, 300 profitability of, 133–134 fundamental, 473 Bar charts, 38–39 Andrews, Dr. -

Tradescript.Pdf

Service Disclaimer This manual was written for use with the TradeScript™ language. This manual and the product described in it are copyrighted, with all rights reserved. This manual and the TradeScript™ outputs (charts, images, data, market quotes, and other features belonging to the product) may not be copied, except as otherwise provided in your license or as expressly permitted in writing by Modulus Financial Engineering, Inc. Export of this technology may be controlled by the United States Government. Diversion contrary to U.S. law prohibited. Copyright © 2006 by Modulus Financial Engineering, Inc. All rights reserved. Modulus Financial Engineering and TradeScript™ are registered trademarks of Modulus Financial Engineering, Inc. in the United States and other countries. All other trademarks and service marks are the property of their respective owners. Use of the TradeScript™ product and other services accompanying your license and its documentation are governed by the terms set forth in your license. Such use is at your sole risk. The service and its documentation (including this manual) are provided "AS IS" and without warranty of any kind and Modulus Financial Engineering, Inc. AND ITS LICENSORS (HEREINAFTER COLLECTIVELY REFERRED TO AS “MFE”) EXPRESSLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO THE IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE AND AGAINST INFRINGEMENT. MFE DOES NOT WARRANT THAT THE FUNCTIONS CONTAINED IN THE SERVICE WILL MEET YOUR REQUIREMENTS, OR THAT THE OPERATION OF THE SERVICE WILL BE UNINTERRUPTED OR ERROR-FREE, OR THAT DEFECTS IN THE SERVICE OR ERRORS IN THE DATA WILL BE CORRECTED. FURTHERMORE, MFE DOES NOT WARRANT OR MAKE ANY REPRESENTATIONS REGARDING THE USE OR THE RESULTS OF THE USE OF THE SERVICE OR ITS DOCUMENTATION IN TERMS OF THEIR CORRECTNESS, ACCURACY, RELIABILITY, OR OTHERWISE. -

![8 Best Bearish Candlestick Patterns for Day Trading [Free Guide & Video]](https://docslib.b-cdn.net/cover/5489/8-best-bearish-candlestick-patterns-for-day-trading-free-guide-video-595489.webp)

8 Best Bearish Candlestick Patterns for Day Trading [Free Guide & Video]

8 Best Bearish Candlestick Patterns for Day Trading [Free Guide & Video] Recently, we discussed the general history of candlesticks and their patterns in a prior post. We also have a great tutorial on the most reliable bullish patterns. But for today, we’re going to dig deeper, and more practical, explaining 8 bearish candlestick patterns every day trader should know. We’ll cover the following: What these patterns look like The criteria for confirming them The story these candles tell How to set entries and risk for each Some common mistakes when interpreting them. 8 Bearish Candlesticks Video Tutorial If you have a few minutes, our in-house trading expert, Aiman Almansoori has cut out a lot of the leg-work for us in this fantastic webinar. We’ve time-stamped the exact spot in the recording where he begins speaking about these 8 bearish candlestick patterns. Have a watch while you read! Also, feel free to use our quick reference guide below for bearish candlestick patterns! Be sure to save the image for your use with your trading and training in the market! What Bearish Candlesticks Tell Us Hopefully at this point in your trading career you’ve come to know that candlesticks are important. Not only do they provide a visual representation of price on a chart, but they tell a story. Behind this story is the belief that the chart tells us everything we need to know: the what being more important than the why. Each candlestick is a representation of buyers and sellers and their emotions, regardless of the underlying “value” of the stock. -

Technical Analysis Masterclass

TRADING: TECHNICAL ANALYSIS MASTERCLASS - Master The Financial Markets – Rolf Schlotmann & Moritz Czubatinski Copyright © 2019, Rolf Schlotmann, Moritz Czubatinski, Quantum Trade Solutions GmbH All rights reserved, including those of reprinting of extracts, photomechanical and electronical reproduction and translation. Any duplication, reproduction and publication outside the provisions of copyright law (Urheberrechtsgesetz) is not permitted as a whole or in part without the prior written consent of the author. This work is not intended to give specific investment recommendations and merely provides general guidance, exemplary illustrations and personal views. Author, publisher and cited sources are not liable for any loss or other consequences arising from the implementation of their thoughts and views. Any liability is excluded. The advice and information published in this book has been carefully prepared and reviewed by the author. Anyhow, a guarantee or other responsibility for their accuracy, completeness and timeliness cannot be given. In particular, it should be noted that all speculative investment transactions involve a significant risk of loss and are not suitable for all investors. It is strongly recommended not to rely solely on this book, but to conduct own investigations and analyses and, if necessary, to obtain advice from financial advisors, tax advisors and lawyers before making an investment decision. Company identity Quantum Trade Solutions GmbH Jahnstrasse 43 63075 Offenbach Germany Chairmen: Schlotmann, Rolf and Czubatinski, Moritz Publication date: 19.02.2019 1st version Financial charts have been obtained through www.tradingview.com Foreword Introduction 1. What is trading? 1.1 The profit potential 1.2 Decision-making 1.3 Short-term vs. long-term trading 2. -

Data Visualization and Analysis

HTML5 Financial Charts Data visualization and analysis Xinfinit’s advanced HTML5 charting tool is also available separately from the managed data container and can be licensed for use with other tools and used in conjunction with any editor. It includes a comprehensive library of over sixty technical indictors, additional ones can easily be developed and added on request. 2 Features Analysis Tools Trading from Chart Trend Channel Drawing Instrument Selection Circle Drawing Chart Duration Rectangle Drawing Chart Intervals Fibonacci Patterns Chart Styles (Line, OHLC etc.) Andrew’s Pitchfork Comparison Regression Line and Channel Percentage (Y-axis) Up and Down arrows Log (Y-axis) Text box Show Volume Save Template Show Data values Load Template Show Last Value Save Show Cross Hair Load Show Cross Hair with Last Show Min / Max Show / Hide History panel Show Previous Close Technical Indicators Show News Flags Zooming Data Streaming Full Screen Print Select Tool Horizontal Divider Trend tool Volume by Price Horizonal Line Drawing Book Volumes 3 Features Technical Indicators Acceleration/Deceleration Oscillator Elliot Wave Oscillator Accumulation Distribution Line Envelopes Aroon Oscilltor Fast Stochastic Oscillator Aroon Up/Down Full Stochastic Oscillator Average Directional Index GMMA Average True Range GMMA Oscillator Awesome Oscillator Highest High Bearish Engulfing Historical Volatility Bollinger Band Width Ichimoku Kinko Hyo Bollinger Bands Keltner Indicator Bullish Engulfing Know Sure Thing Chaikin Money Flow Lowest Low Chaikin Oscillator -

The Cycle Trading Pattern Manual 2 Copyright © Walter Bressert, Inc

TIMING IS EVERYTHING …And the use of time cycles can greatly improve the accuracy and success of your trading and/or system. There is no magic oscillator or indicator that will bring you THE CYCLE success in the markets. Knowledge of trading techniques and tools to improve TIMING and determine TREND is the key to low TRADING risk high probability trades that can bring you success. Knowledge, self-discipline and persistence are the true keys to PATTERN success in trading. Over time you will develop a trading style that fits your personality and trading skills. There are many tools to MANUAL help improve your trading, but only cycles will allow you to add By Walter Bressert the element of TIME into your trading. www.walterbressert.com Simple buy and sell signals do not consider the whole picture. By combining mechanical trading signals with daily and weekly cycles (or two intra-day time periods and cycles, such as a 45- minute and 180-minute, or a 5-minutes and 20-minute), retracements, trend Indicators and trendlines into Cycle Trading Patterns, you can greatly improve your accuracy and odds of making money on a trade or with a system. The following charts and trading concepts are based on trading the long side of a market. The same techniques and concepts work in mirror image fashion for trading the short side TABLE OF CONTENTS IDENTIFYING CYCLE TOPS AND BOTTOMS USING OSCILLATORS 2 Detrending Takes the Mystery Out of Cycles 3 Oscillators Show Cycle Tops and Bottoms 5 OSCILLATOR/PRICE PATTERNS GENERATE MECHANICAL TRADING SIGNALS 6 Detrended -

Investing with Volume Analysis

Praise for Investing with Volume Analysis “Investing with Volume Analysis is a compelling read on the critical role that changing volume patterns play on predicting stock price movement. As buyers and sellers vie for dominance over price, volume analysis is a divining rod of profitable insight, helping to focus the serious investor on where profit can be realized and risk avoided.” —Walter A. Row, III, CFA, Vice President, Portfolio Manager, Eaton Vance Management “In Investing with Volume Analysis, Buff builds a strong case for giving more attention to volume. This book gives a broad overview of volume diagnostic measures and includes several references to academic studies underpinning the importance of volume analysis. Maybe most importantly, it gives insight into the Volume Price Confirmation Indicator (VPCI), an indicator Buff developed to more accurately gauge investor participation when moving averages reveal price trends. The reader will find out how to calculate the VPCI and how to use it to evaluate the health of existing trends.” —Dr. John Zietlow, D.B.A., CTP, Professor of Finance, Malone University (Canton, OH) “In Investing with Volume Analysis, the reader … should be prepared to discover a trove of new ground-breaking innovations and ideas for revolutionizing volume analysis. Whether it is his new Capital Weighted Volume, Trend Trust Indicator, or Anti-Volume Stop Loss method, Buff offers the reader new ideas and tools unavailable anywhere else.” —From the Foreword by Jerry E. Blythe, Market Analyst, President of Winthrop Associates, and Founder of Blythe Investment Counsel “Over the years, with all the advancements in computing power and analysis tools, one of the most important tools of analysis, volume, has been sadly neglected. -

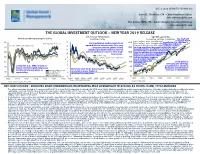

The Global Investment Outlook – New Year 2019 Release U.S

DEC 4 2018 (UPDATED TO NOV 30) Daniel E. Chornous, CFA Chief Investment Officer [email protected] Eric Savoie, MBA, CFA Senior Analyst, Investment Strategy [email protected] THE GLOBAL INVESTMENT OUTLOOK – NEW YEAR 2019 RELEASE U.S. 10-year T-Bond yield S&P 500 equilibrium Global purchasing managers' indices Equilibrium range Normalized earnings & valuations The S&P 500 Nov. '18 Range: 2141 - 3563 (Mid: 2852) is slightly below 65 16 5120 equilibrium (i.e. the band’s ISM Peak Aug 2018: 61.3 Our equilibrium model suggests an Nov. '19 Range: 2218 - 3691 (Mid: 2954)midpoint), and many Previous ISM Peak Feb 2011: 59.2 14 upward bias to interest rates for a very Current (30-November-18): 2760 other markets continue 60 long time into the future should 2560 to show significant discounts to their fair value. A significant rise in inflation and interest rates 12 inflation premiums and real rates of will eventually reduce the sustainable 55 interest ultimately return to their long- 1280 level for valuations, but normalizing 10 term norms. P/E’s and corporate profitability to Last Plot: 2.99% reflect current levels for these 50 8 Current Range: 2.12% - 3.90% (Mid: 3.01%) 640 critical variables suggests % stock market valuations are reasonable, but 45 6 320 certainly not Solid gains in “cheap” in all revenues and earnings 4 Led by the U.S., PMIs remain at 160 locations. propelled U.S. stocks in 40 particular, but threats to levels consistent with expansion, 2 But in the near-term, the pressure but the trend everywhere is both are accumulating. -

Application of Machine Learning in High Frequency Trading of Stocks

International Journal of Scientific & Engineering Research Volume 10, Issue 5, May-2019 1592 ISSN 2229-5518 Application of Machine Learning in High Frequency Trading of Stocks Obi Bertrand Obi Worldquant University 201 St. Charles Avenue, Suite 2500 New Orleans, LA 70170, USA [email protected] Abstract Algorithmic trading strategies have traditionally been centered on follwing the market trends and the use of technical indicators. Over the years High Frequency algorithmic Trading has been left only in the hands of institutional players with deep pockets and lots of assets under management, despite huge returns involved. In this project webuilt trading strategies by applying Machine Learning models to technical indicators based on High Frequency Stock data. The result is an automated trading system which when applied to any stock could generate returns which are ten times higher than the market returns without significant increase in volatility. With advancement in technology High Frequency Algorithmic trading can be undertaken even by individuals or retail traders with moderate initial investment and technical skills. Keywords:Machine Lerning; Prediction of stock prices movements; Classification reports; Algorithmic trading; High frequency trading; Key performace indicators IJSER 1. Introduction Not too long ago, Algorithmic Trading was only available for institutional players with deep pockets and lots of assets under management. Recent developments in the areas of open source, open data, cloud computing and storage as well as online trading platforms have leveled the playing field for smaller institutions and individual traders, making it possible to venture in this fascinating discipline with only a modern notebook and an Internet connection. Nowadays, Python and its eco-system of powerful packages is the technology platform of choice for algorithmic trading. -

Trading Indicator Blueprint

Effective use of the most popular trading indicators www.netpicks.com This information is prepared solely for general information and educational purposes and is not a solicitation to buy or sell securities or financial products mentions in the content, nor a recommendation to participate in any particular trading strategy. Please consult your broker for trading advice. The author is not a broker on a licensed investment advisor and is not licensed to give trading advice or any sort, nor make specific trading recommendations. Entire risk disclosure can be found at www.sec.gov Whether you are a new or experienced trader, you are probably familiar with the multitude of trading indicators available. I know when I started trading almost a decade ago, virtually every indicator ended up on my charts at one time or another. And it was frustrating! You may be able to relate to: Always searching for the “perfect” combination of indicators for high probability trading setups. Tweaking inputs over and over again trying to “fit” the indicator to past price to match the perfect trade. Looking to “catch the turn” to avoid adverse excursion and to take every pip or tick the market is willing to give. Adverse Excursion The amount of loss an open trade takes before completion with profit or a loss. The hard truth is that PERFECTION does not exist in trading. 1 Neither does the perfect indicator or perfect setting. You can use indicators as part of an overall trading system and although that requires a lot of work and testing, it can be done! So where do you start? The majority of indicators use price in their mathematical calculations before plotting on your chart. -

Using the Z-Trend Oscillator for Long-Term Bond Market Timing

Using the Z-TrendOscillator for Long-Term Bond Market Timing 6 Submitted by Robert T. Zukowski, CMT March4. 1996 Overview Because it reflects mass psychology, the Coppock Curve is labeled by tnost technicians attd traders as a setttimettt This paper examines the concept of modifying the indicator. As a result, the curve siguals market tops and Coppock Curve to better identify major tops attd bottoms bottoms quite well and proves to be a valuable addition to in the bond futures market for lottg-term positioning. The atty trader’s tool kit. Coppock combined art 1 l- and 14 modified versiott of the Coppock Curve is referred to as mouth ROC, smoothed over by a lo-tnottth weighted mov- the Z-Trend Oscillator. Most oscillators are used for trad- ing average, which cat1 be explaitted by the yearly titne ing periods of price consolidation, but the Z-Trend Oscil- cycles frequent in tnost tnarket indices. A buy signal oc- lator is specifically used for trading all market cottditiotts curs when the curve turns up or becotnes positively sloped from accumulation, to trending, to distribution. while below the zero litte. A sell sigttal occurs when the curve turns down or becomes negatively sloped while Introduction to Rate of Change and the above the zero line. Coppock Curve Otte of the older, sitnpler tcchttical ittdicators to un- The Problem - Indicator Consistency derstand is the rate of chattge or ROC for short. ROC catt When the Coppock Curve is applied to the monthly confirm tnarket trends and forewarn of market reversals. continuation chart of U.S. -

“Identifying Explosive Behavioral Trace in the CNX Nifty Index: a Quantum Finance Approach”

“Identifying explosive behavioral trace in the CNX Nifty Index: a quantum finance approach” Bikramaditya Ghosh https://orcid.org/0000-0003-0686-7046 AUTHORS http://www.researcherid.com/rid/W-3573-2019 Emira Kozarević https://orcid.org/0000-0002-5665-640X Bikramaditya Ghosh and Emira Kozarević (2018). Identifying explosive ARTICLE INFO behavioral trace in the CNX Nifty Index: a quantum finance approach. Investment Management and Financial Innovations, 15(1), 208-223. doi:10.21511/imfi.15(1).2018.18 DOI http://dx.doi.org/10.21511/imfi.15(1).2018.18 RELEASED ON Saturday, 03 March 2018 RECEIVED ON Thursday, 28 December 2017 ACCEPTED ON Monday, 19 February 2018 LICENSE This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License JOURNAL "Investment Management and Financial Innovations" ISSN PRINT 1810-4967 ISSN ONLINE 1812-9358 PUBLISHER LLC “Consulting Publishing Company “Business Perspectives” FOUNDER LLC “Consulting Publishing Company “Business Perspectives” NUMBER OF REFERENCES NUMBER OF FIGURES NUMBER OF TABLES 39 4 8 © The author(s) 2021. This publication is an open access article. businessperspectives.org Investment Management and Financial Innovations, Volume 15, Issue 1, 2018 Bikramaditya Ghosh (India), Emira Kozarević (Bosnia and Herzegovina) Identifying Explosive BUSINESS PERSPECTIVES Behavioral Trace in the CNX Nifty Index: A Quantum Finance LLC “СPС “Business Perspectives” Approach Hryhorii Skovoroda lane, 10, Sumy, 40022, Ukraine www.businessperspectives.org Abstract The financial markets are found to be finite Hilbert space, inside which the stocks are displaying their wave-particle duality. The Reynolds number, an age old fluid -me chanics theory, has been redefined in investment finance domain to identify possible explosive moments in the stock exchange.