Securities and Exchange Commission Sec Form 20-Is

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

(Leaders, Experts, and Advocates

PROGRAM NAME OF PROVIDER ACCREDITATION. TITLE OF THE PROGRAM NO. 2009 Pharmacist LEADS (Leaders, 1 Pfizer, Inc. 2009-003-001 Experts, and Advocates on Drug Safety) Philippine Society for Parenteral 5th Annual PhilSPEN 2 and Enteral Nutrition (PHILSPEN), 2010-006-002 Convention Inc. University of the Philippines, Teaching Clinical Pharmacy: 3 2010-007-003 College of Pharmacy Competency Based Approach 2010 4 Pfizer, Inc. 2009-003-004 Pharmacist LEADS 5 Pfizer, Inc. 2009-003-004 Pharmacist LEADS 6 Pfizer, Inc. 2009-003-004 Pharmacist LEADS 7 Pfizer, Inc. 2009-003-004 Pharmacist LEADS 8 Pfizer, Inc. 2009-003-004 Pharmacist LEADS University of the Philippines, Teaching Clinical Pharmacy: 9 2010-007-005 College of Pharmacy Competency Based Approach Philippine Association of Hospital Formulary and 10 Pharmacists in the Pharmaceutical 2010-005-006 Cascade of ACCSQ-PWG Industry (PAPPI) Meetings Philippine Society for Parenteral 6th Annual Convention 11 and Enteral Nutrition (PHILSPEN), 2010-006-007 Theme: Clinical Nutrition: Inc. Basic Revisited Optimum Health Outcomes Unilab Medical Education & 12 2009-002-008 Through Medication Safety Development (UMED) (Module 2) 2011 The Quality of Health in Our 13 Pfizer, Inc. 2009-003-009 Hands Watsons Pharmacists 14 Watsons Personal Care Store 2010-004-010 Stepping Up to Help People Get More from Life Teaching Clinical Pharmacy: 15 College of Pharmacy, UP Manila 2010-007-011 Competency Based Approach Pharmacist LEADS-The 16 Pfizer, Inc. 2009-003-012 Quality of Health in Our Hands Philippine Pharmacists Association, Asian Conference on Clinical 17 2009-001-013 Inc. Pharmacy 2011 (ACCP 2011) Health and Wellness Watsons Personal Care Stores 18 2010-004-014 Counsellor Training Program- (Phils.) Dermatological and Asthma Clinical Skills Improvement 19 UP College of Pharmacy 2010-007-015 for Ambulatory and In-patient Services Philippine Society for Parenteral Evolutions and Revolutions in 20 and Enteral Nutrition (PHILSPEN), 2010-006-016 Nutrition Therapy Inc. -

SUMMARY of DONATION (DOMESTIC-RECEIVED ) As of 22 May 2020

SUMMARY OF DONATION (DOMESTIC-RECEIVED ) as of 22 May 2020 DATE DONOR SECTOR TYPE PARTICULARS AMOUNT RECIPIENT UPDATES 24-Mar-20 Maynilad Private In-Kind Purified Drinking Water 6,048.00 Office of Civil Defense Distributed 27-Mar-20 San Miguel Corp. Private In-Kind Alcohol 20 liters per gallon Office of Civil Defense Distributed 28-Mar-20 Pepsi Corp. Private In-Kind Purified Drinking Water 84,000.00 Office of Civil Defense Distibuted Private In-Kind Non Sterile Proctective Suit Office of Civil Defense Distributed Anonymous donor through Presidential 30-Mar-20 Private In-Kind Face Mask (surgical type) Office of Civil Defense Distributed Management Staff Private In-Kind Gloves (Surgical) Office of Civil Defense Distributed Private In-Kind Surgical Gloves 200,000.00 For distribution tp other beneficiaries Private In-Kind Personal Protective Clothing 1,279,700.00 For distribution tp other beneficiaries Private In-Kind Raincoat 300,000.00 Distributed 04-Apr-20 SM Foundation Office of Civil Defense Private In-Kind Shoe Cover 100,000.00 Distributed Private In-Kind Kn95 Masks 82,000.00 Distributed Private In-Kind Surgical Face Masks 1,000,000.00 Distributed Private In-Kind Alcohol 438,000.00 Distributed Private In-Kind Mask(surgical) Office of Civil defense Distributed 06-Apr-20 Fastel Service Inc. Private In-Kind 25 kls Sacks of Rice Office of Civil Defense Distributed 07-Apr-20 Philippine Spring Water resources Inc. Private In-Kind Purified Drinking Water(500 ml) 6,048.00 Office of Civil Defense For Distribution to other beneficiaries 08-Apr-20 Trend Micro Private In-Kind Surgical Face Masks Office of Civil Defense For Distribution to other beneficiaries Civil Society In-Kind Kn95 Masks 12,375,000.00 Office of Civil Defense Federation of Indian Chambers of Commerce (PH) 09-Apr-20 Distributed Inc. -

This Directory Is As of August 04, 2016 METRO MANILA PICK-UP CHANNEL PROVINCE AREA/CITY ADDRESS PALAWAN PAWNSHOP METRO MANILA MANILA 1738 D JUAN ST

METRO MANILA PICK-UP CHANNEL PROVINCE AREA/CITY ADDRESS PALAWAN PAWNSHOP METRO MANILA CALOOCAN CITY UNIT B-5 A. MABINI STREET, CALOOCAN CITY LANDMARK: WITHIN SANGANDAAN PLAZA, A. MABINI PALAWAN PAWNSHOP METRO MANILA CALOOCAN CITY 368 EDSA, CALOOCAN CITY LANDMARK: FRONT OF MCU (MANILA CENTRAL UNIVERSITY) PALAWAN PAWNSHOP METRO MANILA CALOOCAN CITY STALL #1, MARIETTA ARCADE, 1107 GE. SAN MIGUEL ST., SANGANDAAN, CALOOCAN LANDMARK: NEAR UNIVERSITY OF CALOOCAN RD PAWNSHOP METRO MANILA CALOOCAN CITY 149-D AVE., GRACE PARK, CALOOCAN CITY RD PAWNSHOP METRO MANILA CALOOCAN CITY A1 LTL BLDG. CAMARIN RD. COR. SIKATUNA AVE. URDEJA V CARD BANK METRO MANILA LAS PIÑAS CITY BRGY E. ALDANA REAL ST. LAS PIÑAS CITY PALAWAN PAWNSHOP METRO MANILA LAS PIÑAS CITY 407 ALABANG-ZAPOTE RD., TALON 1, LAS PINAS LANDMARK: FRONT OF MOONWALK MARKET PALAWAN PAWNSHOP METRO MANILA LAS PIÑAS CITY 487 ALMANZA GREGORIO AVENUE, LAS PIÑAS CITY LANDMARK: NEAR SM SOUTH MALL PALAWAN PAWNSHOP METRO MANILA LAS PIÑAS CITY 325 DE GUZMAN COMPOUND, REAL ST. PULANG LUPA 1, LASPINAS CITY LANDMARK: NEAR SHELL STATION PALAWAN PAWNSHOP METRO MANILA LAS PIÑAS CITY UNIT H, ZAPOTE-ALABANG RD, PAMPLONA, LAS PIÑAS LANDMARK: NEAR ZAPOTE FLYOVER PALAWAN PAWNSHOP METRO MANILA LAS PIÑAS CITY BLK 2 LOT 12 CAA ROAD, AGUILAR AVE., PULANG LUPA DOS, LAS PINAS CITY LANDMARK: IN FRONT OF MARY QUEEN OF APOSTLES PARISH PALAWAN PAWNSHOP METRO MANILA LAS PIÑAS CITY 400 REAL ST., TALON, LAS PINAS CITY LANDMARK : NEAR PUREGOLD MOONWALK RD PAWNSHOP METRO MANILA LAS PIÑAS CITY BLDG. B, CTC COMM. REAL ST. RD PAWNSHOP METRO MANILA LAS PIÑAS CITY 400 REAL ST. -

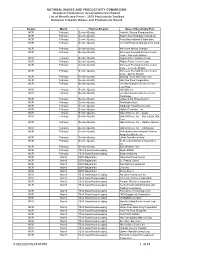

Name of Provider Program Accreditation. No. Title Of

PROGRAM TITLE OF THE DATE OF CONDUCT APPROVED NAME OF PROVIDER ACCREDITATION. PLACE CONDUCTED PROGRAM CREDIT UNIT NO. FROM TO 2009 Pharmacist LEADS (Leaders, Experts, and 1 Pfizer, Inc. 2009-003-001 07-May-09 Iloilo 3 Advocates on Drug Safety) 08-May-09 Bacolod Philippine Society for Parenteral 5th Annual PhilSPEN 13-Nov- 2 and Enteral Nutrition 2010-006-002 12-Nov-09 Manila Diamond Hotel 8 Convention 09 (PHILSPEN), Inc. Teaching Clinical University of the Philippines, UP College of 3 2010-007-003 Pharmacy: Competency 15-Oct-09 17-Oct-09 22 College of Pharmacy Pharmacy Based Approach 2010 4 Pfizer, Inc. 2009-003-004 Pharmacist LEADS Jun-10 Cebu 5 5 Pfizer, Inc. 2009-003-004 Pharmacist LEADS Jul-10 San Pablo / Quezon 5 6 Pfizer, Inc. 2009-003-004 Pharmacist LEADS Sep-10 Baguio 5 7 Pfizer, Inc. 2009-003-004 Pharmacist LEADS Nov-10 Ilocos Norte 5 8 Pfizer, Inc. 2009-003-004 Pharmacist LEADS Dec-10 Manila 5 Teaching Clinical University of the Philippines, College of Pharmacy 9 2010-007-005 Pharmacy: Competency 21-Oct-10 23-Oct-10 20 College of Pharmacy and PGH, UP Manila Based Approach Philippine Association of Hospital Formulary and Pharmacists in the 10 2010-005-006 Cascade of ACCSQ-PWG 24-Sep-10 Glaxosmithkline Phils. 3 Pharmaceutical Industry Meetings (PAPPI) Philippine Society for Parenteral 6th Annual Convention 09-Nov- 11 and Enteral Nutrition 2010-006-007 Theme: Clinical Nutrition: 08-Nov-10 Manila Diamond Hotel 12 10 (PHILSPEN), Inc. Basic Revisited Optimum Health Unilab Medical Education & Outcomes Through Galaxias Function 12 2009-002-008 14-Jan-11 8 Development (UMED) Medication Safety (Module Room, Diamond Hotel 2) 2011 The Quality of Health in 13 Pfizer, Inc. -

PRIVATE and CONFIDENTIAL June 3, 2020 EMBASSY of BRAZIL 16Th

PRIVATE AND CONFIDENTIAL June 3, 2020 EMBASSY OF BRAZIL 16th Floor, Liberty Center, 104 H.V. de la Costa Street, Salcedo Village Makati City, Philippines Attention: H.E. Rodrigo do Amaral Souza Ambassador Your Excellency: We are pleased to submit the Market Research Report on Medicaments that we prepared for the Embassy of Brazil in Manila. The report incorporates the comments and additions to the draft submitted on February 28, 2020. The information and data presented were gathered through research and interviews with representatives of relevant agencies and associations. Our report was prepared prior to the COVID-19 pandemic announcement by the World Health Organization on March 11, 2020. There may have been changes in the Philippine economic and business conditions brought about by the pandemic which may affect the forecasts and estimates provided in the report. Reyes Tacandong & Co. (RT&Co.) assumes no responsibility for updating or revising this report based on circumstances, developments or events occurring after this date. We understand that the results of the market research will be shared with appropriate agencies of the Government of Brazil as well as private sector entities for the purpose of generating interest in doing business in the Philippines. It is not to be used for any other purpose or to be distributed to any other party. We would like to thank the Embassy of Brazil in Manila for the opportunity to be of service. Very truly yours, Mildred R. Ramos Managing Partner, Advisory Services PRIVATE AND CONFIDENTIAL Medicaments Market Research Report Disclaimer This Report was prepared after the COVID-19 pandemic announcement by the World Health Organization on March 11, 2020. -

ACCREDITED DENTISTS August 2018

Where beautiful smiles begin www.elitegroup.com.ph ACCREDITED DENTISTS www.elitegroup.com.ph August 2018 TABLE OF CONTENTS Area Page No. Area Page No. Area Page No. NCR – METRO MANILA 3 REGION 2 - CAGAYAN VALLEY 12 REGION 7 - CENTRAL VISAYAS 19 Caloocan City 3 Cagayan 12 Bohol 19 Las Piñas City 3 Isabela 12 Cebu 19 Makati City 3 Nueva Vizcaya 12 Malabon 4 REGION 8 - EASTERN VISAYAS 20 Mandaluyong 4 REGION 3 - CENTRAL LUZON 12 Leyte 20 Manila 5 Aurora 12 Northern Samar 20 Binondo 5 Bataan 12 Samar 20 Sta. Cruz 5 Bulacan 12 Marikina City 5 Nueva Ecija 13 REGION 9 - ZAMBOANGA PENINSULA 20 Muntinlupa City 6 Pampanga 13 Zamboanga del Sur 20 Navotas City 6 Tarlac 14 Parañaque 6 Zambales 14 REGION 10 - NORTHERN MINDANAO 21 Pasay City 7 Bukidnon 21 Pasig City 7 REGION 4A - CALABARZON 14 Lanao del Norte 21 Ortigas Center 7 Batangas 14 Misamis Occidental 21 The Medical Center 8 Cavite 15 Misamis Oriental 21 Pateros 8 Laguna 16 Quezon City 8 Quezon 17 REGION 11 - DAVAO REGION 21 Cubao 10 Rizal 17 Davao del Sur 21 Libis 10 Davao del Norte 22 Novaliches 10 REGION 4B – MIMAROPA 18 St. Lukes Medical Center 10 Occidental Mindoro 18 REGION 12 – SOCCSKSARGEN 22 San Juan 10 Oriental Mindoro 18 North Cotabato 22 Taguig 10 Palawan 18 South Cotabato 22 Valenzuela 11 Sultan Kudarat 22 REGION 5 - BICOL REGION 18 CAR – Albay 18 REGION 13 – CARAGA 22 CORDILLERA ADMINISTRATIVE REGION 11 Camarines Sur 19 Agusan del Norte 22 Benguet 11 Masbate 19 Agusan del Sur 22 REGION 1 - ILOCOS REGION 11 REGION 6 - WESTERN VISAYAS 19 ARMM 22 Ilocos Norte 11 Aklan 19 Maguindanao 22 La Union 11 Capiz 19 Pangasinan 11 Iloilo City 19 Negros Occidental 19 Page | 2 ACCREDITED DENTISTS www.elitegroup.com.ph August 2018 National Capital Region Location: opposite MCU Hospital; located at Access Computer DR. -

Of 83 01/02/2020 06:18:57 PM 1 NATIONAL WAGES AND

NATIONAL WAGES AND PRODUCTIVITY COMMISSION Regional Productivity Accomplishment Report List of Beneficiary Firms - 2019 Productivty Toolbox Regional Tripartle Wages and Productivity Board Region Month Training Program Name of Beneficiary Firm NCR February Service Quality Yakiniku Sakura Restaurant Inc. NCR February Service Quality Airport Juan Holdings Corporation NCR February Service Quality Fersal International Corporation NCR February Service Quality Vermont Property Management Corp. NCR February Service Quality Achievers Money Changer NCR February Service Quality Achievers Fuel and Service Center Corp. - San Isidro Branch NCR February Service Quality Rogers Place Condotel Corp. NCR February Service Quality Filipino Travel Center Corp. NCR February Service Quality Achievers Fuel and Service Center Corp. - Ireneville Branch NCR February Service Quality Achievers Fuel and Service Center Corp. - Quirino Branch NCR February Service Quality Baliwag Tours and Travel, Inc. NCR February Service Quality Han Nan Food Corporation NCR February Service Quality Jen Star Gasoline Service Center - Las Piñas NCR February Service Quality HAREM, Inc. NCR February Service Quality Jen Star Gasoline Service Center - Paranaque NCR February Service Quality Jupiter Arms Properties Inc. NCR February Service Quality The Manila Hotel NCR February Service Quality Katipunan Food Services Inc. NCR February Service Quality Malate Pensionne, Inc. NCR February Service Quality Max's Kitchen, Inc. - Ayala NCR February Service Quality Max's Kitchen, Inc. - San Lazaro, Sta. Cruz NCR February Service Quality Max's Kitchen, Inc. - Harbour Square NCR February Service Quality Max's Kitchen, Inc. - Intramuros NCR February Service Quality Metropolitan International Christian Academy (MICA), Inc. NCR February Service Quality Urban Traveller's Hotel NCR February Service Quality St. Benedict School of Novaliches, Inc. -

SUMMARY of DONATION (DOMESTIC-RECEIVED) As of 27 May 2020

SUMMARY OF DONATION (DOMESTIC-RECEIVED) as of 27 May 2020 QUANTI DATE DONOR SECTOR TYPE UNIT PARTICULARS RECIPIENT UPDATES TY 24-Mar-20 Maynilad Private In-Kind 720 bott Purified Drinking Water Office of Civil Defense Distributed 27-Mar-20 San Miguel Corp. Private In-Kind 10 gal Alcohol 20 liters per gallon Office of Civil Defense Distributed 28-Mar-20 Pepsi Corp. Private In-Kind 10,000 bott Purified Drinking Water Office of Civil Defense Distibuted Private In-Kind 500 pcs Non Sterile Proctective Suit Office of Civil Defense Distributed 30-Mar-20 Anonymous donor through Presidential Management Staff Private In-Kind 75,600 pcs Face Mask (surgical type) Office of Civil Defense Distributed Private In-Kind 10,000 pcs Gloves (Surgical) Office of Civil Defense Distributed Private In-Kind 20,000 pcs Surgical Gloves For distribution tp other beneficiaries Private In-Kind 5,000 pcs Personal Protective Clothing For distribution tp other beneficiaries Private In-Kind 10,000 pcs Raincoat Distributed 04-Apr-20 SM Foundation Office of Civil Defense Private In-Kind 20,000 pcs Shoe Cover Distributed Private In-Kind 1,000 pcs Kn95 Masks Distributed Private In-Kind 50,000 pcs Surgical Face Masks Distributed Private In-Kind 1,000 gal Alcohol Distributed Private In-Kind 2,000 pcs Mask(surgical) Office of Civil defense Distributed 06-Apr-20 Fastel Service Inc. Private In-Kind 28 pcs 25 kls Sacks of Rice Office of Civil Defense Distributed 07-Apr-20 Philippine Spring Water resources Inc. Private In-Kind 120,960 pcs Purified Drinking Water(500 ml) Office of Civil Defense For Distribution to other beneficiaries 08-Apr-20 Trend Micro Private In-Kind 100 pcs Surgical Face Masks Office of Civil Defense For Distribution to other beneficiaries Civil Society In-Kind 75,000 pcs Kn95 Masks Office of Civil Defense 09-Apr-20 Federation of Indian Chambers of Commerce (PH) Inc. -

Lhp Cles Legs Tiwi Community College Oas Community College Bicol University Zamora Memorial College San Jose Community College D

LEES CONDUCTED LHP CLES LEGS Small Talk Café TIWI COMMUNITY COLLEGE Divine Word College of Legazpi (DWCL) Glamoreux Salon OAS COMMUNITY COLLEGE STI COLLEGE LEGAZPI PNB BICOL UNIVERSITY LEGAZPI CITY SCIENCE HIGH SCHOOL Hi-tone Security Agency ZAMORA MEMORIAL COLLEGE ST. AGNES ACADEMY Apple Peach House SAN JOSE COMMUNITY COLLEGE SOUTH LUZON TECHNOLOGICAL COLLEGES FOUNDATION, INC. CASABLANCA HOTEL DR. CARLOS LANTING COLLEGE UNIVERSITY OF SANTO TOMAS - LEGAZPI 7 DEGREES GRILL & RESTAURANT COLEGIO DE STA. ISABELA OF POLANGUI MARCIAL O. RAÑOLA MEMORIAL SCHOOL HOTEL REX TESDA ALBAY PONSO NATIONAL HIGH SCHOOL BICOL BESTRADO DANIEL B. PEÑA MEMORIAL COLLEGE FOUNDATION ST. RAPHAEL ACADEMY EBG MANPOWER DEPED ALBAY DIVISION MALINAO NATIONAL HIGH SCHOOL Fornix Corporation POLANGUI COMMUNITY COLLEGE LIGAO NATIONAL HIGH SCHOOL Belleza Transport Corp. SOUTHERN LUZON COMMUNITY COLLEGE MABINI COLLEGES, INC. CENTRAL PLAZA RESTAURANT LIBON COMMUNITY COLLEGE CAMARINES NORTE STATE COLLEGE GUISICAN MULTI PURPOSE COOP. AQUINAS UNIVERSITY OF LEGAZPI LA CONSOLACION COLLEGE KOOPERATIBA PARA SA MALILIIT NA MAGNINIYOG NG BRGY. KAPANAWAN POLYTECHNIC INSTITUTE OF TABACO AMA COMPUTER LEARNING CENTER STO. NIŇO HOSPITAL (HERRMONTE MEDICAL CLINIC) DIVINE WORLD COLLEGE OF LEGAZPI MARIA AURORA ACADEMY LISAZO HOSPITAL AGO MEDICAL & EDUCATIONAL CENTER RIZAL NATIONAL HIGH SCHOOL DAET ELEM. SCHOOL TEACHER'S COOP. AMANDO COPE COLLEGE RIZAL NATIONAL HIGH SCHOOL FLOWER SHOP & LAPIDA FORBES COLLEGE STA. ELENA COLLEGE, INC. MANG INASAL ZAMORA MEMORIAL COLLEGE STA. ELENA COLLEGE, INC. -

PAPPI PAPPI First General Membership Meeting 21-Mar-14

DATE OF CONDUCT NAME OF PROVIDER TITLE OF THE PROGRAM PLACE CONDUCTED FROM TO Nathan Hall GSK 57 PAPPI PAPPI First General Membership Meeting 21-Mar-14 Compound, Pasong Tamo Extn Makati City Augusto Barcelon 1st Postgraduate Course in Critical Care The Medical City 12-Apr-14 14-Apr-14 Auditorium The Medical 58 Pharmacy City Mariano K. Tan Hall UL Developing Filipino Pharmacists Competency Bayanihan Center PPhA, Inc. "Moving Mainstream Practice toward Clinical 28-Mar-14 30-Mar-14 59 Pioneer St. Mandaluyong Pharmacy" City "Access to Pharmacists, Access to Better Teacher's Conference PPhA, Inc. 21-Feb-14 60 Health" Room, Batangas City "Access to Pharmacists, Access to Better Garden Orchid Hotel, PPhA, Inc. 15-Mar-14 61 Health" Zamboanga City "Access to Pharmacists, Access to Better The Tavern Hotel, PPhA, Inc. 22-Mar-14 62 Health" Surigao City City Bakeshop and "Access to Pharmacists, Access to Better PPhA, Inc. 05-Apr-14 Restaurant, Dagupan 63 Health" City, Pangasinan "Access to Pharmacists, Access to Better San Carlos City, Negros PPhA, Inc. 03-May-14 64 Health" Occidental "Access to Pharmacists, Access to Better PPhA, Inc. 24-May-14 Quezon City 65 Health" "Access to Pharmacists, Access to Better PPhA, Inc. 30-May-14 Isabela 66 Health" "Access to Pharmacists, Access to Better Crown Hotel, Camarines PPhA, Inc. 07-Jun-14 67 Health" Sur "Access to Pharmacists, Access to Better Iligan City, Lanao del PPhA, Inc. 05-Jul-14 68 Health" Norte "Access to Pharmacists, Access to Better Venue 88, General PPhA, Inc. 19-Jul-14 69 Health" Santos City AJ, Hi-Time Hotel, "Access to Pharmacists, Access to Better PPhA, Inc. -

Ppp in Health Manila 2012

Appendix 10 PPP IN HEALTH MANILA 2012 DEVELOPING MODELS, ENSURING SUSTAINABILITY: PERSPECTIVES FROM ASIA AND EUROPE DRAFT PROCEEDINGS OF THE REGIONAL FORUM EDITED BY CHANTAL HERBERHOLZ TA 7257-PHI: Public-Private Partnership in Health Consultant’s Final Report Table of Contents Foreword ....................................................................................................................................................... 4 Contributors .................................................................................................................................................. 5 Acknowledgements ..................................................................................................................................... 14 Abbreviations .............................................................................................................................................. 16 Forum Synthesis and Summary .................................................................................................................. 18 Introduction to the Proceedings ................................................................................................................. 34 Part I: PPP in Health: Overview and Best Practices .................................................................................... 35 1. Opening Ceremonies ....................................................................................................................... 35 1.1. Welcome Remarks ................................................................................................................. -

Complainant Respondent Status NCR-01-00001-19 MICHAEL JOHN COLEGADO DE GRACIA LUCKBAY TRUCKING PENDING NCR-01-00002-19 JAIME BAYONAS PESCADERO, Et

Status of Cases 2nd Quarter 2019 Case No. Complainant Respondent Status NCR-01-00001-19 MICHAEL JOHN COLEGADO DE GRACIA LUCKBAY TRUCKING PENDING NCR-01-00002-19 JAIME BAYONAS PESCADERO, et. al. UNO TRANSPORT PENDING NCR-01-00004-19 ARTHUR BERNANTE TOLEDO, JR. S & I INTERNATIONAL MANAGEMENT INC. PENDING NCR-01-00006-19 MICHAEL LEONARDO LACTAO CITIGROUP BUSINESS PROCESS SOLUTIONS PENDING NCR-01-00007-19 RAYMUNDO ABUTIN PEREZ VARIANCE SECURITY AGENCY CORPORATION PENDING NCR-01-00011-19 RODOLFO RODRIGO ISANAN FINMAT INTERNATIONAL RESOURCES INC. DISPOSED NCR-01-00012-19 JORGE PURA LICOBEN BERROD DEVELOPMENT CORPORATION PENDING NCR-01-00013-19 ROMEO MONTOYA ASIS BUILDER 1927 PENDING NCR-01-00014-19 WILLIAM TINAMPAY PAGUIA SLC MACHINE SHOP PENDING NCR-01-00015-19 PAUL HIZON ESPIRITU III DELS APPAREL CORPORATION PENDING NCR-01-00017-19 LUZ DELA CRUZ RAYMUNDO, et. al. DELA SALLE UNIVERSITY - CENTER FOR LANGUAGE PENDING NCR-01-00018-19 PAMELA AVILA ESPIRITU PHILIPPINE RED CROSS DISPOSED NCR-01-00025-19 JOSE JOEL EWAYAN LAWAS ST. ANTHONY OF PADUA TRANSPORT PENDING NCR-01-00026-19 RICO PALAY MARCELLANA, et. al. COSMIC ENTERPRISES INC. PENDING 1.KENSONIC INC. / ONE ALPHA COMMUNICATION NCR-01-00028-19 NEIL PEREZ BALEÑA 2.AXELERATE MANPOWER AGENCY INC. DISPOSED NCR-01-00029-19 ROMMEL LINAJA MARABE JOVEN ESPIRITU ELECTRICAL SERVICES PENDING NCR-01-00033-19 RAYMOND FULO HERRERA COFFRAL FORMWORKS AND SCAFFOLDS INC. PENDING NCR-01-00036-19 CARMELO GALWAT MAGALIM MAYON SECURITY AGENCY DISPOSED NCR-01-00038-19 ERIC JOSEPH YOUNG MANANQUIL LEISURE & RESORT WORLD CORPORATION DISPOSED NCR-01-00043-18 ROSANNA ALBORQUE ARGANTE LUFTHANSA TECHNIK PHILIPPINES (LTP) DISPOSED NCR-01-00043-19 JIMMUEL ROMAY TAYING, et.