Enhanced Coppock Curve

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Copyrighted Material

INDEX Page numbers followed by n indicate note numbers. A Arnott, Robert, 391 Ascending triangle pattern, 140–141 AB model. See Abreu-Brunnermeier model Asks (offers), 8 Abreu-Brunnermeier (AB) model, 481–482 Aspray, Thomas, 223 Absolute breadth index, 327–328 ATM. See Automated teller machine Absolute difference, 327–328 ATR. See Average trading range; Average Accelerated trend lines, 65–66 true range Acceleration factor, 88, 89 At-the-money, 418 Accumulation, 213 Average range, 79–80 ACD method, 186 Average trading range (ATR), 113 Achelis, Steven B., 214n1 Average true range (ATR), 79–80 Active month, 401 Ayers-Hughes double negative divergence AD. See Chaikin Accumulation Distribution analysis, 11 Adaptive markets hypothesis, 12, 503 Ayres, Leonard P. (Colonel), 319–320 implications of, 504 ADRs. See American depository receipts ADSs. See American depository shares B 631 Advance, 316 Bachelier, Louis, 493 Advance-decline methods Bailout, 159 advance-decline line moving average, 322 Baltic Dry Index (BDI), 386 one-day change in, 322 Bands, 118–121 ratio, 328–329 trading strategies and, 120–121, 216, 559 that no longer are profitable, 322 Bandwidth indicator, 121 to its 32-week simple moving average, Bar chart patterns, 125–157. See also Patterns 322–324 behavioral finance and pattern recognition, ADX. See Directional Movement Index 129–130 Alexander, Sidney, 494 classic, 134–149, 156 Alexander’s filter technique, 494–495 computers and pattern recognition, 130–131 American Association of Individual Investors learning objective statements, 125 (AAII), 520–525 long-term, 155–156 American depository receipts (ADRs), 317 market structure and pattern American FinanceCOPYRIGHTED Association, 479, 493 MATERIALrecognition, 131 Amplitude, 348 overview, 125–126 Analysis pattern description, 126–128 description of, 300 profitability of, 133–134 fundamental, 473 Bar charts, 38–39 Andrews, Dr. -

Stock Market Explained

Stock Market Explained A Beginner's Guide to Investing and Trading in the Modern Stock Market © Ardi Aaziznia www.PeakCapitalTrading.com Copyrighted Material © Peak Capital Trading CHAPTER 1 Copyrighted Material © Peak Capital Trading Figure 1.1: “covid-19” and “stock market” keyword Google search trends between April 2019 and April 2020. As you can see, there is a clear correlation. As the stock market drop hit the news cycles, people started searching more and more about the stock market in Google! Copyrighted Material © Peak Capital Trading COVID-19 Bear Market 2019 Bull Market 2020 recession due to pandemic v Figure 1.2: Comparison between the bull market of 2019 and the bear market of 2020, as shown by the change in share value of 500 of the largest American companies. These companies are tracked by the S&P 500 and are traded in an exchange-traded fund known as the SPDR S&P 500 ETF Trust (ticker: SPY). For your information, S&P refers to Standard & Poor’s, one of the indices which used to track this information. Copyrighted Material © Peak Capital Trading Figure 1.3: How this book is organized. Chapters 1-4 and 7-11 are written by me. Chapters 5 and 6 on day trading are written by Andrew Aziz. Copyrighted Material © Peak Capital Trading CHAPTER 2 Copyrighted Material © Peak Capital Trading Figure 2.1: The return on investing $100 in an exchange-traded fund known as the SPDR S&P 500 ETF Trust (ticker: SPY) (which tracks the share value of 500 of the largest American companies (as rated by the S&P 500)) vs. -

The Best Candlestick Patterns

Candlestick Patterns to Profit in FX-Markets Seite 1 RISK DISCLAIMER This document has been prepared by Bernstein Bank GmbH, exclusively for the purposes of an informational presentation by Bernstein Bank GmbH. The presentation must not be modified or disclosed to third parties without the explicit permission of Bernstein Bank GmbH. Any persons who may come into possession of this information and these documents must inform themselves of the relevant legal provisions applicable to the receipt and disclosure of such information, and must comply with such provisions. This presentation may not be distributed in or into any jurisdiction where such distribution would be restricted by law. This presentation is provided for general information purposes only. It does not constitute an offer to enter into a contract on the provision of advisory services or an offer to buy or sell financial instruments. As far as this presentation contains information not provided by Bernstein Bank GmbH nor established on its behalf, this information has merely been compiled from reliable sources without specific verification. Therefore, Bernstein Bank GmbH does not give any warranty, and makes no representation as to the completeness or correctness of any information or opinion contained herein. Bernstein Bank GmbH accepts no responsibility or liability whatsoever for any expense, loss or damages arising out of, or in any way connected with, the use of all or any part of this presentation. This presentation may contain forward- looking statements of future expectations and other forward-looking statements or trend information that are based on current plans, views and/or assumptions and subject to known and unknown risks and uncertainties, most of them being difficult to predict and generally beyond Bernstein Bank GmbH´s control. -

Data Visualization and Analysis

HTML5 Financial Charts Data visualization and analysis Xinfinit’s advanced HTML5 charting tool is also available separately from the managed data container and can be licensed for use with other tools and used in conjunction with any editor. It includes a comprehensive library of over sixty technical indictors, additional ones can easily be developed and added on request. 2 Features Analysis Tools Trading from Chart Trend Channel Drawing Instrument Selection Circle Drawing Chart Duration Rectangle Drawing Chart Intervals Fibonacci Patterns Chart Styles (Line, OHLC etc.) Andrew’s Pitchfork Comparison Regression Line and Channel Percentage (Y-axis) Up and Down arrows Log (Y-axis) Text box Show Volume Save Template Show Data values Load Template Show Last Value Save Show Cross Hair Load Show Cross Hair with Last Show Min / Max Show / Hide History panel Show Previous Close Technical Indicators Show News Flags Zooming Data Streaming Full Screen Print Select Tool Horizontal Divider Trend tool Volume by Price Horizonal Line Drawing Book Volumes 3 Features Technical Indicators Acceleration/Deceleration Oscillator Elliot Wave Oscillator Accumulation Distribution Line Envelopes Aroon Oscilltor Fast Stochastic Oscillator Aroon Up/Down Full Stochastic Oscillator Average Directional Index GMMA Average True Range GMMA Oscillator Awesome Oscillator Highest High Bearish Engulfing Historical Volatility Bollinger Band Width Ichimoku Kinko Hyo Bollinger Bands Keltner Indicator Bullish Engulfing Know Sure Thing Chaikin Money Flow Lowest Low Chaikin Oscillator -

Trading System Development

Trading System Development An Interactive Qualifying Project Submitted to the Faculty of WORCESTER POLYTECHNIC INSTITUTE In partial fulfillment of the requirements for the Degree of Bachelor of Science By Brian O’Day Dylan Stimson Branden Diniz Submitted to: Prof. Michael Radzicki (advisor) Prof. Hossein Hakim (co-advisor) May 9, 2015 Abstract The purpose of this project was to construct a system of trading systems that would demonstrate a successful long term return on investment across different market conditions. The team was given $300,000 to distribute amongst three scientifically developed systems on the TradeStation platform provided by our advisors. The strategies were designed to incorporate both technical and fundamental data as well as trade diverse markets. The resulting cultivation of systems involved the use of two automated trading strategies and one manual trading strategy that showed substantial profits in the long term. 1 Acknowledgments We would like to thank Professor Radzicki and Professor Hakim for their guidance and support throughout the course of the project. We would also like to thank TradeStation for providing us with a platform for trading that made this project possible. 2 Authorship Page Introduction - Brian Problem Statement - Brian Overview of Systems - All Foundations of Trading and Investing Trading vs Investing - Branden Types of Exchanges - Branden, Dylan Investment Funds - Dylan Types of Orders - Dylan Market Conditions - Dylan Trading different Time Frames - Brian, Branden Costs of Trading/Investing -

Candlestick Patterns

INTRODUCTION TO CANDLESTICK PATTERNS Learning to Read Basic Candlestick Patterns www.thinkmarkets.com CANDLESTICKS TECHNICAL ANALYSIS Contents Risk Warning ..................................................................................................................................... 2 What are Candlesticks? ...................................................................................................................... 3 Why do Candlesticks Work? ............................................................................................................. 5 What are Candlesticks? ...................................................................................................................... 6 Doji .................................................................................................................................................... 6 Hammer.............................................................................................................................................. 7 Hanging Man ..................................................................................................................................... 8 Shooting Star ...................................................................................................................................... 8 Checkmate.......................................................................................................................................... 9 Evening Star .................................................................................................................................... -

© 2012, Bigtrends

1 © 2012, BigTrends Congratulations! You are now enhancing your quest to become a successful trader. The tools and tips you will find in this technical analysis primer will be useful to the novice and the pro alike. While there is a wealth of information about trading available, BigTrends.com has put together this concise, yet powerful, compilation of the most meaningful analytical tools. You’ll learn to create and interpret the same data that we use every day to make trading recommendations! This course is designed to be read in sequence, as each section builds upon knowledge you gained in the previous section. It’s also compact, with plenty of real life examples rather than a lot of theory. While some of these tools will be more useful than others, your goal is to find the ones that work best for you. Foreword Technical analysis. Those words have come to have much more meaning during the bear market of the early 2000’s. As investors have come to realize that strong fundamental data does not always equate to a strong stock performance, the role of alternative methods of investment selection has grown. Technical analysis is one of those methods. Once only a curiosity to most, technical analysis is now becoming the preferred method for many. But technical analysis tools are like fireworks – dangerous if used improperly. That’s why this book is such a valuable tool to those who read it and properly grasp the concepts. The following pages are an introduction to many of our favorite analytical tools, and we hope that you will learn the ‘why’ as well as the ‘what’ behind each of the indicators. -

Harmonic Conditions How to Define Price and Time Cycles

Interview: Tim Hayes – A Class of its Own Your Personal Trading Coach Issue 03, April 2010 | www.traders-mag.com | www.tradersonline-mag.com Harmonic Conditions How to Define Price and Time Cycles Great Profi ts through When to Trade The Right Use of Failed Chart Patterns & When to Fade Cyclical Analysis We Show You How to Recognise Them Gaining an Edge in Forex Trading Timing Is Everything for Lasting Success TRADERS´EDITORIAL Harmonising Price with Time Harmonising price with time is one of the issues serious traders grapple with at one point in their careers. And how could this possibly be otherwise? After all, if you wish to predict the future you have to consider the past. And if you look back on the history of trading, you will automatically end up coming across some of the heroes who have written this history. Jesse Livermore is one of them, so is Ralph Nelson Elliott and, last but not least, William D. Gann. Among all the greats of the trade he certainly stands out as the enigma. Square of Nine, Gann Lines and Gann Angles, the law of vibration of the sphere of activity, i.e. the rate of internal vibration all of which you will come The harmony of price and time results in incredible forecasts across once you begin to study the trading hero. Gann’s forecasts are credited with 90% success rates and his trading results are said to have amounted to 50 million dollars. Considering that he lived from1878 to 1955, it is easy to imagine what an incredible fortune this would be today. -

The Boundaries of Technical Analysis Milton W

The Boundaries of Technical Analysis Milton W. Berg, CFA 1 Market Prognostication In his treatise on stock market patterns, the late Professor Harry V. Roberts1 observed that “of all economic time series, the history of stock prices, both individual and aggregate, has probably been most widely and intensively studied,” and “patterns of technical analysis may be little if nothing more than a statistical artifact.”2 Ibbotson and Sinquefield maintain that historical stock price data cannot be used to predict daily, weekly or monthly percent changes in the market averages. However, they do claim the ability to predict in advance the probability that the market will move between +X% and -Y% over a specific period.3 Only to this very limited extent – forecasting the probabilities of return – can historical stock price movements be considered indicative of future price movements. In Chart 1, we present a histogram of the five-day rate of change (ROC) in the S&P 500 since 1928. The five-day ROC of stock prices has ranged from -27% to + 24%. This normal distribution4 is strong evidence that five-day changes in stock prices are effectively random. Out of 21,165 observations of five-day ROCs, there have been 138 declines exceeding -8%, (0.65% of total) and 150 gains greater than +8% (0.71% of total). Accordingly, Ibbotson and Sinquefield would maintain that over any given 5-day period, the probability of the S&P 500 gaining or losing 8% or more is 1.36%. Stated differently, the probabilities of the S&P 500 returning between -7.99% and +7.99% are 98.64%. -

Ned Davis Research Group

Ned Davis Research Group THE OUTLooK FOR StoCKS, CoMMODITIES, AND GLOBAL THEMES: SECULAR AND CYCLICAL INFLUENCES Atlanta MTA & CFA Society of Atlanta | September 24, 2008 Tim Hayes, CMT, Chief Investment Strategist The NDR Approach • Identify investment themes and stay with them until a sentiment extreme is reached. • We say… » "Go with the flow until it reaches an extreme and then reverses." » "The big money is made on the big moves." » "Let your profits run, cut your losses short." • We develop reliable indicators and models based on… » "The Tape" – Trend, momentum, confirmation & divergence. » Investor psychology – Sentiment and valuation extremes. » Liquidity – Monetary and economic conditions, supply & demand. • In summary, NDR approach is… » Objective » Disciplined » Risk-Averse » Flexible 1 Ned Davis Research Group Please see important disclosures at the end of this document. CURRENT POSITIONS Global Allocation: Overweight/Bullish: Underweight/Bearish: Stocks » Bonds (by 10%) » Stocks (by 15%) Cash 40% » Cash (by 5%) 15% Bonds 45% » Pacific ex. Japan » U.K. » U.S. » Japan U.S. Allocation: Stocks 40% Cash 20% » Cash (by 10%) » Stocks (by 15%) » Bonds (by 5%) Bonds 40% Styles: » Growth » Value Sectors: » Energy » Consumer Discretionary » Basic Resources » Financials » Consumer Staples » Utilities Commodities: » Correction within secular uptrend Bonds: » 105% of benchmark duration Neutral Positions: » Large-caps vs. Small-caps » Yield curve 2 Ned Davis Research Group Please see important disclosures at the end of this document. We've -

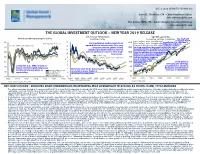

The Global Investment Outlook – New Year 2019 Release U.S

DEC 4 2018 (UPDATED TO NOV 30) Daniel E. Chornous, CFA Chief Investment Officer [email protected] Eric Savoie, MBA, CFA Senior Analyst, Investment Strategy [email protected] THE GLOBAL INVESTMENT OUTLOOK – NEW YEAR 2019 RELEASE U.S. 10-year T-Bond yield S&P 500 equilibrium Global purchasing managers' indices Equilibrium range Normalized earnings & valuations The S&P 500 Nov. '18 Range: 2141 - 3563 (Mid: 2852) is slightly below 65 16 5120 equilibrium (i.e. the band’s ISM Peak Aug 2018: 61.3 Our equilibrium model suggests an Nov. '19 Range: 2218 - 3691 (Mid: 2954)midpoint), and many Previous ISM Peak Feb 2011: 59.2 14 upward bias to interest rates for a very Current (30-November-18): 2760 other markets continue 60 long time into the future should 2560 to show significant discounts to their fair value. A significant rise in inflation and interest rates 12 inflation premiums and real rates of will eventually reduce the sustainable 55 interest ultimately return to their long- 1280 level for valuations, but normalizing 10 term norms. P/E’s and corporate profitability to Last Plot: 2.99% reflect current levels for these 50 8 Current Range: 2.12% - 3.90% (Mid: 3.01%) 640 critical variables suggests % stock market valuations are reasonable, but 45 6 320 certainly not Solid gains in “cheap” in all revenues and earnings 4 Led by the U.S., PMIs remain at 160 locations. propelled U.S. stocks in 40 particular, but threats to levels consistent with expansion, 2 But in the near-term, the pressure but the trend everywhere is both are accumulating. -

Timeframeset

QuantShare Programming Language Table of contents 1. QuantShare Language 1.1 Application Info 1.1.1 NbGroups 1.1.2 NbIndexes 1.1.3 NbIndustries 1.1.4 NbInGroup 1.1.5 NbInIndex 1.1.6 NbInIndustry 1.1.7 NbInMarket 1.1.8 NbInSector 1.1.9 NbMarkets 1.1.10 NbSectors 1.2 Candlestick Pattern 1.2.1 Cdl2crows (0) 1.2.2 Cdl2crows (1) 1.2.3 Cdl3blackcrows (0) 1.2.4 Cdl3blackcrows (1) 1.2.5 Cdl3inside (0) 1.2.6 Cdl3inside (1) 1.2.7 Cdl3linestrike (0) 1.2.8 Cdl3linestrike (1) 1.2.9 Cdl3outside (0) 1.2.10 Cdl3outside (1) 1.2.11 Cdl3staRsinsouth (0) 1.2.12 Cdl3staRsinsouth (1) 1.2.13 Cdl3whitesoldiers (0) 1.2.14 Cdl3whitesoldiers (1) 1.2.15 CdlAbandonedbaby (0) 1.2.16 CdlAbandonedbaby (1) 1.2.17 CdlAdvanceblock (0) 1.2.18 CdlAdvanceblock (1) 1.2.19 CdlBelthold (0) 1.2.20 CdlBelthold (1) 1.2.21 CdlBreakaway (0) 1.2.22 CdlBreakaway (1) 1.2.23 CdlClosingmarubozu (0) 1.2.24 CdlClosingmarubozu (1) 1.2.25 CdlConcealbabyswall (0) 1.2.26 CdlConcealbabyswall (1) 1.2.27 CdlCounterattack (0) 1.2.28 CdlCounterattack (1) 1.2.29 CdlDarkcloudcover (0) 1.2.30 CdlDarkcloudcover (1) 1.2.31 CdlDoji (0) 1.2.32 CdlDoji (1) 1.2.33 CdlDojistar (0) 1.2.34 CdlDojistar (1) 1.2.35 CdlDragonflydoji (0) 1.2.36 CdlDragonflydoji (1) 1.2.37 CdlEngulfing (0) 1.2.38 CdlEngulfing (1) 1.2.39 CdlEveningdojistar (0) 1.2.40 CdlEveningdojistar (1) 1.2.41 CdlEveningstar (0) 1.2.42 CdlEveningstar (1) 1.2.43 CdlGapsidesidewhite (0) 1.2.44 CdlGapsidesidewhite (1) 1.2.45 CdlGravestonedoji (0) 1.2.46 CdlGravestonedoji (1) 1.2.47 CdlHammer (0) 1.2.48 CdlHammer (1) 1.2.49 CdlHangingman (0) 1.2.50