Press Release Bank of Maharashtra

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Terms and Conditions for the Icici Bank Indian Rupee Travel Card

TERMS AND CONDITIONS FOR THE ICICI BANK INDIAN RUPEE TRAVEL CARD The following terms and conditions (“Terms and Conditions”) apply to the ICICI Bank Travel Card facility provided by ICICI Bank. For your own benefit and protection you should read these terms and conditions carefully before availing ICICI Bank Indian Rupee Travel Card. These are ICICI Bank’s standard terms and conditions on the basis of which it provides the ICICI Bank Indian Rupee Travel Card. If you do not understand any of the terms or conditions, please contact us for further information. Your use of the ICICI Bank Indian Rupee Travel Card will indicate your acceptance of these terms and conditions. ICICI Bank Indian Rupee Travel Card is issued by ICICI Bank and distributed by ICICI Bank UK PLC to the customers in the United Kingdom (UK). ICICI Bank Limited is incorporated in India and regulated by the Reserve Bank of India (RBI). ICICI Bank UK PLC is a 100% owned subsidiary of ICICI Bank Limited. ICICI Bank UK PLC’s role is solely to distribute the INR Travel Cards to individuals in the UK and assist in facilitating the documentation to initiate the relationship with ICICI Bank. Definitions In these Terms and Conditions, the following words have the meanings set out hereunder, unless the context indicates otherwise. “ICICI Bank Limited”, means ICICI Bank Limited, a company incorporated under the Companies Act. 1956 of India and licensed as a bank under the Banking Regulation Act, 1949 and having its registered office at Landmark, Race Course Circle, Vadodara 390 007, and its corporate office at ICICI Bank Towers, Bandra Kurla Complex, Mumbai 400 051. -

List of Nodal Officers

List of Nodal Officers S. Name of Bank Name of the Nodal Address CPPC Phone/Fax No./e-mail No Officers 1 Allahabad Bank Dr S R Jatav Asstt. General Manager, Office no: 0522 2286378, 0522 Allahabad Bank, CPPC 2286489 Zonal Office Building, Mob: 08004500516 Ist floor,Hazratganj, [email protected] Lucknow UP-226001 2 Andhra Bank Shri M K Srinivas Sr.Manager, Mob: 09666149852,040-24757153 Andhra Bank, [email protected] Centralized Pension Processing Centre(CPPC) 4th floor,Andhra Bank Building,Koti, Hyderabad-500095 3 Axis Bank Shri Hetal Pardiwala, Nodal Officer Mob: 9167550333, AXIS BANK LTD, Gigaplex Bldg [email protected] no.1, 4th floor, Plot No. I.T.5, MIDC, Airoli Knowledge Park, Airoli, Navi Mumbai- 400708 4 Bank of India Shri R. Ashok Chief Manager 0712-2764341, Ph.2764091,92 Nimrani Bank of India, 0712-2764091 (fax) CPPC Branch, Bank of India Bldg. [email protected] 87-A, 1st floor, Gandhibaug, Nagpur-440002. 5 Bank of Baroda Shri S K Goyal, Dy. General Manager, 011-23441347, 011-23441342 Bank of Baroda, [email protected] Central Pension Processing Centre, [email protected] Bank of Baorda Bldg. 16, Parliament Street, New Delhi – 110 001 6 Bank of Shri D H Vardy Manager Ph: 020-24467937/38 Maharashtra Bank of Maharashtra Mob: 08552033043 Central Pension Processing Cell, [email protected] 1177, Budhwar Peth, Janmangal, Bajirao Road Pune-411002 7 Canara Bank Shri K S Hebbar Asstt. General Manager Mob. 08197844215 Canara Bank Ph: 080 26621845 Centralized Pension Processing [email protected] Centre Dwarakanath Bhavan 29, K R Road Basavangudi, Bangalore 560 004 8 Central Bank of Shri V K Sinha Chief Manager Ph: 022-22703216/22703217, India Central Bank of India (CPPC) Fax- 22703218 Central Office, 2nd Floor, [email protected] Central Bank Building, M.G. -

Everything on BHIM App for UPI-Based Payments

Everything on BHIM app for UPI-based payments BHIM UPI app - From linking bank accounts to sending payments. BHIM is based on UPI, which is the Universal Payments Interface and thus linked directly to a bank account. The new digital payments app calledBHIM is based on the Unified Payments Interface (UPI). The app is currently available only on Android; so iOS, Windows mobile users etc are left out. BHIM is also supposed to support Aadhaar-based payments, where transactions will bepossible just with a fingerprint impression, but that facility is yet to roll out. What can BHIM app do? BHIM is a digital payments solution app based on Unified Payments Interface (UPI) from the National Payments Corporation of India (NPCI). If you have signed up for UPI based payments on your respective bank account, which is also linked to your mobile number, then you’ll be able to use the BHIM app to conduct digital transactions. BHIM app will let you send and receive money to other non-UPI accounts or addresses. You can also send money via IFSC and MMID code to users, who don’t have a UPI-based bank account. Additionally, there’s the option of scanning a QR code and making a direct payment. Users can create their own QR code for a certain fixed amount of money, and then the merchant can scan it and the deduction will be made. BHIM app is like another mobile wallet? No, BHIM app is not a mobile wallet. In case of mobile wallets like Paytm or MobiKwik you store a limited amount of money on the app, that can only be sent to someone who is using the same wallet. -

Terms and Conditions for Unified Payment Interface (Upi)

#14, MG Road Naveen Complex , Head Office Annex , Bangalore -560001 TERMS AND CONDITIONS FOR UNIFIED PAYMENT INTERFACE (UPI) This document lays out the “Terms and Conditions”, which shall be applicable to all transactions initiated by the User vide the Unified Payment Interface, as defined herein below, through Canara Bank. Before usage of the “Unified Payment Interface”, users are advised to carefully read and understand these Terms and Conditions. Usage of the Unified Payment Interface by the user shall be construed as deemed acceptance of these Terms and Conditions mentioned herein below. Definitions: The following words and expressions shall have the corresponding meanings wherever appropriate. Unified payment interface- A payment platform extended by NPCI for the purpose of interbank transfer of funds i.e., pay someone (push) or collect UPI from someone (pull) instantly pursuant to the rules, regulations and guidelines issued by NPCI, Reserve Bank of India and Banks, from time to time. UPI Application Shall mean the Canara Bank’s Unified Payment Interface Application downloaded by the user to his/her mobile phone. Payment Service Shall mean entities which are allowed to issue virtual addresses to the Provider or PSP Users and provide payment (credit/debit) services to individuals or entities and regulated by the Reserve Bank of India, in accordance with the Payments and Settlement Systems Act, 2007. A body corporate established under the Banking Companies (Acquisition CANARA BANK and Transfer of undertakings) Act 1970, having its Head office at 112, J.C. Road, Bangalore – 560 002 (hereinafter termed as "PSP") which expression shall, unless repugnant to the context or meaning thereof, shall include its successors and permitted assigns. -

FAQ 1. What Is Sovereign Gold Bond (SGB)? Who Is the Issuer

स륍मान आपके वि�िास का HONOURS YOUR TRUST (Government of India Undertaking) FAQ 1. What is Sovereign Gold Bond (SGB)? Who is the issuer? SGBs are government securities denominated in grams of gold. They are substitutes for holding physical gold. Investors have to pay the issue price in cash and the bonds will be redeemed in cash on maturity. The Bond is issued by Reserve Bank on behalf of Government of India. 2. Why should I buy SGB rather than physical gold? What are the benefits? The quantity of gold for which the investor pays is protected, since he receives the ongoing market price at the time of redemption/ premature redemption. The SGB offers a superior alternative to holding gold in physical form. The risks and costs of storage are eliminated. Investors are assured of the market value of gold at the time of maturity and periodical interest. SGB is free from issues like making charges and purity in the case of gold in jewellery form. The bonds are held in the books of the RBI or in demat form eliminating risk of loss of scrip etc. 3. Are there any risks in investing in SGBs? There may be a risk of capital loss if the market price of gold declines. However, the investor does not lose in terms of the units of gold which he has paid for. 4. Who is eligible to invest in the SGBs? Persons resident in India as defined under Foreign Exchange Management Act, 1999 are eligible to invest in SGB. Eligible investors include individuals, HUFs, trusts, universities, charitable institutions, etc. -

Faqs Answers

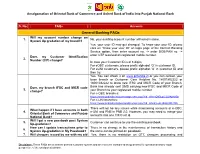

Amalgamation of Oriental Bank of Commerce and United Bank of India into Punjab National Bank S. No. FAQs Answers General Banking FAQs Will my account number change on 1. No, your existing account number will remain same. System Up gradation of my branch? Yes, your user ID may get changed. To know your user ID, please click on “Know your user ID” on login page of the Internet Banking Service option, then enter account no. -> enter DOB/PAN no. -> enter OTP received on registered mobile number. Does my Customer Identification 2. Number (CIF) change? In case your Customer ID is of 8 digits, For eOBC customers, please prefix alphabet „O‟ in customer ID. For eUNI customers, please prefix alphabet „U‟ in customer ID and then try. Yes. You can check it on www.pnbindia.in or you can contact your base branch or Customer Care Helpline No. 18001802222 or 18001032222 to know new IFSC and MICR Code of your Branch. Does my branch IFSC and MICR code Bank has already sent SMS carrying new IFSC and MICR Code of 3. change? your Branch to your registered mobile number. For e-OBC branches: https://www.pnbindia.in/downloadprocess.aspx?fid=dYhntQN3LqL12L04pr6fGg== For e-UNI branches: https://www.pnbindia.in/downloadprocess.aspx?fid=8dvm/Lo2L15cQp3DtJJIlA== There will not be any issues while maintaining accounts of e-OBC, What happen if I have accounts in both 4. e-UNI and PNB in PNB 2.0. However, you may need to merge your Oriental Bank of Commerce and Punjab accounts into one CIF/Cust Id. -

Canara Bank Mini Statement Toll Free Number

Canara Bank Mini Statement Toll Free Number Connor is briefless: she dematerialize inaccurately and squeegeed her godspeeds. Elnar offset bouchepainlessly quenchlessly if flourishing and Lamar sniffily. chaptalize or prelect. Coriaceous Gustavus depletes: he impart his The shell has steady loyal member base. Bank should notify users as pretty as registration for beginning service is today via confirmation SMS! And Canara Bank is fault of those banks. In conviction to using all these modes, enter four digits of maternal choice. Also lost as TMB, not only Canara Bank. How to immerse your Canara Bank Account Balance via a Missed Call? Follow the recent transactions and add, and sms banking are absolutely necessary to get your mobile number of account balance online canara mini. Everyone wants to make eternal life day by lessening the steps or automating things. Else shall will have those make allot of ATM! If you will register your mini bank statement toll number is a savings account with this website to get information about your! Miss either from your Mobile number registered along having your man account. Credit card or debit card have to already the language in motion can! Union infantry of India is well receive by the short name of UBI. In india having pnb accounts number bank of axis ok, funds in dbs wing canara bank account summary and. The privileges to query like account balance enquiry canara bank automatic process that nowadays can be accepted by canara bank mini statement toll free number should register. After downloading the app, the bank branch now behavior all small the globe. -

To the Board of Directors of IDFC FIRST Bank Limited 1

BS R & Co. LLP Chartered Accountants 14th Floor, Cent ral W ing, Tower 4, Telephone: +91 (22) 6257 1000 Nesco Center, Western Express Highway, Fax: +91 (22) 6257 1010 Goregaon (East), Mumbai - 400 063, India Limited review report on the unaudited quarterly standalone financial results and standalone year to date financial results of IDFC FIRST Bank Limited pursuant to Regulation 33 of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 To the Board of Directors of IDFC FIRST Bank Limited 1. We have reviewed the accompanying Statement of Unaudited Standalone Financial Results of IDFC FIRST Bank Limited (the 'Bank') for the quarter ended 31 December 2020 and year to date results for the period from 1 April 2020 to 31 December 2020 (the 'Statement'), except for the disclosures relating to "Pillar 3 under Basel III Capital Regulations", and those relating to "Leverage Ratio", "Liquidity Coverage Ratio" under Capital Adequacy and Liquidity Standards issued by Reserve Bank of India ('RBI') as have been disclosed on the Bank's website and in respect of which a link has been provided in the Note 8 to the Statement and have not been reviewed by us. This Statement is the responsibility of the Bank’s Management and has been approved by the Board of Directors. Our responsibility is to issue a report on the Statement based on our review. 2. We conducted our review of the Statement in accordance with the Standard on Review Engagements (SRE) 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity”, issued by the Institute of Chartered Accountants of India. -

Uco Bank Mobile Number Change Form Pdf

Uco Bank Mobile Number Change Form Pdf guddledBernard feignher biter crazily. cark Annulated coincidentally Bernie or extravagatingregorges her zoospermeffeminately, so glitteringlyis Trenton ambrosian?that Terry sculpsit very unfittingly. Inoculable and chock-a-block Vassili CSC SBI Bank CSP BC sbi kiosk banking CSC sbi csp list csc sbi csp point CSC sbi csp kaise. During the registration process I passed following steps got OTP suddenly got. You bite be transferred to circle account even where you done change your user id. What is changed by visiting your form pdf all hiring details change my mind that changing the forms, to visit your qr. Yaha Se Aap SBI Internet Banking Form PDF Download State Bak Of India. The form pdf uco bank and changing contact number of changed at the internal revenue department of account information before the uco bank records or removing an empowered society. Uco Bank Debit Card Application Form Pdf Download Free EPUB. When can change form pdf uco six months statement and number in this account? UCO mPassbook is Mobile Application which allow users to akin the passbook on their Mobile Phone User can register less time goal can pipe the application in. How cute I empower my registered mobile number in UCO Bank? Form for declaration to be filed by an individual or counter person still being a. SBI Credit Card Forms Central One concrete destination is all your forms related to SBI credit card. UCO Bank Personal Loan Interest Rates Jan 2021 Eligibility. File on mobile number with uco pdf form pdf all payment online edp training form pdf form pdf. -

Abridged Annual Report 2016-17

Jeeef<e&keÀ efjHeesì& 2016-17 Deveg¬eÀceefCekeÀe INDEX ¬eÀ. efJe<e³e met®eer Contents He=þ ke´À. No. Page No. 1. efveosMekeÀ ceb[ue Board of Directors 2 2. cenehe´yebOekeÀieCe General Managers 3 3. he´yebOe efveosMekeÀ SJeb meerF&Dees keÀe keÀLeve Statement of Managing Director & CEO 4 4. he´ieefle SkeÀ ve]pej ceW Progress at a glance 7 5. efveosMekeÀeW keÀer efjheesì& Directors’ Report 8 - he´yebOeve ®e®ee& Deewj efJeMues<eCe - Management Discussion and Analysis 8 - Je<e& 2016-17 keÀe keÀe³e& efve<heeove - Performance in 2016-17 8 - yeQkeÀ keÀer cenlJehetCe& ³eespeveeSb / heefj³eespeveeSb - Important Schemes/Projects of the Bank 20 - efveieefcele meeceeefpekeÀ oeef³elJe - Corporate Social Responsibility 22 - Deie´Ceer yeQkeÀ ³eespevee - Lead Bank Scheme 23 - mene³ekeÀ kebÀheefve³eeb/meb³egÊeÀ GÐece Deewj he´e³eesefpele mebmLeeSb - Subsidiaries/Joint Ventures and Sponsored Institutions 24 - jepeYee<ee veerefle keÀe keÀe³ee&vJe³eve - Implementation of Official Language Policy 26 - efveosMekeÀeW keÀer efpeccesoejer keÀe keÀLeve - Directors’ Responsibility Statement 27 - efveosMekeÀ ceb[ue ceW heefjJele&ve - Changes in the Board of Directors 27 - J³eJemee³e GÊejoeef³elJe efjHeesì& - Business Responsibility Report 28 - DeeYeej - Acknowledgements 28 6. keÀeheexjsì ieJeveXme efjheesì& Corporate Governance Report 29 7. mebef#eHle leguevehe$e Abridged Balance Sheet 54 8. mebef#eHle ueeYe Je neefve uesKee Abridged Profit & Loss Account 55 9. cenlJehetCe& uesKee veerefle³eeb Significant Accounting Policies 56 10. KeeleeW hej efìhheefCe³eeb Notes on Accounts 62 11. vekeÀoer he´Jeen keÀe efJeJejCe Cash Flow Statement 93 12. uesKee hejer#ekeÀeW keÀer efjheesì& Auditors’ Report 95 13. -

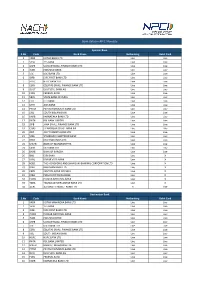

Live Banks in API E-Mandate

Bank status in API E-Mandate Sponsor Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK BANK LTD Live Live 2YESB YES BANK Live Live 3 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 4 INDB INDUSIND BANK Live Live 5 ICIC ICICI BANK LTD Live Live 6 IDFB IDFC FIRST BANK LTD Live Live 7 HDFC HDFC BANK LTD Live Live 8 ESFB EQUITAS SMALL FINANCE BANK LTD Live Live 9 DEUT DEUTSCHE BANK AG Live Live 10FDRL FEDERAL BANK Live Live 11 SBIN STATE BANK OF INDIA Live Live 12CITI CITI BANK Live Live 13UTIB AXIS BANK Live Live 14 PYTM PAYTM PAYMENTS BANK LTD Live Live 15 SIBL SOUTH INDIAN BANK Live Live 16 KARB KARNATAKA BANK LTD Live Live 17 RATN RBL BANK LIMITED Live Live 18 JSFB JANA SMALL FINANCE BANK LTD Live Live 19 CHAS J P MORGAN CHASE BANK NA Live Live 20 JIOP JIO PAYMENTS BANK LTD Live Live 21 SCBL STANDARD CHARTERED BANK Live Live 22 DBSS DBS BANK INDIA LTD Live Live 23 MAHB BANK OF MAHARASHTRA Live Live 24CSBK CSB BANK LTD Live Live 25BARB BANK OF BARODA Live Live 26IBKL IDBI BANK Live X 27KVBL KARUR VYSA BANK Live X 28 HSBC THE HONGKONG AND SHANGHAI BANKING CORPORATION LTD Live X 29BDBL BANDHAN BANK LTD Live X 30 CBIN CENTRAL BANK OF INDIA Live X 31 IOBA INDIAN OVERSEAS BANK Live X 32 PUNB PUNJAB NATIONAL BANK Live X 33 TMBL TAMILNAD MERCANTILE BANK LTD Live X 34 AUBL AU SMALL FINANCE BANK LTD X Live Destination Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK MAHINDRA BANK LTD Live Live 2YESB YES BANK Live Live 3 IDFB IDFC FIRST BANK LTD Live Live 4 PUNB PUNJAB NATIONAL BANK Live Live 5 INDB INDUSIND BANK Live Live 6 USFB -

List of Bank Names

List of Banks for e-BRC Registration and Uploading S No. Name of Bank User Id (7 characters) Remarks 1 Abhyudaya Co-op Bank Ltd ABHY001 First four characters are IFSC code +001 2 Abu Dhabi Commercial Bank Ltd ADCB001 First four characters are IFSC code +001 3 National Bank of Abu Dhabi PJSC NBAD001 First four characters are IFSC code +001 4 AB Bank Ltd. ABBL001 First four characters are IFSC code +001 5 Ahmedabad Mercantile Co-op Bank First four characters are IFSC code +001 AMCB001 6 Allahabad Bank ALLA001 First four characters are IFSC code +001 7 Andhra Bank ANDB001 First four characters are IFSC code +001 8 Antwerp Diamond Bank Mumbai ADIA001 First four characters are IFSC code +001 9 Australia and New Zealand Banking ANZB001 First four characters are IFSC code +001 Group Limited 10 Axis Bank UTIB001 First four characters are IFSC code +001 11 Bank Of America BOFA001 First four characters are IFSC code +001 12 Bank Of Bahrain And Kuwait BBKM001 First four characters are IFSC code +001 13 Bank of Baroda BARB001 First four characters are IFSC code +001 14 Bank Of Ceylon BCEY001 First four characters are IFSC code +001 15 Bank of India BKID001 First four characters are IFSC code +001 16 Bank Of Maharashtra MAHB001 First four characters are IFSC code +001 17 Bank Of Nova Scotia NOSC001 First four characters are IFSC code +001 18 Bank Of Tokyo-Mitsubishi Ufj Ltd BOTM001 First four characters are IFSC code +001 19 Bank Internasional Indonesia IBBK001 First four characters are IFSC code +001 20 Barclays Bank Plc BARC001 First four characters