Jpiseptember2015.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Title: Further Discussion on the Motion to Consider Statutory Resolution Regarding Disapproval of Coal Mines (Special Provisions) Second Ordinance, 2014 (No

an> Title: Further discussion on the motion to consider Statutory Resolution regarding disapproval of Coal Mines (Special Provisions) Second Ordinance, 2014 (No. 7 of 2014) and the Coal Mines (Special Provisions) Bill, 2015 (Statutory Resolution withdrawn and Government Bill-Passed). HON. SPEAKER: Now, the House will take up item Nos. 13 and 14 together. Shri Kalyan Banerjee has to start the discussion on this. ...(Interruptions) SHRI ADHIR RANJAN CHOWDHURY (BAHARAMPUR): Madam, I have given a notice. ...(Interruptions) माननीय अय : कल छु ी दी ह,ै इसिलए आज यादा काम करना ह,ै आप सब लोग को जाना भी है SHRI ADHIR RANJAN CHOWDHURY: I have given a notice for 'Zero Hour'. ...(Interruptions) माननीय अय : जीरो ऑवर शाम को करग,े जो रहग,े व े बोलग,े अभी नह ...(Interruptions) SHRI KALYAN BANERJEE (SREERAMPUR): Madam, I express my heartiest thanks for giving me this opportunity. ...(Interruptions) HON. SPEAKER: Please sit down. Now we are taking up the Coal Mines Bill. ...(Interruptions) SHRI KALYAN BANERJEE: When this Ordinance was introduced in this House, I made my elaborate speech. I do not want to repeat the contents of that speech. I just want to tell something to the hon. Minister. Yesterday, I was hearing his speech regarding the auction and the scrapping of the coal blocks, and the auction because of the order of the hon. Supreme Court. I want to say through you that this is not the first time the Supreme Court has said this. I just want to draw the attention of the hon. -

India's Democracy at 70: Toward a Hindu State?

India’s Democracy at 70: Toward a Hindu State? Christophe Jaffrelot Journal of Democracy, Volume 28, Number 3, July 2017, pp. 52-63 (Article) Published by Johns Hopkins University Press DOI: https://doi.org/10.1353/jod.2017.0044 For additional information about this article https://muse.jhu.edu/article/664166 [ Access provided at 11 Dec 2020 03:02 GMT from Cline Library at Northern Arizona University ] Jaffrelot.NEW saved by RB from author’s email dated 3/30/17; 5,890 words, includ- ing notes. No figures; TXT created from NEW by PJC, 4/14/17 (4,446 words); MP ed- its to TXT by PJC, 4/19/17 (4,631 words). AAS saved by BK on 4/25/17; FIN created from AAS by PJC, 5/26/17 (5,018 words). FIN saved by BK on 5/2/17 (5,027 words); PJC edits as per author’s updates saved as FINtc, 6/8/17, PJC (5,308 words). PGS created by BK on 6/9/17. India’s Democracy at 70 TOWARD A HINDU STATE? Christophe Jaffrelot Christophe Jaffrelot is senior research fellow at the Centre d’études et de recherches internationales (CERI) at Sciences Po in Paris, and director of research at the Centre national de la recherche scientifique (CNRS). His books include Religion, Caste, and Politics in India (2011). In 1976, India’s Constitution of 1950 was amended to enshrine secular- ism. Several portions of the original constitutional text already reflected this principle. Article 15 bans discrimination on religious grounds, while Article 25 recognizes freedom of conscience as well as “the right freely to profess, practise and propagate religion.” Collective as well as indi- vidual rights receive constitutional recognition. -

Amit Shah at Parivartan Yatra Rally in Mysore

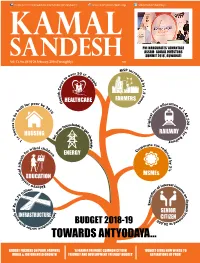

https://www.facebook.com/Kamal.Sandesh/ www.kamalsandesh.org @kamalsandeshbjp PM INAUGURAtes ‘ADVANTAGE ASSAM- GLOBAL INVESTORS SUMMit 2018’, GUWAHATI Vol. 13, No. 04 16-28 February, 2018 (Fortnightly) `20 HEALTHCARE FARMERS HOUSING RAILWAY ENERGY MSMEs EDUCATION SENIOR INFRASTRUCTURE BUDGET 2018-19 CITIZEN TOWARDS ANTYODAYA... BUDGET FOCUSES ON POOR, FARMERS ‘A FARMER FRIENDLY, COMMON CITIZEN ‘BUDGET GIVES NEW WINGS TO RURAL & JOB ORIENTED GROWTH FRIENDLY AND DEVELOPMENT FRIENDLY BUDGEt’ 16-28 FEBRUARY,ASP IRATIONS2018 I KAMAL OF P SANDESHoor’ I 1 Karnataka BJP welcomes BJP National President Shri Amit Shah at Parivartan Yatra Rally in Mysore. BJP National President Shri Amit Shah hoisting the tri-colour on the 69th Republic Day celebration at BJP HQ, New Delhi. BJP National President Shri Amit Shah paying floral tributes Shri Amit Shah addressing the SARBANSDANI to to Sant Ravidas ji on his Jayanti at BJP H.Q. in New Delhi commemorate the 350th birth anniversary of Guru Gobind 2 I KAMAL SANDESH I 16-28 FEBRUARY, 2018 Singh ji at Chandani Chowk, New Delhi. Fortnightly Magazine Editor Prabhat Jha Executive Editor Dr. Shiv Shakti Bakshi Associate Editors Ram Prasad Tripathy Vikash Anand Creative Editors Vikas Saini Mukesh Kumar Phone +91(11) 23381428 FAX +91(11) 23387887 BUDGET FOCUSES ON POOR, FARMERS RURAL & JOB E-mail ORIENTED GROWTH [email protected] Finance Minister Shri Arun Jaitley presented on February 1, 2018 general [email protected] 06 Budget 2018-19 in Parliament. It was second time the budget was Website: www.kamalsandesh.org presented on first of February instead following colonial era practices of... VAICHARIKI 17 C M SIDDARAMAIAH SYNONYMOUS WITH Aspects of Economics 21 CORRUPTION: AMIT SHAH BJP National President Shri SHRADHANJALI Amit Shah said Karnataka CM Siddaramaiah was synonymous Chintaman Vanga / Hukum Singh 23 with corruption and added 15 CONGRESS GOVERNMENT that the state government was ARTICLE IN KARNATAKA IS ON EXIT protecting the killers of Hindu.. -

Ministry of Defence

21 STANDING COMMITTEE ON DEFENCE (2015-2016) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2016-17) MINISTRY OF DEFENCE (MISCELLANEOUS) (DEMAND NO. 20) TWENTY-FIRST REPORT LOK SABHA SECRETARIAT NEW DELHI May, 2016/ Vaisakha, 1938 (Saka) 1 TWENTY-FIRST REPORT STANDING COMMITTEE ON DEFENCE (2015-2016) (SIXTEENTH LOK SABHA) MINISTRY OF DEFENCE DEMANDS FOR GRANTS (2016-2017) (MISCELLANEOUS) (DEMAND NO. 20) Presented to Lok Sabha on 03.05.2016 Laid in Rajya Sabha on 03.05.2016 LOK SABHA SECRETARIAT NEW DELHI May, 2016/ Vaisakha, 1938 (Saka) 2 CONTENTS Composition of the Committee (2015-16)………………………………………. Introduction ………………….……………………………………………………… PART - I Chapter I Ordnance Factory Board……………………...……………….….. Chapter II Defence Research and Development Organization …………… Chapter III Ex- Servicemen Contributory Health Scheme …………………. Chapter IV Directorate General Quality Assurance ……. …………………. Chapter V National Cadet Corps …………………………..…………………. PART – II OBSERVATIONS/RECOMMENDATIONS........................................... ANNEXURE ………………………………………………………….……... APPENDICES Minutes of the sitting of the Committee on Defence held on 4.4.2016, 5.4.2016, 6.04.2016 and 29.04.2016…………………………………………………………… 3 COMPOSITION OF THE STANDING COMMITTEE ON DEFENCE (2015-16) Maj Gen B C Khanduri, AVSM (Retd) - Chairperson Members Lok Sabha 2. Shri Suresh C. Angadi 3. Shri Shrirang Appa Barne 4. Shri Dharambir 5. Shri Thupstan Chhewang 6. Col Sonaram Choudhary(Retd) 7. Shri H.D. Devegowda 8. Shri Sher Singh Ghubaya 9. Shri G. Hari 10. Shri Ramesh Jigajinagi 11. Dr. Murli Manohar Joshi 12. Km. Shobha Karandlaje 13. Shri Vinod Khanna 14. Dr. Mriganka Mahato 15. Shri Tapas Paul 16. Shri Ch. Malla Reddy 17. Shri Rajeev Satav 18. Smt. Mala Rajya Lakshmi Shah 19. Capt Amarinder Singh(Retd) 20. -

C:\Users\ACCER\Desktop\JULY QUESTION LIST\Final Make\Final

LOK SABHA ______ List of Questions for ORAL ANSWERS Monday, July 19, 2021/Ashadha 28, 1943 (Saka) ______ (Ministries of Corporate Affairs; Culture; Education; Finance; Labour and Employment; Petroleum and Natural Gas; Skill Development and Entrepreneurship; Steel; Tourism; Tribal Affairs) (ÛúÖò¯ÖÖì¸êü™ü ÛúÖµÖÔ; ÃÖÓÃÛúéןÖ; ׿ÖõÖÖ; ×¾Ö¢Ö; ÁÖ´Ö †Öî¸ü ¸üÖê•ÖÝÖÖ¸ü; ¯Öê™ÒüÖê×»ÖµÖ´Ö †Öî¸ü ¯ÖÏÖÛéúןÖÛú ÝÖîÃÖ; ÛúÖî¿Ö»Ö ×¾ÖÛúÖÃÖ †Öî¸ü ˆª×´ÖŸÖÖ; ‡Ã¯ÖÖŸÖ; ¯ÖµÖÔ™ü®Ö; •Ö®Ö•ÖÖŸÖßµÖ ÛúÖµÖÔ ´ÖÓ¡ÖÖ»ÖµÖ ) ______ Total Number of Questions — 20 Impact of Covid-19 Pandemic on Indian Tourism Scheme (ECLGS) to Rs.4.5 lakh crore from Rs.3 lakh crore Industry and if so, the details thereof; †*1. SHRI RAMESH CHANDER KAUSHIK: (d) whether the Government has planned to give SHRI RAJU BISTA: loan guarantees to tourism sector under ECLGS and free Will the Minister of TOURISM visa for first 5 lakh tourists once borders re-open and if so, the details thereof; and ¯ÖµÖÔ™ü®Ö ´ÖÓ¡Öß (e) the other important steps being taken by the be pleased to state: Government during the Covid-19 pandemic in this regard? (a) whether the Government has constituted any working group to assess the impact of Covid-19 pandemic Increasing Prices of Petroleum Products on tourism industry and if so, the details thereof along with the quantum of loss in terms of job losses and *3. SHRI N.K. PREMACHANDRAN: foreign exchange loss, State/UT-wise; SHRI K. MURALEEDHARAN: (b) the number of foreign tourists visited the country Will the Minister of PETROLEUM AND NATURAL during first and second waves of -

Pages I-II.Pmd

The Journal of Parliamentary Information VOLUME LXIII NO. 2 JUNE 2017 LOK SABHA SECRETARIAT NEW DELHI CBS Publishers & Distributors Pvt. Ltd. 24, Ansari Road, Darya Ganj, New Delhi-2 EDITORIAL BOARD Editor : Anoop Mishra Secretary-General Lok Sabha Associate Editors : Dr. D. Bhalla Secretary Lok Sabha Secretariat Atul Kaushik Additional Secretary Lok Sabha Secretariat Abhijit Kumar Joint Secretary Lok Sabha Secretariat Dr. R. N. Das Director Lok Sabha Secretariat Assistant Editors : Babu Lal Naik Additional Director Lok Sabha Secretariat H. Soikholian Simte Joint Director Lok Sabha Secretariat © Lok Sabha Secretariat, New Delhi Contents iii THE JOURNAL OF PARLIAMENTARY INFORMATION VOLUME LXIII NO. 2 JUNE 2017 CONTENTS PAGE EDITORIAL NOTE 95 ADDRESSES Address by the President to Parliament 97 Address by the Speaker of Lok Sabha, Smt. Sumitra Mahajan at the South Asian Speakers’ Summit, Indore, Madhya Pradesh 111 DECLARATION OF SOUTH ASIAN SPEAKERS’ SUMMIT ON ‘ACHIEVING THE SUSTAINABLE DEVELOPMENT GOALS’ 117 ARTICLE South Asian Speakers’ Summit on ‘Achieving the Sustainable Development Goals’, Indore, 18-20 February 2017 - By Shri Anoop Mishra 119 PARLIAMENTARY EVENTS AND ACTIVITIES Conferences and Symposia 130 Birth Anniversaries of National Leaders 132 Exchange of Parliamentary Delegations 134 Parliament Museum 134 Bureau of Parliamentary Studies and Training 134 PROCEDURAL MATTERS 139 PARLIAMENTARY AND CONSTITUTIONAL DEVELOPMENTS 141 SESSIONAL REVIEW Lok Sabha 146 Rajya Sabha 172 State Legislatures 201 iv The Journal of Parliamentary Information RECENT LITERATURE OF PARLIAMENTARY INTEREST 206 APPENDICES I. Statement showing the work transacted during the Eleventh Session of the Sixteenth Lok Sabha 212 II. Statement showing the work transacted during the 242nd Session of the Rajya Sabha 216 III. -

Lok Sabha ___ Synopsis of Debates

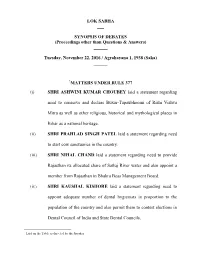

LOK SABHA ___ SYNOPSIS OF DEBATES (Proceedings other than Questions & Answers) ______ Tuesday, November 22, 2016 / Agrahayana 1, 1938 (Saka) ______ *MATTERS UNDER RULE 377 (i) SHRI ASHWINI KUMAR CHOUBEY laid a statement regarding need to conserve and declare Buxar-Tapaubhoomi of Rishi Vishva Mitra as well as other religious, historical and mythological places in Bihar as a national heritage. (ii) SHRI PRAHLAD SINGH PATEL laid a statement regarding need to start cow sanctuaries in the country. (iii) SHRI NIHAL CHAND laid a statement regarding need to provide Rajasthan its allocated share of Satluj River water and also appoint a member from Rajasthan in Bhakra Beas Management Board. (iv) SHRI KAUSHAL KISHORE laid a statement regarding need to appoint adequate number of dental hygienists in proportion to the population of the country and also permit them to contest elections in Dental Council of India and State Dental Councils. * Laid on the Table as directed by the Speaker. (v) SHRIMATI JAYSHREEBEN PATEL laid a statement regarding need to construct Railway over Bridges in Mehsana City, Gujarat. (vi) SHRI SUBHASH CHANDRA BAHERIA laid a statement regarding need to construct roads under Pradhan Mantri Gram Sadak Yojana in all the villages of Bhilwara parliamentary constituency, Rajasthan. (vii) SHRIMATI DARSHANA VIKRAM JARDOSH laid a statement regarding need to conduct certificate course in manufacturing in Industrial Training Institutes in the country. (viii) SHRI SUSHIL KUMAR SINGH laid a statement regarding need to undertake renovation of historic Surya Temple and other temples in Aurangabad parliamentary constituency, Bihar. (ix) SHRI RAGHAV LAKHANPAL laid a statement regarding need to address the problems faced by retired bank employees. -

Press Release This Is to Intimate That the Post Office Passport Seva

Press Release This is to intimate that the Post Office Passport Seva Kender at Head Post Office, Near Sher Shah Wali Chowk, Ferozepur Cantt was scheduled to be inaugurated on 9th Jan 2019 at 11.00 AM by Sh. Sher Singh Ghubaya Hon’ble Member Parliament Firozpur. Due to a call of strike by the Postal Employees Union on 8th and 9th Jan 2019, the scheduled inauguration on 9th Jan 2019 is postponed. The POPSK Ferozepur will now be inaugurated on 11th Jan 2019 at 11.00 AM by Sh. Sher Singh Ghubaya, Hon’ble Member Parliament Firozpur. The applicants who have already booked their appointments for 9th Jan 2019 are advised to reschedule their appointment at the website www.passportindia.gov.in using the same login id and password, without paying any additional fee. Munish Kapoor Regional Passport Officer Amritsar Press Release This is for the information of General Public that the first Post Office Passport Seva Kender (POPSK) of Regional Passport Office Amritsar is going to be inaugurated at Head Post Office, Near Sher Shah Wali Chowk, Firozpur on 9th Jan 2019 at 11.00 AM. The POPSK will be inaugurated by Sh. Sher Singh Ghubhaya Hon’ble Member Parliament Firozpur. At present, all the applicants falling under Regional Passport Office viz Amritsar, Tarn Taran, Firozpur, Faridkot, Fazilka and Sri Mukatsar Sahib have to submit their passport related applications at Passport Seva Kender Amritsar only. The ministry of External Affairs has liberalized the conditions under which any citizen can apply for passport related services anywhere in India irrespective of his place of residence. -

![Cryf] Cvdfccvted Xrczsz Yrer`](https://docslib.b-cdn.net/cover/4570/cryf-cvdfccvted-xrczsz-yrer-904570.webp)

Cryf] Cvdfccvted Xrczsz Yrer`

+ ! < # % 5 ! % 5 5 )*+!) , -./0 -0"-"1 ,-$./& 0-#/( ('31()'$= '=3;(')'0/)>3 )/'1=0)'1))/('1 !"#!$%&'( )"'*! )"$)* +(*, ,*%"#,*#$, ;?$;//43;1 /')='1310'('1$) -.631)4/;6767@4'(3?3)/ %"*# *," ",*$ ( $ '( AB)) CA D' !) ' # # 1 # 2/1 23-45 -/ 6 Q #$$ # Q R 1)2)(3 orty-eight-year after Indira FGandhi came to power in 1971 on the ear-catching slogan #!%2 of “Garibi hatao”, her grandson " / Rahul Gandhi has reinvented 3 #+ %$! the same theme by announcing ! 67 #! ! his own version of “surgical” ! 3 #! 86"777 strike on poverty to revive the Congress fortune in the Lok %3 "! .# ! . Sabha elections. ! ! %2 As part of the Congress " $! manifesto for general elections, Congress chief Rahul Gandhi said 20 per cent families in through idea. We have con- claimed there is enough money poorest of the poor category sulted many economists on in India and the Congress will be given 72,000 each the scheme. It will be a fiscal- guarantees that 20 per cent ')* ' &+&'" annually as a minimum !" # ly prudent scheme,” Rahul said poorest families will be given " , * - , ** * !" " * income. Accusing the Prime 72,000 per year. Making the announcement Terming it to be a “final each annually,” Rahul said soon Minister of giving money to the “Remember that in unanimous decision, the party According to a senior party at a Press conference post the assault” to eradicate poverty in after starting -

The Journal of Parliamentary Information ______VOLUME LXVI NO.1 MARCH 2020 ______

The Journal of Parliamentary Information ________________________________________________________ VOLUME LXVI NO.1 MARCH 2020 ________________________________________________________ LOK SABHA SECRETARIAT NEW DELHI ___________________________________ The Journal of Parliamentary Information VOLUME LXVI NO.1 MARCH 2020 CONTENTS PARLIAMENTARY EVENTS AND ACTIVITIES PROCEDURAL MATTERS PARLIAMENTARY AND CONSTITUTIONAL DEVELOPMENTS DOCUMENTS OF CONSTITUTIONAL AND PARLIAMENTARY INTEREST SESSIONAL REVIEW Lok Sabha Rajya Sabha State Legislatures RECENT LITERATURE OF PARLIAMENTARY INTEREST APPENDICES I. Statement showing the work transacted during the Second Session of the Seventeenth Lok Sabha II. Statement showing the work transacted during the 250th Session of the Rajya Sabha III. Statement showing the activities of the Legislatures of the States and Union Territories during the period 1 October to 31 December 2019 IV. List of Bills passed by the Houses of Parliament and assented to by the President during the period 1 October to 31 December 2019 V. List of Bills passed by the Legislatures of the States and the Union Territories during the period 1 October to 31 December 2019 VI. Ordinances promulgated by the Union and State Governments during the period 1 October to 31 December 2019 VII. Party Position in the Lok Sabha, Rajya Sabha and the Legislatures of the States and the Union Territories PARLIAMENTARY EVENTS AND ACTIVITES ______________________________________________________________________________ CONFERENCES AND SYMPOSIA 141st Assembly of the Inter-Parliamentary Union (IPU): The 141st Assembly of the IPU was held in Belgrade, Serbia from 13 to 17 October, 2019. An Indian Parliamentary Delegation led by Shri Om Birla, Hon’ble Speaker, Lok Sabha and consisting of Dr. Shashi Tharoor, Member of Parliament, Lok Sabha; Ms. Kanimozhi Karunanidhi, Member of Parliament, Lok Sabha; Smt. -

Ministry of External Affairs Public Accounts Committee (2015-16)

30 GLOBAL ESTATE MANAGEMENT BY THE MINISTRY OF EXTERNAL AFFAIRS MINISTRY OF EXTERNAL AFFAIRS PUBLIC ACCOUNTS COMMITTEE (2015-16) THIRTIETH REPORT SIXTEENTH LOK SABHA LOK SABHA SECRETARIAT NEW DELHI 1 PAC NO. 2062 THIRTIETH REPORT PUBLIC ACCOUNTS COMMITTEE (2015-16) (SIXTEENTH LOK SABHA) GLOBAL ESTATE MANAGEMENT BY THE MINISTRY OF EXTERNAL AFFAIRS MINISTRY OF EXTERNAL AFFAIRS Presented to Lok Sabha on: 21.12.2015 Laid in Rajya Sabha on: 21.12.2015 LOK SABHA SECRETARIAT N E W D E L H I December, 2015 / Agrahayana 1937 (Saka) 2 CONTENTS PAGES COMPOSITION OF THE PUBLIC ACCOUNTS COMMITTEE (2015-16)…… (ii) COMPOSITION OF THE PUBLIC ACCOUNTS COMMITTEE (2014-15)…… (iv) INTRODUCTION……………….. (vi) REPORT PART- I I Introductory 1-5 II Organisational Set-up 6 III Absence of domain information 6-10 IV Absence of action plan 11-12 V Failure/delay in purchase of land/acquisition of property 12-22 VI Inability to acquire land on reciprocal basis 23-25 VII Purchase of building unsuitable for public assembly/representational functions for Indian Cultural Centre (ICC) at Eol, France. 25-28 VIII Delay in commencement of construction 28-37 IX Inefficiencies in renovation/ redevelopment 37-42 X Expenditure beyond delegated financial powers 42-44 XI Retention of vacant accommodation 44-45 XII Property lying unutilised (EoI Berlin, Germany) 45-46 XIII Jawaharlal Nehru Bhawan 46-47 XIV Regional Passport Offices (RPO)/ FSI 47-53 PART - II Observations/Recommendations 54-69 APPENDICES I Minutes of the Thirteenth sitting of the PAC (2014-15) held on 05.01.2015 II Minutes of the Sixth sitting of the PAC (2015-16) held on 19.08.2015 III Minutes of the Sixteenth sitting of the PAC (2015-16) held on 17.12.2015 ANNEXURE Statement indicating the changes/modifications made in Draft Repot ‘Global Estate Management by the Ministry of External Affairs’ 3 COMPOSITION OF THE PUBLIC ACCOUNTS COMMITTEE (2015-16) Prof. -

LOK SABHA ___ BULLETIN-PART II (General Information Relating To

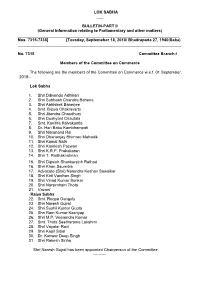

LOK SABHA ___ BULLETIN-PART II (General Information relating to Parliamentary and other matters) ________________________________________________________________________ Nos. 7315-7338] [Tuesday, Septemeber 18, 2018/ Bhadrapada 27, 1940(Saka) _________________________________________________________________________ No. 7315 Committee Branch-I Members of the Committee on Commerce The following are the members of the Committee on Commerce w.e.f. 01 September, 2018:- Lok Sabha 1. Shri Dibyendu Adhikari 2. Shri Subhash Chandra Baheria 3. Shri Abhishek Banerjee 4. Smt. Bijoya Chakravarty 5. Shri Jitendra Chaudhury 6. Shri Dushyant Chautala 7. Smt. Kavitha Kalvakuntla 8. Dr. Hari Babu Kambhampati 9. Shri Nityanand Rai 10. Shri Dhananjay Bhimrao Mahadik 11. Shri Kamal Nath 12. Shri Kamlesh Paswan 13. Shri K.R.P. Prabakaran 14. Shri T. Radhakrishnan 15. Shri Dipsinh Shankarsinh Rathod 16. Shri Khan Saumitra 17. Advocate (Shri) Narendra Keshav Sawaikar 18. Shri Kirti Vardhan Singh 19. Shri Vinod Kumar Sonkar 20. Shri Narsimham Thota 21. Vacant Rajya Sabha 22. Smt. Roopa Ganguly 23. Shri Naresh Gujral 24. Shri Sushil Kumar Gupta 25. Shri Ram Kumar Kashyap 26. Shri M.P. Veerendra Kumar 27. Smt. Thota Seetharama Lakshmi 28. Shri Vayalar Ravi 29. Shri Kapil Sibal 30. Dr. Kanwar Deep Singh 31. Shri Rakesh Sinha Shri Naresh Gujral has been appointed Chairperson of the Committee. ---------- No.7316 Committee Branch-I Members of the Committee on Home Affairs The following are the members of the Committee on Home Affairs w.e.f. 01 September, 2018:- Lok Sabha 1. Dr. Sanjeev Kumar Balyan 2. Shri Prem Singh Chandumajra 3. Shri Adhir Ranjan Chowdhury 4. Dr. (Smt.) Kakoli Ghosh Dastidar 5. Shri Ramen Deka 6.