Corporate Presentation Investor Relations, May 2015 General Information

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Gedeon Richter Annual Report Gedeon Richtergedeon • Annual Report • 2011

GEDEON RICHTER ANNUAL REPORT GEDEON RICHTERGEDEON • ANNUAL REPORT • 2011 1901 2011 00Borito_annual_report_angol_2012_140_old.indd 1 3/25/12 2:29 PM Delivering quality therapy through generations 2011 01_angol_elso_resz_01_66.indd 1 3/26/12 2:23 PM 2 Contents CONTENTS Richter Group – Fact Sheet . 3 Consolidated Financial Highlights . 5 Chairman’s Statement . 7 Directors’ Report . 9 Information for Shareholders . 9 Shareholders’ Highlights . 9 Market Capitalisation . 9 Annual General Meeting . 10 Investor Relations Activities . 10 Dividend . 11 Information Regarding Richter Shares . 12 Shares in Issue . 12 Treasury Shares . 12 Registered Shareholders . 12 Share Ownership by Company Board Members . 13 Risk Management . 14 Corporate Governance . 16 Company’s Boards . 18 Board of Directors . 18 Executive Board . 21 Supervisory Committee . .22 Managing Director’s Review . 25 Operating Review . 29 Consolidated Turnover . 29 Markets – Pharmaceutical Segment . 31 Hungary . 32 International Sales . 34 European Union . 35 CIS . 37 USA . 38 Rest of the World . 38 Wholesale and Retail Activities . 39 Research and Development . 40 Female Healthcare . 42 Products . 46 Manufacturing and Supply . 50 Corporate Social Responsibility . 51 Environmental Policy . 51 Health and Safety at Work . 52 Work Health and Safety Management System . 52 Practical Implementation . 52 Community Involvement . 53 People . 54 Employees . 54 Recruitment and Individual Development . 55 Developing Leaders . 56 Remuneration and Other Employee Programmes . 56 Financial Review . 59 Key Financial Data . 59 Cost of Sales . 59 Gross Profit . 59 Operating Expenses . 60 Profit from Operations . 61 Net Financial Income . 61 Share of Profit of Associates . 62 Income Tax . 62 Profit for the Year . 62 Profit Attributable to Owners of the Parent . 62 Balance Sheet . 63 Cash Flow . -

Corporate Presentation Investor Relations, April 2016 General Information

STADA Corporate Presentation Investor Relations, April 2016 General information By making use of this document the reader acknowledges and agrees to the following: We accept no liability arising from the use of this document. STADA Arzneimittel AG, Bad Vilbel (hereinafter “STADA”), has made every effort to make sure that this document contains correct and up-to- date information. STADA accepts no responsibility for and makes no guarantee whatsoever in respect of currentness, accuracy and completeness of the information and assumes no obligation to update, complete or correct this information. The anticipated opportunities and risks to STADA’s activities have been described in detail in the Executive Board’s management reports in the annual reports. Current possible opportunities and risks are discussed in the respective interim report. STADA’s performance indicators are party influenced by one-time special effects and/or effects not arising from the operating business. Disclosure of key figures adjusted for these effects (so called “pro forma” key figures) by STADA is only to provide a supplement to the recorded IFRS key figures for a transparent comparison to a relevant period from the previous year. All text, pictures, trademarks, and other information contained in this document are subject to the copyright of STADA or subject to rights acquired from third parties. Trademark protection may apply even for preparations not indicated as trade marks. This document may not be reproduced in whole or in part without the express written consent of STADA. Any disputes arising out of or in connection with the content of this document, insofar as they are directed against STADA, shall be subject to German law, without prejudice to mandatory provisions of foreign law. -

Gedeon Richter Annual Report 2014 Table of Contents

Gedeon Richter Annual Report 2014 Table of Contents I. Richter – Corporate Review 4 1. Fact Sheet 5 2. Financial Highlights 6 3. Chairman’s Letter to the Shareholders 9 4. Investor Information 10 a) Share Price and Market Capitalisation 10 b) Annual General Meeting 11 c) Dividend 11 d) Investor Relations Activities 11 e) Analysts Providing Coverage 12 f) Information Regarding Richter Shares 13 5. Corporate Governance 16 6. Company’s Boards 19 7. Risk Management 22 8. Litigation Proceedings 23 II. Managing Director’s Review 24 III. In Transition 28 1. The Pharmaceutical Industry 29 2. Transition from Regional Midpharma to Pan-European Specialty Pharma 29 3. Strategic Focus – Innovation 30 a) Female Healthcare 30 b) Original Research – Focus on CNS 34 c) Biosimilars 35 IV. Business Review 36 1. Pharmaceuticals 37 a) Research and Development 37 b) Manufacturing and Supply 41 c) Products 41 d) Sales by Markets 45 e) Corporate Social Responsibility 55 f) People 57 2. Wholesale and Retail 61 3. Group Figures 61 a) Business Segment Information 62 b) Consolidated Turnover 62 c) Key Financial Data 63 d) Profi t and Loss Items 63 e) Balance Sheet Items 66 f) Cash Flow 67 g) Treasury Policy 67 h) Capital Expenditure 67 V. Appendices 70 Annual Report I Gedeon Richter 2014 I 3 1. Fact Sheet Richter Group is active in two major business segments, primarily Pharmaceuticals comprising the research and development, manufacturing, sales and marketing of pharmaceutical products, and it is also engaged in the Wholesale and Retail of these products. In addition, there is a third group (’Other’) of companies compris- I. -

Corporate Presentation Investor Relations, May 2016 General Information

STADA Corporate Presentation Investor Relations, May 2016 General information By making use of this document the reader acknowledges and agrees to the following: We accept no liability arising from the use of this document. STADA Arzneimittel AG, Bad Vilbel (hereinafter “STADA”), has made every effort to make sure that this document contains correct and up-to- date information. STADA accepts no responsibility for and makes no guarantee whatsoever in respect of currentness, accuracy and completeness of the information and assumes no obligation to update, complete or correct this information. The anticipated opportunities and risks to STADA’s activities have been described in detail in the Executive Board’s management reports in the annual reports. Current possible opportunities and risks are discussed in the respective interim report. STADA’s performance indicators are party influenced by one-time special effects and/or effects not arising from the operating business. Disclosure of key figures adjusted for these effects (so called “pro forma” key figures) by STADA is only to provide a supplement to the recorded IFRS key figures for a transparent comparison to a relevant period from the previous year. All text, pictures, trademarks, and other information contained in this document are subject to the copyright of STADA or subject to rights acquired from third parties. Trademark protection may apply even for preparations not indicated as trade marks. This document may not be reproduced in whole or in part without the express written consent of STADA. Any disputes arising out of or in connection with the content of this document, insofar as they are directed against STADA, shall be subject to German law, without prejudice to mandatory provisions of foreign law. -

Fy2014-Corporate-Presentation-March

STADA General information By making use of this document the reader acknowledges and agrees to the following: We accept no liability arising from the use of this document. STADA Arzneimittel AG, Bad Vilbel (in the following “STADA”), has made every effort to make sure that this document contains correct and up-to-date information. However, it accepts no responsibility or guarantee whatsoever in respect of topicality, accuracy and completeness of the information and assumes no obligation to update, complete or correct the information contained therein. The anticipated opportunities and risks to STADA’s activities have been described in detail in the Executive Board’s management reports in the annual reports. Current possible opportunities and risks are mentioned in the respective interim report. STADA’s performance indicators are party influenced by one-time special effects and/or effects not arising from the operating business. Disclosure of key figures adjusted for these effects (so called “pro forma” key figures) by STADA is only to provide a supplement to the recorded IFRS key figures for a transparent comparison to a relevant period from the previous year. All text, pictures, trademarks, and other information contained in this document are subject to the copyright of STADA or subject to rights acquired from third parties. Trademark protection may apply even for preparations not indicated as trade marks. This document may not be reproduced in whole or in part without the express written consent of STADA. Any disputes arising out of or in connection with the content of this document, insofar as they are directed against STADA, shall be subject to German law, without prejudice to mandatory provisions of foreign law. -

STADA General Information

STADA General information By making use of this document the reader acknowledges and agrees to the following: We accept no liability arising from the use of this document. STADA Arzneimittel AG, Bad Vilbel (in the following “STADA”), has made every effort to make sure that this document contains correct and up-to-date information. However, it accepts no responsibility or guarantee whatsoever in respect of topicality, accuracy and completeness of the information and assumes no obligation to update, complete or correct the information contained therein. The anticipated opportunities and risks to STADA’s activities have been described in detail in the Executive Board’s management reports in the annual reports. Current possible opportunities and risks are mentioned in the respective interim report. STADA’s performance indicators are party influenced by one-time special effects and/or effects not arising from the operating business. Disclosure of key figures adjusted for these effects (so called “pro forma” key figures) by STADA is only to provide a supplement to the recorded IFRS key figures for a transparent comparison to a relevant period from the previous year. All text, pictures, trademarks, and other information contained in this document are subject to the copyright of STADA or subject to rights acquired from third parties. Trademark protection may apply even for preparations not indicated as trade marks. This document may not be reproduced in whole or in part without the express written consent of STADA. Any disputes arising out of or in connection with the content of this document, insofar as they are directed against STADA, shall be subject to German law, without prejudice to mandatory provisions of foreign law. -

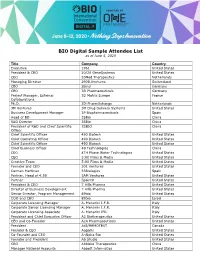

BIO Digital Sample Attendee List As of June 5, 2020

BIO Digital Sample Attendee List as of June 5, 2020 Title Company Country Executive 1961 United States President & CEO 20/20 GeneSystems United States CEO 20Med Therapeutics Netherlands Managing Director 2908.Ventures Switzerland CEO 2bind Germany CEO 3B Pharmaceuticals Germany Project Manager, External 3D Matrix Europe France Collaborations Ph.D. 3D-PharmXchange Netherlands 3M Ventures 3M Drug Delivery Systems United States Business Development Manager 3P Biopharmaceuticals Spain Head of BD 3SBio China R&D Director 3SBio China President of R&D and Chief Scientific 3SBIO China Officer Chief Scientific Officer 490 Biotech United States Chief Operating Officer 490 Biotech United States Chief Scientific Officer 490 Biotech United States Chief Business Officer 4B Technologies China CEO 4TH Phase Water Technologies United States CEO 5:00 Films & Media United States Creative Team 5:00 Films & Media United States Founder and CEO 501 Ventures United States Carmen Martinez 53Biologics Spain Partner, Head of 4:59 5AM Ventures United States Partner 5point0 United States President & CEO 7 Hills Pharma United States Director of Business Development 7 Hills Pharma United States Senior Director, Program Management 89bio United States COO and CBO 89bio Israel Corporate Licensing Manager A. Menarini I.F.R. Italy Corporate Senior Licensing Manager A. Menarini I.F.R. Italy Corporate Licensing Associate A. Menarini IFR Italy President and Chief Executive Officer A2 Biotherapeutics United States CEO and Co-Founder A2A Pharmaceuticals United States President -

2012 Gedeon Richter Annual Report

Gedeon Richter annual report 2012 WorldReginfo - e64f6d7c-27ef-4dd3-b875-e8259c334c8c Table of Contents I. Richter – Corporate Review 4 1. Fact Sheet 5 2. Financial Highlights 6 3. Chairman’s Letter to the Shareholders 9 4. Investor Information 10 a. Share Price and Market Capitalisation 10 b. Annual General Meeting 11 c. Dividend 11 d. Investor Relations Activities 11 e. Analysts Providing Coverage 12 f. Information Regarding Richter Shares 12 5. Corporate Governance 15 6. Company’s Boards 17 7. Risk Management 20 8. Litigation Proceedings 21 II. Managing Director’s Review 22 III. In Transition 26 1. The Pharmaceutical Industry 27 2. Transition from Regional Midpharma to Pan-European Specialty Pharma 27 3. Strategic Focus – Innovation 28 a. Female Healthcare 28 b. Original Research – Focus on CNS 31 c. Biosimilars 32 IV. Business Review 34 1. Pharmaceuticals 35 a. Research and Development 35 b. Manufacturing and Supply 39 c. Products 39 d. Sales by Markets 45 e. Corporate Social Responsibility 55 f. People 57 2. Wholesale and Retail 61 3. Group Figures 61 a. Business Segment Information 62 b. Consolidated Turnover 62 c. Key Financial Data 63 d. Profit and Loss Items 63 e. Balance Sheet Items 66 f. Cash Flow 67 g. Treasury Policy 67 h. Capital Expenditure 68 V. Consolidated Financial Statements 69 VI. Appendices 136 Annual Report | Gedeon Richter 2012 | 3 WorldReginfo - e64f6d7c-27ef-4dd3-b875-e8259c334c8c 1. Fact Sheet ichter Group is active in two major busi- marketing of pharmaceutical products are the core R ness segments, primarily Pharmaceuticals activities of Richter and in this endeavour the Group comprising the research and development, is supported by a number of subsidiaries, joint manufacturing, sales and marketing of ventures and associated companies. -

Gedeon Richter Annual Report 2013 Table of Contents

Gedeon Richter Annual Report 2013 Table of Contents I. Richter – Corporate Review 4 1. Fact Sheet 5 2. Financial Highlights 6 3. Chairman’s Letter to the Shareholders 9 4. Investor Information 10 a) Share Price and Market Capitalisation 10 b) Annual General Meeting 11 c) Dividend 11 d) Investor Relations Activities 11 e) Analysts Providing Coverage 12 f) Information Regarding Richter Shares 13 5. Corporate Governance 15 6. Company’s Boards 17 7. Risk Management 20 8. Litigation Proceedings 21 II. Managing Director’s Review 22 III. In Transition 26 1. The Pharmaceutical Industry 27 2. Transition from Regional Midpharma to Pan-European Specialty Pharma 27 3. Strategic Focus – Innovation 27 a) Female Healthcare 28 b) Original Research – Focus on CNS 32 c) Biosimilars 33 IV. Business Review 34 1. Pharmaceuticals 35 a) Research and Development 35 b) Manufacturing and Supply 37 c) Products 38 d) Sales by Markets 40 e) Corporate Social Responsibility 49 f) People 51 2. Wholesale and Retail 55 3. Group Figures 55 a) Business Segment Information 56 b) Consolidated Turnover 56 c) Key Financial Data 57 d) Profit and Loss Items 57 e) Balance Sheet Items 60 f) Cash Flow 61 g) Treasury Policy 61 h) Capital Expenditure 62 V. Appendices 64 Annual Report I Gedeon Richter 2013 I 3 1. Fact Sheet Richter Group is active in two major business segments, primarily Pharmaceuticals comprising the research and development, manufacturing, sales and marketing of pharmaceutical products, and it is also engaged in the I. Richter – Corporate Review Wholesale and Retail of these products. In addition, there is a third group (’Other’) of companies comprising those members of the Group which provide auxiliary services to the former segments. -

World Journal of Pharmaceutical Research Sen Et Al

World Journal of Pharmaceutical Research Sen et al. World Journal of Pharmaceutical SJIF ImRepactsearch Factor 6.805 Volume 5, Issue 9, 1841-1866. Review Article ISSN 2277– 7105 BIOSIMILARS AS BIOACTIVE MOLECULAR CLONE 1Prof. Dr. Dhrubo Jyoti Sen*, 2Jahangir Nabi, 2Pooja Raj and 2Jainik Khamar 1Department of Pharmaceutical Chemistry, Shri Sarvajanik Pharmacy College, Gujarat Technological University, Arvind Baug, Mehsana-384001, Gujarat, India. 2Delhi Institute of Pharmaceutical Sciences & Research (DIPSAR), Mehrauli-Badarpur Road, Puspvihar, Sector-3, New Delhi-110017, India. ABSTRACT Article Received on 24 July 2016, Biologics are 200 to 1,000 times the size of a small molecule (generic) Revised on 12 August 2016, drug and far more structurally complex. Additionally, biologics and Accepted on 01 Sept 2016 biosimilars are manufactured in living cells, then extracted and DOI: 10.20959/wjpr201610-7121 purified, whereas small molecule drugs and generics are manufactured purely via chemical synthesis. These fundamental differences in *Corresponding Author complexity and large-scale manufacturing are at the core of why Prof. Dr. Dhrubo Jyoti Sen Department of biosimilars are not equal to generics. Biologics and biosimilars are Pharmaceutical Chemistry, produced in living cells with a multi-step process. Initially, a basic Shri Sarvajanik Pharmacy protein structure is ―translated‖ from a DNA sequence and then College, Gujarat modifications, including changes and additions, are made to that basic Technological University, protein structure. These later changes and additions are called post- Arvind Baug, Mehsana- 384001, Gujarat, India. translational modifications. The impact of post-translational modifications on a product is similar to the impact of a farming environment on growing tomatoes.