IN the COURT of SPECIAL JUDGE XXXVI ADDITIONAL CITY CIVIL and SESSIONS JUDGE, BANGALORE Spl

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

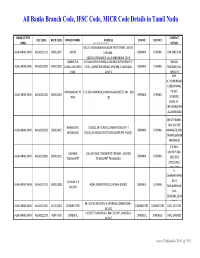

Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu

All Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu NAME OF THE CONTACT IFSC CODE MICR CODE BRANCH NAME ADDRESS CENTRE DISTRICT BANK www.Padasalai.Net DETAILS NO.19, PADMANABHA NAGAR FIRST STREET, ADYAR, ALLAHABAD BANK ALLA0211103 600010007 ADYAR CHENNAI - CHENNAI CHENNAI 044 24917036 600020,[email protected] AMBATTUR VIJAYALAKSHMIPURAM, 4A MURUGAPPA READY ST. BALRAJ, ALLAHABAD BANK ALLA0211909 600010012 VIJAYALAKSHMIPU EXTN., AMBATTUR VENKATAPURAM, TAMILNADU CHENNAI CHENNAI SHANKAR,044- RAM 600053 28546272 SHRI. N.CHANDRAMO ULEESWARAN, ANNANAGAR,CHE E-4, 3RD MAIN ROAD,ANNANAGAR (WEST),PIN - 600 PH NO : ALLAHABAD BANK ALLA0211042 600010004 CHENNAI CHENNAI NNAI 102 26263882, EMAIL ID : CHEANNA@CHE .ALLAHABADBA NK.CO.IN MR.ATHIRAMIL AKU K (CHIEF BANGALORE 1540/22,39 E-CROSS,22 MAIN ROAD,4TH T ALLAHABAD BANK ALLA0211819 560010005 CHENNAI CHENNAI MANAGER), MR. JAYANAGAR BLOCK,JAYANAGAR DIST-BANGLAORE,PIN- 560041 SWAINE(SENIOR MANAGER) C N RAVI, CHENNAI 144 GA ROAD,TONDIARPET CHENNAI - 600 081 MURTHY,044- ALLAHABAD BANK ALLA0211881 600010011 CHENNAI CHENNAI TONDIARPET TONDIARPET TAMILNADU 28522093 /28513081 / 28411083 S. SWAMINATHAN CHENNAI V P ,DR. K. ALLAHABAD BANK ALLA0211291 600010008 40/41,MOUNT ROAD,CHENNAI-600002 CHENNAI CHENNAI COLONY TAMINARASAN, 044- 28585641,2854 9262 98, MECRICAR ROAD, R.S.PURAM, COIMBATORE - ALLAHABAD BANK ALLA0210384 641010002 COIIMBATORE COIMBATORE COIMBOTORE 0422 2472333 641002 H1/H2 57 MAIN ROAD, RM COLONY , DINDIGUL- ALLAHABAD BANK ALLA0212319 NON MICR DINDIGUL DINDIGUL DINDIGUL -

SNO APP.No Name Contact Address Reason 1 AP-1 K

SNO APP.No Name Contact Address Reason 1 AP-1 K. Pandeeswaran No.2/545, Then Colony, Vilampatti Post, Intercaste Marriage certificate not enclosed Sivakasi, Virudhunagar – 626 124 2 AP-2 P. Karthigai Selvi No.2/545, Then Colony, Vilampatti Post, Only one ID proof attached. Sivakasi, Virudhunagar – 626 124 3 AP-8 N. Esakkiappan No.37/45E, Nandhagopalapuram, Above age Thoothukudi – 628 002. 4 AP-25 M. Dinesh No.4/133, Kothamalai Road,Vadaku Only one ID proof attached. Street,Vadugam Post,Rasipuram Taluk, Namakkal – 637 407. 5 AP-26 K. Venkatesh No.4/47, Kettupatti, Only one ID proof attached. Dokkupodhanahalli, Dharmapuri – 636 807. 6 AP-28 P. Manipandi 1stStreet, 24thWard, Self attestation not found in the enclosures Sivaji Nagar, and photo Theni – 625 531. 7 AP-49 K. Sobanbabu No.10/4, T.K.Garden, 3rdStreet, Korukkupet, Self attestation not found in the enclosures Chennai – 600 021. and photo 8 AP-58 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Community Certificate Wrongly enclosed Pondicherry – 605 007. 9 AP-60 V.A.Kishor Kumar No.19, Thilagar nagar, Ist st, Kaladipet, Only one ID proof attached. Thiruvottiyur, Chennai -600 019 10 AP-61 D.Anbalagan No.8/171, Church Street, Only one ID proof attached. Komathimuthupuram Post, Panaiyoor(via) Changarankovil Taluk, Tirunelveli, 627 761. 11 AP-64 S. Arun kannan No. 15D, Poonga Nagar, Kaladipet, Only one ID proof attached. Thiruvottiyur, Ch – 600 019 12 AP-69 K. Lavanya Priyadharshini No, 35, A Block, Nochi Nagar, Mylapore, Only one ID proof attached. Chennai – 600 004 13 AP-70 G. -

S. No. App.No. Name Address 1 AP-6 J.R. Rahul 2 AP-16 K. Pradeep

Accepted list for the post of Reader - BC (OTBCM) (NP) -2 S. No. App.No. Name Address 1 AP-6 J.R. Rahul No.23/61, Gokulam Attingarai, Manavalakurichi, Kanyakumari – 629 252 2 AP-16 K. Pradeep Subramanian No.30, Pandiyan Street, Sundar Nagar, Thirunagar, Madurai – 625 006. 3 AP-30 A. John Antony K.Rasiamangalam(Po.), Alangankudi Taluk, Pudhukottai – 622 301. 4 AP-33 M. Subha Door No.6, 2ndFloor, Vasanth Apartments, C Block, No.1, Maduraiswamy Madam Street, Perambur, Chennai – 600 011. 5 AP-35 R. Vijayalakshmi No.26-A, Sathymoorthy Street, Narimedu, Madurai – 625 002. 6 AP-40 P. Ganesh Old No.L/1229, New No.20, 29thCross Street, Thiruvalluvar Nagar, Thiruvanmiyur, Chennai – 600 041. 7 AP-45 K. Balasubramanian No.6/40, Thiruvalluvar Street, Kuladheepamangalam (Post) Thirukovilur Taluk, Villupuram – 605 756. 8 AP-51 L. Babu No.73/45, Munusamy Street, Ayanavaram, Chennai – 600 023. 9 AP-56 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Pondicherry – 605 007. 10 AP-62 R.D. Mathanram No.57, Jeeyar Narayanapalayam St, Kanchipuram – 631 501 11 AP-77 M.Parameswari No.8/4, Alagiri Nagar, 1ststreet, Vadapalani, chennai -26. 12 AP-83 G. Selva Kumari No. 12, G Block, Singara thottam, Police Quarters, Old Washermen pet, Chennai 600 021 13 AP-89 P. Mythili No.137/64, Sanjeeviroyan Koil Street, Old Washermenpet, Chennai – 600 021. 14 AP-124 K. Balaji No.11, Muthumariamman Koil Street, Bharath Nagar, Selaiyur, Chennai – 600 073. 15 AP-134 S. Anitha No.5/55-A, Main Road, Siruvangunam, Iraniyasithi Post, Seiyur Taluk, Kancheepuram – 603 312. -

Sri P.A.C. Ramasamy Raja "Gurubakthamani" Founder, Ramco Group Sri P.R

SRI P.A.C. RAMASAMY RAJA "GURUBAKTHAMANI" FOUNDER, RAMCO GROUP SRI P.R. RAMASUBRAHMANEYA RAJHA SRIDHARMARAKSHAKAR, RAMCO GROUP ISO 14001 & ISO 9001 IS 18001 Company Overview Company Overview Flagship Company & Brand of the Ramco Group The Ramco Cements Limited is the flagship company of the Ramco Group, a well-known business group of South India. It is headquartered at Chennai. The main product of the company is Portland cement, manufactured in eight state-of-the art production facilities that includes Integrated Cement plants and Grinding units with a current total production capacity of 16.5 MTPA (out of which Satellite Grinding units capacity alone is 4 MTPA). The company is the fifth largest cement producer in the country. is the most popular cement brand in South India. The company also produces Ready Mix Concrete and Dry Mortar products, and operates one of the largest wind farms in the country. Integrated Cement Plants ✓Ramasamy Raja Nagar, Virudhunagar District, Tamil Nadu ✓Alathiyur, Ariyalur District, Tamil Nadu ✓Ariyalur, Govindapuram, Ariyalur District, Tamil Nadu ✓Jayanthipuram,Krishna District, Andhra Pradesh ✓Mathodu, Chitradurga District, Karnataka Grinding Units •Uthiramerur, Kanchipuram District, Tamil Nadu •Valapady, Salem District, Tamil Nadu •Kolaghat, Purba Medinipur District, West Bengal •Vizag, Visakhapatnam , Andhra Pradesh Packing Terminals •Nagercoil Packing Unit, Kumarapuram, Aralvaimozhi, Kanyakumari District, Tamil Nadu State-of-the-Art Research Centre •Ramco Research Development Centre (RRDC), Chennai Page 1/30 Safety Department Objectives ➢ Achieving ‘Zero Injuries/Incidents’. To attain accident free man hours. ➢ Emergency Preparedness & Response and Planning. ➢ To promote and improve the Safety and Health awareness of company employees & contract workmen. ➢ To strengthen safety movement and drive the culture from top to bottom level as the safety is each and every one’s responsibility. -

Tamil Nadu Government Gazette

© [Regd. No. TN/CCN/467/2009-11. GOVERNMENT OF TAMIL NADU [R. Dis. No. 197/2009. 2011 [Price: Rs. 25.60 Paise. TAMIL NADU GOVERNMENT GAZETTE PUBLISHED BY AUTHORITY No. 23] CHENNAI, WEDNESDAY, JUNE 22, 2011 Aani 7, Thiruvalluvar Aandu–2042 Part VI—Section 4 Advertisements by private individuals and private institutions CONTENTS PRIVATE ADVERTISEMENTS Change of Names .. 1245-1308 1119 NOTICE NO LEGAL RESPONSIBILITY IS ACCEPTED FOR THE PUBLICATION OF ADVERTISEMENTS REGARDING CHANGE OF NAME IN THE TAMIL NADU GOVERNMENT GAZETTE. PERSONS NOTIFYING THE CHANGES WILL REMAIN SOLELY RESPONSIBLE FOR THE LEGAL CONSEQUENCES AND ALSO FOR ANY OTHER MISREPRESENTATION, ETC. (By Order) Director of Stationery and Printing. CHANGE OF NAMES My son, H. Dhamodaran, son of Thiru S.B. Harikrishnarajh, My son, Mohammed Azeez, born on 4th February 2007 born on 24th January 1996 (native district: Tiruvallur), residing (native district: Vellore), residing at No. 73, 3rd Street, at No. 31/2, Balasubramaniam Street, VOC Block, Gaffarbad, Vaniyambadi, Vellore-635 751, shall henceforth Jafferkanpet, Chennai-600 083, shall henceforth be known be known as I MD SHUBAZ. as S.H. VIJAYDAMODAR. M. ILIYAS AHMED. H. GOMATHI. Vaniyambadi, 13th June 2011. (Father.) Chennai, 13th June 2011. (Mother.) I, L. Violet, wife of Thiru M.M. Luke, born on My daughter, C. Muthumeena, born on 3rd August 1993 3rd August 1960 (native district: Salem), residing at (native district: Chennai), residing at Old No. 1/98A, New No. 618, Perfume Paradise, Lady Seat Road, Yercaud, No. 3/241, Neelankarai, Sengeni Amman Koil Street, Salem-636 601, shall henceforth be known Tambaram, Chennai-600 041, shall henceforth be known as as L NAVIS VIOLET. -

Mint Building S.O Chennai TAMIL NADU

pincode officename districtname statename 600001 Flower Bazaar S.O Chennai TAMIL NADU 600001 Chennai G.P.O. Chennai TAMIL NADU 600001 Govt Stanley Hospital S.O Chennai TAMIL NADU 600001 Mannady S.O (Chennai) Chennai TAMIL NADU 600001 Mint Building S.O Chennai TAMIL NADU 600001 Sowcarpet S.O Chennai TAMIL NADU 600002 Anna Road H.O Chennai TAMIL NADU 600002 Chintadripet S.O Chennai TAMIL NADU 600002 Madras Electricity System S.O Chennai TAMIL NADU 600003 Park Town H.O Chennai TAMIL NADU 600003 Edapalayam S.O Chennai TAMIL NADU 600003 Madras Medical College S.O Chennai TAMIL NADU 600003 Ripon Buildings S.O Chennai TAMIL NADU 600004 Mandaveli S.O Chennai TAMIL NADU 600004 Vivekananda College Madras S.O Chennai TAMIL NADU 600004 Mylapore H.O Chennai TAMIL NADU 600005 Tiruvallikkeni S.O Chennai TAMIL NADU 600005 Chepauk S.O Chennai TAMIL NADU 600005 Madras University S.O Chennai TAMIL NADU 600005 Parthasarathy Koil S.O Chennai TAMIL NADU 600006 Greams Road S.O Chennai TAMIL NADU 600006 DPI S.O Chennai TAMIL NADU 600006 Shastri Bhavan S.O Chennai TAMIL NADU 600006 Teynampet West S.O Chennai TAMIL NADU 600007 Vepery S.O Chennai TAMIL NADU 600008 Ethiraj Salai S.O Chennai TAMIL NADU 600008 Egmore S.O Chennai TAMIL NADU 600008 Egmore ND S.O Chennai TAMIL NADU 600009 Fort St George S.O Chennai TAMIL NADU 600010 Kilpauk S.O Chennai TAMIL NADU 600010 Kilpauk Medical College S.O Chennai TAMIL NADU 600011 Perambur S.O Chennai TAMIL NADU 600011 Perambur North S.O Chennai TAMIL NADU 600011 Sembiam S.O Chennai TAMIL NADU 600012 Perambur Barracks S.O Chennai -

![119] 000033 CHENNAI, FRIDAY, APRIL 1, 2011 Panguni 18, Thiruvalluvar Aandu–2042 Part V—Section 2](https://docslib.b-cdn.net/cover/5657/119-000033-chennai-friday-april-1-2011-panguni-18-thiruvalluvar-aandu-2042-part-v-section-2-2215657.webp)

119] 000033 CHENNAI, FRIDAY, APRIL 1, 2011 Panguni 18, Thiruvalluvar Aandu–2042 Part V—Section 2

© [Regd. No. TN/CCN/467/2009-11. GOVERNMENT OF TAMIL NADU [R. Dis. No. 197/2009. 2011 [Price: Rs. 96.80 Paise. TAMIL NADU GOVERNMENT GAZETTE EXTRAORDINARY PUBLISHED BY AUTHORITY No. 119] 000033 CHENNAI, FRIDAY, APRIL 1, 2011 Panguni 18, Thiruvalluvar Aandu–2042 Part V—Section 2 Notifications relating to list of contesting candidates from Collectors and Returning Officers, other Heads of Departments, Election Tribunals, etc. GENERAL ELECTIONS TO TAMIL NADU LEGISLATIVE ASSEMBLY, 2011 No. SRO E-1/2011. Dated 1st April 2011. In pursuance of sub-rule (2) of rule 11 of the Conduct of Elections Rules, 1961, the following is published for general information:— FORM 7-A LIST OF CONTESTING CANDIDATES [See rule 10(1) of the Conduct of Elections Rules, 1961.] Election to the Tamil Nadu Legislative Assembly from the 1. GUMMIDIPOONDI CONSTITUENCY Serial Name of Candidate. Address of Candidate. Party Affiliation. Symbol Allotted. Number. (1) (2) (3) (4) (5) 1 Chakravarthi Old No. 321, New No. 396, Bharatiya Lotus Sriraman, B. Sengalamman Kandigai, Janata Party Uthukottai Taluk, Tiruvallur District. 2 Srinivasan, D. No. 209/D, C.V. Road, 1st Lane, Bahujan Elephant Tiruvallur-602 001. Samaj Party 3 Sekar, K.N. 16/25, Anna Street, Pattali Mango Kallikuppam, Makkal Katchi Ambattur, Chennai-600 053. DTP—V-2 Ex. (119)—1 [1] 2 TAMIL NADU GOVERNMENT GAZETTE EXTRAORDINARY Serial Name of Candidate. Address of Candidate. Party Affiliation. Symbol Allotted. Number. (1) (2) (3) (4) (5) 4 Asokan, G. 1/344, Perumal Koil Street, Puratchi Brush Bammudhukulam Village, Bharatham Ambathur Taluk, Tiruvallur District. 5 Sudhakar, M. No. 98, Karakkambakkam, Republican Party of Television Devandavakkam, India (A) Uthukkottai Taluk, Tiruvallur District. -

List of Suppliers/Manufacturers Enlisted with TEDA for SPV/Solar Thermal Systems

List of Suppliers/Manufacturers enlisted with TEDA for SPV/Solar Thermal Systems Note: The purchaser shall ensure the quality and standards of system/components as per MNRE/BIS/IEC standards before purchase. TEDA does not certify the quality & prices of enlisted Suppliers/Manufacturers/System Integrators Tamil Nadu Energy Development Agency (A unit of Government of Tamil Nadu) List of Manufacturers/Suppliers of Solar Products Enlisted with TEDA 5th Floor EVK Sampath Maaligai, 68 College Road, Chennai 600 006 Phone: 28224830, 28212249, 28236592, Fax No.: 28222971 Emai: [email protected], www.teda.in Telephone Name of the Products Manufacturer/ S. No Number Valid upto Company Supplier/ & Fax Number System Integrator Solar Lantern(LED), M/s. Nova Energy Corp., [email protected] Solar street lighting 1 [email protected] 30.04.2020 No.132,Nehru Street, Indira Nagar, System(LED & CFL), Manufacturer Perumugai, M: 9159111888/8940500641 Solar Home Vellore-632 009 Lighting System (M2) M/s. Aargee Equipments Pvt.Ltd., SPV(Solar Lantern No.197/7A, 10 th 044-42834477 (2A), Solar Street 2 Street, Jain Nagar, M: 9442242398 Lighting System 31.3.2017 Manufacturer Arumbakkam, [email protected] (CFL), Solar Home Chennai 600 106 [email protected] Lighting System (M4) 0427- M/s. Annai Solar Systems & Solar Photovoltaic 4037295/4037018 Fabricators Systems 3 9443217945/ 31.5.2020 Supplier 19/82 G, Ramalinga & 9965517945 Madalayam Street Solar Water Heating [email protected] Gugai, Salem – 636 006 Systems 0422-2901468/ M/s. KL Solar Company Pvt Ltd 0422-6563638 SLS-CFL 1/482, Transport 4 F:0422-2567562 SHL (CFL) –Model 30.4.2017 Manufacturer Nagar,Neelambur Cell:9894028393 IV - Coimbatore [email protected] Pin Code 641 062 044 -42129378 M/s. -

CHENNAI NORTH No

PURPOSE FOR WHICH S. No. CIRCLE OFFICE NAME OF ADVOCATE POSTAL ADDRESS CONTACT NO./ MOBILE NO. EMAIL APPROVED CO: CHENNAI NORTH No. 75, F2, 1st floor, KK Road, Venkatapuram, 1 Chennai North Reghu Raja 9841107212 [email protected] DRT/ Civil cases Ambattur, Chennai - 600 053 No.6/2,Gangaiyammen Koil Street 2 Chennai North Sh.S.Senthillazhagan 9789238627 [email protected] DRT/ Civil cases Pernambut,Pernambut Taluk, Vellore District. 30/D,1st East Main Road, 1st Floor, Near Silk Mill 3 Chennai North K.M.Bhoopthi Stop and Mahindra Tractor Company, 9842378972 [email protected] DRT/ Civil cases Gandhinagar, Vellore.-6. Office: no. 12A, Brindhavanam Street, Mylapore, Chennai - 600004; Chamber : no. 1, Law 4 Chennai North Abdul Wahab 044-24984299; 9444334299 [email protected] DRT/ Civil cases Chambers, High Court Buildings, Chennai - 600104 Chokalingam.S.P.,F-4 Morning Rose,R.C.Victoriya 5 Chennai North Chokkalingam Garden,No -1,Airforce Station Road, East 9840121245 [email protected] DRT/ Civil cases Tambaram,Chennai-59. old No 125, 4th floor , Angappan Naiken street, 7 Chennai North Jayachandra Babu 9940193926 [email protected] DRT/ Civil cases Cananra Bank building, Parry's Chennai-1 K.N.ChinnaKrishnan,No 9/4 MGR 8 Chennai North K.N. Chinnakrishnan Street,Venkateswara Nagar, GKM Colony, 9965554234, 25507000 [email protected] DRT/ Civil cases Chennai-600082 F-101,First floor, Subiksha Trinity, 14/9, 4th 9840075917/24422588/24450 9 Chennai North K.V. Babu [email protected] DRT/ Civil cases Street, Bakthavatsalam Nagar, Chennai 60 830 WOMEN LAWYERS ASSOCIATION, NEW LAW 10 Chennai North L. -

A-CHANNEL PPA DETAILS for 2009 Seat PP S.N Year Name Address Proposal Se File No

A-CHANNEL PPA DETAILS FOR 2009 Seat PP S.N Year Name Address Proposal Se File No. Year Appd.on No. o. at A 4909 1 2009 N.P. Raghunath Door No.2, East Coast Addl. Construction of GF A2 13928 2008 5/1/2009 Road, Kottivakkam, pt + FF (pt) with three Chennai, s.No.239/2, 3 dwelling units & 4 Patta S.No.239/0,1, 2, Kottivakkam 4910 2 2009 S. Margabandu P.No.36 & 37, 2-nd GF Part + FF part with A1 5143 2008 12/1/2009 Cross Street, one d.u. Karpagambal Nagar 1-st Main Road in S.No.232/1B1 as per patta S.No.232/43 & 44, Kottivakkam A 4911 3 2009 A. Murugan P No.36/2, 37/1, 37/2, Stilt Floor pt + GFpt +FF A2 17745 2008 7/1/2009 Ramakrishna Nagar, & SF part with 6 d.u. res. Porur, Chennai in Buldg A S.No.309/4B, Porur 4912 4 2009 Dhanuskodi P.No.66B, 8-th Street, Stilt Floor pt + GFpt +FF A1 8056 2008 Ram Nagar North & SF part with 4 d.u. res. Extension, Velachery, Buldg Chennai-42 in Patta S.No.709/24 part, A Velachery 4913 5 2009 S. Alamelu P.No.70, Alagammal GF with one d.u. A2 7417 2008 2/1/2009 Nagar 2-st Main Road, Chennai-107 in S.No.101 part, Patta S.No.101/1A2, A Nerkundram 4914 6 2009 Saravana Prabhu P.No.A,B,C, Stilt Floor pt + GFpt +FF A3 21858 2007 27/1/2009 Thiruvalluvar Salai, & SF part with 4 d.u. -

Tamil Nadu Public Service Commission Bulletin

© [Regd. No. TN/CCN-466/2012-14. GOVERNMENT OF TAMIL NADU [R. Dis. No. 196/2009 2018 [Price: Rs. 145.60 Paise. TAMIL NADU PUBLIC SERVICE COMMISSION BULLETIN No. 7] CHENNAI, FRIDAY, MARCH 16, 2018 Panguni 2, Hevilambi, Thiruvalluvar Aandu-2049 CONTENTS DEPARTMENTAL TESTS—RESULTS, DECEMBER 2017 NAME OF THE TESTS AND CODE NUMBERS Pages Pages The Tamil Nadu Government office Manual Departmental Test for Junior Assistants In Test (Without Books & With Books) the office of the Administrator - General (Test Code No. 172) 552-624 and official Trustee- Second Paper (Without Books) (Test Code No. 062) 705-706 the Account Test for Executive officers (Without Books& With Books) (Test Code No. 152) 625-693 Local Fund Audit Department Test - Commercial Book - Keeping (Without Books) Survey Departmental Test - Field Surveyor’s (Test Code No. 064) 706-712 Test - Paper -Ii (Without Books) (Test Code No. 032) 694-698 Fisheries Departmental Test - Ii Part - C - Fisheries Technology (Without Books) Fisheries Departmental Test - Ii Part - B - (Test Code No. 067) 712 Inland Fisheries (Without Books) (Test Code No. 060) 698 Forest Department Test - forest Law and forest Revenue (Without Books) Fisheries Departmental Test - Ii Part - (Test Code No. 073) 713-716 A - Marine Fisheries (Without Books) (Test Code No. 054) 699 Departmental Test for Audit Superintendents of Highways Department - Third Paper Departmental Test for Audit Superintendents (Constitution of India) (Without Books) of Highways Department - First Paper (Test Code No. 030) 717 (Precis and Draft) (Without Books) (Test Code No. 020) 699 The Account Test for Public Works Department officers and Subordinates - Part - I (Without Departmental Test for the officers of Books & With Books) (Test Code No. -

SL.No Street Name Zone Code

SL.No Zone Code Street Name WD001 SANTHI NAGAR 1 SANTHI NAGAR 6TH STREET D 2 THIRUMAL NAGAR 2ND STREET D 3 APPADHURAI NAGAR MAIN STREET D 4 APPADHURAI NAGAR 5TH STREET D 5 APPADHURAI NAGAR 4TH STREET D 6 APPADHURAI NAGAR 3RD STREET D 7 APPADHURAI NAGAR 2ND STREET D 8 APPADHURAI NAGAR 1ST STREET D 9 ANJAL NAGAR 3RD STREET D 10 ANJAL NAGAR 2ND STREET D 11 ANJAL NAGAR 1ST STREET D 12 CHOKKALINGA NAGAR 3RD STREET(VILANGUDI) D 13 CHOKKALINGA NAGAR 2ND STREET(VILANGUDI) D 14 CHOKKALINGA NAGAR 1ST STREET(VILANGUDI) D 15 CHELLAYA NAGAR D 16 ASOHK NAGAR 4TH STREET D 17 ASOHK NAGAR 3RD STREET D 18 CHOKKALINGA NAGAR 6TH STREET (VILANGUDI) D 19 ASOHK NAGAR 2ND STREET D 20 ASOHK NAGAR 1ST STREET D 21 PERIYAR NAGAR 1ST STREET D 22 PANDIYAN NAGAR 4TH STREET D 23 PANDIYAN NAGAR 3RD STREET D 24 PANDIYAN NAGAR 2ND STREET D 25 PANDIYAN NAGAR 1ST STREET D 26 PALAMEDU MAIN ROAD, RAILAR NAGAR D 27 PALAMEDU MAIN ROAD, ASOHK NAGAR MAIN D 28 PALAMEDU MAIN ROAD CHOKKALINGA NAGAR D 29 PALAMEDU MAIN ROAD D 30 RAILAR NAGAR 6TH STREET D 31 RAILAR NAGAR 5TH STREET D 32 RAILAR NAGAR 4TH STREET D 33 RAILAR NAGAR 3RD STREET D 34 RAILAR NAGAR 2ND STREET D 35 RAILAR NAGAR 1ST STREET D 36 POOMAN NAGAR 4TH STREET D 37 POOMAN NAGAR 3RD STREET D 38 POOMAN NAGAR 2ND STREET D 39 SANTHI NAGAR 4TH STREET D 40 SANTHI NAGAR 3RD STREET D 41 SANTHI NAGAR 2ND STREET D 42 SANTHI NAGAR 1ST STREET D 43 SANTHI NAGAR , MALLIGAI STREET D 44 RMS COLONY 4TH STREET D 45 RMS COLONY 3RD STREET D 46 RMS COLONY 2ND STREET D 47 RMS COLONY 1ST STREET D 48 SANTHI NAGAR 5TH STREET D 49 RAMUNI NAGAR