Meeting the Needs of Vulnerable Claimants

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

All Party Parliamentary Group on British Muslims

All Party Parliamentary Group on British Muslims The inquiry into a working definition of Islamophobia Report on the inquiry into A working definition of Islamophobia / anti-Muslim hatred All Party Parliamentary Group on British Muslims Report on the inquiry into a working definition of Islamophobia / anti-Muslim hatred 3 The All Party Parliamentary Group on British Muslims was launched in 2017. The cross party group of parliamentarians is co-chaired by Anna Soubry MP and Wes Streeting MP. The Group was established to highlight the aspirations and challenges facing British Muslims; to celebrate the contributions of Muslim communities to Britain and to investigate prejudice, discrimination and hatred against Muslims in the UK. appgbritishmuslims.org facebook.com/APPGBritMuslims @APPGBritMuslims Report on the inquiry into A working definition of Islamophobia / anti-Muslim hatred All Party Parliamentary Group on British Muslims Contents Foreword by Dominic Grieve QC 6 Foreword by Anna Soubry and Wes Streeting 7 Executive Summary 9 Introduction 12 Chapter 1 Literature review 19 Chapter 2 - Arriving at a working definition 23 Chapter 3 - Our findings 27 An INDEX to Tackle Islamophobia 51 Chapter 4 - Community consultation findings 52 Conclusion 56 Acknowledgements 60 Appendix 1 - Written evidence 61 Appendix 2 - Oral evidence sessions 62 Appendix 3 - Community consultation participants 63 Appendix 4 - Islamophobia / Anti Muslim hatred questionnaire 64 Bibliography 66 5 Foreword s Chair of the Citizens UK Commission on Islam, Participation and Public Life, I travelled round the country hearing evidence as to the extent to which this desirable goal was taking place and as to the reasons why it was not happening Ain the way many Muslims and others wished. -

Organised With: Fabian Summer Conference 2016 Britain's Future, Labour's Future Saturday 21 May 2016, 09.30 – 17.15 TUC Co

Organised with: Fabian Summer conference 2016 Britain’s Future, Labour’s Future Saturday 21 May 2016, 09.30 – 17.15 TUC Congress Centre, 28 Great Russell Street, London, WC1B 3LS 9.30-10.20 Registration Tea and coffee 10.20-10.45 Welcome Main Hall Andrew Harrop (general secretary, Fabian Society) Massimo D’Alema (president, Foundation for European Progressive Studies) 10.45-11.30 Keynote speech Main Hall Gordon Brown (former prime minister) 11.30-12.20 Morning Plenary ‘Should we stay or should we go now’: What should the left decide? Main Hall Caroline Flint MP (Labour MP, Don Valley) Baroness Jenny Jones (Green Party, Member of the House of Lords) Tim Montgomerie (columnist, The Times) Chair: Andrew Harrop, (general secretary, Fabian Society) 12.30-13.30 Breakout sessions Main Hall It’s the economy, stupid: what’s best for jobs and growth? Shabana Mahmood MP (Labour MP, Birmingham Ladywood) John Mills (deputy chair, Vote Leave) Lucy Anderson MEP (Labour MEP for London) Vicky Pryce (economist) Chair: Michael Izza (chief executive, ICAEW) Council Chamber The jury’s out: can the campaigns persuade the ‘undecideds’? Interactive session Brendan Chilton (general secretary, Labour Leave) Antonia Bance (head of campaigns and communications, TUC) Richard Angell (director, Progress) Chair: Felicity Slater (exec member, Fabian Women’s Network) Meeting Room 1 Drifting apart? The four nations and Europe Nia Griffith MP (shadow secretary of state for wales and Labour MP for Llanelli) John Denham (director, University of Winchester’s Centre for English -

1. Debbie Abrahams, Labour Party, United Kingdom 2

1. Debbie Abrahams, Labour Party, United Kingdom 2. Malik Ben Achour, PS, Belgium 3. Tina Acketoft, Liberal Party, Sweden 4. Senator Fatima Ahallouch, PS, Belgium 5. Lord Nazir Ahmed, Non-affiliated, United Kingdom 6. Senator Alberto Airola, M5S, Italy 7. Hussein al-Taee, Social Democratic Party, Finland 8. Éric Alauzet, La République en Marche, France 9. Patricia Blanquer Alcaraz, Socialist Party, Spain 10. Lord John Alderdice, Liberal Democrats, United Kingdom 11. Felipe Jesús Sicilia Alférez, Socialist Party, Spain 12. Senator Alessandro Alfieri, PD, Italy 13. François Alfonsi, Greens/EFA, European Parliament (France) 14. Amira Mohamed Ali, Chairperson of the Parliamentary Group, Die Linke, Germany 15. Rushanara Ali, Labour Party, United Kingdom 16. Tahir Ali, Labour Party, United Kingdom 17. Mahir Alkaya, Spokesperson for Foreign Trade and Development Cooperation, Socialist Party, the Netherlands 18. Senator Josefina Bueno Alonso, Socialist Party, Spain 19. Lord David Alton of Liverpool, Crossbench, United Kingdom 20. Patxi López Álvarez, Socialist Party, Spain 21. Nacho Sánchez Amor, S&D, European Parliament (Spain) 22. Luise Amtsberg, Green Party, Germany 23. Senator Bert Anciaux, sp.a, Belgium 24. Rt Hon Michael Ancram, the Marquess of Lothian, Former Chairman of the Conservative Party, Conservative Party, United Kingdom 25. Karin Andersen, Socialist Left Party, Norway 26. Kirsten Normann Andersen, Socialist People’s Party (SF), Denmark 27. Theresa Berg Andersen, Socialist People’s Party (SF), Denmark 28. Rasmus Andresen, Greens/EFA, European Parliament (Germany) 29. Lord David Anderson of Ipswich QC, Crossbench, United Kingdom 30. Barry Andrews, Renew Europe, European Parliament (Ireland) 31. Chris Andrews, Sinn Féin, Ireland 32. Eric Andrieu, S&D, European Parliament (France) 33. -

One Nation: Power, Hope, Community

one nation power hope community power hope community Ed Miliband has set out his vision of One Nation: a country where everyone has a stake, prosperity is fairly shared, and we make a common life together. A group of Labour MPs, elected in 2010 and after, describe what this politics of national renewal means to them. It begins in the everyday life of work, family and local place. It is about the importance of having a sense of belonging and community, and sharing power and responsibility with people. It means reforming the state and the market in order to rebuild the economy, share power hope community prosperity, and end the living standards crisis. And it means doing politics in a different way: bottom up not top down, organising not managing. A new generation is changing Labour to change the country. Edited by Owen Smith and Rachael Reeves Contributors: Shabana Mahmood Rushanara Ali Catherine McKinnell Kate Green Gloria De Piero Lilian Greenwood Steve Reed Tristram Hunt Rachel Reeves Dan Jarvis Owen Smith Edited by Owen Smith and Rachel Reeves 9 781909 831001 1 ONE NATION power hope community Edited by Owen Smith & Rachel Reeves London 2013 3 First published 2013 Collection © the editors 2013 Individual articles © the author The authors have asserted their rights under the Copyright, Design and Patents Act, 1998 to be identified as authors of this work. All rights reserved. Apart from fair dealing for the purpose of private study, research, criticism or review, no part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, electrical, chemical, mechanical, optical, photocopying, recording or otherwise, without the prior permission of the copyright owner. -

Parliamentary Debates House of Commons Official Report General Committees

PARLIAMENTARY DEBATES HOUSE OF COMMONS OFFICIAL REPORT GENERAL COMMITTEES Public Bill Committee HEALTH AND SOCIAL CARE (RE-COMMITTED) BILL Eighth Sitting Thursday 7 July 2011 (Afternoon) CONTENTS Clause 55 agreed to. Schedule 8 agreed to. Clauses 56, 58, 59 and 63 agreed to, some with amendments. Adjourned till Tuesday 12 July at half-past Ten o’clock. PUBLISHED BY AUTHORITY OF THE HOUSE OF COMMONS LONDON – THE STATIONERY OFFICE LIMITED £5·00 PBC (Bill 177) 2010 - 2012 Members who wish to have copies of the Official Report of Proceedings in General Committees sent to them are requested to give notice to that effect at the Vote Office. No proofs can be supplied. Corrigenda slips may be published with Bound Volume editions. Corrigenda that Members suggest should be clearly marked in a copy of the report—not telephoned—and must be received in the Editor’s Room, House of Commons, not later than Monday 11 July 2011 STRICT ADHERENCE TO THIS ARRANGEMENT WILL GREATLY FACILITATE THE PROMPT PUBLICATION OF THE BOUND VOLUMES OF PROCEEDINGS IN GENERAL COMMITTEES © Parliamentary Copyright House of Commons 2011 This publication may be reproduced under the terms of the Parliamentary Click-Use Licence, available online through The National Archives website at www.nationalarchives.gov.uk/information-management/our-services/parliamentary-licence-information.htm Enquiries to The National Archives, Kew, Richmond, Surrey TW9 4DU; e-mail: [email protected] 331 Public Bill Committee7 JULY 2011 Health and Social Care 332 (Re-committed) Bill The Committee consisted of the following Members: Chairs: †MR ROGER GALE,MR MIKE HANCOCK,MR JIM HOOD,DR WILLIAM MCCREA † Abrahams, Debbie (Oldham East and Saddleworth) † Morris, Grahame M. -

View Questions Tabled on PDF File 0.16 MB

Published: Monday 5 July 2021 Questions tabled on Friday 2 July 2021 Includes questions tabled on earlier days which have been transferred. T Indicates a topical oral question. Members are selected by ballot to ask a Topical Question. † Indicates a Question not included in the random selection process but accepted because the quota for that day had not been filled. N Indicates a question for written answer on a named day under S.O. No. 22(4). [R] Indicates that a relevant interest has been declared. Questions for Answer on Monday 5 July Questions for Written Answer 1 N Angela Rayner (Ashton-under-Lyne): To ask the Chancellor of the Duchy of Lancaster and Minister for the Cabinet Office, what assessment he has made of the accuracy of the Prime Minister's Official Spokesperson's statement of 28 June 2021 on the conduct of ministerial government business through departmental email addresses. [Transferred] (24991) 2 Dr Matthew Offord (Hendon): To ask the Secretary of State for Business, Energy and Industrial Strategy, what assessment his Department has made of the potential merits of setting a target for onshore wind ahead of COP26. [Transferred] (25780) 3 Stephen Morgan (Portsmouth South): To ask the Secretary of State for Education, what steps he is taking to ensure that all children receive LGBTQ+ inclusive education. [Transferred] (25919) 4 Jim Shannon (Strangford): To ask the Secretary of State for International Trade, what recent progress has been made towards agreeing a trade deal with Australia. [Transferred] (25817) 5 Daisy Cooper (St Albans): To ask the Secretary of State for Health and Social Care, if he will offer reimbursements to the single cohort of speech and language therapy undergraduates who self-funded their degrees when starting university in September 2017 before Government funding was re-instated. -

Shadow Cabinet Meetings with Proprietors, Editors and Senior Media Executives

Shadow Cabinet Meetings 1 June 2015 – 31 May 2016 Shadow cabinet meetings with proprietors, editors and senior media executives. Andy Burnham MP Shadow Secretary of State’s meetings with proprietors, editors and senior media executives Date Name Location Purpose Nature of relationship* 26/06/2015 Alison Phillips, Editor, Roast, The General Professional Sunday People Floral Hall, discussion London, SE1 Peter Willis, Editor, 1TL Daily Mirror 15/07/2015 Lloyd Embley, Editor in J Sheekey General Professional Chief, Trinity Mirror Restaurant, discussion 28-32 Saint Peter Willis, Editor, Martin's Daily Mirror Court, London WC2N 4AL 16/07/2015 Kath Viner, Editor in King’s Place Guardian daily Professional Chief, Guardian conference 90 York Way meeting London N1 2AP 22/07/2015 Evgeny Lebedev, Private General Professional proprieter, address discussion Independent/Evening Standard 04/08/2015 Lloyd Embley, Editor in Grosvenor General Professional Chief, Trinity Mirror Hotel, 101 discussion Buckingham Palace Road, London SW1W 0SJ 16/05/2016 Eamonn O’Neal, Manchester General Professional Managing Editor, Evening Manchester Evening News, discussion News Mitchell Henry House, Hollinwood Avenue, Chadderton, Oldham OL9 8EF Other interaction between Shadow Secretary of State and proprietors, editors and senior media executives Date Name Location Purpose Nature of relationship* No such meetings Angela Eagle MP Shadow Secretary of State’s meetings with proprietors, editors and senior media executives Date Name Location Purpose Nature of relationship* No -

Environment Bill (Report Stage Decisions)

Report Stage: Wednesday 26 May 2021 Environment Bill (Report Stage Decisions) This document sets out the fate of each clause, schedule, amendment and new clause considered at report stage. A glossary with key terms can be found at the end of this document. NEW CLAUSES AND NEW SCHEDULES RELATING TO PART 6; AMENDMENTS TO PART 6; NEW CLAUSES AND NEW SCHEDULES RELATING TO PART 7; AMENDMENTS TO PART 7; NEW CLAUSES AND NEW SCHEDULES RELATING TO CLAUSES 132 TO 139; AMENDMENTS TO CLAUSES 132 TO 139 NEW CLAUSES AND NEW SCHEDULES RELATING TO PART 6 Secretary George Eustice Agreed to NC21 To move the following Clause— “Habitats Regulations: power to amend general duties (1) The Secretary of State may by regulations amend the Conservation of Habitats and Species Regulations 2017 (S.I. 2017/1012) (the “Habitats Regulations”), as they apply in relation to England, for the purposes in subsection (2). 5 (2) The purposes are—— (a) to require persons within regulation 9(1) of the Habitats Regulations to exercise functions to which that regulation applies— (i) to comply with requirements imposed by regulations 10 under this section, or (ii) to further objectives specified in regulations under this section, instead of exercising them to secure compliance with the requirements of the Directives; 15 (b) to require persons within regulation 9(3) of the Habitats Regulations, when exercising functions to which that regulation applies, to have regard to matters specified by regulations under this section instead of the requirements of the Directives. (3) The regulations may impose requirements, or specify objectives or 20 matters, relating to— (a) targets in respect of biodiversity set by regulations under section 1; 2 Wednesday 26 May 2021 REPORT STAGE (b) improvements to the natural environment which relate to biodiversity and are set out in an environmental improvement 25 plan. -

Members of the House of Commons December 2019 Diane ABBOTT MP

Members of the House of Commons December 2019 A Labour Conservative Diane ABBOTT MP Adam AFRIYIE MP Hackney North and Stoke Windsor Newington Labour Conservative Debbie ABRAHAMS MP Imran AHMAD-KHAN Oldham East and MP Saddleworth Wakefield Conservative Conservative Nigel ADAMS MP Nickie AIKEN MP Selby and Ainsty Cities of London and Westminster Conservative Conservative Bim AFOLAMI MP Peter ALDOUS MP Hitchin and Harpenden Waveney A Labour Labour Rushanara ALI MP Mike AMESBURY MP Bethnal Green and Bow Weaver Vale Labour Conservative Tahir ALI MP Sir David AMESS MP Birmingham, Hall Green Southend West Conservative Labour Lucy ALLAN MP Fleur ANDERSON MP Telford Putney Labour Conservative Dr Rosena ALLIN-KHAN Lee ANDERSON MP MP Ashfield Tooting Members of the House of Commons December 2019 A Conservative Conservative Stuart ANDERSON MP Edward ARGAR MP Wolverhampton South Charnwood West Conservative Labour Stuart ANDREW MP Jonathan ASHWORTH Pudsey MP Leicester South Conservative Conservative Caroline ANSELL MP Sarah ATHERTON MP Eastbourne Wrexham Labour Conservative Tonia ANTONIAZZI MP Victoria ATKINS MP Gower Louth and Horncastle B Conservative Conservative Gareth BACON MP Siobhan BAILLIE MP Orpington Stroud Conservative Conservative Richard BACON MP Duncan BAKER MP South Norfolk North Norfolk Conservative Conservative Kemi BADENOCH MP Steve BAKER MP Saffron Walden Wycombe Conservative Conservative Shaun BAILEY MP Harriett BALDWIN MP West Bromwich West West Worcestershire Members of the House of Commons December 2019 B Conservative Conservative -

Stephen Kinnock MP Aberav

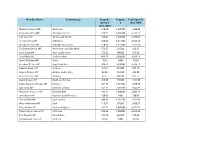

Member Name Constituency Bespoke Postage Total Spend £ Spend £ £ (Incl. VAT) (Incl. VAT) Stephen Kinnock MP Aberavon 318.43 1,220.00 1,538.43 Kirsty Blackman MP Aberdeen North 328.11 6,405.00 6,733.11 Neil Gray MP Airdrie and Shotts 436.97 1,670.00 2,106.97 Leo Docherty MP Aldershot 348.25 3,214.50 3,562.75 Wendy Morton MP Aldridge-Brownhills 220.33 1,535.00 1,755.33 Sir Graham Brady MP Altrincham and Sale West 173.37 225.00 398.37 Mark Tami MP Alyn and Deeside 176.28 700.00 876.28 Nigel Mills MP Amber Valley 489.19 3,050.00 3,539.19 Hywel Williams MP Arfon 18.84 0.00 18.84 Brendan O'Hara MP Argyll and Bute 834.12 5,930.00 6,764.12 Damian Green MP Ashford 32.18 525.00 557.18 Angela Rayner MP Ashton-under-Lyne 82.38 152.50 234.88 Victoria Prentis MP Banbury 67.17 805.00 872.17 David Duguid MP Banff and Buchan 279.65 915.00 1,194.65 Dame Margaret Hodge MP Barking 251.79 1,677.50 1,929.29 Dan Jarvis MP Barnsley Central 542.31 7,102.50 7,644.81 Stephanie Peacock MP Barnsley East 132.14 1,900.00 2,032.14 John Baron MP Basildon and Billericay 130.03 0.00 130.03 Maria Miller MP Basingstoke 209.83 1,187.50 1,397.33 Wera Hobhouse MP Bath 113.57 976.00 1,089.57 Tracy Brabin MP Batley and Spen 262.72 3,050.00 3,312.72 Marsha De Cordova MP Battersea 763.95 7,850.00 8,613.95 Bob Stewart MP Beckenham 157.19 562.50 719.69 Mohammad Yasin MP Bedford 43.34 0.00 43.34 Gavin Robinson MP Belfast East 0.00 0.00 0.00 Paul Maskey MP Belfast West 0.00 0.00 0.00 Neil Coyle MP Bermondsey and Old Southwark 1,114.18 7,622.50 8,736.68 John Lamont MP Berwickshire Roxburgh -

Edinburgh Research Explorer

Edinburgh Research Explorer The parrot is not dead, just resting Citation for published version: Harwood, S 2018 'The parrot is not dead, just resting: The UK universal credit system – An empirical narrative' University of Edinburgh Business School Working Paper Series, University of Edinburgh Business School, Edinburgh. Link: Link to publication record in Edinburgh Research Explorer Document Version: Publisher's PDF, also known as Version of record General rights Copyright for the publications made accessible via the Edinburgh Research Explorer is retained by the author(s) and / or other copyright owners and it is a condition of accessing these publications that users recognise and abide by the legal requirements associated with these rights. Take down policy The University of Edinburgh has made every reasonable effort to ensure that Edinburgh Research Explorer content complies with UK legislation. If you believe that the public display of this file breaches copyright please contact [email protected] providing details, and we will remove access to the work immediately and investigate your claim. Download date: 24. Sep. 2021 THE PARROT IS NOT DEAD, JUST RESTING: THE UK UNIVERSAL CREDIT SYSTEM – AN EMPIRICAL NARRATIVE RESEARCH PAPER Stephen A. Harwood, University of Edinburgh Business School, University of Edinburgh, UK., [email protected] January 2018 ABSTRACT This paper provides a descriptive account of the implementation of Universal Credit, a flagship project of the UK Government. This is a system designed to simply the existing complex that constitutes welfare support to the unemployed, those on low incomes and those unable to work. This study draws upon a range of material, in particular official documents and Government debates. -

Publication of the Law Commission’S Recommendations, and That Draft Must Be in a Form Which Would Implement All Those Recommendations

Committee Stage: Wednesday 19 May 2021 Police, Crime, Sentencing and Courts Bill (Amendment Paper) This document lists all amendments tabled to the Police, Crime, Sentencing and Courts Bill. Any withdrawn amendments are listed at the end of the document. The amendments are arranged in the order in which it is expected they will be decided. Amendments which will comply with the required notice period at their next appearance. Sarah Champion 2 Sarah Jones Clause 1, page 2, line 2, after “workforce,”, insert “including the impact of working with traumatised survivors on officers’ wellbeing and morale,” Member’s explanatory statement This amendment aims to ensure the police covenant report, when addressing the health and well- being of members and formers members of the police workforce, also addresses the specific impact working with traumatised survivors, such as survivors of child sexual abuse, has on officers’ wellbeing and morale. Stella Creasy 50 Clause 7, page 8, line 4, at end insert— “(3A)Specified authorities which are housing authorities must have particular regard to their housing duties when performing their duties under this section.” Stella Creasy 52 Clause 7, page 8, line 10, at end insert— “(d) each registered provider of social housing in the area.” 2 Wednesday 19 May 2021 COMMITTEE STAGE Stella Creasy 53 Clause 7, page 8, line 15, at end insert— “(d) each registered provider of social housing in the area.” Stella Creasy 51 Clause 8, page 9, line 11, at end insert— “(3A)Specified authorities which are housing authorities