World Bank Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SEF Assisted Schools (SAS)

Sindh Education Foundation, Govt. of Sindh SEF Assisted Schools (SAS) PRIMARY SCHOOLS (659) S. No. School Code Village Union Council Taluka District Operator Contact No. 1 NEWSAS204 Umer Chang 3 Badin Badin SHUMAILA ANJUM MEMON 0333-7349268 2 NEWSAS179 Sharif Abad Thari Matli Badin HAPE DEVELOPMENT & WELFARE ASSOCIATION 0300-2632131 3 NEWSAS178 Yasir Abad Thari Matli Badin HAPE DEVELOPMENT & WELFARE ASSOCIATION 0300-2632131 4 NEWSAS205 Haji Ramzan Khokhar UC-I MATLI Matli Badin ZEESHAN ABBASI 0300-3001894 5 NEWSAS177 Khan Wah Rajo Khanani Talhar Badin HAPE DEVELOPMENT & WELFARE ASSOCIATION 0300-2632131 6 NEWSAS206 Saboo Thebo SAEED PUR Talhar Badin ZEESHAN ABBASI 0300-3001894 7 NEWSAS175 Ahmedani Goth Khalifa Qasim Tando Bago Badin GREEN CRESCENT TRUST (GCT) 0304-2229329 8 NEWSAS176 Shadi Large Khoski Tando Bago Badin GREEN CRESCENT TRUST (GCT) 0304-2229329 9 NEWSAS349 Wapda Colony JOHI Johi Dadu KIFAYAT HUSSAIN JAMALI 0306-8590931 10 NEWSAS350 Mureed Dero Pat Gul Mohammad Johi Dadu Manzoor Ali Laghari 0334-2203478 11 NEWSAS215 Mureed Dero Mastoi Pat Gul Muhammad Johi Dadu TRANSFORMATION AND REFLECTION FOR RURAL DEVELOPMENT (TRD) 0334-0455333 12 NEWSAS212 Nabu Birahmani Pat Gul Muhammad Johi Dadu TRANSFORMATION & REFLECTION FOR RURAL DEVELOPMENT (TRD) 0334-0455333 13 NEWSAS216 Phullu Qambrani Pat Gul Muhammad Johi Dadu TRANSFORMATION AND REFLECTION FOR RURAL DEVELOPMENT (TRD) 0334-0455333 14 NEWSAS214 Shah Dan Pat Gul Muhammad Johi Dadu TRANSFORMATION AND REFLECTION FOR RURAL DEVELOPMENT (TRD) 0334-0455333 15 RBCS002 MOHAMMAD HASSAN RODNANI -

Covid-19 Emergency Response

COVID-19 EMERGENCY RESPONSE Daily Situation Report- April 16, 2020 Sindh Rural Support Organizaiton (SRSO) SRSO Complex, Shikarpur Road, Sukkur (Sindh), Pakistan, Ph.#: 071-56271820 Website: www.srso.org.pk Daily Situation Report All the cities of Sindh are locked down. Daily wagers faced much difficulties to meet their ends. In such a pandemic and lockdown situation poor people of the community cannot afford their basic needs of life. In this situation, the Community didn’t leave alone to the poor daily wagers and elderly people of their communities. SRSO through representatives of community institutions (CIs) and staff are responding COVID-19 emergency within its outreach areas through Community Savings, Ration and Vegetables Distribution, Linkages Development, Identification of deserving HHs, delivering awareness sessions on precautionary measures to fight COVID-19 and Registration of needy and poor families under the Govt. of Pakistan Ehsaas Emergency Cash Programme. Households and individuals are being supported with Cash, Ration and capitalizing LSO linkages for relief activities in their concerned areas. SRSO well trained human capital is engaged in Government relief activities through identification of deserving beneficiaries, distribution of ration bags, conducting awareness sessions on preventive measures to combat COVID-19 SRSO is also facilitating the Government of Sindh in the identification of deserving families and distribution of food items in most needy households. SRSO outreach and scale of response to COVID-19 outbreak -

Format for the Minutes of Monthly Review Meeting

MINUTES OF THE (10th ) MONTHLY REVIEW MEETING OF DISTRICT HYDERABAD Monthly Review Meeting (M.R.M) of District, Hyderabad for the Month of August, 2012 was held on 13.09.2012 at meeting Hall of Ex-Zila Nazim Office, Hyderabad. Written invitations to participate were sent to the Administrator/ DCO, the D.H.O, all Focal persons of Vertical Programs, District Population Officer i.e EPI, TB DOTS,MNCH, National Program, Malaria Control, Hepatitis, DHIS & DEWS, representatives WHO, all I/c Medical Officers/ FMOs/LHVs etc. List of Participants: S Sr. Names Designation Names Designation # 1. Mr. Mustafa Kamal Tagar DSM, PPHI 41 Dr. Shazia Zeeshan FMO 2. Dr. Ahmed Ali Talpur A: DHO 42 Dr. Anaila Soomro WMO 3. Dr. Qazi Rasheed Ahmed F.P, DHIS 43 Dr. Mumtaz Rajper FMO 4. Dr. Sono Khan Bhurgri T.H.O Hyd Rural 44 Dr. Neelofer Kazi FMO 5. Dr. M Ayoub Unar Dist: T.B Coor. 45 Dr. Rubina Sheikh SWMO 6. Dr. Naveed Ahmed Eye Specialist 46 Dr. Samira Tebani WMO 7. Dr. Shabum DDO 47 Dr. Yasir MO 8. Dr. Rafique Ahmed MO 48 Dr. Mehwish FMO 9. Dr. Ammnullah Ogahi SMO 49 Dr. Fareeda FMO 10. Dr. Azeem Shah SMO I/C 50 Dr. Shabnum Tunio FMO 11. Dr. A. Rahim Khatian SMO I/C 51 Dr. Liaquat Siyal MO 12. Dr. Raza Muhammad SMO I/C 52 Dr. Farzana Agha WMO 13. Dr. Muqadus Ali MO 53 Dr. Kapil Dev M O HQ 14. Dr. Khadim Hussain SMO / IC 54 Sanjar Kumar Asst. 15. Dr. Khalid Dawich MO I/C 55 Dr. -

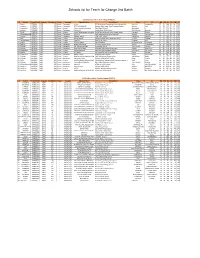

Schools List for Teach for Change 2Nd Batch

Schools list for Teach for Change 2nd Batch ESSP Schools List For Teach for Change (PHASE-II) S # District School Code Program Enrollment Phase Category Operator Name School Name Taluka UC ND NM NS ED EM ES 1 Sukkur ESSP0041 ESSP 435 Phase I Elementary Ali Bux REHMAN Model Computrized School Mubrak Pur. Pano Akil Mubarak Pur 27 40 288 69 19 729 2 Jamshoro ESSP0046 ESSP 363 Phase I Elementary RAZA MUHAMMAD Shaheed Rajib Anmol Free Education System Sehwan Arazi 26 28 132 67 47 667 3 Hyderabad ESSP0053 ESSP 450 Phase I Primary Free Journalist Foundation Zakia Model School Qasimabad 4 25 25 730 68 20 212 4 Khairpur ESSP0089 ESSP 476 Phase I Elementary Zulfiqar Ali Sachal Model Public School Thari Mirwah Kharirah 27 01 926 68 31 711 5 Ghotki ESSP0108 ESSP 491 Phase I Primary Lanjari Development foundation Sachal Sarmast model school dargahi arbani Khangarh Behtoor 27 49 553 69 20 705 6 ShaheedbenazirabaESSP0156 ESSP 201 Phase I Elementary Amir Bux Saath welfare public school (mashaik) Sakrand Gohram Mari 26 15 244 68 08 968 7 Khairpur ESSP0181 ESSP 294 Phase I Elementary Naseem Begum Faiza Public School Sobhodero Meerakh 27 15 283 68 20 911 8 Dadu ESSP0207 ESSP 338 Phase I Primary ghulam sarwar Danish Paradise New Elementary School Kn Shah Chandan 27 03 006 67 34 229 9 TandoAllahyar ESSP0306 ESSP 274 Phase I Primary Himat Ali New Vision School Chumber Jarki 25 24 009 68 49 275 10 Karachi ESSP0336 ESSP 303 Phase I Primary Kishwar Jabeen Mazin Academy Bin Qasim Twon Chowkandi 24 51 388 67 14 679 11 Sanghar ESSP0442 ESSP 589 Phase I Elementary -

Part-I: Post Code Directory of Delivery Post Offices

PART-I POST CODE DIRECTORY OF DELIVERY POST OFFICES POST CODE OF NAME OF DELIVERY POST OFFICE POST CODE ACCOUNT OFFICE PROVINCE ATTACHED BRANCH OFFICES ABAZAI 24550 Charsadda GPO Khyber Pakhtunkhwa 24551 ABBA KHEL 28440 Lakki Marwat GPO Khyber Pakhtunkhwa 28441 ABBAS PUR 12200 Rawalakot GPO Azad Kashmir 12201 ABBOTTABAD GPO 22010 Abbottabad GPO Khyber Pakhtunkhwa 22011 ABBOTTABAD PUBLIC SCHOOL 22030 Abbottabad GPO Khyber Pakhtunkhwa 22031 ABDUL GHAFOOR LEHRI 80820 Sibi GPO Balochistan 80821 ABDUL HAKIM 58180 Khanewal GPO Punjab 58181 ACHORI 16320 Skardu GPO Gilgit Baltistan 16321 ADAMJEE PAPER BOARD MILLS NOWSHERA 24170 Nowshera GPO Khyber Pakhtunkhwa 24171 ADDA GAMBEER 57460 Sahiwal GPO Punjab 57461 ADDA MIR ABBAS 28300 Bannu GPO Khyber Pakhtunkhwa 28301 ADHI KOT 41260 Khushab GPO Punjab 41261 ADHIAN 39060 Qila Sheikhupura GPO Punjab 39061 ADIL PUR 65080 Sukkur GPO Sindh 65081 ADOWAL 50730 Gujrat GPO Punjab 50731 ADRANA 49304 Jhelum GPO Punjab 49305 AFZAL PUR 10360 Mirpur GPO Azad Kashmir 10361 AGRA 66074 Khairpur GPO Sindh 66075 AGRICULTUR INSTITUTE NAWABSHAH 67230 Nawabshah GPO Sindh 67231 AHAMED PUR SIAL 35090 Jhang GPO Punjab 35091 AHATA FAROOQIA 47066 Wah Cantt. GPO Punjab 47067 AHDI 47750 Gujar Khan GPO Punjab 47751 AHMAD NAGAR 52070 Gujranwala GPO Punjab 52071 AHMAD PUR EAST 63350 Bahawalpur GPO Punjab 63351 AHMADOON 96100 Quetta GPO Balochistan 96101 AHMADPUR LAMA 64380 Rahimyar Khan GPO Punjab 64381 AHMED PUR 66040 Khairpur GPO Sindh 66041 AHMED PUR 40120 Sargodha GPO Punjab 40121 AHMEDWAL 95150 Quetta GPO Balochistan 95151 -

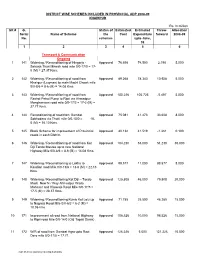

ADP 08-09 All Districts(CP-RAM)6/25/2004 Rs

DISTRICT WISE SCHEMES INCLUDED IN PROVINCIAL ADP 2008-09 KHAIRPUR Rs. In million SR # G. Status of Estimated Estimated Throw- Allocation Serial Name of Scheme the Cost Expenditure forward 2008-09 No. schemes upto June, 08 12 3456 Transport & Communication Ongoing 1 141 Widening / Reconditioning of Hingorja - Approved 76.698 74.500 2.198 5.000 Seharja Thari Mirwah road mile 0/0-17/0 = 17- 0 (M) = 27.37 Kms. 2 142 Widening / Reconditioning of road from Approved 89.268 78.340 10.928 5.000 Khairpur (Luqman) to main Machi Chowk mile 0/0-8/6 = 8-6 (M) = 14.08 Kms 3 143 Widening / Reconditioning of road from Approved 100.226 105.723 -5.497 5.000 Rashdi Petrol Pump to Ripri via Ahmedpur Manghanwari road mile 0/0-17/2 = 17-2 (M) = 27.77 Kms. 4 144 Reconditioning of road from Gambat Approved 75.081 41.473 33.608 8.000 Sobhodero via Thatti mile 0/0-10/0 = 10- 0 (M) = 16.10 Kms. 5 145 Block Scheme for improvement of Provincial Approved 40.138 41.519 -1.381 0.100 roads in each District. 6 146 Widening / Reconditioning of road from Kot Approved 104.230 53.000 51.230 30.000 Diji Tando Mastee up to new National Highway Mile 0/0-8/6 = 8-6 (M) = 14.08 Kms. 7 147 Widening / Reconditioning to Lakha to Approved 99.577 11.000 88.577 8.000 Kandiari road Mile 0/0-13/6 = 13-6 (M) = 22.13 Kms. 8 148 Widening / Reconditioning Kot Diji – Tando Approved 125.808 46.000 79.808 20.000 Masti New N / Way Ahmedpur Wada Mahasar and Khowaja Road Mile 0/0-17/5 = 17-5 (M) = 28.37 Kms. -

Budget Execution Report 2Nd QUARTER 2020-21

Budget Execution Report 2nd QUARTER 2020-21 31th December, 2020 Government of Sindh Finance Department Table of contents: Introduction ............................................................................................................................................................................. 2 Table 1 Interim Fiscal Statement .......................................................................................................................................... 3 Table 2 Revenue by Object .................................................................................................................................................... 4 Table 3 Revenue by Department........................................................................................................................................... 7 Table 4 Expenditure by Department .................................................................................................................................... 9 Table 5 Recurrent Expenditure by Department, Grant and Object ............................................................................... 20 Table 6 Provincial ADP by Sector and Sub-sector .......................................................................................................... 41 Table 7 Development Expenditure by Sector, Subsector and Scheme ....................................................................... 42 Table 8 Current Capital Expenditure ............................................................................................................................... -

PESA-DP-Sukkur-Sindh.Pdf

Landsowne Bridge, Sukkur “Disaster risk reduction has been a part of USAID’s work for decades. ……..we strive to do so in ways that better assess the threat of hazards, reduce losses, and ultimately protect and save more people during the next disaster.” Kasey Channell, Acting Director of the Disaster Response and Mitigation Division of USAID’s Office of U.S. Foreign Disas ter Ass istance (OFDA) PAKISTAN EMERGENCY SITUATIONAL ANALYSIS District Sukkur September 2014 “Disasters can be seen as often as predictable events, requiring forward planning which is integrated in to broader development programs.” Helen Clark, UNDP Administrator, Bureau of Crisis Preven on and Recovery. Annual Report 2011 Disclaimer iMMAP Pakistan is pleased to publish this district profile. The purpose of this profile is to promote public awareness, welfare, and safety while providing community and other related stakeholders, access to vital information for enhancing their disaster mitigation and response efforts. While iMMAP team has tried its best to provide proper source of information and ensure consistency in analyses within the given time limits; iMMAP shall not be held responsible for any inaccuracies that may be encountered. In any situation where the Official Public Records differs from the information provided in this district profile, the Official Public Records should take as precedence. iMMAP disclaims any responsibility and makes no representations or warranties as to the quality, accuracy, content, or completeness of any information contained in this report. Final assessment of accuracy and reliability of information is the responsibility of the user. iMMAP shall not be liable for damages of any nature whatsoever resulting from the use or misuse of information contained in this report. -

Government of Sindh Finance Department

2021-22 Finance Department Government of Sindh 1 SC12102(102) GOVERNOR'S SECRETARIAT/ HOUSE Rs Charged: ______________ Voted: 51,652,000 ______________ Total: 51,652,000 ______________ ____________________________________________________________________________________________ GOVERNOR'S SECRETARIAT ____________________________________________________________________________________________ BUILDINGS ____________________________________________________________________________________________ P./ADP DDO Functional-Cum-Object Classification & Budget NO. NO. Particular Of Scheme Estimates 2021 - 2022 ____________________________________________________________________________________________ Rs 01 GENERAL PUBLIC SERVICE 011 EXECUTIVE & LEGISLATIVE ORGANS, FINANCAL 0111 EXECUTIVE AND LEGISLATIVE ORGANS 011103 PROVINCIAL EXECUTIVE KQ5003 SECRETARY (GOVERNOR'S SECRETARIAT/ HOUSE) ADP No : 0733 KQ21221562 Constt. of Multi-storeyed Flats Phase-II at Sindh Governor's 51,652,000 House, Karachi (48 Nos.) including MT-s A12470 Others 51,652,000 _____________________________________________________________________________ Total Sub Sector BUILDINGS 51,652,000 _____________________________________________________________________________ TOTAL SECTOR GOVERNOR'S SECRETARIAT 51,652,000 _____________________________________________________________________________ 2 SC12104(104) SERVICES GENERAL ADMIN & COORDINATION Rs Charged: ______________ Voted: 1,432,976,000 ______________ Total: 1,432,976,000 ______________ _____________________________________________________________________________ -

National Assembly Polling Scheme

ELECTION COMMISSION OF PAKISTAN FORM 28 [See Rule 50] LIST OF POLLING STATIONS FOR A CONSTITUENCY Election to the National Assembly Sindh No. & Name of Constituency:- NA-208 Khairpur-I Number of Booths Number of Voters assigned In case of Rural areas In case of Urban Areas Serial No of assigned to Polling to Polling Stations voters on E Stations S.No. No. & Name of Polling Station A in case of Name of Electoral Census Block Name of Electoral Census Block bifurcation Male Female Total Male Female Total Area Code Area Code of EA 1 2 3 4 5 6 7 8 9 10 11 12 13 1 GPS Saleem Abad MC Khairpur 333040101 861 735 1596 2 2 4 MC Khairpur 333040106 861 735 1596 2 2 4 2 GPS Boys Faiz Abad Colony (Male) MC Khairpur 333040102 312 0 312 3 0 3 MC Khairpur 333040103 254 0 254 MC Khairpur 333040104 306 0 306 MC Khairpur 333040105 217 0 217 1089 0 1089 3 0 3 3 GGPS Faiz Abad Colony (Female) MC Khairpur 333040102 0 228 228 0 3 3 MC Khairpur 333040103 0 202 202 MC Khairpur 333040104 0 250 250 MC Khairpur 333040105 0 233 233 0 913 913 0 3 3 4 District Council Office Khairpur-I MC Khairpur 333040201 495 422 917 2 1 3 MC Khairpur 333040206 495 422 917 2 1 3 District Council Office Khairpur-II 5 MC Khairpur 333050405 1231 0 1231 4 0 4 (Male) MC Khairpur 333050410 Page 1 of 130 Number of Booths Number of Voters assigned In case of Rural areas In case of Urban Areas Serial No of assigned to Polling to Polling Stations voters on E Stations S.No. -

Khairpur, Sindh 5/3/1980 Matric 15/07/2014 Sheikh

Renewal List S/NO REN# / NAME FATHER'S PRESENT ADDRESS DATE OF ACADEMIC REN DATE NAME BIRTH QUALIFICATION 1 30738 NAIMAT ULLAH NASRULLAH P/O RIB MEHAR SHAH VIA KHUHRA , KHAIRPUR, SINDH 5/3/1980 MATRIC 15/07/2014 SHEIKH 2 25955 SHAMSHAD MATARO KHAN VILL MITHO MARI P/O KHANPUR TALUKA DISTT, 1-12- MATRIC 18/10/2014 ALI KHAIRPUR, KHAIRPUR, SINDH 1972 3 39041 ABDULLAH UMEED ALI GOTH KHAN PUR TEH, & DISTT, KHAIR PUR, KHAIRPUR, 23-11- MATRIC 20/10/2014 SINDH 1966 4 33075 SHAHIDA MUHAMMAD P/O BABARLO VILL. DUHOON IBRAHIMSHAH, 4/3/1979 MATRIC 28/10/2014 BANO BACHAL KHAIRPUR, SINDH 5 40550 SHOUKAT ALI KEWRO KHAN VILLAGE BULHARO P/O COAT TEH, KHAS , KHAIRPUR, 6-2-1983 MATRIC 15/1/2015 BURDI SINDH 6 36796 DULAHNO BODA RAM SABO DERO DISTT,, KHAIRPUR, SINDH 2-3-1955 MATRIC 2/4/2015 MAL KHEMANI 7 28616 YAR SHAMAN AL-FAQUEER HOMOEO STORE DARGHAROAD PIR JO 1-2-1979 FA 13/10/2015 MUHAMMAD CHANNA GOTH , KHAIRPUR, SINDH 8 49393 NASIM RAZA QASIM RAZA H-NO.1-A/34 BADA ALAM , KHAIRPUR, SINDH 18/1/1972 MATRIC 14/10/2015 SAYED 9 30746 HUBDAR ALI ALLAH DAD P/O LUQMAN JAN WERI MOH, AL FAZAL HOUSE 10-7- FA 19/11/2015 KHAIRPUR MIRS, KHAIRPUR, SINDH 1976 10 39949 MUHAMMAD ABDULLAH AZIZ DAWAKHANA RANIPUR., KHAIRPUR, SINDH 20/1/1940 30/12/2015 MALOOK 11 39037 ABDUL ABDUL RAZAK NEAR JAMILA MOSQUE LUQMAN MOH: MEMON , 1-4-1958 MATRIC 28/1/2016 JABBAR MEMON KHAIRPUR, SINDH MEMON 12 41770 ABDUL LATIF MUAHMMAD P.O.SETHARJA., KHAIRPUR, SINDH 15/8/1966 MATRIC 25/3/2016 SADIQ 13 41841 ABID HUSSAIN MUHAMMAD MOHSIN SHAH AGRICULTUR FARM SITHAJA 3-3-1987 MATRIC 28/3/2016 SARDAR -

ATC PROCLAIMED OFFENDFERS of DISTRICT KHAIRPUR. S.No Range District P.S FIR No Under Section Name of Accused Father's Name Residential Address CNIC NO

ATC PROCLAIMED OFFENDFERS OF DISTRICT KHAIRPUR. S.No Range District P.S FIR No Under Section Name of Accused Father's Name Residential Address CNIC NO. Date of PO 1 Sukkur Khairpur Shaheed SI Murtaza 198/2009 302-PPC Mir Muhammad Salam Shaikh Saleem Abad Khp - 12/11/2011 Meerani 2 Sukkur Khairpur Shaheed SI Murtaza 198/2009 302-PPC Bakhshal Salam Shaikh Saleem Abad Khp - 12/11/2011 Meerani 3 Sukkur Khairpur Shaheed SI Murtaza 198/2009 302-PPC Mumtaz Ali Rasool Bux Shaikh near Radi Station Muhala 45203- 12/11/2011 Meerani Saleem Abad 2689896-3 4 Sukkur Khairpur Shaheed SI Murtaza 198/2009 302-PPC Naseer Ahmed Muhammad Sharif near Therhi Phatak 45203- 12/11/2011 Meerani Shaikh Faizabad Khairpur 8782956-1 5 Sukkur Khairpur Shaheed SI Murtaza 198/2009 302-PPC Abdul Ghani Madad Ali Shaikh Imam Bux Shaikh, Faiz 45203- 12/11/2011 Meerani Abad Colony 4166858-3 6 Sukkur Khairpur Shaheed SI Murtaza 198/2009 302-PPC Khuda Bux @ Khuddu Miran Bux Jagirani Saleem Abad Khp. - 12/11/2011 Meerani 7 Sukkur Khairpur Shaheed SI Murtaza 198/2009 302-PPC Saeed Khan Ali Khan Phulpoto Saleem Abad Khp. - 12/11/2011 Meerani 8 Sukkur Khairpur Shaheed SI Murtaza 218/2009 302-PPC Mahmood Taj Muhammad village Lutuf Ali Jagirani, 45502- 4/11/2011 Meerani Jagrani Kandhar 4840434-7 9 Sukkur Khairpur Shaheed SI Murtaza 107/2013 324-384-387-PPC Qasim Asghar Mastoi Kangani Babarloi 04.06.2013 Meerani 10 Sukkur Khairpur Shaheed SI Murtaza 281/2013 341-147-506/ 2-PPC, 7- Haji Khan @ Bachal Phulpoto Village Raina Tehsil 45203- 14.02.2014 Meerani ATA Gh.Hussain Khairpur 9303132-9