Annual Report to the Legislature

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nebraska Farm Bureau Board Sets 2020 Agriculture Policy Priorities

www.nefb.org FEBRUARY/MARCH 2020 | VOL. 38 | ISSUE 1 FARM BUREAU NEWS 4 Trade Victories NEFB-PAC Friends 6 of Agriculture SWEET SIXTEEN YF&R Conference LEADERSHIP FINALIST 9 Success ACADEMY PAGE 8 INSIDE 10 Teacher of the Year PAGE 5 Nebraska Farm Bureau board sets 2020 agriculture policy priorities he Nebraska Farm Bureau Board of Directors has set the organization’s public policy priorities for 2020. Nebraska Farm Bureau’s state policy Nebraska Farm Bureau’s national policy TEach year the Board identifies priorities to guide the priority list for 2020 includes: priority list for 2020 includes: organization in its efforts to support Nebraska’s farm and l Reducing Nebraska’s overreliance on l Continuing to promote and work to expand international ranch families. property taxes and seeking a more markets for Nebraska agricultural products. “There are many issues that impact our farms and balanced system to fund education. l Ensuring federal regulations and federal programs work ranches. It’s no secret that when agriculture does well, our l Growing Nebraska’s livestock sector for farm and ranch families including: rural communities thrive, and our entire state benefits. To and value-added agriculture. l Appropriate allocation of federal assistance to expand that end, it’s imperative we focus on the areas where we l Expanding farm and ranch access broadband access in rural areas; can do the most good in helping our members be success- to high-quality broadband service l Protecting farmers’ access to modern farming technology, ful,” said Steve Nelson, Nebraska Farm Bureau president. statewide. veterinary medications and crop protection tools; Every policy issue Farm Bureau works on is connected in l Proactive engagement on both state l Proper implementation of renewable energy mandates; some way to helping members keep their operations viable water quality and quantity issues. -

April 26-29, 2021

UNICAMERAL UPDATE News published daily at Update.Legislature.ne.gov Vol. 44, Issue 17 / April 26 - 29, 2021 Corporate tax cut, Tax credit for private school other revenue measures advanced scholarship contributions, fter two days of discussion, child care stalls lawmakers gave first-round bill that A approval April 27 to a bill that would create includes several tax-related proposals, A a tax credit including a cut to Nebraska’s top scholarship program corporate income tax rate. for private school The Revenue Committee intro- students stalled on duced LB432 as a placeholder bill. A general file April 28 committee amendment would have after a failed cloture replaced it with the provisions of five motion. other bills heard by the committee LB364, intro- this session. duced by Elkhorn Omaha Sen. John Cavanaugh made Sen. Lou Ann a motion to divide the question and Linehan, would al- consider the various provisions as sepa- low individuals, rate amendments. The motion carried. passthrough entities, One amendment, adopted 30-7, estates, trusts and contained the provisions of LB680, corporations to claim introduced by Sen. Lou Ann Linehan a nonrefundable in- of Elkhorn. They would cut the state’s come tax credit of top corporate income tax rate to 6.84 up to 50 percent of percent — the same as the state’s top their state income individual income tax rate — begin- tax liability on con- ning Jan. 1, 2022. tributions they make Sen. Lou Ann Linehan said the proposed tax credit would incentiv- Corporations currently pay a state to nonprofit orga- ize donations to scholarship granting organizations, increasing the income tax rate of 5.58 percent on the nizations that grant number of low-income students who could attend private school. -

Introduction

1 INTRODUCTION At the 2017 Annual Meeting, the League of Women Voters of Nebraska voted to approve a Money in Politics study in Nebraska. Much has been written and researched nationally about the overall increase in campaign donations and “dark money” funneled through shadowy non-profit organizations; the LWVNE study focused on what, if any, of the nationally identified trends were also true in Nebraska. The League study was scoped down to the 2016 Nebraska State Legislature races to analyze: 1. To what extent can a winner be predicted based on the amount of money raised? 2. What did the source of donations play? 3. Was “dark money” a part of Nebraska’s political landscape? 4. How do Nebraska campaign finance laws compare to surrounding states? 5. What is the overall effect of Nebraska’s campaign finance laws on the Nebraska Unicameral? 6. Has the Governor gone too far in recruiting and financing Unicameral candidates? 7. How could Nebraska’s campaign finance laws be updated and improved? The League of Women Voters of Nebraska, a non-partisan non-profit organization, does not endorse, support or oppose candidates for office. The League of Women Voters takes positions on and advocates for issues particularly in the area of voting rights and protecting and promoting democracy. The League of Women Voters-US has a long-standing position on Money in Politics which can be summed up as: Elections should be about the voters not big money interests. This study will be used to develop the Nebraska League’s position statement. When this report is read on-line, links to the full data are enabled for readers who wish to see a full 50 state comparison or additional commentary. -

Revenue Hearing January 24, 2019

Transcript Prepared by Clerk of the Legislature Transcribers Office Revenue Committee January 24, 2019 LINEHAN: Welcome to the Revenue Committee public hearing. My name is Lou Ann Linehan. I'm from Elkhorn, Nebraska, and represent District 39, Legislative District 39, and serve as Chair of this committee. The committee will take up bills in the order posted. Our hearing today is your public part of the legislative process. This is your opportunity to express your position on the proposed legislation before us today. If you are unable to attend the public hearing and would like your position stated for the record, you must submit your written testimony by 5:00 p.m. the day prior to the hearings. Letters received after the cutoff will not be read into the record. No exceptions. To better facilitate today's proceeding, I ask that you provide by the following procedures. I'm gonna do this myself. Please turn off your cell phones and other electronic devices. And I want to emphasize this because it, I tried to say it yesterday but it didn't seem to work. If you want to testify on the bill that's up, move to the front so we have some-- because these go long and we want you all to have an opportunity speak. So if you're going to testify, please move forward. The order of the testimony is introducer, proponents, opponents, and neutral and closing remarks. If you will be testifying, please complete the green form and hand it to the committee clerk when you come up to testify. -

Session Review 2017 Volume XL, No

THE 105TH NEBRASKA LEGISLATURE FIRST SESSION Unicameral Update Session Review 2017 Volume XL, No. 21 2017 Session Review Contents Agriculture .......................................................................................... 1 Appropriations .................................................................................... 2 Banking, Commerce and Insurance .................................................. 4 Business and Labor ........................................................................... 6 Education ............................................................................................ 8 Executive Board ............................................................................... 11 General Affairs .................................................................................. 12 Government, Military and Veterans Affairs ...................................... 13 Health and Human Services ............................................................ 16 Judiciary ........................................................................................... 20 Natural Resources ............................................................................ 24 Retirement Systems ......................................................................... 26 Revenue ............................................................................................ 27 Transportation and Telecommunications ........................................ 30 Urban Affairs .................................................................................... -

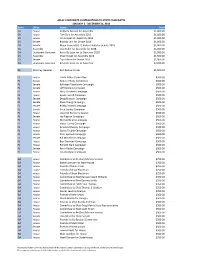

State Office Name Total CA House Anthony Rendon for Assembly

AFLAC CORPORATE CONTRIBUTIONS TO STATE CANDIDATES JANUARY 1 - DECEMBER 31, 2016 State Office Name Total CA House Anthony Rendon for Assembly $1,000.00 CA House Tom Daly for Assembly 2016 $1,000.00 CA House Jim Cooper for Assembly 2016 $1,000.00 CA Senate Ricardo Lara for Senate 2016 $1,000.00 CA Senate Major General (RET) Richard Roth for Senate 2016 $1,000.00 CA Assembly Jean Fuller for Assembly for 2018 $1,000.00 CA Lieutenant Governor Kevin De Leon for Lt. Governor 2018 $1,000.00 CA Assembly Chad Mayes for Assembly 2016 $1,500.00 CA Senate Toni Atkins for Senate 2016 $1,500.00 CA Lieutenant Governor Kevin De Leon for Lt. Governor $2,000.00 DC Attorney General Karl Racine for AG $1,500.00 FL House Frank Artiles Committee $500.00 FL Senate Anitere Flores Committee $500.00 FL Senate Kathleen Passidomo Campaign $500.00 FL Senate Jeff Clemens Campaign $500.00 FL House Holly Raschein Campaign $500.00 FL House Gayle Harrell Campaign $500.00 FL Senate Doug Broxson Campaign $500.00 FL Senate Dana Young Campaign $500.00 FL Senate Bobby Powell Campaign $500.00 FL Senate Greg Steube Campaign $500.00 FL House Jeanette Nunez Campaign $500.00 FL Senate Joe Negron Campaign $500.00 FL House Michael Bileca Campaign $500.00 FL House Victor Torres Campaign $500.00 FL House Amanda Murphy Campaign $500.00 FL House Carols Trujilio Campaign $500.00 FL House Chris Sprowls Campaign $500.00 FL Senate Bill Montford Campaign $500.00 FL House Ben Diamond Campaign $500.00 FL House Richard Stark Campaign $500.00 FL Senate Kevin Rader Campaign $500.00 FL House Jim Waldman Campaign $500.00 GA House Committee to Re-Elect Michele Henson $250.00 GA House Eddie Lumsden for State House $250.00 GA House Friends of David Casas $250.00 GA House Friends of Shaw Blackmon $250.00 GA House Friends of Shaw Blackmon $250.00 GA House Committee to Elect Earnest Coach Williams $350.00 GA House Committee to Elect Earnest Smith $350.00 GA House Committee to Elect Erica Thomas $350.00 GA House Committee to Elect Thomas S. -

![[LB737 LB771 LB778 LB857] the Committee on Education Met at 1](https://docslib.b-cdn.net/cover/4384/lb737-lb771-lb778-lb857-the-committee-on-education-met-at-1-2734384.webp)

[LB737 LB771 LB778 LB857] the Committee on Education Met at 1

Transcript Prepared By the Clerk of the Legislature Transcriber's Office Education Committee January 16, 2018 [LB737 LB771 LB778 LB857] The Committee on Education met at 1:30 p.m. on Tuesday, January 16, 2018, in Room 1525 of the State Capitol, Lincoln, Nebraska, for the purpose of conducting a public hearing on LB771, LB857, LB737, and LB778. Senators present: Mike Groene, Chairperson; Rick Kolowski, Vice Chairperson; Laura Ebke; Steve Erdman; Lou Ann Linehan; Adam Morfeld; Patty Pansing Brooks; and Lynne Walz. Senators absent: None. SENATOR GROENE: Thank you for attending. We'll start the first public hearing of the Education Committee. Sorry about being late. My clock in my office is the same as that one up there and it needs a new battery. So we will start with how we will operate the committee. Welcome to the Education Committee public hearing. My name is Mike Groene from Legislative District 42. I serve as the Chair of this committee. Committee will take up the bills in the posted agenda. Our hearing today is your public part of the legislative process. This is your opportunity to express your position on the proposed legislation before us today. You are the second house of the Legislature. To better facilitate today's proceedings, I ask that you abide by the following procedures. Please turn off cell phones and other electronic devices; move to the chairs at the front of the room when you are ready to testify. The order of testimony is introducer, proponents, opponents, neutral, and closing remarks. I will leave it open that if we have an awful...we ever have legislation that has a lot of testifiers, I will leave it that we can alternate to give everybody a chance to speak and both sides can be heard. -

Pfizer Inc. Regarding Congruency of Political Contributions on Behalf of Tara Health Foundation

SANFORD J. LEWIS, ATTORNEY January 28, 2021 Via electronic mail Office of Chief Counsel Division of Corporation Finance U.S. Securities and Exchange Commission 100 F Street, N.E. Washington, D.C. 20549 Re: Shareholder Proposal to Pfizer Inc. Regarding congruency of political contributions on Behalf of Tara Health Foundation Ladies and Gentlemen: Tara Health Foundation (the “Proponent”) is beneficial owner of common stock of Pfizer Inc. (the “Company”) and has submitted a shareholder proposal (the “Proposal”) to the Company. I have been asked by the Proponent to respond to the supplemental letter dated January 25, 2021 ("Supplemental Letter") sent to the Securities and Exchange Commission by Margaret M. Madden. A copy of this response letter is being emailed concurrently to Margaret M. Madden. The Company continues to assert that the proposal is substantially implemented. In essence, the Company’s original and supplemental letters imply that under the substantial implementation doctrine as the company understands it, shareholders are not entitled to make the request of this proposal for an annual examination of congruency, but that a simple written acknowledgment that Pfizer contributions will sometimes conflict with company values is all on this topic that investors are entitled to request through a shareholder proposal. The Supplemental letter makes much of the claim that the proposal does not seek reporting on “instances of incongruency” but rather on how Pfizer’s political and electioneering expenditures aligned during the preceding year against publicly stated company values and policies.” While the company has provided a blanket disclaimer of why its contributions may sometimes be incongruent, the proposal calls for an annual assessment of congruency. -

Pray for Our Leaders Today

Lifting Leaders to the Throne of God Lifting Leaders to the Throne of God I urge you that first of all intercession and thanksgiving be made for those in I urge you that first of all intercession and thanksgiving be made for those in authority so you might live peaceful and quiet lives. authority so you might live peaceful and quiet lives. II Timothy 2:1- 2 II Timothy 2:1- 2 Nebraska State Senators Nebraska State Senators Joni Albrecht Steve Halloran Adam Morfield Joni Albrecht Steve Halloran Adam Morfield Roy Baker Matt Hansen John Murante Roy Baker Matt Hansen John Murante Carol Blood Burke Harr Patty Pansing Brooks Carol Blood Burke Harr Patty Pansing Brooks Kate Bolz Mike Hilgers Dan Quick Kate Bolz Mike Hilgers Dan Quick Bruce Bostelman Robert Hilkeman Merv Riepe Bruce Bostelman Robert Hilkeman Merv Riepe Lydia Brasch Sara Howard Jim Scheer Lydia Brasch Sara Howard Jim Scheer Tom Brewer Dan Hughes Paul Schumacher Tom Brewer Dan Hughes Paul Schumacher Tom Briese Rick Kolowski Jim Smith Tom Briese Rick Kolowski Jim Smith Ernie Chambers Mark Kolterman John Stinner Ernie Chambers Mark Kolterman John Stinner Rob Clements Bob Krist Tony Vargas Rob Clements Bob Krist Tony Vargas Joni Craighead John Kuehn Dan Watermeier Joni Craighead John Kuehn Dan Watermeier Sue Crawford Tyson Larson Matt Williams Sue Crawford Tyson Larson Matt Williams Laura Ebke Brett Lindstrom Lynne M. Walz Laura Ebke Brett Lindstrom Lynne M. Walz Steve Erdman Lou Ann Linehan Justin Wayne Steve Erdman Lou Ann Linehan Justin Wayne Curt Friesen John S. Lowe Sr. Anna Wishart Curt Friesen John S. -

Vol. XLII, Issue 4: Jan. 28-Feb. 1, 2019

UNICAMERAL UPDATE News published daily at Update.Legislature.ne.gov Vol. 42, Issue 4 / Jan. 28 - Feb. 1, 2019 Civics exam for middle and Sales tax high schoolers proposed requirements for remote sellers considered he Revenue Committee heard testimony on three bills Jan. 31 T that would require out-of-state internet retailers to collect and remit state sales tax on purchases made by Nebraska residents. The U.S. Supreme Court ruled last June in South Dakota v. Wayfair that a state may require online retailers with- out a physical presence in the state to collect and remit state sales tax. In a July statement, the state De- partment of Revenue said remote Sen. Julie Slama said LB399 would ensure that Nebraska schools emphasize the teaching of sellers engaged in business in Ne- U.S. history and government. braska must, before Jan. 1, 2019, begin he Education Committee and assesses foundational knowledge collecting and remitting tax on sales heard testimony Jan. 29 on a in civics, history, economics, financial made to customers in Nebraska. The T bill intended to ensure civic literacy and geography.” department said it would administer competence among Nebraska stu- Additionally, the committee would the sales tax collection consistent with dents. ensure that the district administers the the court’s ruling, which upheld South Under current law, school boards 100-question civics portion of the U.S. Dakota’s exception for small retailers are required to appoint three members Citizenship and Immigration Services with sales of $100,000 or less or 200 or to a committee on Americanism, naturalization exam to students no fewer annual transactions in the state. -

Holland Children's Movement

Nebraska Legislature: How they Voted for the Early Advantage of Children in the 105th Legislature 1st Session 2017 Dear Nebraska Friends and Colleagues, July 2017 Holland Children’s Movement has put together a list of important legislative votes on proposals important to improving the lives of working families and their children. The selected votes in this issue are from the 2017 legislative session. These proposals were priorities of the Holland Children’s Movement as they relate to issues of access to quality health care, child care, education, and economic opportunity. We have included a percentage of each senator’s support of these priorities based on their votes on specific legislative measures for 2017 and cumulatively with their 2016 results. These voting records do not cover all legislative actions and proposals of interest to Nebraska children, such as committee votes or bills introduced. In that regard, we would like to commend Senators John Stinner and Jim Smith for removing language which would have suspended the School Readiness Tax Credits critical to raising quality standards. We also commend Senator Sue Crawford for introducing paid family and medical leave legislation and Senator Lynn Walz for introducing pre-K expansion legislation. We are pleased to report that nearly half of senators voted in support of the position of the Holland Children’s Movement 83% or more of the time. We extend our sincere appreciation to all our senators for their dedication to public service and our gratitude for the actions taken to protect Nebraska children and families in difficult financial times. The 2017 legislative session presented challenges, such as LB 461 which posed a direct threat to the future of quality health and education programs for years to come, and LB 335, which would have eliminated the use of a market rate survey to set child care subsidy rates. -

2020 Nebraska Lobbying Report.Pdf

Shucking the Bucks: Another Record Harvest for Nebraska’s Lobbyists Nebraska Lobbying Report 2020 Acknowledgments This report is funded by Nebraskans eager to reduce money’s influence in politics and government who expect the highest ethical standards from those who seek to serve the public. As members and supporters of Common Cause Nebraska, we work together across party lines to strengthen the people’s voice in our democracy. Additional support is provided by the Common Cause Education Fund, the research and public education affiliate of Common Cause and its 1.2 million supporters. Founded by John Gardner in 1970, Common Cause has helped everyday Americans exert their power by working together over the last 50 years. We create open, honest and accountable government that serves the public interest; promote equal rights, opportunities and representation for all; and empower all people to make their voices heard in the political process. Thanks to the Philip and Janice Levin Foundation for their ongoing dedication to re- searching, producing and distributing important educational information that the public needs. The Common Cause Education Fund is grateful to the Democracy Fund, the Arkay Foundation, and the Johnson Family Foundation for their support of our work toward reducing money’s influence in politics. Common Cause Nebraska board member and policy chair Jack Gould is the author of this report, and he wishes to thank the many people who helped research, compile, track, and make this data available to the public through this annual report: Common Cause Nebraska advisory board members and Gavin Geis, executive director; Karen Hobert Fly- nn Common Cause president, Scott Blaine Swenson, vice president of communications; Linda Boonyuen Owens, west region communications and multimedia strategist; Melissa Brown Levine for her command of language and copyediting gift; and Kerstin Vogdes Diehn of KV Design for helping readers focus on important content through good design.