Taxpayer Registration Starter Pack

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Republic of Uganda (Ministry of Works And

THE REPUBLIC OF UGANDA (MINISTRY OF WORKS AND TRANSPORT COMPONENT) IDA CREDIT NO.4147 UG REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF THE EAST AFRICA TRADE AND TRANSPORT FACILITATION PROJECT (EATTFP) FOR THE YEAR ENDED 30TH JUNE, 2015 OFFICE OF THE AUDITOR GENERAL UGANDA TABLE OF CONTENTS REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30TH JUNE 2015 ...................................................................................................................... iv REPORT OF THE AUDITOR GENERAL ON THE SPECIAL ACCOUNT OPERATIONS FOR THE YEAR ENDED 30TH JUNE 2015 ........................................................................................................... vi 1.0 INTRODUCTION ........................................................................................................................ 1 2.0 PROJECT BACKGROUND .......................................................................................................... 1 3.0 PROJECT OBJECTIVES AND COMPONENTS .......................................................................... 1 4.0 AUDIT OBJECTIVES .................................................................................................................. 2 5.0 AUDIT PROCEDURES PERFORMED ........................................................................................ 3 6.0 CATEGORIZATION AND SUMMARY OF FINDINGS ............................................................... 4 6.2 Summary of Findings ............................................................................................................... -

COVID-19 Interventions Report Financial Year 2019/20

COVID-19 Interventions Report Financial Year 2019/20 October 2020 Budget Monitoring and Accountability Unit (BMAU) Ministry of Finance, Planning and Economic Development P.O. Box 8147, Kampala www.finance.go.ug Table of Contents 1.0 Introduction .......................................................................................................................... 1 1.1 Methodology .................................................................................................................... 1 2.0 Sector Performance .............................................................................................................. 2 2.1Agriculture Sector ............................................................................................................. 2 2.2 Education and Sports Sector ............................................................................................ 2 2.3 Health Sector .................................................................................................................... 7 2.3.1 Financial Performance................................................................................................... 7 2.3.2 Overall performance ...................................................................................................... 9 2.3.3 Detailed Performance by output for GoU Support........................................................ 9 2.3.4 Contingency Emergency Response Component (CERC) towards COVID-19 by the World Bank .......................................................................................................................... -

STATEMENT by H.E. Yoweri Kaguta Museveni President of the Republic

STATEMENT by H.E. Yoweri Kaguta Museveni President of the Republic of Uganda At The Annual Budget Conference - Financial Year 2016/17 For Ministers, Ministers of State, Head of Public Agencies and Representatives of Local Governments November11, 2015 - UICC Serena 1 H.E. Vice President Edward Ssekandi, Prime Minister, Rt. Hon. Ruhakana Rugunda, I was informed that there is a Budgeting Conference going on in Kampala. My campaign schedule does not permit me to attend that conference. I will, instead, put my views on paper regarding the next cycle of budgeting. As you know, I always emphasize prioritization in budgeting. Since 2006, when the Statistics House Conference by the Cabinet and the NRM Caucus agreed on prioritization, you have seen the impact. Using the Uganda Government money, since 2006, we have either partially or wholly funded the reconstruction, rehabilitation of the following roads: Matugga-Semuto-Kapeeka (41kms); Gayaza-Zirobwe (30km); Kabale-Kisoro-Bunagana/Kyanika (101 km); Fort Portal- Bundibugyo-Lamia (103km); Busega-Mityana (57km); Kampala –Kalerwe (1.5km); Kalerwe-Gayaza (13km); Bugiri- Malaba/Busia (82km); Kampala-Masaka-Mbarara (416km); Mbarara-Ntungamo-Katuna (124km); Gulu-Atiak (74km); Hoima-Kaiso-Tonya (92km); Jinja-Mukono (52km); Jinja- Kamuli (58km); Kawempe-Kafu (166km); Mbarara-Kikagati- Murongo Bridge (74km); Nyakahita-Kazo-Ibanda-Kamwenge (143km); Tororo-Mbale-Soroti (152km); Vurra-Arua-Koboko- Oraba (92km). 2 We are also, either planning or are in the process of constructing, re-constructing or rehabilitating -

Vote:781 Kira Municipal Council Quarter1

Local Government Quarterly Performance Report FY 2017/18 Vote:781 Kira Municipal Council Quarter1 Terms and Conditions I hereby submit Quarter 1 performance progress report. This is in accordance with Paragraph 8 of the letter appointing me as an Accounting Officer for Vote:781 Kira Municipal Council for FY 2017/18. I confirm that the information provided in this report represents the actual performance achieved by the Local Government for the period under review. Name and Signature: Accounting Officer, Kira Municipal Council Date: 27/08/2019 cc. The LCV Chairperson (District) / The Mayor (Municipality) 1 Local Government Quarterly Performance Report FY 2017/18 Vote:781 Kira Municipal Council Quarter1 Summary: Overview of Revenues and Expenditures Overall Revenue Performance Ushs Thousands Approved Budget Cumulative Receipts % of Budget Received Locally Raised Revenues 7,511,400 1,237,037 16% Discretionary Government Transfers 2,214,269 570,758 26% Conditional Government Transfers 4,546,144 1,390,439 31% Other Government Transfers 0 308,889 0% Donor Funding 0 0 0% Total Revenues shares 14,271,813 3,507,123 25% Overall Expenditure Performance by Workplan Ushs Thousands Approved Cumulative Cumulative % Budget % Budget % Releases Budget Releases Expenditure Released Spent Spent Planning 298,531 40,580 12,950 14% 4% 32% Internal Audit 110,435 15,608 10,074 14% 9% 65% Administration 1,423,810 356,949 150,213 25% 11% 42% Finance 1,737,355 147,433 58,738 8% 3% 40% Statutory Bodies 1,105,035 225,198 222,244 20% 20% 99% Production and Marketing -

The Informal Cross Border Trade Qualitative Baseline Study 2008 Uganda Bureau of Statistics

UGANDA BUREAU OF STATISTICS THE INFORMAL CROSS BORDER TRADE QUALIT ATIVE BASELINE STUDY 2008 February 2009 FOREWORD The Qualitative Module of the Informal Cross Border Trade (ICBT) Survey is the first comprehensive Study of its kind to be conducted in Uganda to bridge information gaps regarding informal trade environment. The study was carried out at Busia, Mirama Hills, Mpondwe and Mutukula border posts. The ICBT Qualitative study collected information on informal trade environment and the constraints traders’ experience in order to guide policy formulation, planning and decision making in the informal cross border sub-sector. The study focused specifically on gender roles in ICBT, access to financial services, marketing information, food security, and tariff and non-tariff barriers to trade among others. This study was conducted alongside the ICBT Quantitative Module that collected information on the nature of products transacted, their volumes and value, and, the direction of trade. Notwithstanding the significant contribution informal cross border trade has made to the welfare of the people of the East African region (in terms of employment creation, economic empowerment of women, food security, regional and social integration), there are no appropriate policies designed to guide players in the informal trade sector. The information gathered, therefore, will provide an insight into the challenges informal traders face in their day to day business and will guide policy and decision makers to enact appropriate policies to harness the potential benefits of informal cross border trade. The Bureau is grateful to the Integrated Framework (IF) through TRACE Project of the Ministry of Tourism, Trade and Industry for the financial contribution that facilitated the study. -

List of URA Service Offices Callcenter Toll Free Line: 0800117000 Email: [email protected] Facebook: @Urapage Twitter: @Urauganda

List of URA Service Offices Callcenter Toll free line: 0800117000 Email: [email protected] Facebook: @URApage Twitter: @URAuganda CENTRAL REGION ( Kampala, Wakiso, Entebbe, Mukono) s/n Station Location Tax Heads URA Head URA Tower , plot M 193/4 Nakawa Industrial Ara, 1 Domestic Taxes/Customs Office P.O. Box 7279, Kampala 2 Katwe Branch Finance Trust Bank, Plot No 115 & 121. Domestic Taxes 3 Bwaise Branch Diamond Trust Bank,Bombo Road Domestic Taxes 4 William Street Post Bank, Plot 68/70 Domestic Taxes Nakivubo 5 Diamond Trust Bank,Ham Shopping Domestic Taxes Branch United Bank of Africa- Aponye Hotel Building Plot 6 William Street Domestic Taxes 17 7 Kampala Road Diamond Trust Building opposite Cham Towers Domestic Taxes 8 Mukono Mukono T.C Domestic Taxes 9 Entebbe Entebbe Kitooro Domestic Taxes 10 Entebbe Entebbe Arrivals section, Airport Customs Nansana T.C, Katonda ya bigera House Block 203 11 Nansana Domestic Taxes Nansana Hoima road Plot 125; Next to new police station 12 Natete Domestic Taxes Natete Birus Mall Plot 1667; KyaliwajalaNamugongoKira Road - 13 Kyaliwajala Domestic Taxes Martyrs Mall. NORTHERN REGION ( East Nile and West Nile) s/n Station Location Tax Heads 1 Vurra Vurra (UG/DRC-Border) Customs 2 Pakwach Pakwach TC Customs 3 Goli Goli (UG/DRC- Border) Customs 4 Padea Padea (UG/DRC- Border) Customs 5 Lia Lia (UG/DRC - Border) Customs 6 Oraba Oraba (UG/S Sudan-Border) Customs 7 Afogi Afogi (UG/S Sudan – Border) Customs 8 Elegu Elegu (UG/S Sudan – Border) Customs 9 Madi-opei Kitgum S/Sudan - Border Customs 10 Kamdini Corner -

Mogondo Julius Wondero EOEIYE

d/ TELEPHONES: 04L434OLO0l4340LL2 Minister of State for East E.MAIL: [email protected] African Community Affairs TELEFAX: o4t4-348r7t 1't Floor, Postal Building Yusuf Lule Road ln any correspondence on this subject P.O. Box 7343, Kampala please quote No: ADM 542/583/01 UGANDA rHE REPUBLIC OF UGANDA 22"4 August,2Ol9 FTHES P ( L \-, 4 Hon. Oumo George Abott U Choirperson, Committee for 2019 * 2 3 AUG s Eost Africon Community Affoirs Porlioment of Ugondo EOEIYE L t4 raE \, \, KAMPATA NT OF CLOSURE OF UGANDA.RWANDA BORDERS Reference is mode to letter AB: I 171287 /01 doted l5rn August,20l9 oddressed to the Minister of Eost Africon Community Affoirs ond copied to the Permonent Secretory, Ministry of Eost Africon Community Affoirs regording the obove subject motter. ln the letter, you invited the Ministry to updote the EAC Committee on the progress mode to hondle the Closure of Ugondo-Rwondo Borders on Ihursdoy,29r,August, 2019 at 10.00om. As stoted this discussion would help ensure thot the Eost Africon Common Morket Protocol is effectively implemented for the benefit of Ugondo ond other Portner Stofes. The Purpose of this letter therefore, is to forword to you o Report on the Stotus of the obove issue for further guidonce during our interoction with the committee ond to re-offirm our ottendonce os per the stipuloted dote ond time Mogondo Julius Wondero MINISTER OF STATE FOR EAST AFRICAN COMMUNITY AFFAIRS C.C. The Speoker, Porlioment of Ugondo, Kompolo The Clerk to Porlioment, Porlioment of Ugondo, Kompolo Permonent Secretory, Ministry of Eost Africon Community Affoirs MINISTRY OF EAST AFRICAN COMMUNITY AFFAIRS REPORT ON THE CLOSURE OF UGANDA. -

Agent Id Agent Name Actual Location 100375 Annonceur Limited Near Centenary Kawuku, Entebbe Road 101286 Aiyun Investments Ltd Ab

ABAITA Agent Id Agent Name Actual location 100375 Annonceur Limited Near Centenary Kawuku, Entebbe Road 101286 Aiyun Investments Ltd Abaita town near Barclays Branch(Buy&Save Supermarket) 101626 S And S Enterprises Abaita S And S Enterprises Abaita (S and S Mall) 101635 Ferguson Enterprises Ltd Ferguson Ent Ltd Kawuku 101627 S And S Enterprises Nkumba 1 Nkumba 1 ACACIA Agent Id Agent Name Actual location 100480 Gn Associates Kamwokya Kanjokya Street ARUA Agent Id Agent Name Actual location 100653 Abiriga Hassan Ent Arua Town Arua town council 101278 Equata Tobacco Arua Adumi road , Arua 101763 Destiny Chain Traders Arua-Pakwach Road, opposite NN Toyota. 101942 Virah Forex Bureau (U) Limited Amuru Arua Arua 100661 Abiriga Hassan Ent Koboko koboko town council 100662 Abiriga Hassan Ent Yumbe Yumbe trading centre BUGOLOBI Agent Id Agent Name Actual location 100310 Shell Portbell Road Luzira Mbuya mutungo juction 100479 Valley Hostels,Nakawa Akamwesi hostel, nakawa 100611 Kacerere Inv Nakawa Behind Akamwesi hostel nakawa 100711 Kankan Builders Industrial A Sadolin shop industrial area 100842 Jackato Enterprises Middle east zone luthuli rise street bugolobi 100862 Kingdom Services Kinawataka kinawataka trading centre 101003 Nik Tel Traders Portbel Akamwesi hostel, nakawa 101904 Holy Mark hospitality services Plot 13 Kataza Close Maria House Nakawa 102043 Namukasa Hamidah Enterprises Mutungo Kunya opposite Jay Hotel 102044 Kayondo Denis Traders Mutungo Kunya opposite Jay Hotel 102045 Adot Telecom Mutungo Kunya opposite Muggiez 102046 Mujjunga Joseph Retailers Upper Bbina Luzira, Nakawa Division 102114 Riscom Limited Kunya Bina Road Mutungo after Muggiez 102126 Gok And Sons General Enterprises Mutungo Zone 1-7 close to Cielo Diners 102127 Akello Caroline Enterprises Kitintale Trading Centre close Comfort Zone 102280 Uwera Tracy And Family Busines Kinawataka Mbuya Nakawa opposite Mango Tree Shade CSC Agent Id Agent Name Actual location 101300 Honghai International Co. -

LG Budget Estimates 201213 Wakiso.Pdf

Local Government Budget Estimates Vote: 555 Wakiso District Structure of Budget Estimates A: Overview of Revenues and Expenditures B: Detailed Estimates of Revenue C: Detailed Estimates of Expenditure D: Status of Arrears Page 1 Local Government Budget Estimates Vote: 555 Wakiso District A: Overview of Revenues and Expenditures Revenue Performance and Plans 2011/12 2012/13 Approved Budget Receipts by End Approved Budget June UShs 000's 1. Locally Raised Revenues 3,737,767 3,177,703 7,413,823 2a. Discretionary Government Transfers 5,373,311 4,952,624 5,648,166 2b. Conditional Government Transfers 28,713,079 27,512,936 32,601,298 2c. Other Government Transfers 6,853,215 4,532,570 10,697,450 3. Local Development Grant 1,757,586 1,949,046 1,756,183 Total Revenues 46,434,958 42,124,880 58,116,921 Expenditure Performance and Plans 2011/12 2012/13 Approved Budget Actual Approved Budget Expenditure by UShs 000's end of June 1a Administration 1,427,411 1,331,440 3,894,714 1b Multi-sectoral Transfers to LLGs 5,459,820 4,818,229 0 2 Finance 679,520 658,550 2,623,938 3 Statutory Bodies 1,017,337 885,126 1,981,617 4 Production and Marketing 3,060,260 3,015,477 3,522,157 5 Health 4,877,837 4,807,510 6,201,655 6 Education 21,144,765 19,753,179 24,948,712 7a Roads and Engineering 6,161,280 4,538,877 11,151,699 7b Water 802,836 631,193 1,063,321 8 Natural Resources 427,251 238,655 659,113 9 Community Based Services 610,472 678,202 1,175,071 10 Planning 630,334 302,574 560,032 11 Internal Audit 135,835 117,414 334,893 Grand Total 46,434,958 41,776,425 58,116,922 Wage Rec't: 22,456,951 21,702,872 24,924,778 Non Wage Rec't: 16,062,717 13,930,979 23,191,011 Domestic Dev't 7,915,291 6,142,574 10,001,133 Donor Dev't 0 0 0 Page 2 Local Government Budget Estimates Vote: 555 Wakiso District B: Detailed Estimates of Revenue 2011/12 2012/13 Approved Budget Receipts by End Approved Budget of June UShs 000's 1. -

Vote:781 Kira Municipal Council Quarter2

Local Government Quarterly Performance Report FY 2018/19 Vote:781 Kira Municipal Council Quarter2 Terms and Conditions I hereby submit Quarter 2 performance progress report. This is in accordance with Paragraph 8 of the letter appointing me as an Accounting Officer for Vote:781 Kira Municipal Council for FY 2018/19. I confirm that the information provided in this report represents the actual performance achieved by the Local Government for the period under review. Name and Signature: Accounting Officer, Kira Municipal Council Date: 24/01/2019 cc. The LCV Chairperson (District) / The Mayor (Municipality) 1 Local Government Quarterly Performance Report FY 2018/19 Vote:781 Kira Municipal Council Quarter2 Summary: Overview of Revenues and Expenditures Overall Revenue Performance Ushs Thousands Approved Budget Cumulative Receipts % of Budget Received Locally Raised Revenues 6,177,725 3,467,321 56% Discretionary Government Transfers 2,130,791 1,182,235 55% Conditional Government Transfers 5,982,048 2,899,735 48% Other Government Transfers 3,356,981 1,247,294 37% Donor Funding 280,000 32,370 12% Total Revenues shares 17,927,545 8,828,955 49% Overall Expenditure Performance by Workplan Ushs Thousands Approved Cumulative Cumulative % Budget % Budget % Releases Budget Releases Expenditure Released Spent Spent Planning 185,173 105,514 73,428 57% 40% 70% Internal Audit 102,947 46,004 44,248 45% 43% 96% Administration 1,542,634 1,004,160 782,571 65% 51% 78% Finance 1,378,790 867,332 728,057 63% 53% 84% Statutory Bodies 671,770 452,301 385,332 67% 57% -

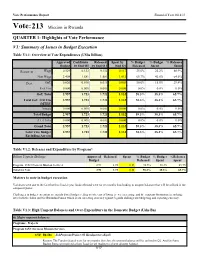

Vote:213 Mission in Rwanda

Vote Performance Report Financial Year 2018/19 Vote:213 Mission in Rwanda QUARTER 1: Highlights of Vote Performance V1: Summary of Issues in Budget Execution Table V1.1: Overview of Vote Expenditures (UShs Billion) Approved Cashlimits Released Spent by % Budget % Budget % Releases Budget by End Q1 by End Q 1 End Q1 Released Spent Spent Recurrent Wage 0.529 0.132 0.132 0.117 25.0% 22.2% 88.9% Non Wage 2.408 1.581 1.581 1.012 65.7% 42.0% 64.0% Devt. GoU 0.020 0.010 0.010 0.003 50.0% 15.0% 29.4% Ext. Fin. 0.000 0.000 0.000 0.000 0.0% 0.0% 0.0% GoU Total 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% Total GoU+Ext Fin 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% (MTEF) Arrears 0.000 0.000 0.000 0.000 0.0% 0.0% 0.0% Total Budget 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% A.I.A Total 0.000 0.000 0.000 0.000 0.0% 0.0% 0.0% Grand Total 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% Total Vote Budget 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% Excluding Arrears Table V1.2: Releases and Expenditure by Program* Billion Uganda Shillings Approved Released Spent % Budget % Budget %Releases Budget Released Spent Spent Program: 1652 Overseas Mission Services 2.96 1.72 1.13 58.3% 38.3% 65.7% Total for Vote 2.96 1.72 1.13 58.3% 38.3% 65.7% Matters to note in budget execution Variances were due to the fact that this finacial year funds released were for six months thus leading to unspent balances that will be utilised in the subquent Quater. -

The Uganda Gazette, General Notice No. 425 of 2021

LOCAL GOVERNMENT COUNCIL ELECTIONS, 2021 SCHEDULE OF ELECTION RESULTS FOR DISTRICT/CITY DIRECTLY ELECTED COUNCILLORS DISTRICT CONSTITUENCY ELECTORAL AREA SURNAME OTHER NAME PARTY VOTES STATUS ABIM LABWOR COUNTY ABIM KIYINGI OBIA BENARD INDEPENDENT 693 ABIM LABWOR COUNTY ABIM OMWONY ISAAC INNOCENT NRM 662 ABIM LABWOR COUNTY ABIM TOWN COUNCIL OKELLO GODFREY NRM 1,093 ABIM LABWOR COUNTY ABIM TOWN COUNCIL OWINY GORDON OBIN FDC 328 ABIM LABWOR COUNTY ABUK TOWN COUNCIL OGWANG JOHN MIKE INDEPENDENT 31 ABIM LABWOR COUNTY ABUK TOWN COUNCIL OKAWA KAKAS MOSES INDEPENDENT 14 ABIM LABWOR COUNTY ABUK TOWN COUNCIL OTOKE EMMANUEL GEORGE NRM 338 ABIM LABWOR COUNTY ALEREK OKECH GODFREY NRM Unopposed ABIM LABWOR COUNTY ALEREK TOWN COUNCIL OWINY PAUL ARTHUR NRM Unopposed ABIM LABWOR COUNTY ATUNGA ABALLA BENARD NRM 564 ABIM LABWOR COUNTY ATUNGA OKECH RICHARD INDEPENDENT 994 ABIM LABWOR COUNTY AWACH ODYEK SIMON PETER INDEPENDENT 458 ABIM LABWOR COUNTY AWACH OKELLO JOHN BOSCO NRM 1,237 ABIM LABWOR COUNTY CAMKOK ALOYO BEATRICE GLADIES NRM 163 ABIM LABWOR COUNTY CAMKOK OBANGAKENE POPE PAUL INDEPENDENT 15 ABIM LABWOR COUNTY KIRU TOWN COUNCIL ABURA CHARLES PHILIPS NRM 823 ABIM LABWOR COUNTY KIRU TOWN COUNCIL OCHIENG JOSEPH ANYING UPC 404 ABIM LABWOR COUNTY LOTUKEI OBUA TOM INDEPENDENT 146 ABIM LABWOR COUNTY LOTUKEI OGWANG GODWIN NRM 182 ABIM LABWOR COUNTY LOTUKEI OKELLO BISMARCK INNOCENT INDEPENDENT 356 ABIM LABWOR COUNTY MAGAMAGA OTHII CHARLES GORDON NRM Unopposed ABIM LABWOR COUNTY MORULEM OKELLO GEORGE ROBERT NRM 755 ABIM LABWOR COUNTY MORULEM OKELLO MUKASA