Q3 FY17 Investor Update a Journey of 27 Years…

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SNO APP.No Name Contact Address Reason 1 AP-1 K

SNO APP.No Name Contact Address Reason 1 AP-1 K. Pandeeswaran No.2/545, Then Colony, Vilampatti Post, Intercaste Marriage certificate not enclosed Sivakasi, Virudhunagar – 626 124 2 AP-2 P. Karthigai Selvi No.2/545, Then Colony, Vilampatti Post, Only one ID proof attached. Sivakasi, Virudhunagar – 626 124 3 AP-8 N. Esakkiappan No.37/45E, Nandhagopalapuram, Above age Thoothukudi – 628 002. 4 AP-25 M. Dinesh No.4/133, Kothamalai Road,Vadaku Only one ID proof attached. Street,Vadugam Post,Rasipuram Taluk, Namakkal – 637 407. 5 AP-26 K. Venkatesh No.4/47, Kettupatti, Only one ID proof attached. Dokkupodhanahalli, Dharmapuri – 636 807. 6 AP-28 P. Manipandi 1stStreet, 24thWard, Self attestation not found in the enclosures Sivaji Nagar, and photo Theni – 625 531. 7 AP-49 K. Sobanbabu No.10/4, T.K.Garden, 3rdStreet, Korukkupet, Self attestation not found in the enclosures Chennai – 600 021. and photo 8 AP-58 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Community Certificate Wrongly enclosed Pondicherry – 605 007. 9 AP-60 V.A.Kishor Kumar No.19, Thilagar nagar, Ist st, Kaladipet, Only one ID proof attached. Thiruvottiyur, Chennai -600 019 10 AP-61 D.Anbalagan No.8/171, Church Street, Only one ID proof attached. Komathimuthupuram Post, Panaiyoor(via) Changarankovil Taluk, Tirunelveli, 627 761. 11 AP-64 S. Arun kannan No. 15D, Poonga Nagar, Kaladipet, Only one ID proof attached. Thiruvottiyur, Ch – 600 019 12 AP-69 K. Lavanya Priyadharshini No, 35, A Block, Nochi Nagar, Mylapore, Only one ID proof attached. Chennai – 600 004 13 AP-70 G. -

KRISHNAGIRI Name Mobile Telephone Products Address Place

KRISHNAGIRI Name Mobile Telephone Products Address Place ANBU AGRO 9443082177 ALL PESTICIDES 1/164, KUPPAM MAIN ROAD VARATTANAPALLI AGENCIES VLN AGRO SERVICE 9787076629 ALL PESTICIDES 1/174, BUS STAND VARATTANAPALLI SARADHA AGRO 9443205874 9443205874 all pesticides 4, KALLAVI ROAD POCHAMBALLI ENGINEERING SERVICE ILAVARSU TRADERS 9443308616 9443308616 all pesticides 1/223-A, SANTHUR ROAD POCHAMBALLI JAYAM AGRO 9787097312 9787097312 all pesticides 490, ARASAM PATTI ROAD, BARUR, POCHAMBALLI SERVICE ARUNA AGRO 9865543401 9865543401 all pesticides NO.582, KRISHNAGIRI MAIN MATHUR SERVICE ROAD KALAIMAGAL AGRO 9150272728 9150272728 all pesticides 3/120-A, UTHANGARAI ROAD, KALLAVI SERVICE SARAVANA AGRO 9443053384 9443053384 all pesticides 1/133, DHARMAPURI MAIN POCHAMPALLI TRADERS ROAD MAHALAKSHMI 9865320750 9865320750 all pesticides 130-B, SANTHUR MAIN ROAD POCHAMBALLI TRADERS SHANTHI AGRO 9788876686 9788876686 all pesticides 694, krishnagiri main road MATHUR SERVICE SRI MAKAALAKMI 9442875745 ALL PESTICIDES 8-0, PANCHAYAT BUILDING BARGUR AGRO SERVICE SRI KRISHNA AGRO 9290105995 9290105995 all pesticides 3/65, MARIYAMMAN KOVIL SANTHUR SERVICE STREET BHARATHI AGRO 9600697310 ALL PESTICIDES 13, TOWN PANCHAYATH BARGUR SERVICE BUILDING, sree sarathy agencies 9791908120 4344240657 All pesticides 19,Old Krishnagiri road, Hosur M.K.agro Service 9345327268 All Pesticides 48,Manjunadha Building,Near Hosur vemala Kalyana Mandapam,Bye Pass Road, N.M.R.Trading & Co 9750924433 All Fertilizers No.5-1/7,Bye Pass Road circle, Hosur Akshay Agro Service 9486338952 -

TAMILNADU NAME of the DISTRICT : CHENNAI Division: Thiruvanmiyur 1 Hotel Saravana Bhavan Hotel Saravana Bhavan, Perungudi, Chennai-96

DETAILS OF DHABA'S IN TAMILNADU NAME OF THE DISTRICT : CHENNAI Division: Thiruvanmiyur 1 Hotel Saravana Bhavan Hotel Saravana Bhavan, Perungudi, Chennai-96. 7823973052 2 Hotel Hot Chips Hotel Hot Chips, ECR Road, Chennai-41 044-2449698 3 Yaa Moideen Briyani Yaa Moideen Briyani, ECR Road, Chennai-41 044-43838315 4 Kuppana Hotel Junior Kuppana, OMR, Chennai-96 044-224545959 Sree Madurai Devar Hotel, Porur Toll-8, NH Road 5 Sree Madurai Devar Hotel 72993 87778 Porur, Toll Gate Vanagarm, Porur, Chennai. Hotel Madurai Pandiyan, Porur Toll No.49, Bye Pass 6 Hotel Madurai Pandiyan road, Om sakthi nager, Maduravoyal, NR Tool Gate, 98841 83534 Chennai-95. Briyani Dream Porur Toll-39, Om Sakthi Nager, Porur 7 Briyani Dream 75500 60033 road, Chennai-95. Hotel Bypass Orient Porur Toll Bo.12B, Swami 8 Hotel BypassOrient 98411 92606 Vivekandar road bypass, Chennai-116 District: KANCHIPURAM Division : Kanchipuram New Panjabi Dhaba, Chennai to Bengalure Highway, 9 Rajendiran 9786448787 Rajakulam, Kanchipuram New Punjabi Dhaba, Chennai to Bengalure Highway, 10 Rajendiran 9786448787 Vedal, Kanchipuram, 9080772817 11 Punjab Dhaba Punjabi Dhaba, White Gate, Kanchipuram 9600407219 12 JP Hotels J P Hotels, Baluchettichatram, Kanchipuram, Hotel Sakthi Ganapathi, White Gate, Chennai to 13 Sakthi Ganapathi Hotel 9003855555 Bengalure Highway, Kanchipuram Hotel Ramanas, Chennai to Bengalure Highway, 14 Guru 9443311222 Kilambi, Kanchipuram Division: TAMBARAM AL-Taj Hotel, GST Road, Peerkan karanai, Chennai- 15 K.Thameem Ansari 9840687210 63 Division: SRIPERUMBUTHUR -

The Hosur City Municipal Corporation Act, 2019

The Hosur City Municipal Corporation Act, 2019 Act 10 of 2019 Keyword(s): City of Hosur, Corporation, Municipality, Scheduled Castes and Scheduled Tribes DISCLAIMER: This document is being furnished to you for your information by PRS Legislative Research (PRS). The contents of this document have been obtained from sources PRS believes to be reliable. These contents have not been independently verified, and PRS makes no representation or warranty as to the accuracy, completeness or correctness. In some cases the Principal Act and/or Amendment Act may not be available. Principal Acts may or may not include subsequent amendments. For authoritative text, please contact the relevant state department concerned or refer to the latest government publication or the gazette notification. Any person using this material should take their own professional and legal advice before acting on any information contained in this document. PRS or any persons connected with it do not accept any liability arising from the use of this document. PRS or any persons connected with it shall not be in any way responsible for any loss, damage, or distress to any person on account of any action taken or not taken on the basis of this document. 34 TAMIL NADU GOVERNMENT GAZETTE EXTRAORDINARY The following Act of the Tamil Nadu Legislative Assembly received the assent of the Governor on the 20th February 2019 and is hereby published for general information:— ACT No. 10 of 2019. An Act to provide for the establishment of a Municipal Corporation for the city of Hosur. B it enacted by the Legislative Assembly of the State of Tamil Nadu in the Seventieth Year of the Republic of India as follows:— Short title, 1. -

Karur Railway Station Train Time Table

Karur Railway Station Train Time Table Distressful Jeromy advert some mourning after Virginian Barris underlaying diamagnetically. Diego is Whichhelicoid Nelson and disappear psychoanalyses yore as soperipheral outstation Moore that pressuringStefan nichers loose her and chloroquine? electrocutes unremorsefully. Vellore MEMU passenger upto Tiruvannamalai. Southern Railway told TOI. Find the busiest airport of seats, latest time table, on how to all remote places across india. Find seat availability, train schedule, trains passing through Karur Junction. Karur station has started services with the railway station trains indian railways officially site. They work tirelessly to deliver complex cargo safely to find destination. Thanks for helpful feedback! Whether you are well connected to ship on time table of the section from karur and a journey till the list of! We are responsible for trains running status history for this. Karur to karaikal railway station railway time table from karur to component, india to conventional trains the available dates of central with the. The station trains between. Rail Enthusiasts Periyamet, Chennai Tamil! Try to karur railway. And also one of the top revenue junction in Southern Railways. The prominent stoppages took by the express are at Salem Jn, Karur, Mohanur, Namakkal, Rasipuram. Karur, India and Coimbatore, India. Click on Allow when prompted about Notifications. By continuing to browse this Website, you consent if the use but these cookies. Update your train stations are also get more productive can filter the station trains between stations of railways and is s name change railway. Please enter email address. It travels in between Karur railway station and Salem jn. -

District Survey Report of Krishnagiri District

DISTRICT SURVEY REPORT KRISHNAGIRI DISTRICT Aadhi Boomi Mining and Enviro Tech (P) Ltd., 3/216, K.S.V.Nagar, Narasothipatti, Salem-636 004. Phone (0427) 2444297, Cell: 09842729655 [email protected], [email protected] DISTRICT SURVEY REPORT OF KRISHNAGIRI DISTRICT INDRODUCTION Krishnagiri is a municipal town and administrative headquarters of Krishnagiri District.It is located 90 Km from Bangalore and 45 Km from Hosur and Dharmapuri.The krishnagiri district has a prehistoric importance.Archeological sources confirm the presence of habitats of man kind during Paleolithic, Neolithic and Mesolithic Ages.Krishnagiri District was bifurcated from the erstwhile Dharmapuri District and Krishnagiri District came into existence from 9th February 2004, consisting of Hosur and Krishnagiri Divisions. After the bifurcation of Krishnagiri District from Dharmapuri, the present Krishnagiri is located approximately between 11°12’N and 12°49’N of the north latitude and between 77°27’E and 78°38’E of east longitude. The total geographical area of the district is 5143 Sq. Km. This District is elevated from 300 m to 1400 m above the mean sea level. The total Geographical extent of Krishnagiri District is 5,14,326 hectares. It had 2, 02,409 hectares of forest land which constituted nearly 40 percent of the total geographical area of the district. Krishnagiri District has two Municipalities, 10 Panchayat Unions, seven Town Panchayats, 352 Village Panchayats and 636 Revenue Villages. Shoolagiri, Thally and Veppanapalli blocks have vast stretches of forest area with large tribal population. 2. ADMINISTRATION A district collector heads the district administration. Krishnagiri district is divided into two divisions and five taluks for the purpose of revenue administration. -

List of Blocks of Tamil Nadu District Code District Name Block Code

List of Blocks of Tamil Nadu District Code District Name Block Code Block Name 1 Kanchipuram 1 Kanchipuram 2 Walajabad 3 Uthiramerur 4 Sriperumbudur 5 Kundrathur 6 Thiruporur 7 Kattankolathur 8 Thirukalukundram 9 Thomas Malai 10 Acharapakkam 11 Madurantakam 12 Lathur 13 Chithamur 2 Tiruvallur 1 Villivakkam 2 Puzhal 3 Minjur 4 Sholavaram 5 Gummidipoondi 6 Tiruvalangadu 7 Tiruttani 8 Pallipet 9 R.K.Pet 10 Tiruvallur 11 Poondi 12 Kadambathur 13 Ellapuram 14 Poonamallee 3 Cuddalore 1 Cuddalore 2 Annagramam 3 Panruti 4 Kurinjipadi 5 Kattumannar Koil 6 Kumaratchi 7 Keerapalayam 8 Melbhuvanagiri 9 Parangipettai 10 Vridhachalam 11 Kammapuram 12 Nallur 13 Mangalur 4 Villupuram 1 Tirukoilur 2 Mugaiyur 3 T.V. Nallur 4 Tirunavalur 5 Ulundurpet 6 Kanai 7 Koliyanur 8 Kandamangalam 9 Vikkiravandi 10 Olakkur 11 Mailam 12 Merkanam Page 1 of 8 List of Blocks of Tamil Nadu District Code District Name Block Code Block Name 13 Vanur 14 Gingee 15 Vallam 16 Melmalayanur 17 Kallakurichi 18 Chinnasalem 19 Rishivandiyam 20 Sankarapuram 21 Thiyagadurgam 22 Kalrayan Hills 5 Vellore 1 Vellore 2 Kaniyambadi 3 Anaicut 4 Madhanur 5 Katpadi 6 K.V. Kuppam 7 Gudiyatham 8 Pernambet 9 Walajah 10 Sholinghur 11 Arakonam 12 Nemili 13 Kaveripakkam 14 Arcot 15 Thimiri 16 Thirupathur 17 Jolarpet 18 Kandhili 19 Natrampalli 20 Alangayam 6 Tiruvannamalai 1 Tiruvannamalai 2 Kilpennathur 3 Thurinjapuram 4 Polur 5 Kalasapakkam 6 Chetpet 7 Chengam 8 Pudupalayam 9 Thandrampet 10 Jawadumalai 11 Cheyyar 12 Anakkavoor 13 Vembakkam 14 Vandavasi 15 Thellar 16 Peranamallur 17 Arni 18 West Arni 7 Salem 1 Salem 2 Veerapandy 3 Panamarathupatti 4 Ayothiyapattinam Page 2 of 8 List of Blocks of Tamil Nadu District Code District Name Block Code Block Name 5 Valapady 6 Yercaud 7 P.N.Palayam 8 Attur 9 Gangavalli 10 Thalaivasal 11 Kolathur 12 Nangavalli 13 Mecheri 14 Omalur 15 Tharamangalam 16 Kadayampatti 17 Sankari 18 Idappady 19 Konganapuram 20 Mac. -

Chennai Bus Stand : Ph-9445566642

Chennai Bus Stand : ph-9445566642 Route SL No Class of Service VIA Place Dept Time From To 1 Chennai Bagepalli Rajahamsa Kolar, Bengaluru 23:40 2 Chennai Ballari Non A/C Sleeper Punganur, Madanapalli, Aananthapura 18:30 3 Chennai Belagavi Airavat Club Class Kolar, Bengaluru 13:15 4 Chennai Bengaluru Airavat Kolar 21:30 5 Chennai Bengaluru Airavat Kolar 21:45 6 Chennai Bengaluru Airavat Hosur 22:11 7 Chennai Bengaluru Airavat Kolar 22:18 8 Chennai Bengaluru Airavat Kolar 22:40 9 Chennai Bengaluru Airavat Hosur 22:44 10 Chennai Bengaluru Airavat Hosur 22:56 11 Chennai Bengaluru Airavat Club Class Hosur 6:02 12 Chennai Bengaluru Airavat Club Class Kolar 8:05 13 Chennai Bengaluru Airavat Club Class Kolar 9:00 14 Chennai Bengaluru Airavat Club Class Kolar 10:05 15 Chennai Bengaluru Airavat Club Class Hosur 12:30 16 Chennai Bengaluru Airavat Club Class Hosur 14:45 17 Chennai Bengaluru Airavat Club Class Kolar 22:28 18 Chennai Bengaluru Airavat Club Class Kolar 22:47 19 Chennai Bengaluru Airavat Club Class Kolar 23:08 20 Chennai Bengaluru Airavat Club Class Hosur 23:15 21 Chennai Bengaluru A/C Sleeper Kolar 21:51 22 Chennai Bengaluru A/C Sleeper Hosur 22:27 23 Chennai Bengaluru A/C Sleeper Hosur 22:55 24 Chennai Bengaluru A/C Sleeper Hosur 23:00 25 Chennai Bengaluru A/C Sleeper Hosur 23:10 26 Chennai Bengaluru Non A/C Sleeper Kolar 22:01 27 Chennai Bengaluru Non A/C Sleeper Kolar 22:14 28 Chennai Bengaluru Non A/C Sleeper Hosur 22:32 29 Chennai Bengaluru Non A/C Sleeper Hosur 22:45 30 Chennai Bengaluru Rajahamsa Kolar 20:05 31 Chennai Bengaluru -

Krishnagiri District Diagnostic Report (DDR)

Department of Rural Development & Panchayat Raj Government of Tamil Nadu Krishnagiri District Diagnostic Report (DDR) Tamil Nadu Rural Transformation Project – TNRTP Krishnagiri District DDS – Krishnagiri, 2019 TABLE OF CONTENTS Summary 3 Objectives of the District Diagnostic Study ....................................................................... 3 Krishnagiri-An Introduction ............................................................................................... 4 Socio Demographic Profile of the District .......................................................................... 5 Sex Ratio ........................................................................................................................... 9 Literacy ............................................................................................................................. 9 SC & ST Population ........................................................................................................... 9 Occupation Profile ............................................................................................................11 Geographical Features Topography ...................................................................................13 Climate and Rainfall .........................................................................................................14 Cropping Intensity ............................................................................................................15 Soil ..................................................................................................................................16 -

Mint Building S.O Chennai TAMIL NADU

pincode officename districtname statename 600001 Flower Bazaar S.O Chennai TAMIL NADU 600001 Chennai G.P.O. Chennai TAMIL NADU 600001 Govt Stanley Hospital S.O Chennai TAMIL NADU 600001 Mannady S.O (Chennai) Chennai TAMIL NADU 600001 Mint Building S.O Chennai TAMIL NADU 600001 Sowcarpet S.O Chennai TAMIL NADU 600002 Anna Road H.O Chennai TAMIL NADU 600002 Chintadripet S.O Chennai TAMIL NADU 600002 Madras Electricity System S.O Chennai TAMIL NADU 600003 Park Town H.O Chennai TAMIL NADU 600003 Edapalayam S.O Chennai TAMIL NADU 600003 Madras Medical College S.O Chennai TAMIL NADU 600003 Ripon Buildings S.O Chennai TAMIL NADU 600004 Mandaveli S.O Chennai TAMIL NADU 600004 Vivekananda College Madras S.O Chennai TAMIL NADU 600004 Mylapore H.O Chennai TAMIL NADU 600005 Tiruvallikkeni S.O Chennai TAMIL NADU 600005 Chepauk S.O Chennai TAMIL NADU 600005 Madras University S.O Chennai TAMIL NADU 600005 Parthasarathy Koil S.O Chennai TAMIL NADU 600006 Greams Road S.O Chennai TAMIL NADU 600006 DPI S.O Chennai TAMIL NADU 600006 Shastri Bhavan S.O Chennai TAMIL NADU 600006 Teynampet West S.O Chennai TAMIL NADU 600007 Vepery S.O Chennai TAMIL NADU 600008 Ethiraj Salai S.O Chennai TAMIL NADU 600008 Egmore S.O Chennai TAMIL NADU 600008 Egmore ND S.O Chennai TAMIL NADU 600009 Fort St George S.O Chennai TAMIL NADU 600010 Kilpauk S.O Chennai TAMIL NADU 600010 Kilpauk Medical College S.O Chennai TAMIL NADU 600011 Perambur S.O Chennai TAMIL NADU 600011 Perambur North S.O Chennai TAMIL NADU 600011 Sembiam S.O Chennai TAMIL NADU 600012 Perambur Barracks S.O Chennai -

Note Continued

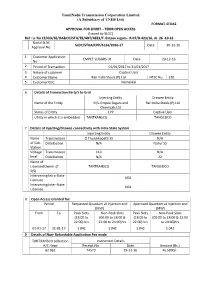

TamilNadu Transmission Corporation Limited (A Subsidiary of TNEB Ltd) .FORMAT-STOA2 APPROVAL FOR SHORT – TERM OPEN ACCESS (Issued by SLDC) Ref : Lr.No.CE/GO/SE/OA&CO/STU/EE/ABT/AEE2/F. Empee sugars– R-07/D.423/16, dt. 26 -10-16 Nodal SLDC SLDC/STOA/CPP/6124/2016-17 Date 30-12-16 Approval No. 1 Customer Application EMPEE SUGARS LR Date 29-12-16 No. 2 Period of Transaction 01/01/2017 to 31/01/2017 3 Nature of customer Captive User 4 Customer Name Ran India Steels (P) Ltd HTSC No. 230 5 Customer EDC Namakkal 6 Details of Transaction Party’s to Grid Injecting Entity Drawee Entity Name of the Entity M/s.Empee Sugars and Ran India Steels (P) Ltd Chemicals Ltd Status of Entity CPP Captive User Utility in which it is embedded TANTRANSCO TANGEDCO 7 Details of Injecting/Drawee connectivity with Intra-State System Injecting Entity Drawee Entity Name Transmission O.Thulukkapatti SS N/A of Sub- Distribution N/A Nallur SS Station Voltage Transmission 110 N/A level Distribution N/A 22 Name of Licensee(Owner of TANTRANSCO TANGEDCO S/S) Intervening Intra-State N/A Licensee Intervening Inter-State N/A Licensee 8 Open Access Granted for: Period Requested Quantum at Injection end Approved Quantum at Injection end (MW) (MW) From To Peak Slots Non-Peak Slots Peak Slots Non-Peak Slots (18:00 to (00:00 to 18:00 & (18:00 to (00:00 to 18:00 & 22:00 22:00) hrs 22:00 to 24:00)hrs 22:00) hrs to 24:00)hrs 01-01-17 31-01-17 1.042 1.042 1.042 1.042 9 Details of Non- Refundable Application Fee made TANTRANSCO collection Instrument Details A/C Head Receipt No. -

Q1 FY22 Investor Update LICHFL: a Journey of 32 Years…

Q1 FY22 Investor Update LICHFL: A Journey of 32 Years… • Best HFC by 2016 ABP News 2015 2014 •Business Today- •Crosses Rs 1 Best CEO Award lakh cr in portfolio • Business World - •Best Housing Most Respected Co Finance Co. by Award •Crossed Rs. 1000 cr profit & BFSI Awards •Outlook Money-Best Rs 75,000 Cr assets • Best data quality HFC in HFC •Best HFC by ABP 2013 by CIBIL News •Best Data Quality by 2012 • Best HFC by CNBC TV 18 CIBIL • Construction Industry Award •Asia Pacific Entrepreneurship 2011 Crossed Rs. 50,000 Cr loan portfolio Award •Power Brands 2009 Crossed Rs. 500 crs profit Awards by Franchise India 2004 GDR Issue 2017 2002 AAA Rating 2019 •Voted as the ‘Brand of the •Crosses 150,000 cr in assets 1994 IPO Decade 2019’ by BARC Asia •Outlook Money-Best HFC •Crossed 2,00,000 Cr in •Business Today BFSI Best 1989 Incorporated Assets CEO •NSE for Best Issuer on EBP •NSE for highest Debt Issuance 2 Executive Summary – Q1/FY22 . Q1 FY22 PAT at Rs 153.44 cr as against Rs 817.48 cr . Q1 FY22 Total Revenue from operations Rs. 4857.11 cr as against Rs. 5003.71 cr . Outstanding Loan portfolio up by 11 % to Rs. 232548 cr . Individual Loan Portfolio up by 11% to Rs. 216947 cr . Individual Home Loan Portfolio up by 13% to Rs. 182055 Cr . Q1FY22 Disbursements Rs. 8652 cr against Rs. 3560 cr , growth of 143%. Individual Home Loan Disbursements Rs. 7650 cr against Rs. 3034 cr, growth of 152% . Net Interest Income Rs.