Difficult Times for US Dairy Long-Term Trends, and Insights for China’S Dairy Companies October 2020 Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ims List Sanitation Compliance and Enforcement Ratings of Interstate Milk Shippers April 2017

IMS LIST SANITATION COMPLIANCE AND ENFORCEMENT RATINGS OF INTERSTATE MILK SHIPPERS APRIL 2017 U.S. Department of Health and Human Services Public Health Service Food and Drug Administration Rules For Inclusion In The IMS List Interstate milk shippers who have been certified by State Milk sanitation authorities as having attained the milk sanitation compliance ratings are indicated in the following list. These ratings are based on compliance with the requirements of the USPHS/FDA Grade A Pasteurized Milk Ordinance and Grade A Condensed and Dry Milk Products and Condensed and Dry Whey and were made in accordance with the procedures set forth in Methods of Making Sanitation Rating of Milk Supplies. *Proposal 301 that was passed at 2001 NCIMS conference held May 5-10, 2001, in Wichita, Kansas and concurred with by FDA states: "Transfer Stations, Receiving Stations and Dairy Plants must achieve a sanitation compliance rating of 90 or better in order to be eligible for a listing in the IMS List. Sanitation compliance rating scores for Transfer and Receiving Stations and Dairy Plants will not be printed in the IMS List". Therefore, the publication of a sanitation compliance rating score for Transfer and Receiving Stations and Dairy Plants will not be printed in this edition of the IMS List. THIS LIST SUPERSEDES ALL LISTS WHICH HAVE BEEN ISSUED HERETOFORE ALL PRECEDING LISTS AND SUPPLEMENTS THERETO ARE VOID. The rules for inclusion in the list were formulated by the official representatives of those State milk sanitation agencies who have participated in the meetings of the National Conference of Interstate Milk Shipments. -

Klein ISD ITB 17-299 Food Service: Dairy Products

Klein ISD ITB 17-299 Food Service: Dairy Products Option 1A - Delivery to all campuses daily - Fixed Prices - All items must be bid at a fixed price for the contract period. Line 1 Line items 1.1 and 1.2 are OPTIONAL Line 1.1 MILK, 11-12 OZ. BOTTLES, SKIM, WHITE Name QTY UOM Unit Price Ext. Price Note to Buyer Borden Milk Products 4200 EA $0.47 $1,974.00 1% sub for skim Hiland dairy Foods 4200 EA $0.79 $3,318.00 Line 1.2 MILK, 11-12 OZ. BOTTLES, FAT FREE, CHOCOLATE FLAVORED Name QTY UOM Unit Price Ext. Price Borden Milk Products 85000 EA $0.47 $39,950.00 Hiland dairy Foods 85000 EA $0.79 $67,150.00 Line 1.3 MILK, HALF-PINT, FAT FREE, CHOCOLATE FLAVORED Name QTY UOM Unit Price Ext. Price Oak Farms Dairy (Dean Foods) 3500000 EA $0.2636 $922,600.00 Borden Milk Products 3500000 EA $0.297 $1,039,500.00 Hiland dairy Foods 3500000 EA $0.33 $1,155,000.00 Line 1.4 MILK, HALF-PINT, FAT FREE, STRAWBERRY FLAVORED Name QTY UOM Unit Price Ext. Price Oak Farms Dairy (Dean Foods) 965000 EA $0.2636 $254,374.00 Borden Milk Products 965000 EA $0.297 $286,605.00 Hiland dairy Foods 965000 EA $0.33 $318,450.00 Line 1.5 MILK, HALF-PINT, SKIM, WHITE Name QTY UOM Unit Price Ext. Price Oak Farms Dairy (Dean Foods) 831000 EA $0.2646 $219,882.60 Borden Milk Products 831000 EA $0.297 $246,807.00 Hiland dairy Foods 831000 EA $0.33 $274,230.00 Line 1.6 BUTTERMILK, HALF-GALLON Name QTY UOM Unit Price Ext. -

A Letter from Gregg Tanner, CEO

JULY ’16 A Letter from Gregg Tanner, CEO As we entered 2016, I lauded our employees’ hard work and expressed the importance of keeping our momentum going by executing our new Strategic Plan. Now, halfway through the year, I am very encouraged by the steps we’ve taken toward delivering the initiatives in our plan. Already this year we made strides against every one of our pillars: • Under the Build and Buy Strong Brands pillar, we • We made great strides continued building our brands with the national launch of toward Enhancing Future Caribou Iced Coffee, TruMoo Calcium Plus, and DairyPure Capabilities with new leadership Lactose Free milk. We also extended our DairyPure training that further develops line into creams and creamers. Within the Buy Strong our people. We also added an Brands portion of the pillar, we officially closed on our extended shelf life line at our Lynn, Mass., facility and are agreement to acquire Friendly’s Ice Cream. This move fills focused on expanding our warehouse capabilities. Earlier a manufacturing and retail void in the Northeast, and the this year, we launched our Purpose, Strengthening Lives brand is a perfect fit for Dean Foods for many reasons. Through the Goodness of Dairy, with meaningful employee One of the goals established in our Strategic Plan is to events in Salt Lake City, San Antonio, Athens (Tenn.), expand our ice cream portfolio, and Friendly’s is uniquely Springfield (Ohio) and Woodbury (Minn.). I greatly enjoyed qualified to help us achieve that goal. In addition to the those visits to the field and the opportunity to strengthen iconic Friendly’s reputation and strong brand awareness, our communities with donations to local hunger relief manufacturing diversity is also a key part of Friendly’s programs. -

CPY Document

NATIONAL DAIRY PRODUCTS CORP. Syllabus It is ordered That the initial decision be modified by striking the last sentence of the fourth fuD paragraph on pag'e 61 and the fifth fuD paragraph on page 61. It is further ordered That the initial decision be modified by striking the order on page 61 and substituting therefor the fol1owing: It is ordered That respondent Montgomery Ward & Co. Incorporated, a corporation , and its offcers, representatives agents and employees, directly or through any corporate or other device , in connection with the offering for sale, sale, or distribution of any articles of merchandise in commerce, as commerce" is defined in the Federal Trade Commission Act do forthwith cease and desist from: Representing, directly or by implication that any of res- pondent's merchandise is guaranteed unless the nature and extent of the guarantee, the identity of the guaran- tor, and the manner in which the guarantor wil perform thereunder are clearly and conspicuously disclosed. It is furtiJer ordered That the hearing examiner s initial deci- sion , as modified by this order and the accompanying opinion be and it hereby is, adopted as the decision of the Commission. It is further ordered That the respondent shaD within sixty (60) days after service upon it of this order, file with the Com- mission a report, in writing, setting forth in detail the manner and form in which they have complied with the order to cease and desist set forth herein. Commissioners Elman and ReiDy dissented and have filed dis- senting opinions. IN THE MATTER OF KATIONAL DAIRY PRODUCTS CORPORATION ORDER , OPINIONS , ETC. -

STARBUCKS: from CROP to CUP APRIL 2015 the IMPACT of SOURCING INDUSTRIAL CONVENTIONAL MILK Updated January 2018

COALITION POWERED BY GREEN AMERICA STARBUCKS: FROM CROP TO CUP APRIL 2015 THE IMPACT OF SOURCING INDUSTRIAL CONVENTIONAL MILK updated January 2018 A MILK COMPANY Starbucks is one of the world’s most popular and widespread coffeehouse brands. It has over 22,000 cafes in 66 countries.1 In Manhattan alone there are 9 Starbucks per square mile.2 Starbucks built its reputation on delivering specialty coffee, putting a lot of energy into telling the story of its coffee from field to café. But what the company fails to address is the fact that each year, it purchases over 140,000,000 gallons of milk— enough to fill an Olympic-sized swimming pool 212 times.3 The fact is that Starbucks is a milk company as much or more than it is a coffee company. It is beyond time that it addresses the many negative impacts the industrial conventional dairy supply chain, from feed crop to cup, has on animal welfare and human and environmental health. If Starbucks’ goal, as stated on the company’s website, is to “share great coffee with [its] friends and help make the world a little better,” it is essential that the company transitions to organic milk.4 By setting the organic milk standard for coffee chains, Starbucks can demonstrate a serious commitment to providing environmentally and socially conscious products. Competitor com- panies like Pret A Manger are able to offer organic milk at a lower price than Starbucks charges for conventional dairy. It is our responsibility as consumers to vote with our dollars and use our voices to persuade the dairy industry to im- prove. -

EXHIBIT ITEM 1 SMA010 Proponent Cooperatives

EXHIBIT ITEM 1 SMA010 Proponent Cooperatives February 2004 Arkansas Dairy Cooperative Association, Inc. Floyd Wiedower, Manager P.O. Box 507 Damascus, Arkansas 72039 501-335-7204 501-335-7705 fax Dairy Farmers of America, Inc. Gary Hanman, Pres. & CEO P.O. Box 909700 Kansas City, Missouri 64190 816-801-6422 816-801-6423 fax Dairymen's Marketing Cooperative, Inc. Don Allen, General Manager 421 East State Street Mountain Grove, Missouri 65711 417-962-7460 417-962-6159 fax Lone Star Milk Producers, Inc. Jim Baird, Manager Route 1, Box 59B Windthorst, Texas 76389 940-378-2311 940-378-2751 fax Maryland & Virginia Milk Producers Cooperative Association, Inc. Jay Bryant, General Manager 1985 Isaac Newton Square West Reston, Virginia 20190 703-742-6800 703-742-7459 fax Southeast Milk, Inc. Calvin Covington, CEO P.O. Box 3790 Belleview, Florida 34421 352-245-2~,37 352-245-9434 fax EXHIBIT ITEM 2 SMA020 Producer Milk Deliveries Proponent Cooperatives and Others November 2003 F.O. 5 F.O. 7 Combined Total Order Producer Milk 507,412,336 593,836,792 1,101,249,128 Member Producer Milk Arkansas Dairy Coop. 13,933,382 13,933,382 Dairy Farmers of America 222,978,642 319,174,550 542,153,192 Dairymen's Marketing Coop. 6,235,057 6,235,057 Lone Star Milk Prod. 16,453,108 34,839,125 51,292,233 MD & VA Milk Prod. 80,473,502 22,119,702 102,593,204 / Southeast Milk 17,401,087 17,401,087 Tota___/I 319,905,252 413,702,903 733,608,155 Percent of Order Total 63.046% 69.666% 66.616% Other Cooperative Producer Milk Marketed Arkansas Dairy Coop. -

Federal Milk Order Distributing Plant Information for 2019 NOTE: "DIP" Indicates Debtor in Possession

Federal Milk Order Distributing Plant Information For 2019 NOTE: "DIP" indicates debtor in possession Pool Distributing Plants State County Plant Name City State ZipCode FIPS FIPS Cl. I Dftl. Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Agropur Grand Rapids MI 49548 26 081 1.80 33 33 33 33 33 33 33 33 33 33 33 33 Agropur Maplewood MN 55113 27 123 1.70 30 30 30 30 30 30 30 30 30 30 Alpenrose Dairy Portland OR 97298 41 051 1.90 124 124 124 124 124 124 124 124 124 124 124 124 Andersen Dairy Battle Ground WA 98604 53 011 1.90 124 124 124 124 124 124 124 124 124 124 124 124 Anderson-Erickson Dairy Des Moines IA 50317 19 153 1.80 32 32 32 32 32 32 32 32 32 32 32 32 Aurora Organic Dairy Platteville CO 80651 08 123 2.45 32 32 32 32 32 32 32 32 32 32 32 32 Blue Kingfisher dba Walmart Fort Wayne IN 46819 18 003 1.80 33 33 33 33 33 33 33 33 33 33 33 33 Boice Brothers Dairy Kingston NY 12401 36 111 2.80 1 1 1 1 1 1 1 1 Borden Dairy Cowarts AL 36321 01 069 4.30 7 7 7 7 7 7 7 7 7 7 7 7 Borden Dairy Miami FL 33164 12 025 6.00 6 6 6 6 6 6 6 6 6 6 6 6 Borden Dairy Winter Haven FL 33881 12 105 5.40 6 6 6 6 6 6 6 6 6 6 6 6 Borden Dairy London KY 40743 21 125 2.90 5 5 5 5 5 5 5 5 5 5 5 5 Borden Dairy Lafayette LA 70596 22 055 3.80 7 7 7 7 7 7 7 7 7 7 7 7 Borden Dairy Hattiesburg MS 39404 28 035 3.80 7 7 7 7 7 7 7 7 7 7 7 7 Borden Dairy Cincinnati OH 45215 39 061 2.20 33 33 33 33 33 33 33 33 33 33 33 33 Borden Dairy Cleveland OH 44111 39 035 2.00 33 33 33 33 33 33 33 33 33 33 33 33 Borden Dairy Charleston SC 29419 45 019 4.30 5 5 5 5 5 5 5 5 5 5 5 5 Borden Dairy Austin TX 78702 48 453 3.30 126 126 126 126 126 126 126 126 126 126 126 126 Borden Dairy Conroe TX 77305 48 339 3.60 126 126 126 126 126 126 126 126 126 126 126 126 Borden Dairy Dallas TX 75221 48 113 3.00 126 126 126 126 126 126 126 126 126 126 126 126 Braum's Tuttle OK 73089 40 051 2.60 32 32 32 32 32 32 32 32 32 32 32 32 Broadacre Dairies Powell TN 37849 47 093 3.20 5 5 5 5 5 5 5 5 5 5 5 5 Byrne Dairy Syracuse NY 13220 36 067 2.50 1 1 1 1 1 1 1 1 1 1 1 C. -

Dean Foods Successfully Implements C2CRM for Their HR Program

Case Study Dean Foods Successfully Implements C2CRM for Their HR Program Fluid Dairy Giant Streamlines Employee Change Request Management System Headquartered in Dallas, Dean Foods is a leading food and beverage company and the largest processor and direct-to-store distributor of fluid milk and other fluid dairy products in the United States. Their products are processed with the help of approximately 17,000 dedicated employees working in approximately 70 plants and close to 100 total locations across the U.S. The Business Problem The Human resources organization is responsible for managing and accurately keeping employee records up-to-date. The administration of these records were handled locally, typically by the 1 to 2 Human Resources personnel and a Business Partner coordinator at each location until the company evolved to a more centralized program. In an effort to better track all of the employee requests, a “Shared Services Center” was then implemented. Although all the requests were aggregated to one centralized location, there were still inefficiencies because the data entry process was manual and if key personnel were out sick or on vacation, critical work would not get done. According to Jessica Kosty, HRIS Manager at Dean Foods, “What was needed was a software that could automate data entry into a system that easily tracks all of their requests while notifying all the stakeholders of the completion of every stage in the process.” Why C2CRM? Leveraging the support module in C2CRM, HR is able to create allocate resources to address the increase of ticket processing. Once various types of tickets via the use and identification of multiple it was determined how successful the application was to their unique email boxes and track the history of work done during the life request process, the team expanded the use evolving from 1-2 of the ticket. -

FOR IMMEDIATE RELEASE Borden Appoints Tom Martin As Vice

FOR IMMEDIATE RELEASE Media Contact: Jessie Conrad Copperfield Advisory Ph: (617) 792-4011 E-mail: [email protected] Borden Appoints Tom Martin as Vice President of Walmart Former Sam’s Team Lead of Quaker Sales at PepsiCo will help scale Borden’s sales team to drive further growth DALLAS – Aug. 14, 2018 – Borden, a heritaGe American brand and leadinG U.S. dairy processer and distributor, today announced that Tom Martin has been appointed as Vice President of Walmart Inc., effective immediately. Martin is the eiGhth senior leader Borden CEO Tony Sarsam has hired since joininG the Company in March. “Tom is an exceptional leader with extensive industry experience and real success in drivinG sales,” said Sarsam. “We are thrilled to welcome someone with his track record of partnership with Walmart at a time when we are investinG to brinG world-class service to our larGest Customer. Tom brinGs terrific enerGy and leadership to the Borden team, and I know he will be an important asset as we brinG Borden into a new era of innovative Growth.” Martin brings 25 years of industry experience to Borden, havinG most recently served as the Sam’s Team Lead for Quaker products at PepsiCo. Previously, he was the Walmart DireCtor of Customer ManaGement and the Sam’s Director of Customer ManaGement for the Frito-Lay Division at PepsiCo. Martin previously served in a variety of senior sales and general manaGement roles at PepsiCo. “I am very excited to be joininG Borden at this important moment in the Company’s lonG history,” said Martin. “I am inspired by the new leadership team and I look forward to workinG with them to build a new Borden.” Martin holds an MBA from Southwest Baptist University. -

FOR IMMEDIATE RELEASE Borden Dairy Initiates Voluntary

FOR IMMEDIATE RELEASE Media Contact: Adrienne Chance Senior Director of Corporate Communications Borden Ph: (214) 957-5518 E-mail: [email protected] Borden Dairy Initiates Voluntary Reorganization Proceedings The Company will continue operating as normal as it works toward achieving a more viable capital structure and stresses “The Borden Difference” as a competitive advantage DALLAS – Jan. 5, 2020 – Borden, one of America’s favorite dairy companies founded in 1857, today announced that it and certain affiliates (collectively, “Borden” or the “Company”) have initiated voluntary reorganization proceedings in the District of Delaware under Chapter 11 of the Bankruptcy Code. The Company intends to use the court process to pursue a financial restructuring designed to reduce its current debt load, maximize value and position the Company for long-term success. Borden plans to continue operating in the ordinary course of business, under the court’s supervision, and remains focused on being the most service-oriented dairy Company that offers delicious and nutritious products consumers love. “Borden is EBITDA-positive and growing, but we must achieve a more viable capital structure,” said Borden CEO Tony Sarsam. “This reorganization will strengthen our position for future prosperity. Over the past 163 years, we have earned the distinction of being one of the most well-recognized and reputable national brands. We remain committed to ‘The Borden Difference,’ which is our promise to be the most service-oriented dairy Company that puts people first. We will continue serving our customers, employees and other stakeholders and operating business as usual throughout this process.” Last year marked several major milestones for the Company, including the revival of Borden’s beloved spokescow Elsie, the brand’s reintroduction in Ohio, and the launch of several innovative products that earned local and national media acclaim, such as State Fair-inspired milk flavors, Gingerbread Eggnog and Kid Builder. -

Plants, Handlers, and Bulk Tank Units Under the New York–New Jersey Marketing Orders

Plants, Handlers, and Bulk Tank Units Under the New York–New Jersey Marketing Orders December 1997 Table of Contents Page Symbols 2 Plant Listing by Handler 3 Plant Listing by Location 6 Bulk Tank Unit Listing by Handler 8 United States Department of Agriculture Agricultural Marketing Service – Dairy Division MARKET ADMINISTRATOR NEW YORK–NEW JERSEY MILK MARKETING AREA New York State Federal New Jersey State Order No. 126 Order No. 2 Order No. 57–3 Symbols NOTE: Symbols refer to a plant's operations during December 1997. There may be some variation in other months. Handlers E — handlers with partially-excluded or wholly-excluded own farm milk P-H — producer-handlers as defined in Section 1002.12 of the Orders Plants D — designated pool plants as defined in Section 1002.24 of the Orders T — temporary pool plants as defined in Section 1002.28 of the Orders N O — plants with no pool obligation Milk Sources O-F — milk produced on own farm BTU — milk from bulk tank units Plt — milk from other plants received in bulk form X — type of milk source Type of Plant Tr. (Transferring Plant) — where milk is assembled for shipment in bulk form to other locations Pr. (Processing Plant) — predominant operation is processing fluid milk products Mf. (Manufacturing Plant) — predominant operation is making Class II, III and III-A products X — plant's primary operation # — plant with transferring of milk as a secondary operation that accounts for at least 10 percent of its total volume, provided that it transfers at least 250,000 pounds (in bulk and/or packaged form) * — plant with manufacturing as a secondary operation that accounts for at least 10 percent of its total volume 2 TABLE 1. -

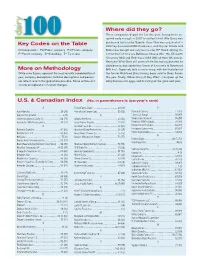

Key Codes on the Table More on Methodology Where Did They

Where did they go? Three companies depart the list this year, having been ac- quired early enough in 2007 to not be listed. Alto Dairy was Key Codes on the Table purchased last year by Saputo, Cass Clay was acquired at in 2007 by Associated Milk Producers, and Crystal Cream and C=Cooperative Pu=Public company Pr=Private company Butter was bought out early last year by HP Hood. Joining the P=Parent company S=Subsidiary T= Tie in rank list for the first time are BelGioso Cheese (No. 75), Ellsworth Creamery (84) and Roth Kase USA (96) all from Wisconsin. Next year Winn-Dixie will come off the list, having divested its dairy processing capabilities (some of it recently to Southeast More on Methodology Milk Inc.). Supervalu tells a similar story, with the final plant of While sales figures represent the most recently completed fiscal the former Richfood Dairy having been sold to Dean Foods year, company descriptions, facilities descriptions and person- this year. Finally, Wilcox Dairy of Roy, Wash., has given up the nel reflect recent changed where possible. Some entries will dairy business for eggs, and its listing will be gone next year. include an explanation of recent changes. U.S. & Canadian Index (No. in parentheses is last year’s rank) A Foster Farms Dairy ....................................... 50 (48) P Agri-Mark Inc. .............................................. 29 (29) Friendly Ice Cream Corp. ...............................55 (56) Parmalat Canada .........................................12 (13) Agropur Cooperative .........................................6 (9) G Perry’s Ice Cream ........................................ 97 (97) Anderson Erickson Dairy Co. ......................... 66 (71) Glanbia Foods Inc. ........................................ 23 (32) Plains Dairy Products ....................................95 (99) Associated Milk Producers Inc.