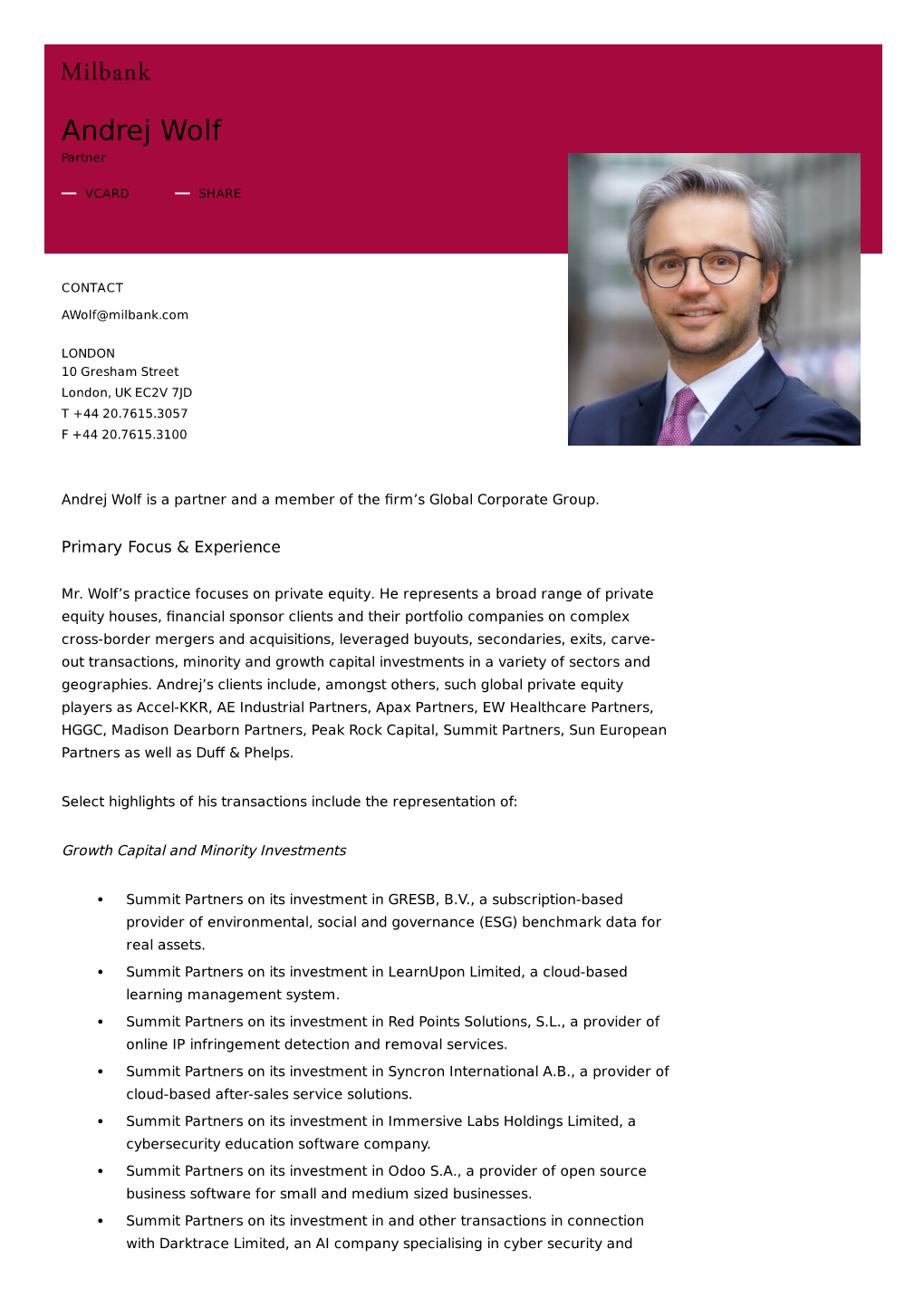

Andrej Wolf Partner

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Looking Somewhere in the Middle

OUR FIRM LMM GROUP CLIENTS TRANSACTIONS NEWS & INTEL CONTACT IN THIS SECTION LOOKING SOMEWHERE IN THE Executive Perspective IT Index MIDDLE News Room Quarterly Earnings March 10, 2006 Scoreboard Spotlight by: Kelly Holman Tracker VDI Accel-KKR LLC didn't set out to specialize in middle-market private equity buyouts in the high-tech sector. Its founders, an Subscribe unusual combination of dealmakers, were focused in 2000 on the bright prospects of the Internet, just as many other investors and entrepreneurs were. But that vista quickly turned as dark as night when the dot-com bubble burst, and Accel-KKR suddenly needed to make a rapid course correction. It did. Today the Menlo Park, Calif.-based firm has made a name for itself acquiring small but fast-growing technology companies. Even as top-tier buyout groups lick their chops over the possibility of doing deals involving big software corporations, Accel- KKR keeps its attention on midmarket and small tech outfits with $15 million to $150 million in annual revenue: software developers, hardware makers, Internet firm and information technology services businesses. To be sure, it's hardly the only middle-market private equity group interested in technology businesses - a number of buyout groups, large and small, have made technology their core investment focus. But Accel-KKR's board and the background it represents set it apart. Members include financial engineering icons Henry Kravis and George Roberts of Kohlberg Kravis & Roberts & Co.; KKR partner Marc Lipschultz; veteran venture capitalist and Accel managing partner Jim Breyer; and former Wells Fargo & Co. chief executive Paul Hazen. -

Capstone Headwaters Education Technology M&A Coverage Report

Capstone Headwaters EDUCATION TECHNOLOGY 2019 YEAR IN REVIEW TABLE OF CONTENTS MERGER & ACQUISTION OVERVIEW M&A Overview The Education Technology (EdTech) industry has continued to experience rapid consolidation with 195 transactions announced or completed in 2019. Active Buyers Heightened merger and acquisition (M&A) activity has been fueled by Notable Transactions persistent demand for disruptive and scalable technology as industry operators Select Transactions seek to expand product offerings and market share. In addition to robust transaction activity, recent investment patterns have targeted EdTech providers Public Company Data that offer innovative products for classroom teacher support and to streamline Firm Transactions in Market administrative operations in K-12 schools. Funding in the segment has risen Firm Track Record substantially with teacher needs and school operations garnering $95 million and $148 million in 2018, respectively, according to EdSurge.1 Large industry operators have remained acquisitive through year-end, evidenced by Renaissance Learning’s three acquisitions (page three) in 2019. CONTRIBUTORS EdTech providers have also utilized M&A as a means to diversify product offerings and end-markets outside of their core competencies. Notably, Health Jacob Voorhees & Safety Institute, a leader in environmental health and safety software and Managing Director, training services, acquired Martech Media, Inc, a provider of industrial Head of Education Practice, technology e-learning training solutions (December 2019, undisclosed). Head of Global M&A 617-619-3323 Private equity firms have remained active in the industry, accounting for 52% of [email protected] transaction volume. Operators that provide disruptive platforms and institutional business models, selling directly to schools districts, have garnered David Michaels significant investment interest and premium valuations. -

PEM Holds a Final Close on Its Fourth Direct Co-Investment Fund

Performance Equity Management, LLC Has Held a Final Close on its Fourth Direct Co-investment Fund Greenwich, CT – March 08, 2021 – Performance Equity Management, LLC (PEM) is pleased to announce the final closing of Performance Direct Investments IV (PDI IV), its fourth co-investment fund. The fund will focus on small and middle-market co-investment opportunities, continuing its successful strategy that was executed for its predecessor funds. PDI IV was significantly oversubscribed and closed on its hard cap of $300 million. Investors include public and corporate pension plans, university endowments, private foundations, insurance companies, family offices, and high net worth individuals across the globe. PDI IV is a continuation of our long-established investment strategy of partnering with premier GPs with demonstrated experience with a focus on defensive growth opportunities to build a high quality, diversified portfolio. Our selection capabilities and disciplined execution has enabled our strong performance and will continue to help us construct a resilient portfolio. “We are pleased with the 100% support of our long-standing investors and grateful to our new investors who have backed us in these unprecedented times,” said John Clark, President of PEM. “We believe our time-tested investment strategy will continue to support us in generating significant alpha for our investors.” Last year PEM also closed on it fourth venture capital fund of funds, Performance Venture Capital IV (PVC IV), in addition to several separate accounts. PVC IV closed above its target and is over 95% committed across premier venture capital funds. The fund’s largest commitments include Accel, Andreessen Horowitz, Redpoint Ventures and Spark Capital. -

Q2 2016 Venture Capital Deals and Exits Download the Data Pack July 2016

Q2 2016 Venture Capital Deals and Exits Download the Data Pack July 2016 Fig. 1: Global Quarterly Venture Capital Deals*, Q1 2011 - Fig. 3: Number of Venture Capital Deals in Q2 2016 by Q2 2016 Fig. 2: Venture Capital Deals* in Q2 2016 by Region Investment Stage 3,000 50 100% 1.5 187 0.6 Angel/Seed 45 1.0 Aggregate Deal Value ($bn) DealValue Aggregate 90% 53 2,500 237 40 80% 1% 8% Series A/Round 1 1% 3% 35 16.7 Series B/Round 2 2,000 70% 460 2% 30 3% 60% 33% Series C/Round 3 1,500 25 50% 407 7% 20 3.1 Series D/Round 4 and Later No. of Deals 1,000 40% 15 Growth Capital/Expansion Proportion of Total Proportion 30% 10 500 17.5 15% PIPE 5 20% 900 0 0 10% Grant Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 0% 27% Venture Debt 2011 2012 2013 2014 2015 2016 No. of Deals Aggregate Deal Value ($bn) Add-on & Other No. of Deals Aggregate Deal Value ($bn) North America Europe Greater China India Israel Other Source: Preqin Private Equity Online Source: Preqin Private Equity Online Source: Preqin Private Equity Online Fig. 5: Average Value of Venture Capital Deals, 2014 - Fig. 6: Number of US Venture Capital Deals* in Q2 2016 by Fig. 4: Venture Capital Deals* in Q2 2016 by Industry H1 2016 State 35% 120 111 111 31% 30% 96 27% 100 25% 2014 California 80 78 21% 21% 26% 20% 20% 16% 60 2015 New York 15% 13% 13% 44 39 37 Massachusetts 10% 9% 40 30 32 H1 2016 45% 25 Proportion of Total Proportion 5% 23 23 4% 4% Deal Size ($mn) Average 18 18 5% 3% 2% 3% 3% 20 10 12 3% Texas 1% 2% 1% 8 10 1% 1 2 0% 1 4% 0 Washington 8% Other Other Other IT Other Internet Business Services Clean Food & Food Series Series B/ Round 2 Round Round 1 Round Round 3 Round Telecoms Related Series Series A/ Series Series C/ 14% Agriculture Software & Healthcare Consumer Technology Angel/Seed Discretionary Expansion 4 andLater 4 Venture Debt Venture No. -

Venture Capital June 2016

Venture Capital June 2016 Strictly for Educational Purposes C lickDisclaimer to edit Master title style This presentation is intended to be a general overview to be used strictly for educational purposes. This presentation may not contain all the details and information necessary for you to make investment decisions or evaluations. This presentation should be viewed in conjunction with the links and sources provided. The information in this presentation are individual opinions and personal academic/industry experiences, all of which are subject to change. They do not necessarily reflect every detailed aspect of the economy, industry, the financial market or finance as an academic major. Comments made are of a general nature and they are not designed to suit personal circumstances. Any representations or illustrations in this presentation may have been modified or simplified to suit the audience it is intended for. Strictly for Educational Purposes 2 C lickContents to edit Master title style Section Page 1 Executive Summary 5 2 Government Initiatives 10 3 Venture Capital Firms and Investment Case Studies 14 4 Conclusion 19 Strictly for Educational Purposes 3 C lickPublications to edit Master Team title style Publications Directors • Jesse Mo • Robin Nandy Subcommittee Contributors • Aditya Katyar • Alex Chye • Alex Chan • Anita Chao • Henry Chen • Kevin Lu Strictly for Educational Purposes 4 Section 1 Executive Summary C lickWhat to editis Venture Master Capital?title style Overview Definition Involved Parties • Venture capital is money -

Public Investment Memorandum Summit Partners Growth Equity

COMMONWEALTH OF PENNSYLVANIA PUBLIC SCHOOL EMPLOYEES’ RETIREMENT SYSTEM Public Investment Memorandum Summit Partners Growth Equity Fund X, L.P. Private Equity Fund Commitment Darren C. Foreman, CAIA Senior Manager, Private Markets Patrick G. Knapp, CFA Senior Investment Professional, Private Markets December 19, 2018 COMMONWEALTH OF PENNSYLVANIA PUBLIC SCHOOL EMPLOYEES’ RETIREMENT SYSTEM Recommendation: Staff, together with Hamilton Lane Advisors, L.L.C. (“Hamilton Lane”), recommends to the Board a commitment of up to $150 million to Summit Partners Growth Equity Fund X, L.P. (“Summit Growth Equity X” or the “Fund”). Summit Partners, L.P. (“Summit” or the “Firm”) is forming the Fund to continue its long history of investing in U.S. growth equity opportunities which spans nine U.S. growth equity funds with aggregate committed capital of $13.6 billion. Firm Overview: Summit Partners, L.P. is a global alternative investment firm managing investment vehicles focused primarily on growth companies. The Firm was founded in 1984 with a commitment to partner with exceptional entrepreneurs and management teams, providing capital and strategic support to help them achieve their growth objectives. Since inception, Summit has raised and managed more than $22 billion in capital dedicated to growth equity, fixed income, and public equity strategies, including 15 growth equity and venture capital funds with combined committed capital of approximately $17.4 billion and eight fixed income funds with combined committed capital of approximately $4.1 billion. Over the last three decades, Summit has invested in more than 475 companies in technology, healthcare and life sciences, and other growth industries — including more than 430 companies from the U.S. -

GROWTHCAP INSIGHTS 2016 Top 40 Under 40 Growth Investors

GrowthCap 40 Under 40 | November 2016 GROWTHCAP INSIGHTS 2016 Top 40 Under 40 Growth Investors It gives us great pleasure to announce GrowthCap’s 2016 40 Under 40 Growth Investors list. Those appearing in this year’s list were first nominated by their firm, their peers or by GrowthCap. They were then evaluated based on breadth of experience (volume of completed deals, capital invested, number of exits, and realized returns, among other factors) as well as qualitative aspects contributing to their overall effectiveness working with peers, CEOs, LPs and deal professionals. We realized after the publication of our 2014 and 2015 lists, the influence the list can have on LPs evaluating new fund investments or CEOs deciding on prospective capital partners. In particular, the list has been helpful to large family offices in identifying talented investors in the growth equity asset class. The large majority of this year’s nominees provided information on their professional background and investment experience, which played a key role in our selection process and ranking methodology. GrowthCap also conducted interviews with select nominees and in some cases, has had the benefit of direct experience working with nominated individuals and/or represented firms. - RJ Lumba, Managing Partneraaaaa Clockwise from top left: Kapil Venkatachalam (Technology Crossover Ventures), Jason Werlin (TA Associates), Mohamad Makhzoumi (New Enterprise Associates), Chris Adams (Francisco Partners) Page 1 GrowthCap 40 Under 40 | November 2016 Kapil Venkatachalam joined Technology Crossover Ventures in 2006 as an 1 associate and now works as a general partner for the firm. Reflecting on his experience with TCV, Kapil remarks, “Technology is the heart of our business. -

Vcs Like of Accel Partners India, Nexus Venture Partners & SAIF

VCs like of Accel Partners India, Nexus Venture Partners & SAIF Partners pool in $1 billion for Indian start-ups The Economic Times, 26th March 2015 http://economictimes.indiatimes.com/news/emerging-businesses/startups/vcs-like-of-accel-partners-india-nexus-venture- partners-saif-partners-pool-in-1-billion-for-indian-start-ups/articleshow/46695239.cms MUMBAI: India's top venture capital firms are raising larger pools of capital, encroaching into early growth territory as tech startups scrambling for bigger deals knock at hedge funds and other global investors rushing into the country. Just three VCs - Accel Partners India, Nexus Venture Partners and SAIF Partners - have pooled nearly $1 billion this month alone for investments in Indian startups. Accel, an early investor in Flipkart, on Tuesday closed a $305 million (Rs 1,900 crore) fund, nearly double the size of its previous fund raised four years ago. Snapdeal investor Nexus Venture Partners anticipates wrapping up around $450 million this month, $180 million larger than its previous corpus. Increased fundraising by venture capital firms coincides with the entry of hedge funds and investors such as Japan's Softbank and Russian billionaire Yuri Milner's investment fund DST Global into India's tech financing market in the past year. Entry of these investors has increased deal sizes, with internet companies seeking larger fund doses in shorter time. Startups raised $2.1 billion in venture funding in 2014, an increase of 50% over the prior year, according to research firm VCCEdge. This was in addition to around $3.2 billion (Rs 20,000 crore) raised by more mature internet companies such as Flipkart, Snapdeal, Quikr, Info Edge and Makemytrip. -

PLAYA HOTELS & RESORTS NV Nieuwezijds Voorburgwal 104 1012

PLAYA HOTELS & RESORTS N.V. Nieuwezijds Voorburgwal 104 1012 SG Amsterdam, the Netherlands June 3, 2021 Dear Playa Hotels & Resorts N.V. Shareholders: You are cordially invited to attend the rescheduled annual general meeting of shareholders (the “AGM”) of Playa Hotels & Resorts N.V. (“Playa” or the “Company”), which will be held on Tuesday, June 29, 2021 at 4:00 p.m. Central European Summer Time (CEST), at the Company’s offices, located at Nieuwezijds Voorburgwal 104, 1012 SG Amsterdam, the Netherlands. Please note that the AGM has been rescheduled from the original date of May 13, 2021, and the enclosed Notice and Proxy Statement are replacing the materials originally mailed to you on or about April 19, 2021. We request that you vote your shares for the rescheduled AGM, as proxies that were delivered or votes that were received for the AGM originally scheduled for May 13, 2021 will not be valid. During the AGM, shareholders will be asked to vote on the appointment of directors; the adoption of the Dutch Statutory Annual Accounts for fiscal year 2020; the ratification of the selection of Deloitte & Touche LLP as Playa’s independent registered accounting firm for fiscal year 2021; the instruction to Deloitte Accountants B.V. for the audit of Playa’s Dutch Statutory Annual Accounts for fiscal year 2021; an advisory vote to approve the compensation of our named executive officers; the discharge from liability for Playa’s directors with respect to the performance of their duties in 2020; the authorization of the Board of Directors to acquire shares (and depository receipts for shares) in the Company’s capital; the delegation to the Board of Directors of the authority to issue shares and grant rights to subscribe for shares in the capital of the Company and to limit or exclude pre-emptive rights; and an advisory vote on the frequency of the advisory vote on the compensation of our named executive officers (each a “Proposal” and together the “Proposals”). -

1Q 2019 Relationship Management Purpose-Built for Finance Learn More at Affinity.Co

Co-sponsored by Global League Tables 1Q 2019 Relationship Management Purpose-Built for Finance Learn more at affinity.co IMPROVE ELIMINATE SUPPORT DISCOVER PROPIERTARY CROSSING YOUR NEW EXECUTIVE DEAL FLOW WIRES PORTFOLIO CONNECTIONS Learn why 500+ firms use Affinity's patented technology to leverage their network and increase deal flow “Within weeks of moving “The biggest problems Affinity “Let’s be honest, no one wants to Affinity, we were able to helps me solve are how to to use Salesforce reporting. easily discover and manage track all of my activity and how Affinity isn’t just better for most the 1,000s of entrepreneur to prioritize my time. It makes teams, it’ll make the difference and venture community me a better investor. All of the between managing your relationships already latent things I need to do on a day-to- pipeline to success, versus not within our team." day basis I now do in Affinity.” tracking it at all.” ERIC EMMONS KYLE LUI KEVIN ZHANG Managing Director Partner Principal MassMutual Ventures DCM Ventures Bain Capital Ventures [email protected]@affinity.co AffinityAffinity is a relationship is a relationship intelligence intelligence platform platform built to builtexpand to expandand evolve and theevolve traditional the traditional CRM. AffinityCRM. Affinityinstantly instantly surfaces surfaces all all www.affinity.cowww.affinity.co of yourof team’s your team’sdata to data show to you show who you is bestwho issuited best tosuited make to the make crucial the crucialintroductions introductions you need you to need close to your close next your big next deal. big deal. -

Cloudera Whatsapp

LOS ANGELES | SAN FRANCISCO | NEW YORK | BOSTON | SEATTLE | MINNEAPOLIS | MILWAUKEE August 13, 2013 Michael Pachter Steve Koenig (213) 688-4474 (415) 274-6801 [email protected] [email protected] PRISM … Progress Report for Internet and Social Media In This Issue: Cloudera, WhatsApp Cloudera Big Data analysis firm founded by four tech veterans from Facebook, Yahoo, Google and Oracle. Developed applications based on open source Apache Hadoop to process large data sets. Has raised $141 million over five rounds of funding. Annual revenue estimated at $100 million. Market expected to grow at 54% CAGR over next five years. WhatsApp Mobile instant messaging service with 250 million global monthly active users. Subscription-based revenue model; no advertisements or virtual goods. Mostly self-funded, with only $8 million raised in four years. STRATEGIES GROUP THE INFORMATION HEREIN IS ONLY FOR ACCREDITED INVESTORS AS DEFINED IN RULE 501 OF REGULATION D UNDER THE SECURITIES ACT OF 1933 OR INSTITUTIONAL INVESTORS. WEDBUSH PRIVATE COMPANY Wedbush Securities does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Please see page 10 of this report for analyst certification and important disclosure information. Cloudera Cloudera offers scalable and efficient data storage and analytics solutions to companies in the enterprise, Internet and government sectors. The company, based in Palo Alto, was launched in 2008 by three top engineers from Google, Yahoo, and Facebook (Christophe Bisciglia, Amr Awadallah, and Jeff Hammerbacher, respectively) who joined former Oracle executive Michael Olson to address problems inherent in analyzing large volumes of data quickly. -

INTRODUCTION James R. Swartz Is a General Partner and Founder Of

INTRODUCTION James R. Swartz is a general partner and founder of Accel Partners. He has been active in venture capital since the early 1970s and has served as director for over 50 successful companies. Jim Swartz has been closely involved as the lead investor in numerous industry pioneering public firms including Broadband Technologies, Daisy Systems, Medical Care America, Netopia, PictureTel, Polycom, Remedy Corporation, Riverbed Networks, Ungermann-Bass and many others. In addition, he is working closely with the Accel Europe team as a founder and mentor of Accel’s European business. Before founding Accel Partners in 1983, he was founding general partner of Adler & Company, which he started with Fred Adler in 1978 after his tenure as a vice president of Citicorp Venture Capital. He is a former director and chairman of the National Venture Capital Association. In addition to his ongoing professional commitments, he is a significant leader in numerous cultural, civic, and education-oriented philanthropic activities throughout the nation. A graduate of Harvard University, he also holds a Master’s degree in Industrial Administration from Carnegie Mellon. Mauree Jane Perry: Today is July 19, 2006. This interview with Jim Swartz is taking place at his home in San Francisco, California. My name is Mauree Jane Perry, Oral Historian. Good afternoon, Jim, and thank you. Jim Swartz: Thank you. VENTURE CAPITAL GREATS JAMES R. SWARTZ ________________________________________________________________________ EARLY YEARS MJP: I thought we would begin with the early years of where and when you were born. JS: I was born in 1942 in Pittsburgh, Pennsylvania, at Allegheny General Hospital, which is still there on the north side — actually adjacent to Three River Stadium.