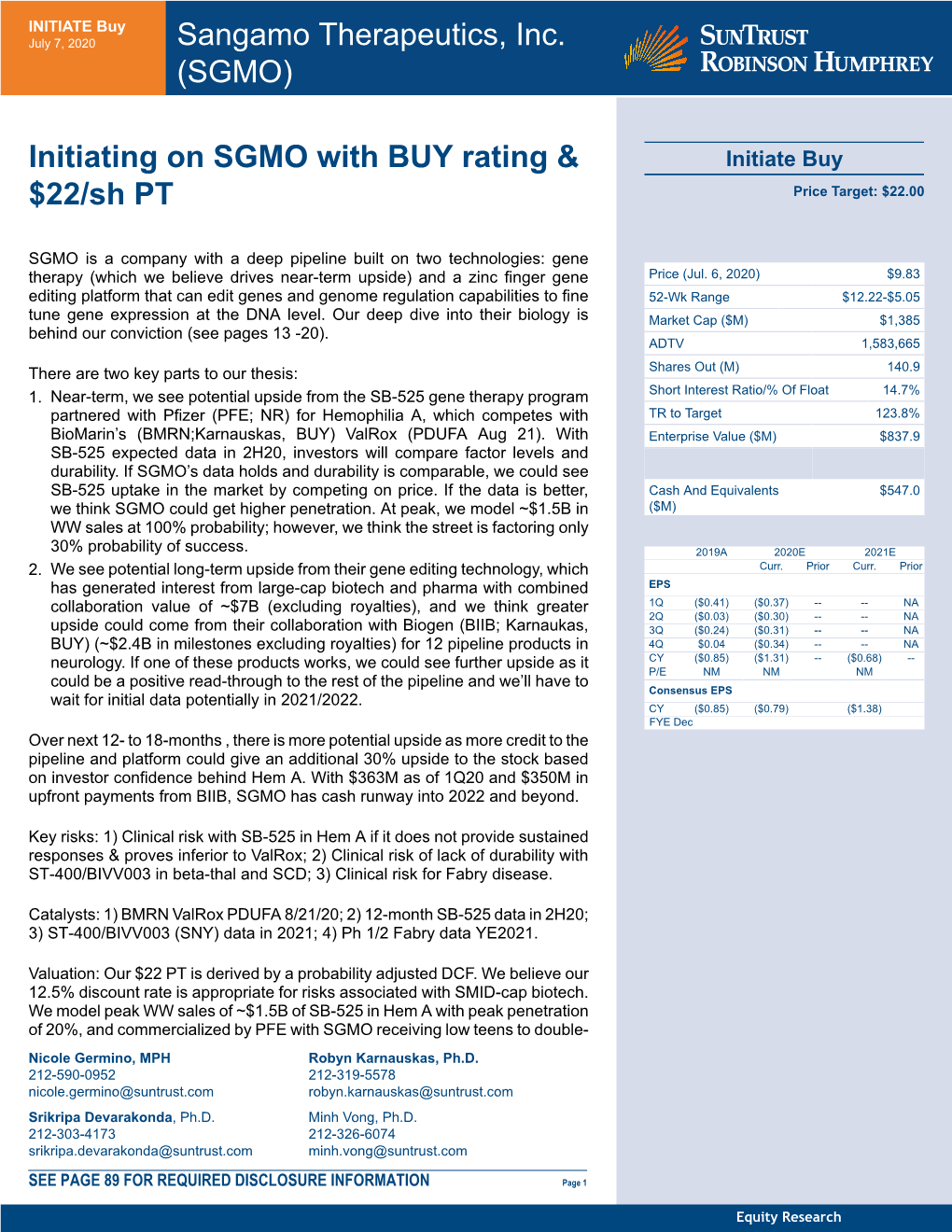

Sangamo Therapeutics, Inc. (SGMO)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SANGAMO THERAPEUTICS, INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended September 30, 2017 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 000-30171 SANGAMO THERAPEUTICS, INC. (exact name of registrant as specified in its charter) Delaware 68-0359556 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification No.) 501 Canal Blvd Richmond, California 94804 (Address of principal executive offices) (510) 970-6000 (Registrant’s telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by section 13 or 15(d) of the Securities Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. -

Medicines in Development -- Cell Therapy and Gene Therapy

Medicines in Development -- Cell Therapy and Gene Therapy Alzheimer's Disease Drug Name Sponsor Indication Development Phase allogeneic mesenchymal Stemedica Cell Technologies Alzheimer's disease Phase II stem cell therapy (itMSCs) San Diego, CA www.stemedica.com AstroStem Nature Cell Alzheimer's disease Phase I/II stem cell therapy Seoul, South Korea www.stemcellbio.com Arthritis/Musculoskeletal Disorders Drug Name Sponsor Indication Development Phase AdipoCell™ U.S. Stem Cell intervertebral disc degeneration Phase II adipose-derived autologous Sunrise, FL www.us-stemcell.com stem cell therapy CybroCell™ SpinalCyte intervertebral disc degeneration Phase I/II human dermal fibroblast-based Houston, TX www.spinalcyte.com cell therapy ECCO-50 Cytori Therapeutics osteoarthritis of the knee Phase II completed (adipose-derived autologous stem San Diego, CA www.cytori.com and regenerative cell therapy) Medicines in Development: Cell Therapy and Gene Therapy ǀ 2018 1 Arthritis/Musculoskeletal Disorders Drug Name Sponsor Indication Development Phase IDCT DiscGenics lumbar degenerative disc disease Phase I/II (allogeneic injectable discogenic Salt Lake City, UT www.discgenics.com cell therapy) JointStem Nature Cell osteoarthritis of the knee Phase II mesenchymal stem cell therapy Seoul, South Korea www.stemcellbio.com mesenchymal stem cell therapy Medipost osteoarthritis Phase I/II completed Seoul, South Korea www.medipost.com PLX-PAD (emiplacel) Pluristem Therapeutics muscle injury following arthroplasty Phase III (human placental stromal cell -

Kite, a Gilead Company, and Sangamo Therapeutics Announce Collaboration to Develop Next-Generation Engineered Cell Therapies for the Treatment of Cancer

Sangamo Therapeutics Logo Kite, a Gilead Company, and Sangamo Therapeutics Announce Collaboration to Develop Next-Generation Engineered Cell Therapies for the Treatment of Cancer February 22, 2018 -- Kite to Receive Exclusive License to Leverage Sangamo's Gene Editing Technology in Allogeneic and Autologous Cell Therapy Programs in Oncology -- SANTA MONICA, Calif. and RICHMOND, Calif., Feb. 22, 2018 /PRNewswire/ -- Kite, a Gilead Company (Nasdaq: GILD) and Sangamo Therapeutics, Inc. (Nasdaq: SGMO) today announced the companies have entered into a worldwide collaboration using Sangamo's zinc finger nuclease (ZFN) technology platform for the development of next-generation ex vivo cell therapies in oncology. Kite will use Sangamo's ZFN technology to modify genes to develop next-generation cell therapies for autologous and allogeneic use in treating different cancers. Allogeneic cell therapies from healthy donor cells or from renewable stem cells would provide a potential treatment option that can be accessed directly within the oncology infusion center, thus reducing the time to infusion for patients. Under the terms of the agreement, Sangamo will receive an upfront payment of $150 million and is eligible to receive up to $3.01 billion in potential payments, aggregated across 10 or more products utilizing Sangamo's technology, based on the achievement of certain research, development, regulatory and successful commercialization milestones. Sangamo would also receive tiered royalties on sales of potential future products resulting from the collaboration. Kite will be responsible for all development, manufacturing and commercialization of products under the collaboration, and will be responsible for agreed upon expenses incurred by Sangamo. "This collaboration between Kite and Sangamo brings together two leading platforms to develop best-in-class cell therapies in oncology," said Sandy Macrae, President and Chief Executive Officer of Sangamo. -

Sangamo Therapeutics Reports First Quarter 2019 Financial Results

Sangamo Therapeutics Logo Sangamo Therapeutics Reports First Quarter 2019 Financial Results May 8, 2019 Conference Call and Webcast Scheduled for 5:00 p.m. Eastern Time BRISBANE, Calif., May 8, 2019 /PRNewswire/ -- Sangamo Therapeutics, Inc. (NASDAQ: SGMO), a genomic medicine company, today reported first quarter 2019 financial results and recent business highlights. "With recent encouraging clinical data in hemophilia A gene therapy and ex vivo gene-edited cell therapy for beta thalassemia, we are moving closer to achieving our vision for Sangamo as an integrated genomic medicine company," said Sandy Macrae, CEO of Sangamo. "Our capabilities in gene therapy, ex vivo gene-edited cell therapy, in vivo genome editing and gene regulation enable us to address genetic diseases with appropriate technologies. We are investing in a diverse pipeline of products where we believe this suite of proprietary technologies is clinically relevant, where the underlying biology is well-characterized, and where there is a defined high unmet medical need." Recent Highlights Clinical In partnership with Pfizer, announced phase 1/2 interim data for SB-525, a gene therapy candidate for the treatment of adults with hemophilia A, demonstrating dose-dependent increases in Factor VIII (FVIII) activity in eight patients, with the two patients treated with the 3e13 vg/kg dose reaching normal FVIII levels Initiated dose expansion of the 3e13 vg/kg dose cohort for the SB-525 hemophilia A program, based on Safety Monitoring Committee recommendations Announced early data -

Family Conference Dec

33RD ANNUAL NATIONAL MPS SOCIETY FAMILY CONFERENCE DEC. 19–21, 2019 • ORLANDO, FL #mpsfamily2019 MISSION STATEMENT The National MPS Society exists to cure, support and advocate for MPS and ML. Contents MPS and ML Chair Letter 1 Mucopolysaccharidoses (MPS) and Mucolipidosis (ML) are genetic lysosomal storage diseases (LSD) caused by the body’s inability to Board of Directors/Staff 2 produce specific enzymes. General Information 3 MPS I MPS IV Hotel Layout 5 MPS I H Hurler MPS IV A Morquio A Schedule 6 MPS I S Scheie Enzyme / Galactose 6-sulfatase MPS IV B Morquio B Speakers 10 MPS I H-S Hurler-Scheie Enzyme / a-L-Iduronidase Enzyme / B-Galactosidase Attendees 30 MPS VI Thank You to Our Sponsors 36 MPS II MPS II Hunter MPS VI Maroteaux-Lamy Notes 38 Enzyme / Iduronate sulfatase Enzyme / (arylsulfatase B) N-Acetylgalac-tosamine 4-sulfatase MPS Jingle Bell Run/Walk 41 MPS III Upcoming Events 42 MPS VII MPS III A Sanfilippo A Enzyme / Heparan N-sulfatase MPS VII Sly Enzyme / B-Glucuronidase MPS III B Sanfilippo B Enzyme / a-N- Acetylglucosaminidase MPS IX MPS III C Sanfilippo C Enzyme / Hyaluronidase Enzyme / Acetyl CoA: a-glycosaminide acetyltransferase ML II/III MPS III D Sanfilippo D Enzyme / N-Acetylglucosamine ML II I-Cell 6-sulfatase ML III Psuedo-Hurler polydystrophy Enzyme / N-acetylglucosamine-1- phosphotransferase Chair Letter I am so excited to be at the National MPS Society’s 33rd Annual Family Conference at the most magical place on earth! Our family conference has a special place in my heart. I dearly treasure the time I spend with all of you and the entire MPS and ML community each year. -

Post-Event Summary

VIRTUAL BIOMANUFACTURING WORLD SUMMIT 20 NOVEMBER 16-17, 2020 POST-EVENT SUMMARY EVENT SITE EPTHOUGHTLEADERS.COM EP_BIOMAN EXECUTIVE PLATFORMS HIGHLIGHTS 200+ Attendees 99% 85% Director-Level have personal budgetary 120+ and Above responsibilities over $5M GLOBAL ORGANIZATIONS 71% have an annual company revenue over $1B Keynotes, case studies, “Excellent ‘virtual’ roundtable discussions, conference with a broad 30+ workshops and more range of presentations and great information exchange on technologies transforming the biopharmaceutical industry.” 20+ Head, Global Biologics Solution Operating Unit providers Days of virtual networking, learning and 2 sharing ideas BIOMANWORLD.COM BMWS20 2 SPEAKERS Here are just a few of our speakers: Juan Andres Patrick Yang Chief Technical Operations Chairman at Acepodia and Quality Officer & Founding Board Director at Sana Biotechnology Lou Schmukler Michael Kamarck EVP and President, Global Product Chief Technology Officer Development & Supply Alison Moore Pam Cheng Chief Technology Officer EVP, President Global Operations & IT Jerry Cacia Derek Adams SVP, Head Global Technical Development Chief Technology and Manufacturing Officer John Pinion Brendan O’Callaghan EVP Translational Sciences, SVP & Global Head Chief Quality Operations Officer of Specialty Care IA Arleen Paulino Jens Vogel SVP Global Manufacturing SVP & Global Head of Biotech Charlene Banard Craig Kennedy Global Head of Technical Operations SVP Global Supply Chain Management for Cell & Gene Therapy BIOMANWORLD.COM BMWS20 3 ATTENDEES A2 Biotherapeutics Sr. Director, Tech Ops Bristol Myers Squibb Sr. Director Acadia Director QA Bristol Myers Squibb Sr. Research Associate Acceleron Pharma Inc VP, Quality Bristol Myers Squibb Director, Cell Culture Eng. CoE (Cell Therapy) Acepodia & Sana Biotechnology Chairman & Founding Board Director Bristol Myers Squibb Director of Manufacturing Adaptimmune Chief Patient Supply Officer Bristol Myers Squibb Engineer ADMA Biologics VP of Quality BMS - Cell Therapy Tech Ops Sr. -

Sangamo Biosciences Presents New Data from in Vivo Protein Replacement Platform Programs for MPS I and MPS II at the 12Th Annual Worldsymposium™ Meeting

Sangamo Therapeutics Logo Sangamo BioSciences Presents New Data From In Vivo Protein Replacement Platform Programs For MPS I And MPS II At The 12th Annual WORLDSymposium™ Meeting March 2, 2016 IVPRP Approach Permits Therapeutic Enzymes for Lysosomal Storage Disorders to Cross the Blood Brain Barrier Improving Cognitive Symptoms of Disease RICHMOND, Calif., March 2, 2016 /PRNewswire/ -- Sangamo BioSciences, Inc. (NASDAQ: SGMO), the leader in therapeutic genome editing, announced the presentation of new preclinical data in disease models from its In Vivo Protein Replacement Platform™ (IVPRP) programs for MPS I (Hurler syndrome) and MPS II (Hunter syndrome). The data demonstrate that the Company's IVPRP approach enabled stable production of therapeutic levels of replacement enzyme from the liver into the circulation and secondary tissues, including the brain, resulting in significant reduction in biomarkers of the disease and, importantly, statistically significant improvements in cognitive function in treated animals. The data were presented by Sangamo scientists and their collaborators at the University of Minnesota in two oral presentations at the 2016 Annual WORLDSymposium™ Meeting being held in San Diego from February 29 to March 4, 2016. "These data represent a fundamental shift in the therapeutic intervention in Hunter and Hurler syndromes. The data demonstrate that constant, stable production of both the human alpha-L-iduronidase and iduronate 2-sulfatase enzymes generated by the IVPRP strategy enables its transport from the circulation into the brain in sufficient quantities to have a therapeutic benefit on neurological aspects of the disease," said Chester Whitley, Ph.D., M.D., director of the Gene Therapy Center at the University of Minnesota Medical School. -

Sangamo Therapeutics Reports Fourth Quarter and Full Year 2019 Financial Results

Sangamo Therapeutics Logo Sangamo Therapeutics Reports Fourth Quarter and Full Year 2019 Financial Results February 28, 2020 Conference Call and Webcast Scheduled for 8 a.m. Eastern Time BRISBANE, Calif.--(BUSINESS WIRE)-- Sangamo Therapeutics, Inc. (NASDAQ: SGMO), a genomic medicine company, today reported fourth quarter and full year 2019 financial results and recent business highlights. “This quarter marked an important milestone for Sangamo, as we transitioned to a Phase 3 company following the transfer of the IND for SB-525 hemophilia A gene therapy to our partner Pfizer, who plan to commence the registrational study this year. This is a significant step in our mission to bring our genomic medicines to patients,” said Sandy Macrae, CEO of Sangamo. “Additionally this year, we look forward to progressing our wholly owned assets, ST-920 gene therapy for Fabry disease and TX200 CAR-Treg cell therapy, in the clinic, and will work closely with our collaborator, Kite, as they advance KITE-037, an anti-CD19 allogeneic CAR-T therapy into a Phase 1/2 clinical trial. We will also continue to advance new IND targets in highly prevalent diseases, as exemplified by the newly announced Biogen collaboration, and will continue to look for additional synergistic partnership opportunities to advance our mission to bring innovative genomic medicines to patients and to create value for our shareholders.” Recent Highlights Yesterday, announced global collaboration agreement with Biogen to develop and commercialize gene regulation therapies for Alzheimer’s, Parkinson’s, neuromuscular and other neurological diseases. Under the terms of the collaboration, Biogen has exclusive global rights to ST-501 for tauopathies including Alzheimer’s disease, ST-502 for synucleinopathies including Parkinson’s disease, and a third undisclosed neuromuscular disease target. -

Sangamo Therapeutics Reports Second Quarter 2019 Financial Results

Sangamo Therapeutics Logo Sangamo Therapeutics Reports Second Quarter 2019 Financial Results August 7, 2019 Conference Call and Webcast Scheduled for 5:00 p.m. Eastern Time BRISBANE, Calif.--(BUSINESS WIRE)--Aug. 7, 2019-- Sangamo Therapeutics, Inc. (NASDAQ: SGMO), a genomic medicine company, today reported second quarter 2019 financial results and recent business highlights. “We continue to progress our strategy to develop our diversified portfolio of genomic medicine product candidates using our expertise in gene therapy, cell therapy, genome editing and gene regulation,” said Sandy Macrae, CEO of Sangamo. “Last month, we reported updated results for SB-525, our investigational gene therapy for hemophilia A. We are pleased with the emerging clinical profile and competitive positioning of SB-525 and are preparing for a Phase 3 registrational study with our partner Pfizer. The THALES study evaluating ST-400, a gene-edited cell therapy for beta thalassemia being developed with Sanofi, is progressing well and recently enrolled a fourth patient. In the upcoming months, two of our wholly owned programs, ST-920, an investigational gene therapy for Fabry disease, and TX-200, our first CAR-Treg product candidate, are also expected to advance into the clinic.” “We have observed significant increases in efficacy above a defined vector dose threshold with AAV6, the vector we use in our hemophilia gene therapy and our in vivo genome editing clinical programs,” Dr. Macrae continued. “These recent insights into the kinetics of AAV6 suggest rational methods for improving the delivery of zinc finger nucleases, which we believe may substantially enhance the efficacy of in vivo genome editing, especially when added to the significantly increased potency that we expect to obtain with our updated gene editing reagents. -

Sangamo Therapeutics Announces Presentations at 2019 Annual Meeting of the American Society of Gene & Cell Therapy

Sangamo Therapeutics Logo Sangamo Therapeutics Announces Presentations At 2019 Annual Meeting Of The American Society Of Gene & Cell Therapy April 15, 2019 BRISBANE, Calif., April 15, 2019 /PRNewswire/ -- Sangamo Therapeutics, Inc. (NASDAQ: SGMO), a genomic medicine company, today announced that Sangamo scientists and collaborators will present data from the Company's clinical and preclinical pipeline at the 22nd Annual Meeting of the American Society of Gene & Cell Therapy (ASGCT) being held April 29th to May 2nd, 2019 in Washington, D.C. Abstracts accepted for presentation highlight data from the Company's gene therapy program in Fabry disease; ex vivo gene-edited cell therapy programs in hemoglobinopathies being developed in partnership with Sanofi; and preclinical programs for CNS diseases using Sangamo's gene regulation approach, which include tauopathies, C9ORF72-linked ALS in collaboration with Pfizer, and Huntington's disease in collaboration with Takeda. "Sangamo's strong scientific presence at ASGCT demonstrates the breadth of our therapeutic pipeline and our expertise in innovative genomic medicines research and development," said Adrian Woolfson, M.D., Ph.D., Sangamo's Executive Vice President of Research and Development. "Through our pioneering work in developing zinc fingers for ex vivo and in vivo genome editing, we've gained invaluable insights into AAV manufacturing and delivery, as well as gene editing precision, efficiency, and specificity. We're now applying these insights to our integrated portfolio of programs in -

Sangamo Therapeutics Reports Third Quarter 2019 Financial Results

Sangamo Therapeutics Logo Sangamo Therapeutics Reports Third Quarter 2019 Financial Results November 6, 2019 Conference Call and Webcast Scheduled for 5:00 p.m. Eastern Time BRISBANE, Calif.--(BUSINESS WIRE)--Nov. 6, 2019-- Sangamo Therapeutics, Inc. (NASDAQ: SGMO), a genomic medicine company, today reported third quarter 2019 financial results and recent business highlights. “We continue to prioritize and progress our clinical development programs, as demonstrated by the accepted ASH poster presentations for our two most advanced programs, SB-525 hemophilia A gene therapy and ST-400 beta thalassemia cell therapy. Patients are currently being screened for enrollment into the clinical study evaluating ST-920, our wholly owned Fabry disease gene therapy, and we expect to enroll a first patient by the end of the year. We have also recently submitted a CTA for the clinical trial of our CAR-Treg, TX200, in mismatched renal transplantation,” said Sandy Macrae, CEO of Sangamo. “As it is important that we continue to articulate our drug development, research, and partnership strategies, we will host a Sangamo R&D day in New York on December 17, 2019. At this meeting, we will provide updates across our various genomic medicine programs, offer our perspective on the clinical data at ASH, share improvements across our technology platforms, and provide an overview of the manufacturing strategy to support our clinical and commercial supply.” Recent Highlights Clinical Earlier today, announced the upcoming poster presentation of three abstracts at the 61st American Society of Hematology (ASH) annual meeting in Florida: Updated follow-up of the Phase 1/2 Alta Study assessing SB-525 gene therapy in adult patients with severe hemophilia A in partnership with Pfizer. -

Sangamo Announces Publication in Molecular Therapy of Preclinical Study Data from MPS II in Vivo Genome Editing Program

Sangamo Therapeutics Logo Sangamo Announces Publication In Molecular Therapy Of Preclinical Study Data From MPS II In Vivo Genome Editing Program April 4, 2018 Study provided proof of concept for development of SB-913 product candidate currently being evaluated in Phase 1/2 clinical trial RICHMOND, Calif., April 4, 2018 /PRNewswire/ -- Sangamo Therapeutics, Inc. (NASDAQ: SGMO) announced today the publication of preclinical murine study data from the company's in vivo genome editing program for Mucopolysaccharidosis Type II (MPS II) in the April 2018 issue of Molecular Therapy. In the study, in a mouse model of MPS II, zinc finger nuclease (ZFN)-mediated genome editing of cells in the liver resulted in expression of therapeutic levels of iduronate 2-sulfatase (IDS), an enzyme MPS II patients lack, and in the prevention of metabolic and neurological disease symptoms. The work was conducted in collaboration with the University of Minnesota's Center for Genome Engineering. The preclinical study provided proof of concept for development of SB-913, an in vivo genome editing product candidate Sangamo is currently evaluating in the CHAMPIONS Study, a Phase 1/2 clinical trial assessing the potential safety and efficacy of SB-913 in up to nine adult males with attenuated MPS II. SB-913 uses Sangamo's ZFN genome editing technology delivered intravenously via AAV6 vectors and is a single-treatment strategy intended to provide stable, continuous production of the IDS enzyme. About the Preclinical Study Male MPS II model mice between six and nine weeks of age were injected with one of three increasing dose levels of a genome editing treatment consisting of AAV2/8 vectors encoding a pair of ZFNs and a corrective human IDS (hIDS) gene.