GAA Property Insurance Policy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Camogie Association & GAA Information and Guidance Leaflet On

Camogie Association & GAA Information and Guidance leaflet on the National Vetting Bureau (Children & Vulnerable Persons) Act 2012 March 2015 1 National Vetting Bureau (Children & Vulnerable Persons) Act The National Vetting Bureau (Children and Vulnerable Persons) Act 2012 is the vetting legislation passed by the Houses of the Oireachtas in December 2012. This legislation is part of a suite of complementary legislative proposals to strengthen child protection policies and practices in Ireland. Once the ‘Vetting Bureau Act’ commences the law on vetting becomes formal and obligatory and all organisations and their volunteers or staff who with children and vulnerable adults will be legally obliged to have their personnel vetted. Such personnel must be vetted prior to the commencement of their work with their Association or Sports body. It is important to note that prior to the Act commencing that the Associations’ policy stated that all persons who in a role of responsibility work on our behalf with children and vulnerable adults has to be vetted. This applies to those who work with underage players. (The term ‘underage’ applies to any player who is under 18 yrs of age, regardless of what team with which they play). The introduction of compulsory vetting, on an All-Ireland scale through legislation, merely formalises our previous policies and practices. 1 When will the Act commence or come into operation? The Act is effectively agreed in law but has to be ‘commenced’ by the Minister for Justice and Equality who decides with his Departmental colleagues when best to commence all or parts of the legislation at any given time. -

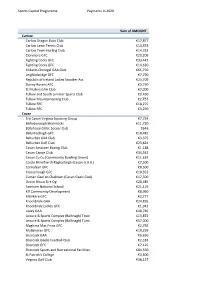

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow Carlow Dragon Boat Club €17,877 Carlow Lawn Tennis Club €14,353 Carlow Town Hurling Club €14,332 Clonmore GFC €23,209 Fighting Cocks GFC €33,442 Fighting Cocks GFC €14,620 Kildavin Clonegal GAA Club €61,750 Leighlinbridge GFC €7,790 Republic of Ireland Ladies Snooker Ass €23,709 Slaney Rovers AFC €3,750 St Mullins GAA Club €7,000 Tullow and South Leinster Sports Club €9,430 Tullow Mountaineering Club €2,757 Tullow RFC €18,275 Tullow RFC €3,250 Cavan 3rd Cavan Virginia Scouting Group €7,754 Bailieborough Shamrocks €11,720 Ballyhaise Celtic Soccer Club €646 Ballymachugh GFC €10,481 Belturbet GAA Club €3,375 Belturbet Golf Club €23,824 Cavan Amatuer Boxing Club €1,188 Cavan Canoe Club €34,542 Cavan Co Co (Community Bowling Green) €11,624 Coiste Bhreifne Uí Raghaillaigh (Cavan G.A.A.) €7,500 Cornafean GFC €8,500 Crosserlough GFC €10,352 Cuman Gael an Chabhain (Cavan Gaels GAA) €17,500 Droim Dhuin Eire Og €20,485 Farnham National School €21,119 Kill Community Development €8,960 Killinkere GFC €2,777 Knockbride GAA €24,835 Knockbride Ladies GFC €1,942 Lavey GAA €48,785 Leisure & Sports Complex (Ballinagh) Trust €13,872 Leisure & Sports Complex (Ballinagh) Turst €57,000 Maghera Mac Finns GFC €2,792 Mullahoran GFC €10,259 Shercock GAA €6,650 Shercock Gaelic Football Club €2,183 Shercock GFC €7,125 Shercock Sports and Recreational Facilities €84,550 St Patrick's College €3,500 Virginia Golf Club €38,127 Sports Capital Programme Payments in 2020 Virginia Kayak Club €9,633 Cavan Castlerahan -

Gaa for All Program Cumman Lúthchleas Gael Whats Inside?

GAA FOR ALL PROGRAM CUMMAN LÚTHCHLEAS GAEL WHATS INSIDE? PAGE CONTENTS 03 What is GAA for ALL? 04 Wheelchair Hurling / Camogie 05 Football for ALL 06 Playing the Game 07 Fun and Run Game 08 Cúl Camps 09 Inclusive Club Program 10 Frequently Asked Questions 11 Contacts WHAT IS GAA FOR ALL? The first line of the GAA Official Guide spells out how the GAA reaches into every corner of Ireland and many communities around the globe. In doing this, the GAA is fully committed to the principles of inclusion and diversity at all levels Our aim: To offer an inclusive, diverse and welcoming environment for everyone. •Inclusion means people having a sense of belonging, of being comfortable in being part of something they value. Inclusion is a choice. Diversity means being aware of accommodating and celebrating difference. •Inclusion and Diversity in many ways go together. Real inclusion reflects diversity, i.e. it aims to offer that sense of belonging to everyone, irrespective of gender, marital status, family status, sexual orientation, religion, age, race or minority community and/or disability. WHEELCHAIR HURLING /CAMOGIE Playing the Game Team Composition Game commences with Throw-in Minimum age 12, no maximum age between two midfielders in centre 6 a side court All players must have physical Game split up into attacking disability half/defensive half Teams score GOALS only Pitch Layout Once a player scores they Half size regulation pitch become goalkeeper for their team Smaller than regulation goals A handpass must be followed by a Playing area -

Wicklow Coaching Calendar 2020

WICKLOW GAA 2020 Coach Education Calendar Because Knowledge is Power TURAS – the Irish word for Journey – it was chosen to support the journey taken by both coaches and players up through the age grades. Player Centered and Coach Driven Better Coaches + Better Players = Better Teams Join, like or follow us for updates on social media Twitter Facebook Website Officialwicklowgaa.ie Wicklow GAA Coach Education Education Programme 2020 Coaches are encouraged to participate practically to maximize their opportunity for learning. Our programme is designed to support all coaches working at child, youth and adult level through specifically planned courses and workshops incorporating all that is good in terms of coaching best practice. Again this year in attempting to meet the mandatory coaching standards as set out by the GAA we are organising the required amount of coaching courses to meet these targets.The Games Development programme for this year provides the best possible support for coaches in relation to Coach Education and Coaching Workshops.TURAS principles should run throughout the coaching & games programme at all levels. As such, all stakeholders Players, Coaches, Managers, Academy leaders & Parents will speak a common language and follow a common pathway as they progress on their TURAS Pathway. TURAS Principals The kep principals underpinning coaching on the Wicklow GAA Coach Development are presented using the acronym TURAS. TURAS is the Irish for journey, it was purposefully chosed to reflect the journey that is player coach development. -

All- Ireland Glory for Nenagh Handball Club!

VOL. 2 ISSUE 3 APRIL 2014 SEPTEMBER 2013 .. NENAGH SENIOR HURLERS MAKE UNDER-16 IT TWO FOR FOOTBALLERS TWO IN THE THROUGH TO COUNTY THE NORTH A SENIOR FINAL HURLING CHAMPIONSHIP ALL- IRELAND GLORY FOR NENAGH HANDBALL CLUB! Congratulations to Katie Morris, Sinéad Meagher and Eimear Meagher, our new All-Ireland medal holders. The girls were part of the Munster team that won the Girls 40x20 Interprovincial Team of 10 event in Kingscourt, Cavan. The girls were the only Tipp representatives on the team which is a great achievement for the club. Well done also to Eamonn Spillane who was one of the two Munster team coaches on their great win. VOL. 2 ISSUE 3 APRIL 2014 SEPTEMBER 2013 FINAL CIVIC RECEPTION AT NENAGH TOWN COUNCIL On Friday April 25th, our club was honoured with a civic reception from Nenagh Town Council. This is the highest award the town can award and it was in recognition of the fantastic success our club enjoyed in 2013 in a number of different codes. Firstly the camogie section was honoured because they won the county Junior League and championship while the U18's also 1 captured county championship honours. Both our Scór and handball sections had numerous successes last year and they were recognised, as were our minor hurlers who won the county title. 2 3 Special mention must go to Aislinn O’Brien who was individually recognised because not only was she on the camogie teams who were so successful but she was also on the Nenagh Town AFC teams that won Munster honours at both U16 and Senior level. -

CCC1 FOOTBALL and HURLING LEAGUE REGULATIONS 2021 Our

CCC1 FOOTBALL AND HURLING LEAGUE REGULATIONS 2021 Our Games - Our Code, The joint Code of Best Practice CCC1 and Dublin County Board fully support ‘Our Games - Our Code’ the joint Code of Best Practice in Youth Sport. This Code has been agreed between the GAA, the Ladies Gaelic Football Association, the Camogie Association, GAA Handball Ireland and the Rounder’s Council of Ireland. The full GAA code of Best Practice – ‘Our Games, Our Code’ is available to download and view at http://www.gaa.ie/the-gaa/child-welfare-and-protection/ (Note the file size is large (7GB) so please allow sufficient time for the document to download.) The full code of Behaviour is available to download and view at http://www.gaa.ie/news/gaa- code-behaviour/ In December 2017 the remaining provisions of the Children First Act commenced in full. Most notably for the GAA our immediate requirements include that all clubs have appointed a Children’s Officer and a Designated Liaison Person. In addition to this each mentor/ coach must have completed: Garda Vetting via the GAA Safeguarding 1-The GAA Sport Ireland Child protection & Welfare workshop A basic Coach Education course (IE. A foundation Award) Further information on Children First requirements for the GAA can be found here: https://res.cloudinary.com/dvrbaruzq/image/upload/ovpxxr64puz6hiatwwnj.pdf Rules a. All U8-U12 games must be played under Go Games Rules as set out and available to view/download in the Go Games Information section http://www.dublingaa.ie/juvenile/regulations b. The kick out mark, advance mark and sin bin rules are not applicable to Go-Games Rules c. -

Nuachtlitir Aibreán 2021

Football Hurling Club General APRIL 2021 NUACHTLITIR AIBREÁN 2021 FOR NEWS, VIDEOS AND FIXTURES www.gaa.ie Football Hurling Club General COVID-19 UPDATE FOR CLUBS: NEARLY THERE AFTER THE LONGEST OF WINTERS, WE threaten to undermine the significant ARE NEARLY THERE. work done by the majority of members in the face of the Pandemic. In the coming weeks activity will return to GAA pitches all over the country. As the Uachtarán and Ard Stiúrthóir They are but the first tentative steps wrote in their letter to clubs on March in Ireland’s easing of restrictions north 30: and south, and they are dependent on virus numbers being manageable, but “These are hugely welcome for the first time in a long time, there is developments and allow us finally to hope again. begin planning on-field activity for the remainder of 2021. However, it should Inter-county training will be allowed to also be noted that these dates are resume north and south from April 19. conditional and will very much depend A revised fixture schedule for the GAA on what happens in terms of the overall season with inter-county competitions COVID-19 picture in the coming weeks. followed by a clear slot for club For that reason, it is more important championship will be released on the than ever that no collective training weekend of April 9. sessions are held between now and the Government indicated return dates. In the 26 Counties juvenile training in Breaches in this context will not only non-contact pods will be allowed from be dealt with under our own Rules but April 26. -

Rules of Handball Place a Presumptive Code of Integrity and Honesty on Each Player

GAA Handball - Official 40x20 & 60x30 Playing Rules ………………………………………..……………………………………….……… Official Irish 40x20 & 60x30 Playing Rules As of September 2017. The One-Wall playing rules can be found separately on www.gaahandball.ie. Any changes in these rules will be maintained by GAA Handball, and will be available at www.gaahandball.ie. Note: • The Playing Rules published in this booklet are those, which apply to GAA Handball as it is played in the All-Ireland Championships for both codes; 40x20 & 60x30, in this country. • 40x20 Nationals or Open tournaments may be played using the International 40x20 Playing Rules, of which there are slight modifications in a few areas of the rulebook. Such variations are noted below (See 4.11, Pg 35). 1 GAA Handball - Official 40x20 & 60x30 Playing Rules ………………………………………..……………………………………….……… Contents: Section 1 - The Game Page 1.1 Types 4 1.2 Description 4 1.3 Objective 4 1.4 Scoring 4 1.5 The Match 5 Section 2 - Courts and Equipment 2.1 Courts 6 2.2 Ball 8 2.3 Gloves 10 2.4 Playing Attire 11 3. Officials and Officiating 3.1 Tournament Director 12 3.2 Chief of Referees 12 3.3 Removal of Officials 12 3.4 Referee 13 3.5 Players’ Code 15 3.6 Line Judges 16 3.7 Appeals 17 3.8 Marker 17 Section 4 - Play Regulations 4.1 Serve 18 4.2 Doubles 19 4.3 Defective Serves 20 4.4 Return of Serve 23 4.5 Changes of Serve 24 4.6 Rally 24 4.7 Dead-ball Hinders 28 4.8 Avoidable Hinders 31 4.9 Technicals 32 4.10 Timeouts & Rest Periods 33 4.11 Key International 40x20 Variations 35 4.12 Key 60x30 Variations 35 2 GAA Handball - Official 40x20 & 60x30 Playing Rules ………………………………………..……………………………………….……… Section 5 - Competition Regulations 5.1 Juvenile Playing Rules 36 5.2 Juvenile Team Championships 38 5.3 Inter-Club Championships 40 5.4 Feile na Gael 40 5.5 Gael Linn Mixed Doubles 41 5.6 Girls Interprovincial Competitions 42 5.7 Boys Colleges 43 5.8 Girls Colleges 44 Section 6 - Appendix 6.1 Fixtures & Postponements Policy 45 3 GAA Handball - Official 40x20 & 60x30 Playing Rules ………………………………………..……………………………………….……… Section 1. -

An Chomhdháil Bhliantúil 2011 GAA Annual Congress 2010 Tuarascáil, Cuntais Airgid Agus Rúin Don Chomhdháil

foR club And county An Chomhdháil Bhliantúil 2011 GAA Annual Congress 2010 Tuarascáil, Cuntais Airgid agus Rúin don Chomhdháil www.gaa.ie 2010 county champions football antrim armagh carlow cavan st gall’s crossmaglen rangers old leighlin kingscourt stars clare cork derry donegal doonbeg nemo rangers coleraine naomh conaill down dublin fermanagh galway burren kilmacud crokes roslea killererin kerry kildare kilkenny laois dr crokes moorefield muckalee portlaoise leitrim limerick longford louth O'C glencar manorhamilton monaleen longford slashers mattock rangers mayo meath monaghan offaly ballintubber skryne clontibret rhode roscommon sligo tipperary tyrone st brigids eastern harps aherlow coalisland waterford westmeath wexford wicklow stradbally garrycastle castletown rathnew 2010 county champions hurling antrim armagh carlow cavan NAOMH MOUNG loughgeil shamrocks keady st mullin’s mullahoranMullach Odhrain Cumann Lúthchleas Gael clare cork derry donegal GAA CLUB crusheen sarsfields lavey seán mac cumhaill’s down dublin fermanagh galway ballygalget ballyboden st enda’s lisbellaw clarinbridge kerry kildare kilkenny laois ballyduff celbridge o’loughlin gael’s rathdowney errill leitrim limerick longford louth st mary’s kilmallock wolfe tones naomh moninne SPORT DON SAOL mayo meath monaghan offaly W S ballyhaunis kildalkey inniskeenO grattansLFETONE coolderry n an m lu - u t c h c h le a s el ga roscommon sligo tipperary tyrone four roads western gaels thurles sarsfields éire óg carrickmore waterford westmeath wexford wicklow de la salle raharney -

Official-Playing-Rule-Book

HANDBALL PLAYING RULES Part V. Competition Rules Contents Page Part I. The Game A Juvenile Competitions 28 Page B Inter Club 33 A Types 1 C Féile na nGael 34 B Description 1 D Ladies Competitions 35 C Objective 1 E Colleges 40 D Points and Handouts 1 F Community Games 44 E Game 1 G International Rules 46 F Match 2 H One-WalI Rules 47 I Playing Equipment 51-52 Part II. Court and Equipment Index A Court 3 [The Playing Rules published in this booklet are those which apply B Ball 5 to GAA Handball as it is played in both codes (60 x 30 & 40 x 20) in C Gloves 6 this country] D Playing Attire 7 E Blood Rule 7 2014 Rule Book Part III. Officials and Officiating A. Fixtures 8 B. Referee 8 C Marker 11 Part IV. Play Regulations A. Serve 11 B Return of Serve 16 C. Change of Serve 17 D Rally 18 E Hinders 21 F Rest Periods 26 OFFICIAL PLAYING RULES PART I - THE GAME. F. MATCH. (a) A match is won by the side first winning two games. A. TYPES. (b) In the case of a match played on a time basis the player or side Four-wall handball may be played by two or four players. When with the highest score at the end of the specified time is the played by two it is called 'singles' and when played by four, winner. If however, the rules of any competition state that extra 'doubles'. time must be played in the event of a tie, the match must continue without an interval after a toss a coin for service has B. -

Result: Winner(S)

Please text all relevant Results to: +353 (0) 873 665330. Liathróid Laímhe CLG na hÉireann OR email to: [email protected] Páirc an Chrócaigh, Baile Átha Cliath 3 Results can also be posted directly onto the ‘Shoutbox’ GAA Handball Ireland System on the gaahandball.ie homepage Croke Park Stadium, Dublin 3 Please refer to the Official National GAA handball website for all updates/rules: www.gaahandball.ie Please post all relevant GAA Handball scorecards to Email: [email protected] Croke Park Address as shown. Guthan 1: +353 (0) 1 8192383 Event: FOR REFEREEING: Turn card over each time so that player(s) serving are facing upright below. Player(s) Venue: Club/County/Province: Date: Time Outs: Game 1: 123 Game 2: 123 Referee: Game 3: 123 Serve: S 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 Start Time: S 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 S 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 Finish Time: Referee’s Checklist Serve: Time Outs: 1. After each rally the receiver has 10 seconds S 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 12 to assume position after which the server has 10 seconds to serve. S 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 12 2. -

The May Edition of the GAA Club Newsletter

Nuachtlitir na gClubanna - Bealtaine 2015 CONNECT WITH GAA Welcome to the May edition of the GAA Club Newsletter. Welcome to the May edition of the GAA Club Newsletter. We are now at the end of another great Allianz League with just the Division I hurling title left to play for this weekend. On the back of this we see our 2015 All-Ireland Championship campaigns open. You can track all stages of this exciting summer of games with our championship wall charts, available here. Over the next week our county stars will be meeting their supporters at the 2015 County Open Nights. A full list of County Open Nights can be found within this edition of the newsletter. At each of these nights there will be entertainment, meet and greets with players and management as well as giveaways. Tweet pictures from the Open Night to @officialGAA using #MeetYourHeroes for a chance to appear on GAA.ie. May also sees the much-anticipated launch of the GAA Club Website Solution. This solution offers clubs the chance to build a new website in minimal time and at a cost of just €100. This is an exciting opportunity for clubs who do not yet have a presence online as well as those looking to upgrade from Google sites. Full details are included in this newsletter. Lisa Clancy, Communications Director GAA CLUB WEBSITE SOLUTION The GAA Club Website solution is now available for clubs to use. It is a website template that offers clubs a user-friendly, simple and very affordable way to develop a club site.